The accounts have been completely audited and are valid till September 30, 2021. Pluto’s net assets have increased by around £30m since March 2021, when the company raised £31m in additional funding. As a result, as of September 2021, Pluto’s net assets were £61m or 9.5p per share.

Pluto has continued to grow its company, collaborating with Maze Theory, a digital entertainment firm, to create high-quality games with token economics to empower the next generation of gamers.

As part of the deal, Pluto will invest £4m in Maze Theory and launch a joint venture, Emergent Games, to create a new gaming blockchain and metaverse studio.

Furthermore, Pluto fully purchased the YOP platform in September 2021 and has been actively expanding this platform to help users operate in and navigate the rapidly increasing the decentralized finance (DeFi) industry.

The total value locked in DeFi is estimated to be around $275bn as of December 2021.

Pluto is currently pursuing other alternatives to access public markets, which are most likely to focus on Canadian markets, after NFT Investments announced on 8 April 2022 that it was no longer proceeding with its proposed acquisition of Pluto. As a result, Pluto is actively seeking other options to access public markets, which are most likely to focus on Canadian markets.

Pires Investments currently owns 32,518,876 Pluto shares and has warrants for almost 24m new ordinary shares, 6m of which have already vested, subject to specific vesting requirements.

Nicholas Lee, Director of Pires commented, “Pluto has made substantial progress in the DeFi, Metaverse and NFT sectors since its inception around 12 months ago.”

“The audited NAV per share figure represents a significant increase compared to the price of the most recent funding round, however, in terms of market valuation, companies similar to Pluto can often trade at a multiple of NAV.”

“It is important that Pluto makes its transition to the public markets in the optimum way and at the right time to maximise the creation of value for its investors and we, as one of the company’s original shareholders, are fully supportive of Pluto’s current approach.”

Poolbeg Pharma, a clinical-stage infectious illness pharmaceutical company updated its intellectual property (IP) for POLB 002, a first-in-class, intranasally delivered RNA-based immunotherapy for respiratory viral infections on Thursday.

It may provide pan-viral protection against respiratory virus infections such as influenza, respiratory syncytial virus and SARS-CoV-2, according to research.

It could potentially provide a viable option for protecting at-risk patients such as the elderly, COPD patients, and asthmatics as a nasally delivered and fast effective preventive antiviral candidate.

This significant patent of the POLB 002 patent family, which protects the use of a defective interfering (DI) influenza virus against influenza infection, has been issued by the European Patent Office for Poolbeg Pharma.

POLB 002 works by inducing an antiviral response in nasal cells utilising DI influenza, which resembles the infectious influenza virus but lacks the capacity to replicate, allowing it to elicit an effective immune response but not induce infection.

Poolbeg Pharma will continue to engage with its patent advisors to broaden and develop this patent family, which includes a method for identifying faulty antiviral medicines.

Following a recent ‘Notice of Allowance’ letter from the USPTO, discussions with patent authorities in other jurisdictions, including the US, are expected to continue, with further favourable announcements expected.

With a global focus on respiratory viral infections and such viruses being regarded a top five global killer, resulting in more than 3m annual deaths worldwide, the discovery of POLB 002 and these patent modifications comes at a critical moment.

The pandemic potential of influenza is still being constantly examined by global health authorities, with the WHO and infectious hazard experts advising that a future influenza pandemic can be expected statistically.

The Centers for Disease Control and Prevention (CDC) has stated that early action and effective preparedness are critical to mitigating risk, emphasising the importance of developing vaccines, prophylactics, and antiviral treatments for viruses, with pan-viral products providing an important solution.

Jeremy Skillington, CEO of Poolbeg Pharma said, “The granting of this patent marks an important step in our development and protection of this important respiratory virus disease treatment. Data for POLB 002 shows it is able to both prevent viral infections and rapidly reduce viral loads where infection has occurred, improving disease symptoms and aiding recovery.”

“This makes it an attractive candidate in a market where a significant unmet need for the treatment of most respiratory virus infections still exists.”

“Our patent portfolio in Europe, US and elsewhere for POLB 002 are growing as part of our overall strategy to enhance the protection of Poolbeg’s assets and we look forward to updating shareholders on future patent grants.”

