The FTSE 100 saw one of the busiest days of the year for corporate results today, dipping 0.1% to 7,339.2 as Shell, Barclays, BAE Systems and ITV, among others, all reported.

Across the Atlantic, the US Federal Reserve hiked interest rates 0.75%, hitting the level expected by analysts for the last few weeks in a bid to fight soaring 9.1% inflation.

However, US Fed chairman Jerome Powell confirmed certain sectors of economic activity had started to soften, providing markets with hope that the coming interest rate decisions might show reason for optimism.

“On a super Thursday for corporate results the FTSE 100 made solid progress in early trading as the US Federal Reserve helped give global markets a boost overnight,” said AJ Bell investment director Russ Mould.

“It wasn’t so much what the Fed did, since a 75 basis point increase in rates was widely expected, as what it said in noting that some economic data had started to soften.”

“This gave investors at least a hint that it might start to ease its foot off the rate acceleration pedal a touch.”

The Dow Jones dipped 0.1% to 31,124, the S&P 500 fell 0.3% to 4,012.5 and the NASDAQ declined 0.7% to 12,530.5 in pre-open trading.

Anglo American

It was a busy day for the top companies on the FTSE 100, with Anglo American shares rising 3.2% to 2,864.2p after the mining giant beat market expectations despite its falling profits and revenues.

Anglo American revenues slid 17% to $18.1 billion in HY1 2022, with an EBITDA drop of 28% to $8.7 billion.

Additionally, the company slashed its dividend by a whopping 47%.

“Mining outfit Anglo American did better than expected. Although, like a high jumper in the early rounds of a competition, it was clearing a low bar as expectations had been successfully managed down by management ahead of time,” said Mould.

Schroders

Schroders shares gained 3.9% to 2,837p following a revenue climb to £1.4 billion, however its interim profits declined 16% to £312.8 million.

“Our returns from balance sheet activities were impacted with net losses on financial instruments and other income of GBP35.2 million,” said Schroders in a statement.

The firm attributed its falling profits to market movements related to the war in Ukraine and rising inflation levels.

The company maintained its dividend payment of 37p per share for the term.

Rentokil

Rentokil shares were up 2.8% to 517p after the firm announced a 7.8% pre-tax profit growth to £161.9 million, and an 8.1% revenue increase to £1.5 billion.

The hygiene group confirmed a HY1 dividend of 2.4p per share, representing a 15% rise year-on-year.

“As a global operation that benefits from highly defensive product and service lines, the company is well placed to navigate macro-economic and geopolitical volatility,” said Rentokil CEO Andy Ransom.

“In the first half, the topline has sustained strong momentum. We’ve been successful in proactively managing cost inflation through pricing to protect margin, while continuing to drive margin improvements through delivery on our strategy.”

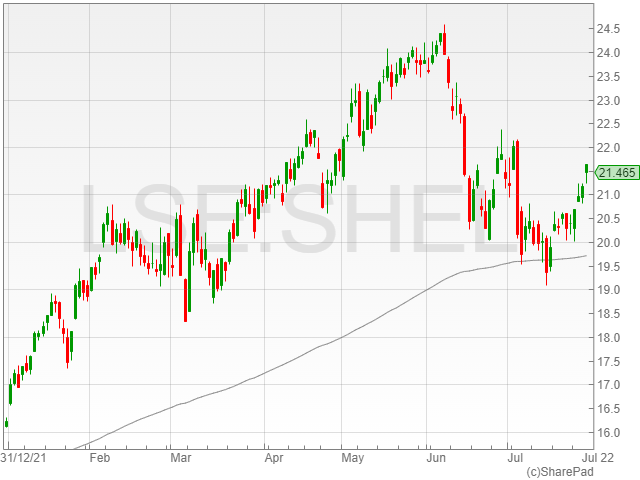

Shell

Shell shares gained 1.6% to 2,151.7p as the energy giant reported a shattering $11.5 billion profit in Q2 2022 against its $9.1 billion profit in Q1.

The oil and gas group announced a further $6 billion share buyback, scheduled for completion by Q3 2022.

