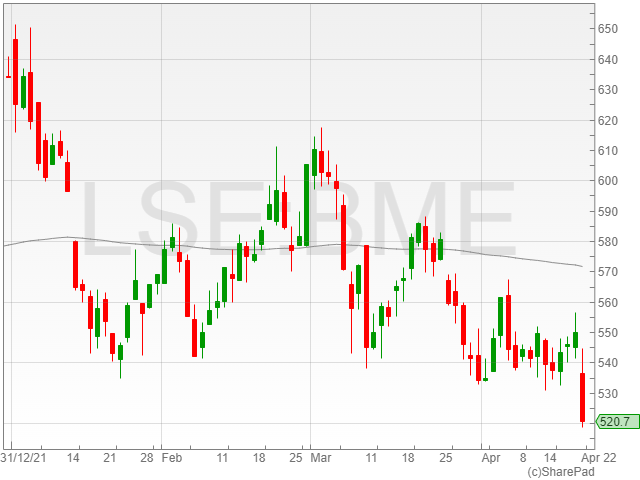

B&M shares were down 6% to 516.8p in early morning trading on Friday, following the announcement that Chief Executive Officer Simon Arora would be stepping down after over 17 years in the position.

The company said that Arora is scheduled to leave the role in 12 months, and will remain at the group over the coming year to facilitate a smooth transition over to his successor.

Chairman Peter Bamford is set to lead a succession process to consider internal and external candidates to replace Arora as Chief Executive.

“On behalf of the Board and all stakeholders of the Group, I would like to thank Simon for his leadership over the past seventeen years,” said chairman Peter Bamford.

“The remarkable growth of the business from its humble beginnings to where it is today reflects his exceptional passion, determination and ability.”

“Moreover, he has established a firm foundation from which the Group will continue to deliver its successful growth strategy and great value for its customers. We are all very grateful for his tireless efforts and he will leave us next year with our best wishes for the future.”

Simon Arora acquired the B&M franchise in 2004 with his brother, Bobby Arora, when the group consisted of only 21 stores.

The two brothers have since developed the company into a portfolio of 1,100 locations and gained a spot on the FTSE 100 index.

Bobby Arora has confirmed that he will remain in his role at the business as Group Trading Director after Simon retires.

“It has been a privilege to lead B&M for seventeen years and I am immensely proud of the incredible journey that we have been on,” said Simon Arora.

“B&M’s value for money proposition remains as relevant and compelling to shoppers today as it has ever been.”

“I would like to thank all 38,000 members of the B&M family for their hard work and commitment both now and as we continue our expansion.”

The XP Factory has made great progress, including completing the Boom integration, growing its UK base, and expanding the site pipeline.

The Boom estate consisted of one owner-operated site and six franchise sites when it was purchased in November 2021 by XP Factory.

There are currently 11 operating sites, consisting of 2 owner-operated and 9 franchised locations, with a further 10 sites currently under construction and set to launch in the following months. Seven out of the 10 sites are nearing or have completed construction said XP Factory.

The expanded estate of 21 locations will include 6 owner-operated and 15 franchised locations once it opens. According to XP Factory, more sites are nearing completion, and construction is slated to begin this summer and into the fall.

XP Factory’s progress thus far suggests that the board’s goal of 27 open Boom venues by the end of 2022 will be easily achieved.

The board’s box-economics projections for both sales and profitability are being validated by trading performance across both owner-operated and franchised locations.

XP Factory’s monthly operating leverage is increasing in line with the board’s planned maturity profile.

Boom and Escape Hunt will open co-located locations in Exeter, Edinburgh, and Oxford Street soon. The XP Factory group has been reinforced following the plans for 2022 and is increasing capacity for the upcoming rollout.

More information will be available in the XP Factory’s audited final results for the fiscal year ending December 31, 2021, which are expected to be disclosed in late May 2022 and will reflect performance in line with the company’s trading update made on January 26, 2022.