Elon Musk has reportedly submitted a bid for social media giant Twitter for $41 billion, following his rejection of a seat on the company’s board earlier in April.

The Tesla and SpaceX tycoon offered the price of $54.20 per share, which represented a 38% premium to the firm’s April 1 close.

Twitter’s share price spiked 12% in premarket trading on Thursday.

“Since making my investment I now realize the company will neither thrive nor serve this societal imperative in its current form. Twitter needs to be transformed as a private company,” Musk wrote in a letter Twitter Chairman Bret Taylor, via Reuters.

“My offer is my best and final offer and if it is not accepted, I would need to reconsider my position as a shareholder.”

Analysts noted the move as a predictable next step in Musk’s involvement with Twitter, and cited the positive response from shareholders to the offer.

“Elon Musk’s unsolicited offer to takeover Twitter has shocked the market. However, the move shouldn’t come as too much of a surprise in reality, when his decision not to take up a seat on Twitter’s board strongly suggested a takeover was in Musk’s thoughts,” said Hargreaves Lansdown lead equity analyst Sophie Lund-Yates.

“Elon Musk thinks Twitter’s potential is stifled by current management and its position as a public company. Changing either of those things is an enormous move, and one that will sting the ego of the existing management team.”

“The premium being offered by Musk to takeover the company suggests he thinks very highly indeed of what Twitter could be, but not what it is at present.”

The FTSE 250 and the AIM all-share index remained flat on Thursday with the FTSE 250 marginally down 0.02% to 20,979 and the AIM up 0.05% to 1,057.

Movements across oil and gas companies counterbalanced each other whereas airline companies such as Wizz Air and EasyJet helped lift the FTSE 250.

The budget airline, Wizz Air shares flew 7% to 3,098p after the company reported a better than anticipated Q4 performance and expects strong demand over the upcoming summer season.

Wizz Air said thanks to a stronger trading environment, the group expects a net loss between €190m and €210m, which would beat previous expectations in Q4.

“We have been encouraged by demand trends in recent weeks and given the shorter booking horizon expect the bookings for this summer to build significantly after Easter,” said the company.

EasyJet shares lifted 3% to 573p as the airline industry expects growth in demand for travel as the summer holidays approach.

Dunelm shares gained 2% to 1,081p after the leading homeware retailer announced a 69% rise in total sales YoY to £399m and YTD sales increased 25% to £1.2bn in its third-quarter due to the reopening of its stores.

Dunelm says the latest range of analyst forecasts for its pretax profit lies between £195m-£215m, with a consensus at £207m for FY22. The company reported a pretax profit of £157.8m in FY21.

“A big part of the recent transformation of the group has been the development of its online proposition and it is not sitting on its laurels here, continuing to refine and improve things,” said Danni Hewson, Financial Analyst, AJ Bell.

“There may be tough times ahead as the cost of living crisis continues to bite into Britons’ household budgets, however Dunelm and its management look to be doing everything under their control to set the business on the right path.”

discoverIE shares rose 0.8% to 766p as the custom electronics company announced a rise of 36% YoY in group orders for 2021 with an order book of £224m marking a record for the company.

Money manager, Ninety One gained 0.9% to 255p after the company announced assets under management rose by 9.9% to £143.9bn in 2021 compared to £130.9m in 2020.

Primary Health Properties’ shares increased 0.4% to 150p as the safety equipment company announced the acquisition of the Chiswick Medical Centre, London for a total consideration of £34.5m.

Countryside Properties fell 2% to 245p after Berenberg cut the company’s price target to 270p from 510p.

Hays shares dropped 1% to 118p after the company reported a £5m hit from pulling out of Russia. The company, however, did note a 32% surge in like-for-like fees over Q3 to Q4, with record-breaking results across 19 countries and its highest-ever monthly fees in March.

Vesuvius, Baltic Classified and Ibstock shares lost 6%, 3.7% and 3.5% marking the top fallers of the FTSE 250.

Oilex shares dropped 14% to 0.2p after the oil and gas company announced a shortage of funds that are required for the C-77H re-frac costs to start up gas production on the Cambay field in India.

