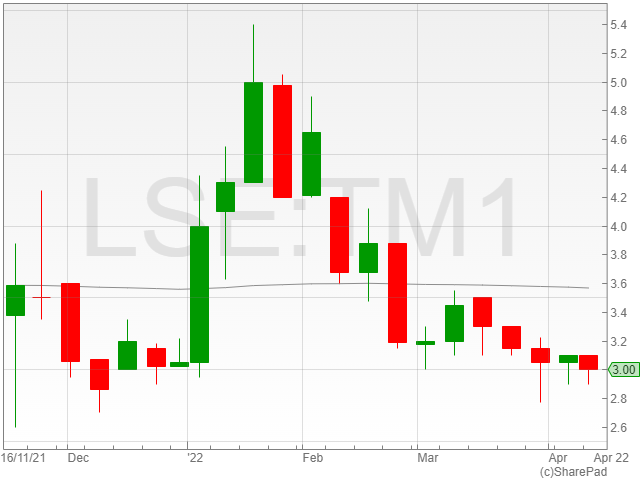

Technology Minerals reported a slate of advancements in its interim results for HY2 2022. The company’s shares were down 3.5% to 2.9p in early morning trading on Tuesday.

The firm has been listed on the London Stock Exchange (LSE) since November 2021, and currently aims to create a sustainable circular economy for battery metals across the UK.

Technology Minerals also noted its 49% owned firm Recyclus Group, which formed a partnership with Slicker Recycling Limited, and is set to see Slicker Recycling collect battery waste from around the UK and transport it to the nearest Recyclus plant.

The firm’s Recyclus achievements included the group’s first recycling site in Tipton, which opened in January 2022 and is set to provide national capability for lead-acid battery recycling.

The company added that Recyclus had opened the first laboratory suite at its new battery processing plant in Wolverhampton to conduct on-site testing for lead and lithium-ion battery recycling processes.

Technology Minerals celebrated its advancement in several ongoing projects, including a promising set of results from a sampling survey in its Oacoma Project, which reportedly confirmed the presence of manganese and rare earth oxides.

The firm confirmed that it had received a positive slate of initial results from due diligence sampling at its Asturmet Copper-Cobalt-Nickel Project in Asturias, Spain.

Technology Minerals also highlighted its acquisition of the Blackbird Creek Property in Idaho, US, which covers 1,285 hectares in the Idaho Cobalt Belt and potentially holds significant Copper-Cobalt deposits.

“It has been a great six months for the development of Technology Minerals,” said Stanbury.

“We successfully listed on the London Stock Exchange in November and raised capital to accelerate our development plans and pursue our growth strategy to create a circular economy for battery metals.”

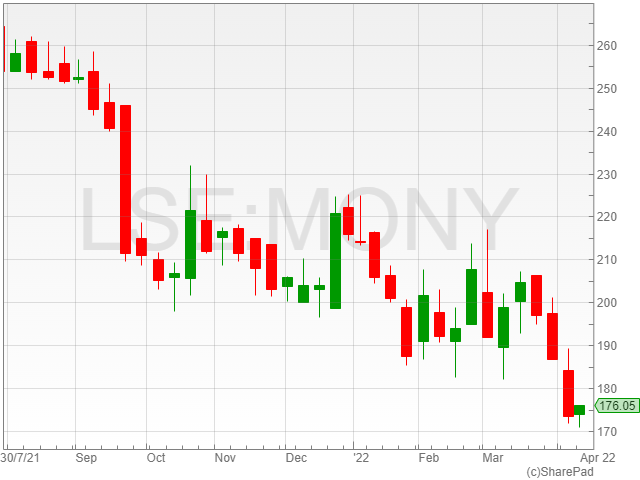

Moneysupermarket shares were up 1.9% to 175.9p in early morning trading on Tuesday after the insurance company announced an 8% growth in revenue in its Q1 2022 trading update.

