The UK Investor Magazine Podcast was thrilled to welcome Stephen Crosher, CEO and Co-Founder of RheEnergise, for an exploration of hydro energy storage and RheEnergise’s innovative high-density solutions.

According to Stephen, 95% of the world’s power storage is facilitated by Pumped Hydro Storage, compared to just 2.5% storage using batteries.

RheEnergise is setting about the development of low-cost and globally scalable solution which will provide power storage solutions in a far shorter time-frame than alternatives.

We discuss the benefits and practicalities of hydro energy storage compared to batteries including how EVs will dominate lithium consumption, piling pressure on other forms of power storage.

Stephen provides fascinating insights on the global clean energy market including European government policy and possible scenarios for meeting climate change targets.

Anglo American shares tumbled 7.9% to 3,712.5p in late morning trading on Thursday, following a 10% drop in production over the quarter compared to the same period last year.

The mining giant blamed its lower production on high rates of Covid-19 absences, high rainfall impacting operations in South Africa and Brazil and a series of safety and operational hurdles at metallurgical coal and iron ore projects.

Anglo American confirmed a full cost guidance increase of 9%, reflecting a 4% knock-on effect from stronger producer currencies and 3% from inflationary pressures, especially diesel costs.

The group’s metallurgical coal production dropped by 32% as a result of a delayed longwall move and a fatal underground incident at Moranbah, with full-year guidance revised to 17-19 million tonnes, down from 20-22 million tonnes.

The firm also blamed the end of production at its Grasstree operation and the suspension of its Grosvenor and Aquila life-extension projects, which restarted operations in mid-February, as contributing factors to production decline.

Anglo American’s iron ore production decreased by 19% as a result of high rainfall and plant issues in Kumba and Minas-Rio, with full-year guidance scaled down to 60-64 million tonnes from 63-67 million tonnes.

The mining company also reported a 13% decrease in copper production due to planned lower grades, along with a 6% fall in metal in concentrate production from its Platinum Group Metals operation due to high rainfall in Mogalakwena, and reported a full-year guidance drop to 3.9-4.3 million ounces compared to 4.1-4.5 million ounces.

It wasn’t all bad news for the group, however, with a reported 25% increase in rough diamond production reflecting a high operational performance and lower rainfall impact, especially across its Botswana projects.

“This challenging start to the year highlights the importance of adhering to our Operating Model to stabilise performance after the necessary disruptions of the last two years as we adapted to – and now learn to live with – Covid,” said Anglo American CEO Mark Cutifani.

“As a result, we are updating our platinum group metals, iron ore and metallurgical coal volume guidance for the full year, and our unit cost guidance for most product groups to also reflect up to date exchange rates and the inflationary pressure on many input prices, particularly diesel.”

Ibstock released full-year results for 2021 in March 2022 which were reportedly strong. The momentum from those results has carried on to the Q1 trading update on Thursday for the group.

Ibstock noted in all of its end markets, demand is still strong. The group’s clay plant network is working well, with production volumes slightly ahead of its estimates and a full recovery of input cost inflation thanks to its innovative marketing approach.

Despite some ongoing supply chain problems, the Concrete division performed in line with expectations due to solid operational execution for Ibstock.

Ibstock saw significant input cost inflation, which continued to characterise the operating environment, particularly in energy, freight, carbon, and materials. In the case of energy, the company’s hedging technique has helped it to stay afloat in the face of rising prices.

Ibstock has now covered nearly all of its power needs for the first half of the year, over 75% of its requirements for the second half, and more than a third of its requirements for 2023.

Ibstock is dedicated to take the steps necessary to safeguard and maintain margins in the future.

“Brickmaker Ibstock is plagued by soaring input costs and ballooning energy bills, but the group appears to be coping well,” said Laura Hoy, Equity Analyst, Hargreaves Lansdown.

“A focus on increasing capacity and efficiency at its factories has allowed it to jump on booming post-pandemic demand. Rising raw material costs have passed on to consumers and energy hedges have offered some protection.”

“You can’t fault Ibstock’s deft management through an increasingly thorny environment. It’s no mean feat to beat expectations despite these challenges.”

The group’s growth plans are moving well, with the Atlas, Aldridge, and Nostell capital investment projects all on track, and Ibstock Futures has made significant progress in integrating the recently acquired glass-reinforced concrete (GRC) assets into its operations.

Ibstock outlined a defined route for growth and value formation over the following five years, based on a combination of investment within its core business and diverse growth possibilities, supported by a set of medium-term financial targets, at the time of its 2021 results announcement in March 2022.

Ibstock stated its intention to launch a share buyback programme of up to £30m as part of its rigorous approach to capital allocation and with estimated group leverage below the target range on Thursday.