Oilex has also negotiated a revised gas sales agreement with Enertech Fuel Solutions for the sale of gas from the Cambay field. The revised gas price is now $7.32/mmBTU compared to the previous gas price of $4.2/mmBTU.

Decontamination company, React shares plummeted over 20% to 1.4p after it announced a proposed placing of 458,333,332 new ordinary shares at a price of 1.2p per Placing Share to raise gross proceeds of £5.5m to strengthen the balance sheet to support the company’s stated acquisition growth strategy and general working capital purposes.

Renold shares soared 31% to 26.5p after the international supplier of industrial chains reported strong momentum in order intake and turnover as it delivered revenue of £195m for the full year, which is an 18% YoY increase on a reported basis, as a result of stronger sales, benefits of cost reduction and efficiency programmes.

Renold’s order intake was £223.7m in 2022 representing a YoY increase of 31.6% on a reported basis. The current order book of £84.1m compared to £53.6m in 2021, which is a record high for the group.

Petrel Resources shares increased 17% to 1.7p as the company’s High Court injunction over the 32.1m shares previously held by the Tamraz Group has been lifted.

Italfluid has verified purchase orders for gas processing and liquefaction packages, as well as the LNG storage tank, which has been issued. Sound Energy has reassessed its broad exploration portfolio in Eastern Morocco’s Greater Tendrara and Annual exploration licences.

Credible counterparties with the ability to mature alternative or complementary funding to debt and mezzanine finance have expressed great interest. Sound Energy is in talks with farmers near its Sidi Moktar gas field to see if solar-powered electricity may be provided.

By continuing to develop its existing gas projects as well as potential new gas-related opportunities, Sound Energy aims to help the energy transition.

Nostra Terra shares lifted 9% to 0.62p after the oil & gas exploration and production company announced the commencement of drilling operations on its new, wholly-owned Grant East Lease located in the Permian Basin of West Texas.

CareTech Holdings dropped 0.3% to 745p after the company confirmed receiving a revised proposal from Sheikh Holdings regarding a possible all-cash offer for the group of 750p per share with a partial share alternative.

The revised proposal comes after Sheikh Holdings prospective offer of 725p per ordinary share in cash, as well as the initial proposal of 710p per ordinary share in cash, both disclosed on April 1, 2022.

The FTSE 100 was flat at 7,577 in late morning trading on Thursday, after the latest 7% rise in UK inflation muted investor optimism and consumers braced for the cost of living to spike.

The move was a sharp turn from the trends set by the Bank of England and the US Federal Reserve, which both chose to hike interest rates in 2022 to address soaring rates of inflation.

“In the current conditions of high uncertainty, the Governing Council will maintain optionality, gradualism and flexibility in the conduct of monetary policy,” said the ECB in a statement.

“The Governing Council will take whatever action is needed to fulfil the ECB’s mandate to pursue price stability and to contribute to safeguarding financial stability.”

“The expectation is that ECB chief Christine Lagarde and her colleagues will sit on their hands but the runaway nature of inflation in the Eurozone is bringing considerable pressure to bear on the central bank,” said AJ Bell financial analyst Danni Hewson.

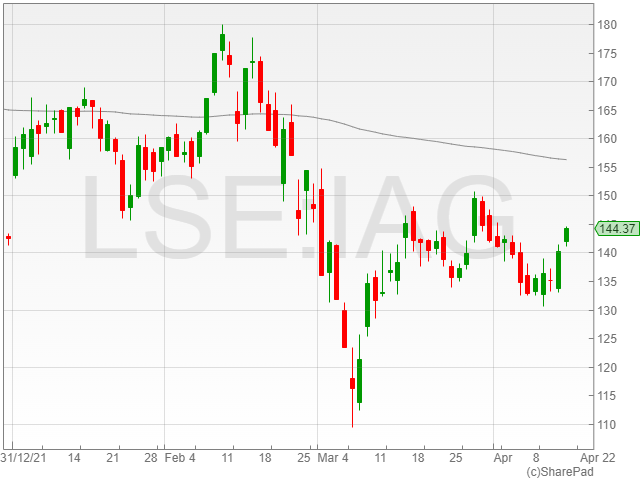

However, it wasn’t entirely bad news, as travel companies took flight with IAG shares rising 2.7% to 144.2p as families broke away from the gloomy UK weather for sunnier countries despite the crushing rate of inflation.