The company reported a rise in revenue to £92.3 million from £85.5 million over the last quarter, with a particular rebound in travel insurance, which hit close to 2019 levels with £3.2 million compared to £400,000 in Q1 2021.

Moneysupermarket highlighted a high rate of retention across its customer base and noted the upcoming launch of its MSE multi-compare tool for car insurance scheduled for launch at the end of Q1 2022 to increase its presence in the market.

The firm celebrated a strong growth in money, which was led by a recovering in borrowing with a 37% increase to £24.8 million against £18.1 million in Q1 2021.

The company also noted an advancement in its banking division, which was reportedly driven by the wide reach of its promotional offers.

Moneysupermarket highlighted that its cashback trading benefited from the recovery in travel, however its regained ground was offset by lower volume in other channels.

The insurance group said that the factors affecting its market remained unchanged from those outlined in its February preliminary results, and that the Board currently anticipates full-year EBITDA to rise to 2020 levels, with its profit weighted in the second half.

“We are pleased with the strong recovery in Money and Travel, and continue to execute well against our strategy,” said Moneysupermarket CEO Peter Duffy.

“With cost-of-living increases adding pressure to consumer budgets, our distinctive brands remain well positioned to help households save money in a broad range of areas.”

Online electricals retailer Marks Electrical (LON: MRK) continues to gain market share in its core domestic appliance market, as well as new markets such as televisions. Marks Electrical has already invested in additional capacity so it can cope with much more growth over the coming years.

Full year revenues were 44% ahead at £80.5m and EBITDA margins are 9%. The fourth quarter revenues to March 2022 were 19% ahead at £20.7m. The comparatives are particularly strong because they were during a period of lockdowns when online sales made up a higher proportion of appliance sales.

There has been c...

Tortilla reported a transformational year on Mondaywith a 79.5% increase in revenue to a record £48.1m in 2021 compared to £26.8m in 2020 due to a strong performance across its venues as consumers begin to eat out again as restrictions ease.

In 2021, Tortilla saw an 80% increase in revenues after the Mexican fast-food chain reopened venues along with adding 7 new restaurants of which 3 were delivery-only despite 285 trading weeks being lost due to pandemic closures. The total number of venues for Tortilla is now 64.

LFL sales grew 23.8% compared to the pre-pandemic levels of 2019 for the group’s existing estates.

The group has launched new partnerships with Merlin Entertainments to open at Chessington World of Adventures and expanded its existing partnership with SSP to open two further sites at Gatwick Airport and Leeds Skelton Services.

Tortilla saw a pre-tax profit of £2.2m after seeing losses of £1.7m in 2020 as eases in restrictions helped the group’s profit bounce back.

The group’s adjusted EBITDA, pre-IFRS 16 increased 262.5% to £8.7m from £2.4m in 2020.

Tortilla’s business is highly cash generative, and benefits from a negative working capital cycle which helps fund new store openings from its capital. The group’s net debt position has been reversed from net debt of £2.3m in 2020 to net cash of £6.7m in 2021.

The group has a total revolving credit facility of £10m held with Santander out of which only £3m is drawn as of 2 January 2022.

For 2021, the board did not recommend a dividend and the capital generated at the moment will be used for the company’s growth.

Going into 2022, the company plans to open 7 more sites to sum up to 45 sites by the end of 2026 underpinning the board’s confidence. The group has already opened up 1 site in Q1 and one in April.

The momentum from 2021 has continued in 2022 and YTD LFL growth is 20.1%, in line with expectations for the group.

Tortilla is well-positioned to handle any macroeconomic pressures with strong support from the brand, value-for-money proposition and flexible operating model.

Richard Morris, CEO of Tortilla said, “Capping off a transformational year for Tortilla, we are very pleased to announce a record financial performance for the group’s maiden Annual Results following its successful IPO in October 2021.”