“Shell’s accelerating its share buybacks after another quarter of bumper profit growth as the energy sector continues to ride high on the supply and demand imbalance caused by the crisis in Ukraine,” said Hargreaves Lansdown equity analyst Laura Hoy.

“Strong oil prices are driving Shell’s bumper performance and the group’s pledged to share more than 30% of the windfall with investors.”

Shell announced a Q2 dividend of 25c per share.

Smith and Nephew

Smith and Nephew shares tumbled 11.4% to 1,066.2p after an 8.5% fall in pre-tax profit to $204 million.

The company also cut its guidance, with an expected trading margin decline to 17.5% from 18.5%, as a result of the “prolonged impact of the inflationary environment and continued external supply challenges.”

Airtel Africa

Airtel Africa shares plummeted 8.8% to 155.8p on the back of economic headwinds in its Q1 results, as inflation pressures suppressed margin progress.

Revenue grew 13% to $1.2 billion, while its EBITDA rose 15% to $614 million and margins increasing to 48.8% from 48%.

“As we flagged in our full-year announcement, this quarter we have faced headwinds from outbound voice call barring for customers who had not yet registered their National Identification Numbers in Nigeria and the loss of site sharing revenue in those OpCos where we recently sold towers,” said Airtel Africa CEO Segun Ogunsanya.

“Inflation is also having an impact on our cost base, particularly on energy costs, but our continued efficiency drives have ensured that we have still been able to increase our margins, albeit at a slightly slower rate.”

“We continue to target growth ahead of the market this year and, despite inflationary pressures, our continued focus on cost efficiencies should also support margin resilience.”

Aveva

Aveva shares fell 6.5% to 2,177.5p in light of a revenue slide at a mid-single digit rate on the back of a decrease in upfront revenue recognition from perpetual licences.

However, the group’s outlook was positive, with a confirmed expected full year ARR climb of 15% due to strong end markets including energy, with a reliable sales pipeline for the remainder of the financial year.

BT

BT shares dropped 5% to 167.4p after a 10% slide in pre-tax profit to £482 million, on the back of increased depreciation offsetting EBITDA growth.

The telecommunications group reported a 1% uptick in revenue to £5.1 billion as a result of improved pricing and trading in its Consumer and Openreach segments.

“BT Group has made a good start to the year; we’re accelerating our network investments and performing well operationally,” said BT CEO Philip Jansen.

“Despite ongoing challenges in our enterprise businesses, we returned to revenue and Ebitda growth in the quarter.”

Centrica

Meanwhile, Centrica shares fell 3.2% to 88p on the back of a HY1 loss of £1.1 billion compared to a profit of £907 year-on-year.

However, the firm saw a revenue climb of 49% to £10.3 billion, which was offset by a 90% surge in the cost of sales to £9 billion from £4.7 billion.

The company issued a dividend payment of 1p per share for the interim term.

“We intend to retain our historic policy of paying roughly a third of the full year dividend as an interim,” said Centrica in a statement.

Barclays

Barclays shares declined 3% to 152.8p as the banking group missed profit expectations with a pre-tax profit of £3.7 billion in HY1.

The firm struggled with the legacy consequences of its over-issuance of US securities earlier this year, which ate £1.5 billion out of its income linked to rescission offer losses, alongside the associated monetary penalty from the SEC.

“Barclays’ numbers were scarred by further damage caused by the structured products debacle in the US,” said Mould.

“The market is pretty unforgiving of banks at the moment. Investors are wary of their exposure to a weakening economic backdrop, despite any benefit they might be getting from rising interest rates.”

“So the last thing banks can afford is self-inflicted damage of the kind Barclays is enduring.”

BAE Systems

BAE Systems shares dipped 1.3% to 771.4p on the back of its interim profits taking an impact from its ship repair business.

The company’s pre-tax profits declined 32% to £779 million, despite a 4.3% growth in revenue to £9.7 billion after the group’s ship repair sector’s profitability was dented by the Covid-19 pandemic.

However, BAE Systems confirmed an optimistic outlook and reiterated its positive FY guidance.

The firm issued a dividend of 10.4p for the HY1 financial period compared to 9.9p the year before.