The capital return is in addition to the £100m in committed growth investments, and the group expects strong financial capacity to sustain more growth investment and additional shareholder returns in the medium term beyond this repurchase programme.

Hoy added, “Efforts to shore up the balance sheet are also paying off—the group’s £30m buyback is evidence. This is in addition to investment in the group’s growth initiatives, including growth in Ibstock Futures, its sustainable construction arm.”

“This part of the business holds a great deal of promise in our eyes, and we look forward to seeing how its latest addition of glass reinforced concrete assets will fit into the existing business.”

AJ Bell shares were down 3.5% to 280.7p in early morning trading on Thursday after the company reported slowing rates of investor activity in Q1 as markets dipped and the impact of the pandemic began to fade.

The investing group said that the Q2 term in 2021 was comparatively stronger as a result of consumers investing excess savings built up over the Covid-19 lockdown period.

However, the upheaval caused by surging inflation and increased market uncertainty left the firm with a weaker Q2 in 2022 as investors became less risk-happy in light of Russia’s war in Ukraine and the skyrocketing cost of living.

AJ Bell still reported decent numbers, with a total customer increase of 21% to 418,309 over the past year and a 5% uptick in Q2, bringing in total net inflows of £1.5 billion over the period.

The group pointed out that the FTSE All-Share index fell by 0.5% and the MSCI World Index fell by 5.5% during the poorly-performing term.

The investment platform noted additional highlights, with over 75% of new accounts listed as tax-advantaged pensions or ISAs, and a customer retention rate at 95%.

AJ Bell reported a slight fall in gross inflows to £2.7 billion compared to £2.8 billion in Q2 2021, and a net inflows drop to £1.6 billion against £1.8 billion.

The group confirmed a et inflows decline to £223 million over Q2 2022 compared to £311 million in Q2 2021.

“Although our D2C customers invested slightly less via our platform than in the comparative period as they assess the impact of the rising cost of living, net inflows to our advised platform remained on par with last year, which was a strong comparative. Net platform inflows of £1.6 billion is an encouraging result given the uncertain market backdrop,” said AJ Bell CEO Andy Bell.

“Our first five multi-asset funds recently passed their fifth anniversary, an important performance milestone particularly for advisers. Performance of all five funds was in the top 30% when compared against their peer groups, with four being in the top quintile.”

“Since launching these funds in 2017 we have shared the benefits of our increasing scale with customers, reducing the Ongoing Charges Figure from 50bps to 31bps during that time.”

The company also announced the launch of its new Dodl by AJ Bell investing app, which is set to expand the platform’s offerings to DIY investors with all the central tax wrappers and a streamlined investment range to help consumers pick funds and shares for their portfolios.

“This week we launched a new investing app called Dodl by AJ Bell which expands our offering to DIY investors. With an annual charge of just 0.15% and no commission for buying or selling investments, Dodl is a low-cost proposition perfectly suited to individuals who want an easy way to invest for their future,” said Bell.

“We believe it will be particularly attractive to the 8.6m adults in the UK who hold more than £10,000 of investible assets in cash, especially in the current climate of rising inflation where cash savings are being eroded in real terms due to the low interest rates available.”

In Rentokil’s Growth and Emerging markets, ongoing revenue increased by 10.9% and 13.6%, respectively.

North America Pest Management, is Rentokil’s largest pest control company and has continued to grow at a healthy pace. The company [North America Pest Management] is increasing organic revenue by over 5% as it is driven by increased revenue from both residential and commercial customers.

Despite the ongoing impact of the pandemic in a number of countries, Hygiene & Wellbeing expanded organically by 12.9% which indicated growth in all areas, including Asia for Rentokil.

Trading conditions in Rentokil’s France Workwear division improved further in Q1 2022, resulting in 14.7% organic growth.

Rentokil’s group ongoing revenue increased by 12.3%, excluding disinfection, with 8.0% organic growth and 4.3% through acquisitions. The group’s organic growth was -2.0% including disinfection.

Rentokil expects robust disinfection revenues of £95.3m in H1 2022, as the group disclosed in its preliminary findings in March.

Rentokil forecasts its disinfection revenues to be in the range of £10m to £20m for the full year of 2022, compared to £116m last year.

In Q1, Rentokil faced inflationary increases in its cost base, such as labour, fuel, consumables, and paper. The group has continued to successfully minimise the impact of these on margins by annual price increases (APIs).

In the first quarter, total price increases completely offset input cost inflation, and Rentokil remained confident that it will be able to continue to use APIs to combat rising pricing throughout the year.

The group’s customer retention was strong in the first quarter, at 85.3%, which was consistent with the full year of 2021.

Colleague retention on a rolling 12-month basis was similar, with service colleague retention at 81.8%, equivalent to the full year of 2021, and sales colleague retention at 83.5% which increased marginally from 2021 for Rentokil.