“During the year we made excellent progress in delivery of our long-term growth strategy. We opened further sites in line with our UK roll out plans, expanded our delivery kitchen estate to fulfil growing customer demand, and both extended and launched franchise partnerships which introduced the Tortilla brand to even more customers across the UK.”

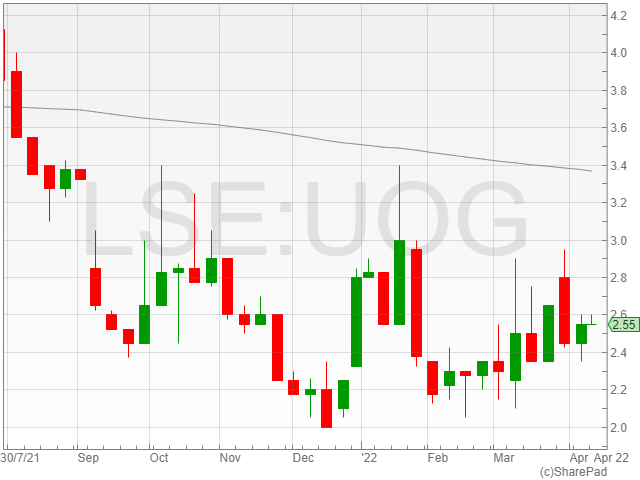

United Oil and Gas shares were up 1.9% to 2.6p in late afternoon trading on Monday after the company announced the sale of its UOG Italia Srl asset to PXOG Marshall Limited for €2,164,701.

The company noted that the UOG Italia Srl asset currently holds a 20% non-operated interest in the Podere Gallina licence, which also contains the Selva gas development project.

United confirmed that it received a completion payment of €2,190,966 which included the balance of the consideration, alongside a working capital adjustment from the effective date of €134,500 less the capital deposit of €108,235, which was reportedly received on 10 August last year.

The deal marks United’s exit from Italian operations, and the group will consequently no longer be liable for its share of the Selva gas development capital expenditure worth approximately €800,000.

United said that the finance from the agreement will be used to strengthen its balance sheet, which in combination with the higher oil prices, places the company in a strong position going forwards in 2022.

“We are pleased to have completed the sale of the Italian asset with our joint venture partner on the licence, Prospex Energy. The proceeds of this transaction along with other divestments strengthen our balance sheet to support our growth strategy,” said United CEO Brian Larkin.

“We have re-focused our portfolio on our core areas which provides us with a platform for organic growth and also a base from which we can evaluate further growth opportunities in 2022 and beyond. We wish Prospex Energy and all stakeholders of the Selva project well during its development”.

Harland & Wolff Group Holdings shares rose 2.8% to 22.3p in late afternoon trading on Monday following reports that the company won a contract from P&O cruises for dry docking two cruise vessels in Harland & Wolff’s Belfast dock.

“We are delighted to be able to have these two ships at a UK shipyard with such a long heritage and reputation and we very much look forward to supporting the UK maritime industry and working closely with the Harland & Wolff team on this project,” said Carnival UK vice-president maritime David Varty.

The contract reportedly marks another milestone for Harland & Wolff’s re-activation strategy across its key markets, which include its goal to operate in five markets and six service sectors in a bid to ensure project continuity, and to provide longevity for its key workforce, with the aim of providing an improved productivity and reduction in project costs for vessel owners.

The company famous for facilitating the construction of the RMS Titanic mentioned that the recent release of the National Shipbuilding Strategy would be a key factor to boost productivity levels at Harland & Wolff.

According to the group, the addition of 150 domestic vessels to be built in the coming years is set to kick the group’s projects up several notches into gear as it anticipates a fresh wave of projects.

“When acquiring the assets of Harland and Wolff (Belfast) in December 2019 and in a pre-pandemic period, the cruise industry was one of our key target markets,” said Harland & Wolff CEO John Wood.

“Our facilities are ideally placed to capitalise on these types of large projects whilst we continue servicing our smaller but regular clients.”