“We are delighted at how well Boom Battle Bar has been integrated into the group. It has been an extremely busy period for site development and we have an exciting run of openings in the coming weeks and months which position us well to deliver on our estate targets for the end of the year,” said Richard Harpham, CEO of XP Factory.

“The recent performances from our new Boom sites have validated our expectations for the site level profitability we believe is achievable. In addition, Escape Hunt performance has exceeded expectations for Q1, giving us confidence for the execution of our strategy as a whole.”

LXi REIT has exchanged contracts on the sale of its property in Saffron Walden, which was let to Premier Inn, B&M, Pure Gym, Pets at Home, and Costa, for £19.33m, with a 4.45% net exit yield, after receiving an unsolicited offer from a UK pension fund.

The property was purchased for £15.8m and a 5.72% net initial yield through a forward funding deal.

The sale generates an attractive 19% per annum IRR for the company and the property was listed for sale at the time of the latest valuation.

LXi REIT Acquistion

Marks & Spencer Food Store

Marks & Spencer is a FTSE 250 company with a market capitalization of around £3bn.

A pre-let forward funding arrangement is being used to acquire the food store in Largs, North Ayrshire by LXi REIT.

The 13,450 sq ft property has been fully pre-let to Marks & Spencer on a fresh, unbroken 15-year lease with five annual rental increases at a fixed growth rate of 2.5% compounded.

MKM Trade Unit

MKM is the largest independent builders’ merchant in the United Kingdom.

The MKM trade unit, which covers 15,250sqft, was built this year and is entirely leased to MKM Building Supplies on a long lease with 20 years remaining until the first break.

The rent is increased every five years under RPI inflation, which is capped at 3.5% per year and collared at 1.5% per year.

Both acquisitions have good ESG credentials, with the MKM unit having an EPC “A” rating and rooftop solar panelling, and the M&S Simply Food expansion aiming for an EPC “A” rating as well.

The remaining funds from the sale will be put into the LXi REIT’s accretive pipeline.

LXi REIT shares fell 0.07% to 150.6p in early morning trade on Friday after the company updated investors on its property portfolio.

Jangada Mines shares plummeted 23.4% to a closing price of 7.8p in Thursday trading following the updated technical report for its Pitombeiras Vanadium Project.

Shares fell after the company said the project now had $96.5 million post-tax Net Present Value (NPV) and 100.3% post-tax Internal Rate of Return (IRR).

This marked a downward revision in the projects economics from a report last year that pointed to a $106.5 million NPV and 317% IRR.

However, the company confirmed in its updated technical report that it had received the green light on all legal, technical and geological fronts, noting no additional impediments to the development and production of its Brazil mine.

Resources

Jangada Mines said that it currently expects high levels of Ferrovandium concentrate (Fe 62%) and Titanium Dioxide (TiO2) from its Pitombeiras Vanadium Brazilian project.

The company noted a particular interest in extracting TiO2 due to its accelerated rate of use in the booming green energy market, especially in lithium batteries used in electric vehicles across the green transport industry.

“We are witnessing an increase in focus on commodities that broadly fit the emerging energy and battery space,” said Jangada Mining executive chairman Brian McMaster.

“Given this, we have gone back and optimised the development route at Pitombeiras to include the 9.85% TiO2 component alongside the Fe 62% and V2O5 to obtain a clearer picture of the Project’s potential.”

The firm said that it anticipated an annual production of 186,000 tonnes of Fe 62% and 66,000 tonnes of TiO2 at a production/processing rate of 600,000 tonnes per year.

The group also commented that it expects a Life of Mine (LoM) extraction of resources at 5.1 million tonnes of measured and indicated material, with 3.1 million tonnes in inferred resources.

“[Given] our extensive in-country contacts and positioning, we are continuously seeing additional projects and regularly review opportunities, particularly in the technology metal space, that may complement our existing asset suite and create further value for shareholders,” said McMaster.

“We look forward to updating the market further as we complete the on-going Feasibility Study including the titanium.”