In Q1, Rentokil acquired 11 firms in Chile, Colombia, Hong Kong, Poland, Malaysia, New Zealand, and the United States, with total annualised revenues of £20m in the year before the purchases.

The company said it will continue to build on the strength of its M&A pipeline in both Pest Control and Hygiene & Wellbeing. Rentokil remainS confident in its target expenditure of roughly £250m for 2022 on M&A.

Rentokil said the appropriate waiting period under the Hart-Scott-Rodino Antitrust Improvements Act of 1976 expired on March 15, completing the antitrust proceedings in the United States.

Rentokil added that obtaining shareholder approval from the company and Terminix, as well as the registration of the company ADSs with the US SEC and their listing on the NYSE, are all prerequisites that must be met.

Both parties are on track to complete the transaction in the second half of 2022, with a target completion date at the end of the third quarter which is owed to solid work on the remaining requirements.

As a consequence of organic growth and revenue flow through from our M&A programme in 2021, the business is operating well and in line with our expectations.

Despite record disinfection revenues in H1 and persistent macroeconomic uncertainties, Rentokil continues to expect the group to make good operational and financial improvements in the second half of 2022.

Rentokil has no activities or exposure in Russia or Ukraine, and has been unaffected by the conflict there.

During the quarter, Rentokil donated £100,000 to UNICEF from the Rentokil Initial Cares charity fund, which is assisting children and families displaced across Ukraine and neighbouring countries with crucial services including as water and sanitation, vaccination, and healthcare.

Segro shares were up 0.5% to 1,373.5p in early morning trading on Thursday, following a £7 million boost over Q1 2022 in total headline rent to £25 million from £18 million in Q1 2021.

The properties firm reported a fall in vacancy rate to 3.3% from 4.4%, and a rise in uplift on rent reviews and renewals to 23% from 12%.

However the company’s customer retention rate dipped slightly to 79% from 82% over the same term last year.

Segro commented that its capital investment continued to focus on asset development and acquisition with future growth potential, alongside its aim to source assets with short-term income and development opportunities to extend the firm’s development pipeline.

“Our business has had a strong start to the year with continued demand from a broad range of customers enabling us to capture further rental growth through rent reviews and the re-letting of space,” said Segro CEO David Sleath.

“We have significantly increased our largely pre-let development pipeline and have secured future opportunities for growth in some of our most supply-constrained urban markets through the acquisition of land, as well as income-producing assets with medium-term redevelopment potential.”

The company reported a development capex rise to £151 million in Q1 2022 from £143 million in the same period last year, and an acquisitions cost of £175 million against £37 million.

Segro further noted 1.4 million square metres of space which is currently under development, representing £108 million in new rent prospects.

The group also mentioned a net debt of £4.4 billion against £4.2 billion in Q1 2021, with its issuance of €1.15 billion in Green bonds over Q1 2022 at a blended coupon of 1.5% helping to strengthen the firm’s balance sheet and keep to a low average cost of debt.

“There have been no direct effects of the invasion on our business, however it has added to construction supply chain and inflationary pressures and we are working closely with our construction partners so as to minimise the impact on our development programme,” said Sleath.

“At the same time, we expect these pressures will further tighten the supply-demand imbalance for industrial assets and place further upward pressure on rents across our portfolio.”

“The industrial sector continues to benefit from highly supportive and long-term structural tailwinds, which are leading to sustained strong occupier and investor demand, despite the challenges that the world is facing. We are alert to ongoing geopolitical and macro-economic risks but remain confident in the outlook for our business in 2022 and beyond.”

Aerospace, defence and energy company, Meggitt announced a trading update for the first quarter of 2022, where the company noted a 116% rise in civil orders on Thursday.

Meggitt recorded original equipment up 54% and aftermarket up 176%, including a good performance from braking systems across large, regional, and business aircraft in Q1 2022.

The group’s civil order intake in the quarter was up 116%, highlighting the civil segment’s recovery but still weak compared to Q1 2021.

Meggitt noted a book-to-bill ratio of 1.38x near the end of the quarter, which was higher than 1.02x at the end of 2021.

On an organic basis, Meggitt’s group revenue increased 5% in the first quarter of 2022 compared to Q1 2021, indicating the upward trajectory in civil aircraft and growth in energy. However, group revenue remained 23% below pre-pandemic times.

Meggitt’s revenue increased by 25% in civil aerospace, with original equipment and aftermarket revenue increasing by 11% and 37%, respectively.

The regional jet revenue increased by 65%, while big and business jet income increased by 40% and 13%, respectively, in the civil aftermarket for Meggitt.

The effects of inventory destocking and weaker orders from the US Defense Logistics Agency in the aftermarket contributed to a 16% drop in defence income compared to Q1 2021 for the group.