“The top riser was British Airways owner International Consolidated Airlines … which suggests people are prioritising air travel despite the pressures on their finances,” said Hewson.

“After so long of having their travel restricted, it seems the appeal of jetting away is very strong.”

InterContinental Hotels shares increased 2.4% to 51,070p as it joined the climbing travel-focused stocks in their gains.

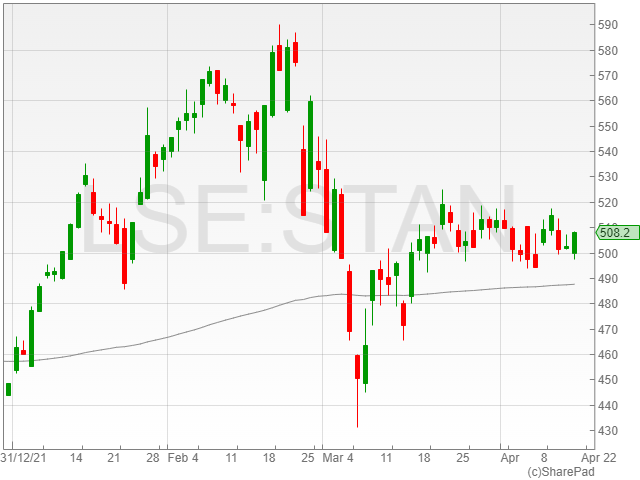

Standard Chartered shares saw an uptcik of 0.9% to 507.2p after the company announced plans to exit its operations in Africa and the Middle-East in a move to “deliver efficiencies” and “reduce complexity.”

The financial company commented that it would be focusing its business on its most significant opportunities for growth, focusing on shareholder returns after its “disciplined” opportunities assessment.

“Subject to regulatory approval, the group now intends to exit onshore operations in seven markets in AME and in a further two markets focus solely on its Corporate, Commercial & Institutional Banking business,” said a Standard Chartered spokesperson.

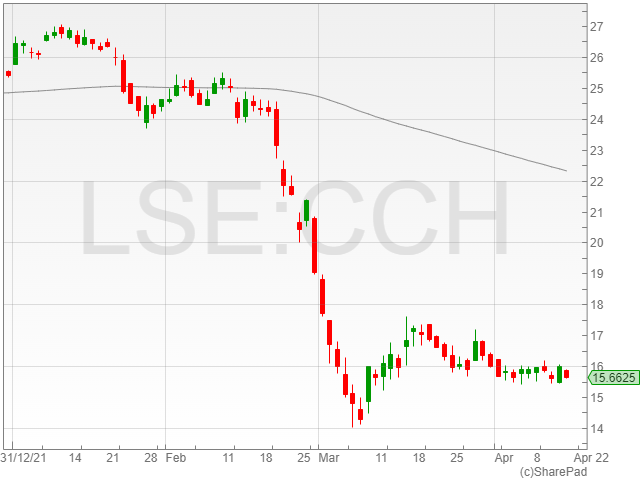

Coca-Cola HBC took a blow of 2% to 15,672p following its price target cut by Credit Suisse to 2,200p from 2,400p.

Smiths Group shares were down 1.5% to 1,414.5 in early morning trading on Thursday, following the firm’s announcement of several new executive appointments.

The engineering company confirmed its appointment of Clare Scherrer as Chief Financial Officer, who has been an advisor to the firm for seven years and is scheduled to replace John Shipsey from 29 April.

She previously spent 25 years at Goldman Sachs, where she worked as partner for over 10 years and was most recently the Co-Head of the Global Industries Business.

Her experience covers a broad range of industrial industries, with specialised interest in the technology sectors, including energy, safety, security and aerospace.

Smiths has also hired Bernard Cicut as President of John Crane, who will take over the position from Jean Vernet on 18 April.