THG reported its annual earnings today and announced that it is receiving “numerous” takeover proposals over the last few weeks. The good start to 2022 has helped the E-commerce retailer’s shares gain 15% to 108p on Thursday after seeing a 50% decrease in share price YTD.

THG debuted on the London Stock Exchange in September 2020. Since then, the organisation’s life as a publicly-traded company has not been easy.

The shares were priced at 500p each when they went on the market. The stock was up 15% to 108p each on Thursday, meaning shares are trading down over 80% from the IPO price.

THG Share movement for the last 6 months

In October of 2021, a capital markets day intended to boost investor confidence instead scared traders. THG shares have been under selling pressure since then.

In October, Moulding, the company’s founder and CEO, stated that he will surrender his so-called ‘golden share,’ resolving a corporate governance issue that has been bothering investors and allowing the company to join the FTSE indices. The decision was made “in furtherance of good corporate governance”.

For three years, Moulding could use the stake to veto any takeover bid. Investors dislike it, and it prevents THG from joining the FTSE 100 or FTSE 250 indices.

“We continue to focus on delivering our exciting growth strategy across a number of large global sectors, and prepare to step up to the premium segment of the LSE at the appropriate time,” said Chief Executive Matthew Moulding.

THG Takeover Proposals

THG has reportedly rejected all takeover proposals it has received in recent weeks due to the company believing the bids did not reflect the full value of the firm. The company confirmed that it is “not currently in receipt of any approaches”.

THG FY ’21 Results and Q1 ’22 Trading Update

During the first quarter of 2022, THG saw “very encouraging” consumer demand compared to a challenging period during the lockdowns in 2021, resulting in Q2 beginning in line with expectations.

THG’s revenue in the first quarter of 2022 increased 16% to £520.2m compared to 2021. The company expects revenue growth to be between 22%-25% at constant currency, however, THG faced a 1% hit from Russia and Ukraine.

The company continues to have similar growth expectations in its adjusted earnings before interest, tax, depreciation and amortisation.

THG’s adjusted EBITDA is estimated to stay around £161.3m in 2021, a 7% increase from £150.8m in 2020. The group’s adjusted EBITDA margin fell to 7.4% in 2021 from 9.3%. Recent increases in inflationary pressure, according to THG, are “transitory in character.”

“The near-term environment has evolved significantly since January due to a number of global factors including the war in Ukraine, Covid-19 related lockdowns in Asia, and inflationary pressure across almost all cost lines,” said the company.

“Given the continually evolving external considerations, the board anticipates FY 2022 adjusted Ebitda to be broadly in line with FY 2021, with a weighting to H2 2022.”

CEO Moulding stated, “In our first full year as a public company, 2021 saw us scale revenue and expand our business model, well ahead of targets set at IPO.”

An Interview with Stephen Crosher, CEO of RheEnergise

Energy storage is set to be a trillion-dollar market, could you explain why?

Governments across the world have recognised the urgency to completely decarbonise over the next 30 years. The recent invasion of Ukraine has amplified the pressing issue of energy security.

To decarbonise, countries must redesign their power systems, switching from coal, oil and gas to renewables. Renewable power is generally more distributed, more local but it is intermittent. Energy storage is the solution to intermittency and will help keep power grids stable and reliable.

Industry experts across the world, including Bloomberg New Energy Finance, IRENA, The Long Duration Energy Storage Council, McKinsey, Jacobs, Accademia, and many others have predicted this trillion-dollar market.

Malcolm Turnbull, a former Australian Prime Minister said at the World Hydro Power conference last year “When we talk about the transition to a zero-emission energy system, we often overlook the crisis within the crisis, and that is long duration storage”

To put the scale of the challenge into perspective, the world needs in the order of 2,000GW of energy storage or at least ten times the current amount available. Batteries, despite their recent growth, still make up a tiny proportion.

Most people think of batteries when they think of energy storage, can you explain how your High-Density Hydro® solution works and why is it better?