Meggitt’s energy revenue increased by 27%, with its Heatric division seeing particularly strong growth.

Meggitt said the European Commission approved Parker-proposed Hannifin’s acquisition on April 11, 2022, subject to full compliance with Parker’s undertakings, including the disposal of Parker’s Aircraft Wheel and Brake division. The deal is still on track to close in the third quarter of 2022.

Outlook

Meggitt is not offering financial guidance for 2022, as previously stated since the group is in an offer phase under the UK Takeover Code and is unable to comment on projected performance in comparison to any analyst projections that may be available.

Credit Suisse Group expects to see losses in the first quarter of 2022 as a result of increased legal provisions, slower commercial activity, and the consequences of Russia’s invasion of Ukraine announced the Swiss bank on Wednesday.

The bank is still recovering from billions in losses in 2021, which led to a top-level management shake-up, and it is facing new compliance and risk-related investigations.

Provisions for a variety of previously announced legal matters, many of which date back more than a decade, will climb by over 600m Swiss francs to total around 700m francs, according to Credit Suisse.

Last month, a Bermuda court found that Georgia’s former prime minister and his family were owed “substantially in excess of $500 million” in damages from Credit Suisse’s local life insurance unit owing to fraud.

The impact of Russia’s invasion of Ukraine would have a negative impact on results of 200m francs in negative revenue and reserves for credit losses.

According to Credit Suisse, the first-quarter results will include previously disclosed losses of roughly 350m francs related to a drop in the value of its 8.6% stake in Allfunds Group.

It stated that weaker business activity and a decrease in capital market issuances had harmed the underlying earnings.

These losses would be somewhat offset by a recovery of roughly 170m francs in reserves for claims against the bankrupt investment fund Archegos, as well as real estate gains of around 160m francs, according to the company.

In earnings due on April 27, it said the group “would expect to report a loss as a consequence of this increase in reserves,” without being more specific.

Credit Suisse shares fell 1.7% to CHF 7.17 after forecasting losses in Q1 2022.

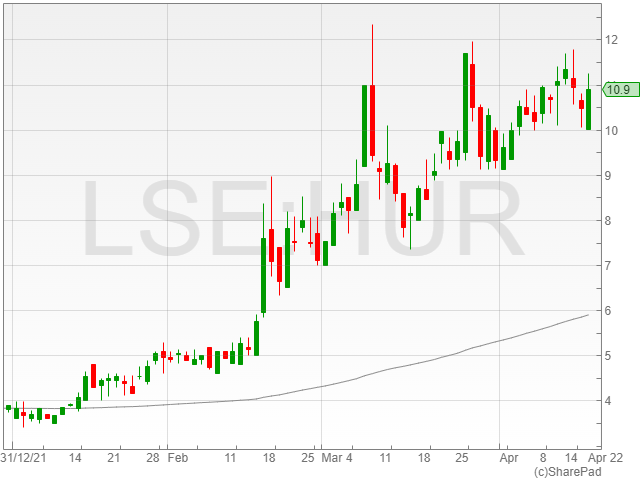

Hurricane Energy shares were up 3.2% to 10.8p in early afternoon trading on Wednesday after the company released the latest update for its Lancaster field operations from March, highlighting a free cash balance of $106 million compared to $71 million at the close of February.

Hurricane Energy said that its Lancaster operation was producing 9,150 barrels of oil per day from its P6 well alone, with an associated water cut of 43%.

The group’s 28th cargo of Lancaster oil was lifted on 22 March and totalled 524,000 barrels.

According to the company, the cargo was priced by reference to the average of the past five days of the dated Brent crude quotes for March at $116 per barrel, with the net revenue reportedly coming in at $60.5 million and the next shipment scheduled for departure in late May this year.

The firm noted a net movement of $9.4 million from free cash into restricted funds, following the energy firm’s agreement of the Aoka Mizu FPSO Bareboat Charter extension on 25 March.

Hurricane Energy mentioned that $78.5 million in Convertible Bonds remained outstanding, and are due in July this year.

The group commented that net free cash provides a helpful measure of liquidity once it has settled its immediate creditors and accruals, alongside recovering amounts due and accrued from joint operation activities and outstanding amounts from crude oil sales.

Hurricane Energy confirmed that the net free cash does not take into account future liabilities which the firm has committed to, but have not yet been accrued, meaning that not all of the net free cash will be available for repayment of the leftover outstanding Convertible Bonds once they reach maturity in July.

Hikma Pharmaceuticals, a multinational pharmaceutical company, announced on Wednesday that it has received preliminary approval from the US Federal Trade Commission (FTC).

The company will now work to complete its previously announced acquisition of Custopharm from Water Street Healthcare Partners on September 27, 2021.

The parties have now received all necessary regulatory approvals to complete the deal. Hikma will make another announcement after the transaction is completed.