Cicut joined the company from his previous role at 3M as President of the business’s $4.5 billion Personal Safety Division, where he led increased growth and a four-fold increase in global respirator supply during the Covid-19 pandemic.

The group announced Vera Kirikova as Chief People Officer, who is set to replace Sheena Mackay from April 18.

Kirikova joined the company from her prior position at Rio Tinto, where she worked as Chief People Officer between 2016 to 2021, following her 22 year employment at Schlumberger in a variety of senior leadership roles.

Smith also announced that Group Head of Strategy is officially set to become an Executive Committee role, with present Group Head Diana Houghton consequently promoted to the Committee from April.

Houghton has been in the role since 2019 and joined the company in 2013, with her contributions playing a key role in developing the firm’s growth strategy over the past few years.

“On behalf of the Board I would like to thank John, Jean and Sheena for their significant contributions to Smiths over the years and wish them continued success in the future,” said Smiths Group CEO Paul Keel.

“At our Capital Markets Event in November, we laid out a plan to accelerate growth at Smiths and deliver on our significant potential.”

“We’re now seeing multiple examples of this such as the earlier than expected close of the Medical Sale, ramp-up in new product activity, and first half results which delivered 3.4% organic revenue growth. Today’s announcement further builds on our momentum.”

Oil prices have been skyrocketing with geopolitical tensions on the rise. Countries have come together to combat the hikes in oil prices due to high global demand. China’s lockdown aids this movement as the halt in production across its industrial sector slows down the country’s demand for oil, according to the International Energy Agency.

China is a major importer of oil and metal to support its industrial sector. With the rise in Covid-19 cases, China has entered into a tight lockdown to combat the pandemic from spreading.

With the country under lockdown, the industrial sector is at a halt resulting in lower demand for oil during times of distress due to the havoc caused by the ban on Russian oil according to the IEA.

The IEA said in its monthly report on world oil markets that Russia’s output would fall by 1.5m barrels per day (BPD) in April, increasing to 3m BPD in May, as consumers either voluntarily stop buying Russian supplies or scale back due to uncertainty over sanctions.

Given Russia’s position as the world’s second-largest oil producer, the prediction suggests that up to 3% of global supply might be lost by the middle of spring.

The IEA said there was unlikely to be a “sharp deficit” in global oil markets because of several variables that offset the impact of lost Russian supplies.

The most recent example is China’s installation of “stringent” anti-Covid regulations, in which China has placed all 26m residents in Shanghai under house arrest.

Weaker-than-expected demand in OECD countries which is a collection of primarily developed countries has contributed to the drop in global demand for oil, according to the IEA.

As a result, the organisation reduced its global oil demand forecast by 260,000 BPD from last month’s estimate, predicting that the global market will require an average of 99.4m BPD in 2022.

Due to the general global economic upswing from 2021, which was more heavily impacted by Covid limitations around the world, the number is still up 1.9m BPD from 2021.

Oil prices have soared to near-record highs as a result of this recovery, as well as market uncertainty induced by Russia’s invasion of Ukraine.

The consequent increase in fuel prices has been felt by motorists in nations such as the United States and the United Kingdom, where gasoline and diesel prices have reached new all-time highs, resulting in a growing cost-of-living crisis.

The IEA’s revised lower prediction should allay fears about oil prices, especially now that the outlook for oil output has improved.

Opec members Saudi Arabia and Iran committed to a 400,000 BPD increase, although not to the extent that big oil consumers like the United States and India had wanted.

Member countries of the IEA have also consented to a coordinated release of 120m barrels of emergency reserves to assist the cut in oil prices, with the price of Brent crude falling by $10 to $104.

During the early days of Russia’s invasion of Ukraine, the price almost reached $120, and analysts predicted it would soon surpass the all-time high of $147.50, set in 2008.

The IEA reports, on the other hand, have contributed to a long-term pattern of declining reserves, with inventory falling for 14 months in a row.

In February, inventories were 740m barrels lower than they were at the end of 2020, with OECD countries accounting for 70% of the reduction.

The oil price dropped 0.6% to $108 a barrel on Thursday as demand eases with China’s lockdown and supply increases with support from nations with oil.