Batteries are an ideal solution for shorter durations of energy storage (2-3 hours) and are good at providing ancillary services such as frequency response. However, with batteries, for every MW of power one purchases, one gets a MWh of storage i.e. the storage lasts for 1 hour. This means that to get lots of MWhs, or long durations of storage, project sizes and costs increase.

Our solution at RheEnergise is different because the power component is decoupled from the storage component. The power is defined by the size of the pipes from the top to the bottom of the hill and the size of the turbines, whilst the energy or duration is defined by the size of the storage tanks and fluid volume. This means that one can set the power one requires and set the duration without oversizing any part of the project.

The lowest cost form of energy storage, for long durations, by far is pumped hydro. It is a very mature technology that has been around for over 100 years. What RheEnergise achieves with its High-Density Hydro® is the same low cost of storage as traditional pumped hydro, but it creates vastly more siting opportunities for projects. This is because HD Hydro uses a fluid that is 2.5 times the density of water (about the density of concrete). With High-Density Hydro® the same performance can be achieved on small hills rather than mountains, when compared to projects using water. This means that there are hundreds of thousands of sites available across the world and sites are close to where they are needed.

To summarise, High Density Hydro presents the ultra-low costs of storage associated with pumped hydro, while dramatically increasing the number of sites available and it also speeds up construction times, so that projects are built in the same sort of time scales as other energy projects – wind, solar, batteries etc.

The UK government has announced its decarbonisation and energy resilience strategy in recent days, does it go far enough?

The short answer is No. Solutions need to be scalable and deployed quickly in the next 20 years. We need solutions that progressively deliver results and lower carbon emissions. Belching out the same level of giga-tonnes of CO2 for 30 years is not a good solution.

One of RheEnergise’s decision making strategies is to always ask whether our solution can deliver at scale, fast. High-Density Hydro can achieve this scaling because our supply chain already exists, companies make pipes and pumps and turbines. Plus, they can make them to our specification for HD Projects.

The German Government, like other European Governments, has also brought forward their decarbonisation plans by 10 years, specifically to get off Russian gas, oil and coal rapidly, how are they all going to achieve it?

How is central Europe including Germany going to get off Russian gas in 13 years? I have absolutely no idea, but what is abundantly clear, is that in addition to rolling out more renewable energy systems and rebuilding large parts of their power grid, they will need to have an aggressive programme of long duration energy storage to manage the energy flows, manage the intermittency and to create a stable power grid from the renewable energy generated. RheEnergise can certainly be a major player in providing the solution.

You are currently submitting your first planning permission in the UK; can you explain the barriers you are experiencing?

Remarkably few to be honest. We have questions about flora and fauna where we are building, ensuring habitat is preserved and that there is a habitat gain. We also receive questions about how we mitigate and manage any spills, in the unlikely event that they happen, and lastly the visual impact of the project. This is relatively easy to resolve as we plan to bury the pipes and screen the landscape.

You are in the final week of what appears to be a very successful fundraising campaign on CrowdCube, what you’re using the capital from the funding campaign for?

We have several objectives over the next year, specifically to increase the commercial side of the business seeking early customers and key partnerships. We plan to continue to develop our engineering capabilities across key areas of engineering in particular our ability to process fluids at scale and the continued development of mechanical systems such as HD Hydro specific pumps, turbines, and valves.

Where are you targeting as your first markets?

Energy markets across the world are transitioning. Australia is interesting as they have prenominal renewable energy resources and a power grid that already has challenges. Parts of the US could really do with our solution – California, New York, Texas, and Mexico have so many suitable project sites, as do places like Turkey or Saudi-Arabia. There is of course, as mentioned before, the whole of central Europe.

Early customers might be large energy consumers with 24/7 power demands, such as mines and quarries, that wish to both manage their energy costs and decarbonise.

Our challenge is actually very little to do with which market, but how to move fast enough to address the growing opportunities that exist across the world.