“We have now secured contracts in four out of our five markets; commercial, cruise & ferry, renewables and energy – we now hope to complete the final milestone of securing a defence contract in the near future.”

Following the recent contract renewal across NHS England for remote consultation services in secondary care, Induction Attend Anywhere contracts have been successfully extended or renewed across 94% of existing contracts, according to Induction, a leading digital health platform driving healthcare system transformation worldwide.

This is well over management’s estimates, and it went into effect on 1 April 2022.

As a result of the foregoing contract renewals, £6.6m in annual recurring income will be recorded in FY23.

Previously all contracts were for one year, the new contracts range in length from one to three years, with the majority committing to at least two years which amounts to a total contract value of £10.9 million.

Induction Healthcare transforms care delivery by delivering a portfolio of software solutions through a single integrated platform.

The company’s system-wide applications enable healthcare practitioners and managers to give care remotely as well as face-to-face, allowing communities to have a more flexible, efficient, and positive experience.

Hundreds of thousands of physicians and millions of patients across almost every hospital in the British Isles rely on its applications, which are used at scale by national and regional healthcare systems as well as non-health government organisations.

It allows patients to attend a medical appointment through video, which helps patients, healthcare providers and the healthcare system as a whole.

Following a successful national roll-out of AA in Scotland and regional trials in England, NHS England centrally contracted with Attend Anywhere in early 2020 to offer healthcare practitioners the option of remote consultations in secondary care for their patients.

The Covid-19 outbreak sprang out a few months later. Attend Anywhere’s rollout under lockdown conditions was one of the fastest in NHS history in terms of a single technology.

This centralised NHS England contract terminated in March 2021 and a series of competitive regional tenders were launched as anticipated.

To enable NHS Trusts to licence a platform of their choosing, central funding has been made available until March 31, 2022.

The directors believe that the NHS contract renewals announced today, which were completed in a highly competitive environment, represent a significant endorsement of the Induction Attend Anywhere solution and a clear justification for the claim to be the UK’s market-leading video consultation service used in secondary care.

Between March 2020 and March 2021, outpatient visits delivered by video utilising the Induction Attend Anywhere platform saved 4.64m hours of inpatient travel and wait times, as well as £40m in patient transport costs and parking charges throughout NHS England.

James Balmain, Chief Executive Officer, Induction Healthcare commented, “We are absolutely delighted by such a significant endorsement of the Induction Attend Anywhere video consultation solution.”

“When we acquired Attend Anywhere in June 2021, we knew that the change to regional procurement might present more of a challenge than national and were aware of the clear competitive pressure from global video conferencing providers, who’ve become household names during the pandemic.”

“It is a testament to the strength and quality of our offering, and to the speed of business integration, that we were in a position to open negotiations within months of the acquisition and complete this complex process within deadline.”

“The conversion rate for these renewals, and the fact that the majority have opted for multi-year contracts, shows that our purpose-built technology has not only become a trusted, long-term solution for secondary care in the UK, but one of the most widely used technologies to be rolled out as part of the digital transformation of the NHS.”

“This not only reinforces the significance of the acquisition but also the intrinsic value that Attend Anywhere brings to the group as part of an integrated and all-encompassing digital health platform.”

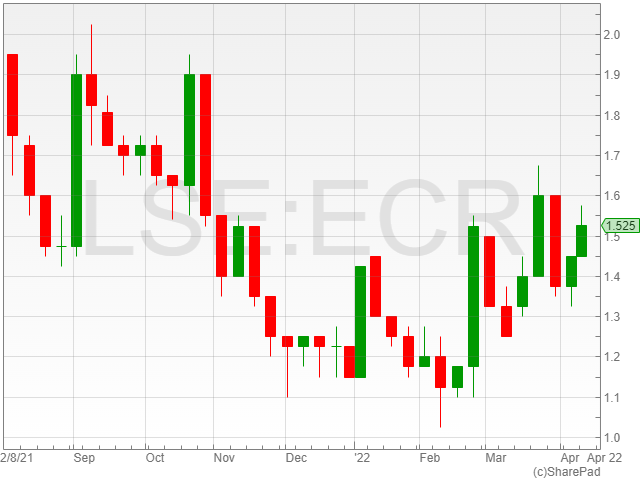

Haythorpe is reportedly scheduled to join the Australia-focused gold mining firm as a non-board CEO before taking on the position of executive director in six months time, pending shareholder approval.