The electronics firm’s group orders remained ahead of its sales with a 36% year-on-year organic growth and a 32% two-year growth driven by strong demand across the company’s target markets.

The group delivered 17% year-on-year sales growth alongside a 13% two-year growth.

The company grew its sales for the past two months 20% year-on-year and 22% over two years, despite ongoing supply chain challenges including semiconductor shortages which caused disruption in two of its 20 businesses.

discoverIE Group highlighted its agility in navigating Covid-19-linked challenged and noted that its exposure to Ukraine remained minimal, with the Russian invasion causing few disruptions its business operations.

The company also celebrated its A rating from the MSCI ESG Research group in recognition of discoverIE Group’s environmental and social governance, along with its strategic focus on sustainable technologies such as renewable energy.

The firm commented that it was well-funded with strong liquidity and a reliable cash flow, alongside additional capital from the sale of its Acal BFi distribution business providing it with significant capacity for future acquisitions and steady pipeline of opportunities for the group to expand.

The discoverIE Group said that the company currently looks well-positioned to make progress on its key priorities going into 2022, with a record order book and “sustainable growth” markets across Europe, North America and Asia.

Healthcare facility investor, Primary Health Properties announced that it acquired Chiswick Medical Centre in London for £34.5m on Thursday.

Primary Health Properties has completed the purchase of the Chiswick Medical Centre in London for £34.5m and the property is fully leased to HCA International Ltd for just under 20 years, with five annual compounded RPI led rent reviews.

The Chiswick Medical Centre has undergone a comprehensive tenant-led fit-out to establish a unique diagnostic and private healthcare centre with some of London’s most advanced medical technology.

The hospital offers a variety of services and specialised teams in neurology, cardiology, orthopaedics, urology, and gastroenterology, as well as women’s healthcare and a children’s unit.

Primary Health Properties’ portfolio will grow to 524 assets, 20 of which are in Ireland, with a committed rent roll of slightly under £143 million as a result of this transaction with Chiswick Medical Centre.

Harry Hyman, Chief Executive Officer, Primary Health Properties, stated, “We are delighted to have acquired this state-of-the-art diagnostic centre in London, let to an excellent covenant which provides a wide range of services which alongside the NHS is assisting with tackling the significant backlog of referrals following COVID-19.”

“We have a strong pipeline of opportunities in the UK and Ireland and are well positioned to continue to grow our portfolio and to support the healthcare systems in these markets through the provision of modern, primary care infrastructure.”

National Grid shares were flat at 1,183p in early morning trading on Thursday, after the group projected moderately above-expected profit returns in its pre-close trading update ahead of its financial results for the last year.

The company confirmed that its New England, New York and National Grid Ventures business units were on track to deliver underlying operating profits in line with management guidance.

However, the firm anticipated a boost in underlying profit in its UK Electricity Distribution business units, with rising inflation driving projected profits above expectations.

The National Grid added that it expects to take on a 25% underlying effective tax rate due to an additional tax charge of approximately £100 million, reflecting the impact in its income statement of deferred tax reversing at a higher rate in future company statements.

The company projected its average expected underlying effective tax rate at a reduced level of 23% for FY 2023.

The group mentioned that it currently expects its 2022 earnings per share to deliver slightly above management guidance.

The National Grid also highlighted a selection of sales and acquisitions across its financial year, including its acquisition of Western Power Distribution on 14 June 2021.

The company confirmed that the contribution from its acquisition had been included in its financial results for the year.

The group noted that it continued to hold its UK Gas Transmission and legacy Metering businesses as discontinued operations since the sale of a majority stake in National Grid Gas on 27 March 2022, and will reportedly continue to hold the entities until the transaction closes later this year.

The National Grid also listed the ongoing sales of its Rhode Island business to PPL, with the transaction projected to close in the first quarter of the firm’s FY 2023.

The company is set to report the asset under its New England business unit until the agreement closes.

The National Grid added that it was currently working with the UK Government to manage a smooth transition as part of the administration’s plan to create a Future System Operator to shoulder the existing Electricity System Operator roles, alongside the longer-term aspects of the Gas System Operator.

The company confirmed that the transition is scheduled for completion by 2024.