Card Factory announced earlier on Thursday that it has successfully completed a refinancing which removed a commitment to raise funds, leading to the 28% jump in the UK’s largest specialised retailer of greeting cards’ shares to 57p.

Card Factory YTD Shares Movement

Card Factory has reached an agreement with its current banking syndicate on refinancing conditions. The company has made considerable progress in reducing overall debt by utilising its positive cash flows.

Card Factory’s group net debt excluding lease liabilities was £79m as of 31 March 2022.

The conditions of the revised facility for Card Factory also entail an £11.25m term loan facility that will be repaid between January 31, 2023, and January 31, 2024, and an £18.75m term loan facility that will be repaid in six £1.75 million quarterly instalments starting in April 2024 and ending with a final repayment of the balance amount in September 2025

As a result, revised agreements on decreased facilities of £150m which was originally £225m, have been reached by the company. Card Factory will cut its government-backed Coronavirus Large Business Interruption Loan Scheme (CLBILS) component from £50m to £20m because of the revised agreements which are due for repayment in September 2023.

Dividend restrictions will remain in place until the CLBILS facilities and the GBP11.25m term loan are paid off, which is due in January 2024, if the leverage ratio stays below 1.5 times.

The revised facilities have withdrawn Card Factory’s best efforts commitment to its banks to obtain net equity proceeds of £70 million by 30 July 2022. The Board has no plans to complete an equity raising at this time said the company.

Darcy Willson-Rymer, Card Factory CEO said, “I am pleased to be able to announce the successful completion of Card Factory’s refinancing today.”

“This is an important milestone for our business, ensuring we have the financial foundations in place to capitalise on the opportunities ahead.”

“We are now well positioned to continue our strategic transition from a store-led card retailer to a market leading omnichannel retailer of cards and gifts. I look forward to updating you on our progress at our full year results next month.”

The UK Government’s green energy proposal released earlier in April caused a great deal of excitement across the market, with investors gearing up for the potential change in the energy landscape laid out in the administration’s ambitious plans.

However, the weighty proposal has come under scrutiny due to a perceived oversight of the wind energy sector. Scientists have pointed out that the Government has not yet taken advantage of the level of power which the country is capable of generating for consumers, adequately capable of meeting household electricity needs.

Experts have also pointed out that the UK appears to have accelerated its investment in nuclear power, which is a far lengthier and more expensive process than its breezy counterpart for energy production requirements.

So, what exactly is going on behind the scenes, and are we actually overlooking a far easier, more cost-friendly option to power the UK to the detriment of consumers?

The Benefits of Wind Power

Despite the comments from Transport Secretary Grant Shapps that wind turbines are an “eyesore” to behold, the renewable energy alternative has been backed by scientists as the possible saviour of UK power.

According to a study from researchers at the University of Sussex and Aarhus University in Denmark, onshore wind turbines have the capacity to match 140% of the UK and Ireland’s energy demand if wind farms were established on prime territory for the maximisation of energy potential.

“Our study revealed that the UK and Ireland had the potential to generate 2,150 TWh of energy from onshore wind, assuming a realistic capacity factor of 28%, which means was the mean capacity factor of onshore wind turbines in the UK in 2020,” said Professor Peter Enevoldsen, who conducted research on the report.

Experts have also highlighted the fact that introducing further onshore wind farms would empower local communities by lowering energy costs and giving them a say in their power infrastructure on the ground.

“If we are going to reintroduce onshore wind, how can the host community benefit?” said Communities for Renewables managing director Jake Burnyeat.

“We think local communities should have a right to buy a meaningful share of any windfarm – maybe 20% or one in five turbines.”

“The community could then use surplus income (after operating and finance costs) to fund net zero transition and fuel poverty projects in the surround locality.”

With energy costs skyrocketing and the 54% rise in the energy price cap tacking on an additional £700 per year to households already struggling under the burden of 7% inflation, it seems that accelerated investment in wind power should be the road to take in the looming energy crisis.