ECR Minerals highlighted Haythorpe’s 30 years of experience in managing listed gold miners and explorers on the Australian Securities Exchange (ASX) and Toronto Stock Exchange (TSX), alongside his career as a mining analyst and hands-on gold exploration work as a geologist.

He is currently working as the managing director of GoldOz Limited.

“I am delighted ECR has attracted a CEO of Andrew’s calibre,” said ECR Minerals chairman David Tang.

“With more than 30 years of experience as a managing director and chairman of junior and mid-tier gold explorers and producers, he’ll be an exceptional addition to our team.”

His previous positions include managing director of Crescent Gold Limited, which spiked from a market capitalisation of $8 million to $250 million within four years under his leadership.

“Andrew built Crescent Gold from an $8 million explorer into a $250 million gold producer. He clearly sees the potential within the ECR portfolio,” said Tang.

He has further been listed as the 12th best gold analyst at Hartley Poynton over his tenure as an international leader in the industrial minerals sector.

Non-executive director Adam Jones added: I’m thrilled to welcome Andrew, a fellow geologist, to ECR.

“Being based initially in Australia he’ll be working closely with me and the field team in Victoria and Queensland, to ensure the exciting developments we are working on are progressed as quickly as possible. We look forward to providing more updates in due course.”

Sabien Technology Group shares were up 0.3% to 16.8p in early afternoon trading on Monday after the company announced a contract win for its Sabien Technology operating subsidiary worth £264,000 from an arm of the UK government.

The contract is reportedly for the extended deployment of Sabien Technology’s M2G Boiler Optimisation Technology across a selection of sites throughout the country in support of a major government project, and follows a previous contract awarded to the group for the use of its Boiler Optimisation products.

The contract comes as the second half of an initial order on 25 March 2022, which is scheduled for implementation through a different facilities managing partner.

The heating, cooling and transportation solutions company said that a minimum of £206,000 of the order will be recognised in FY 2022.

Sabien noted that its latest order increased the firm’s forward orders to 229 M2G Cloud devices to be installed, from which most of the revenue has either been invoiced or is set to be invoiced over 2022.

“This further contract award re-confirms the confidence placed in the M2G Cloud device by a major UK Government department,” said Sabien executive chairman Richard Parris.

“At times of rapidly increasing gas prices, Sabien Cloud delivers significant, easy to install savings, visible in real time through the intuitive M2G Cloud dashboard.”

The industrial laser systems business, 600 Group along with other group companies have completed the sale of the Machine Tool Solutions division, for cash consideration of $21m after the conditions have been met on Monday.

On March 7, 2022, 600 Group announced that it and other group companies had agreed to a conditional sale and purchase agreement with Timesavers Acquisition for the disposal of the entire issued share capital of each of 600 UK Limited, Colchester GmbH, 600 Machinery Australia and Clausing Industrial, which together comprise the group’s Machine Tool Solutions division, for cash consideration of $21m.

The group announced on Monday, that all of the remaining conditions for the sale have been met, and the transaction has been finalised.

The cash consideration of $21m has been received and the company now has a net cash position.

“The disposal of our Machine Tools division completes our strategic shift to the higher margin industrial laser system businesses which continue to deliver new customer wins and carry a record order book,” said Paul Dupee, Chairman of The 600 Group.

“With our net cash position, we now have additional resources and are well placed to capitalise on the opportunity in this highly attractive, yet fragmented, market through organic and inorganic growth strategies.”