“[Even] without accounting for developments in wind turbine technology in the upcoming decades, onshore wind power is the cheapest mature source of renewable energy, and utilizing the different wind regions in Europe is the key to meet the demand for a 100% renewable and fully decarbonized energy system,” said Enevoldsen.

Onshore wind has been backed by experts as the cheapest alternative means of energy for a struggling number of households in the millions, and so it seems odd that it would not have been further prioritised.

The Government’s energy rollout guidelines set the target of raising offshore wind generation from 40GW to 50GW by 2030, but reports from the Guardian cite a leaked earlier edition of the plan which aimed to increase onshore wind capacity from 15GW to 45GW.

However, that earlier ambition was nowhere to be found in the final draft of the Government’s agenda.

Miliband said that onshore wind could actually have replaced Russian oil imports within 24 months, filling a much-needed reliance gap in a mere two years, less than half the amount of time required to develop a small nuclear reactor.

He also added that the administration’s refusal was “not because of the national interest but because some Tory backbenchers said they didn’t want it to happen.”

So far, the Government has been hauled over the coals by everyone from Ed Miliband to Greenpeace, who labelled the energy transition plans “completely inadequate”, while the Association for Renewable Energy & Clean Technology heaped insult to injury with their accusation that the party had “failed to rise to the challenge facing the country.”

Energy and Business Secretary Kwasi Kwarteng released a statement this week which said that the Government would “double-down on every available technology” in support of his comment that cheap renewables were the UK’s “best defence against fluctuations in global gas prices.”

However, despite reiterating offshore wind ambitions to 50GW by 2030, his extensive renewable energy reach did not tap into onshore wind by even a mere passing comment.

It seems odd that the Government has left something so valuable to the taxpayer on the table, picking up the heftier and more time-consuming nuclear option instead.

The administration estimates that the nuclear alternative will represent 25% of the UK’s projected energy demand.

The investment will go towards Small Modular Reactors (SMR), which have been developed by Rolls-Royce, who received a £210 grant from the Government on top of a £195 investment from private firms in 2021.

The Reactors are a form of nuclear fission reactor in a miniaturised edition of the conventional version.

Experts criticised the move and emphasised last year that the focus should be on renewable energy and not nuclear.

The Reactors would be the size of around two football pitches and cost approximately £2 billion per project, providing a more expensive and less efficient means of energy compared to the established wind power potential.

“Big bets on nuclear will provide clean and stable power for consumers and businesses.”

“This scale of ambition should be replicated for other renewable technologies like onshore wind. Commitment to planning reforms and rapid approvals is what will really make the difference now.”

However, the time frame will mean that households are unlikely to see results from the UK’s nuclear investment until around 2030.

The first SMR is currently on a projected schedule to receive regulatory approval by the middle of 2024, with the Reactor estimated to generate power by 2029.

The five-year time frame from start to finish is more than double the timespan required to develop an onshore wind farm, which means that despite the lofty ambitions of the Government to kickstart Britain’s flailing nuclear industry, it does nothing for the millions of consumers who need cheap energy right now.

The FTSE 250 was up 0.5% to 21,192.2 and the AIM was flat at 1,056.7 in late morning trading on Thursday.

Ibstock shares were up 9.5% to 182.2p after the group announced a Q1 2022 performance ahead of management expectations despite climbing inflation, with strong demand across all its end markets.

“Brickmaker Ibstock is plagued by soaring input costs and ballooning energy bills, but the group appears to be coping well,” said Hargreaves Lansdown equity analyst Laura Hoy.

“A focus on increasing capacity and efficiency at its factories has allowed it to jump on booming post-pandemic demand.”

Rank Group shares fell 8.8% to 117.1p after the gambling company cut its full year guidance on the back of poorer performance in March and climbing inflationary pressures.

Ferrexpo shares fell 2% to 176.1p as the company was pulled into the tide of falling commodities stocks today, despite its report of an increase to its humanitarian fund to $12.5 million in a move to assist relief efforts in Ukraine.

“Commodity producers have enjoyed soaring prices in the past year but their moment in the sun might be coming to an end,” said AJ Bell investment director Russ Mould.

“The cracks in the latest round of trading updates from the sector are a reminder that mining operations don’t always run smoothly, commodity prices rarely go up in a straight line on a sustained basis, and earnings are volatile.”

Solid State shares enjoyed an uptick of 13.3% to 11,500p, after the firm announced expected FY2022 results ahead of management expectations.

The company confirmed a 28% rise in revenue to £85 million compared to £66.3 million in 2021, alongside an adjusted pre-tax profit increase of 33% to £7.2 million against £5.4 million.

Churchill China share rose 8.9% to 15,250p following a strong slate of preliminary results for 2021, including an operating profit before exceptional items of £6.1 million, against £0.9 million in 2020.

The company also reported a re-instated final dividend of 17.3p per share after no dividends last year.

“The second half of 2021 saw a strong recovery in our sales to the Hospitality market such that the full year results are ahead of our expectations,” said Churchhill China CEO Alan McWalter.

GB Group shares were up 9.2% to 623p after the firm announced a pre-close trading statement with revenue ahead of management expectation at £242 million for FY2021.

Jangada Mines shares plummeted 27.8% to 7.4p following the release of an updated technical report for its Pitombeiras Vanadium Titano-Magnetite (VTM) project in Brazil, which provided and underwhelming $96.5m post-tax Net Present Value (NPV) and 9-year mine life.

Gear4music shares dropped 27.7% to 260p after the company announced a 6% decrease in total sales in its annual trading update, with higher inflation and weaker consumer demand across February and March predicted to impact the group’s HY1 2023 sales.

“Short-term inflation-linked overhead cost pressures and weaker consumer confidence across the broader retail landscape will mean the best opportunities for stronger growth during FY23 are likely to be in H2,” said Gear4music CEO Andrew Wass.

“We are, accordingly, moderating our overall growth expectations for the new financial year, which we believe is the prudent approach in the current environment.”

Tungsten West shares dropped 17.9% to 52.5p on the back of the group’s suspended operations across its Hemerdon Projects in light of adverse market conditions.

The company reported that it would continue to evaluate alternative approached to reigniting mining operations while it considers it next steps.

Osirium Technologies shares fell 16.6% to 12.5p after the firm reported a widened pre-tax loss of £3.43 million in its 2021 results against a loss of £3.10 million in 2020.

Despite broad weakness in mining companies, the FTSE 100 was trading mostly flat as strong gains elsewhere offset the impact of weaker metals and mining stocks.

“It’s been a bad start to the year operationally for the big mining companies and their latest updates have served to act as a drag on the FTSE 100,” said Russ Mould, Investment Director at AJ Bell.

“The cracks in the latest round of trading updates from the sector are a reminder that mining operations don’t always run smoothly, commodity prices rarely go up in a straight line on a sustained basis, and earnings are volatile.”

Antofagasta’s production of copper fell 24% to 138,800 tonnes compared to 183,000 tonnes in Q1 2022, and 22% lower than Q4 2021.

The group’s gold production dropped by 41% from Q4 2021 to 38,400 ounces in Q1 2022, which is also 35% lower than Q1 2021 when Antofagasta produced 59,100 ounces.

Antofagasta produced 2,000 tonnes of Molybdenum in Q1 2022 which is 33% lower than 2021’s first quarter where the group produced 3,000 tonnes.

A continuing drought at the Los Pelambres mine along with lower grades hampered production, according to Antofagasta.

The net cash cost per pound of copper produced increased to $1.75 from $1.16 in Q1.

For the full year of 2022, the company expects to generate 660,000 to 690,000 tonnes of copper at a net cash cost of $1.55 per pound of copper produced. Antofagasta also expects a total Capex of $1.9bn, which is “at the top end of the previously guided range of $1.7bn to $1.9bn,” the firm said.

Antofagasta faced a difficult first three months of 2022 which led to the group stating that “spending will be at the top end of previous guidance,” according to Russ Mould.

Anglo American

Anglo American shares dropped 8% to 3,707p after the company reported a 10% decline in output during what they describe as a “normally slower” first quarter.

The group’s decrease in output was due to Covid-related absences, high rainfall in South Africa and Brazil, and operational challenges at metallurgical coal and iron ore operations.

Anglo American’s copper production was down 13% YoY, platinum group metals production was down 6%, metallurgical coal production was down 32%, and iron ore production was down 19%.

However, the group’s Diamond output increased by 25%, making it the only category to show a rise.

Anglo American’s cost forecast for the whole year has climbed by 9%, with a 4% hit from stronger producer currencies and a 3% hit from inflationary pressures. Anglo America also lowered its output forecasts for its PGM, iron ore, and metallurgical coal businesses.

Mould says that “shareholders in Anglo American can’t really grumble” about the Q1 results as they have seen 24% gains in share price in the last 12 months, which is “more than double the FTSE 100’s 10.4% gain.”

Mining weakness

Glencore shares lost 5% to 492p despite the company advocating “responsible stewardship” of its coal assets to meet its green ambitions. Glencore said its revised emissions targets are a 15% reduction by 2026 and a 50% cut by 2035.

Berenberg, JP Morgan and RBC all cut Rio’s price target from 6,500p, 5,730p, and to 5,500p respectively.

“Commodity producers have enjoyed soaring prices in the past year but their moment in the sun might be coming to an end,” said Russ Mould.

“The key question now is whether commodity prices are close to their peak for this cycle as a reduction in selling prices together with rising costs will put a squeeze on profit margins.”

FTSE 100 fallers

FTSE 100 fallers included National Grid, HSBC and Ocado whose price targets were altered.

National Grid’s shares fell 1.4% to 1,164p after Berenberg downgraded its view to hold from buy and amended price target to 1,210p.

HSBC Holdings were trading down to 537p despite Jefferies raising its price target to 574p from 473p and BoA raising its price target to 645p from 620p.

Credit Suisse cut Ocado’s price target to 1,600p from 1,650p as Ocado shares dropped 0.25% to 1,079p.

Rentokil

Amongst the risers of the FTSE 100 was Rentokil whose shares gained almost 3% to 528p after the pest control company released an optimistic first-quarter trading update where the company managed to weather the inflation storm.

Meggitt, the defence tech company, reported a 116% rise in its civil order book which lead the company’s stocks to gain 0.03% to 769p.

Rolls-Royce’s shares seem to be enjoying a wave of optimism following its latest update on nuclear reactors. The shares of the company gained 2.6% to 95.9p.

The completion of a financing round saw Ferguson shares rise 1.8% to 10,802p.

Segro said it sees “continued demand from a broad range of customers enabling us to capture further rental growth through rent reviews and the re-letting of space,” according to its CEO, David Sleath.

Aviva shares increased 0.11% to 444p after Jefferies raised Aviva’s price target to 460p from 435p.

Gains in AstraZeneca, Diageo and Unilever also helped the FTSE 100 counteract the damage caused by mining companies today.

AstraZeneca shares were trading up 0.6% to 10,529p, followed by Diageo up 1.4% to 3,926p and Unilever shares increasing 0.9% to 3,498p.

ITV was among FTSE 100 top risers after content-creating rival Netflix signalled they would start to reign spending on Netflix Originals and other forms of content that could possible see budgets flow into ITV Studios.

US Stocks

Tesla shares fell 5% to $977 despite the company reporting a sharp rise in first-quarter earnings as demand for electric vehicles continued in its first quarter. Tesla noted an 81% increase in total revenue to $18.7bn in Q1 2022 compared to $10.4bn in 2021.

While all eyes are on Tesla’s founder’s bid to take over Twitter, “Tesla shares unsurprisingly charged up after market hours in the US yesterday,” handily above quarterly expectations, commented Mould.