Loan allows Argo to retain its current Bitcoin holding

Argo Blockchain (LON:ARB) confirmed on Friday that it has secured a £18.05m loan agreement with Galaxy Digital by using some of its Bitcoin as collateral.

The loan will mature on 29 October 2021.

The blockchain mining company’s outstanding loan with Galaxy is valued at £14m, meaning the new loan agreement will come to a total of £32.05m.

The money will be allocated, in addition to the funds raised by the company previously, to continue the build-out of the West Texas data centre and to meet the firm’s operating cash flow requirements.

The loan will enable Argo to retain its current Bitcoin holding, whilst further expanding its mining operations.

“Argo is delighted to continue working with Galaxy as its financing partner,” the company added.

Argo Blockchain made £6.83m in mining revenue last month, an increase of £2.23m, as the price of bitcoin rose.

The bitcoin mining company mined a total of 206 bitcoins in August, down from 225 in July, bringing the overall amount mined for the year-to-date to 1,314.

Argo sold 61 bitcoins last month, and kept a total of 1,659 bitcoins on its balance sheet, priced at a market value of $82m as of Friday morning.

Peter Wall, Chief Executive of Argo and interim Chairman said: “I am pleased that we have been able to deliver these results at an improved margin this month and continue to deliver value to our shareholders. We are also delighted to have released our Climate Strategy and remain committed in our efforts to enact positive change within the crypto mining sector.”

Argo Blockhain, listed on the London Stock Exchange (LSE) at present, is weighing up a secondary listing on Nasdaq.

Hurricane says $152m of bonds will remain at face value

The Hurricane Energy share price jumped up by 8% in early morning trading on Friday as the firm confirmed it will buy back $78m of bonds at a discount to par.

The AIM-listed company will pay 78p of each pound to buy back convertible bonds, as part of an effort that will take place in 2022.

$152m of bonds will remain at face value after the company’s tender is settled.

“I am pleased that the company has been able to buy back more than 33% of the outstanding bonds,” Antony Maris, Chief Executive Officer said.

“This will reduce the par value of bonds held by third parties to US$152mln, utilising US$62mln of net free cash (inclusive of accrued interest).

“The effect of this will save the company approximately US$22mln of future obligations to bondholders in capital and interest. This is a positive development for the company in managing its outstanding debt.”

Hurricane was established to discover, appraise and develop hydrocarbon resources associated with naturally fractured basement reservoirs. The company’s acreage is concentrated on the Rona Ridge, in the West of Shetland region of the UK Continental Shelf.

EasyJet has its eyes set on acquiring market share from British Airways

EasyJet has rejected an approach from Wizz Air, as the Hungarian airline continues its efforts to expand into the western European market on the back of the pandemic-induced downturn.

The airline confirmed it immediately rejected Wizz’s offer which was a “low premium and highly conditional” al-share deal.

The Financial Times reported that the name of the company making the offer, Wizz Air, was disclosed by someone briefed on the issue.

Johan Lundgren, CEO of EasyJet, has even said his company is exploring the possibility of expanding its operations to directly challenge the market share of British Airways. Funds would be raised by way of the £1.2bn rights issue.

Wizz’s approach, in addition to EasyJet’s plotting, displays the changing of the mood in the industry, as some airlines are looking to strike on the back of the worst crisis in their history.

“I think everybody would agree that when you go through situations like this, that there are consolidation plays happening,” easyJet’s chief executive Johan Lundgren said.

The EasyJet share price is down by 1.78% during the morning session on Friday, while the Wizz Air share price is down by 1.02%.

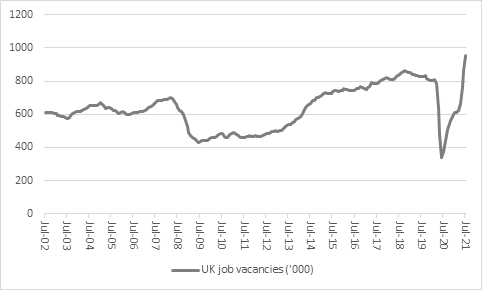

Eyes will be on the latest UK jobs, unemployment, job vacancy and wage growth figures, as anecdotal evidence of labour shortages is popping up everywhere. The Confederation of British Industries’ warned that these shortages could persist for two years, as reported by UK Investor Magazine earlier this week.

“At first sight, talk of labour shortages seem odd,” said Danni Hewson, AJ Bell Financial Analyst. The UK reported 953,000 job vacancies as of June, while 1.6m people were unemployed and 1.9m remained on the furlough scheme.

Source: ONS

“However, the issue seems to be a skills and qualifications mismatch in many industries, from engineering to HGV driving to chefs and hence the call from the CBI and others to add more industries to the Government’s shortage occupations list which permits overseas workers to gain visas so they can work in the UK,” said Hewson.

In addition, the 4.7% unemployment rate is below the long-term average, the employment rate of 75.1% is only a fraction below February 2020’s all-time high of 76.6% and the total employed of 31m is only 694,000 below the all-time peak here, also in February 2020.

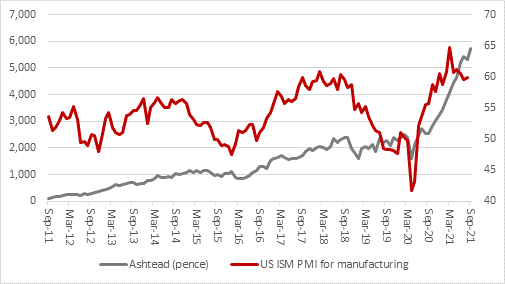

Ashtead Q1 trading update

Shares in Ashtead, the equipment hire firm, have been on an outstanding bull-run as of late. This is despite the pandemic-induced global downturn.

Ashtead gets 90% of its sales from its American Sunbelt operation, while most of the rest comes for the A-Plant business in the UK.

“Perhaps one of the reasons that the shares have done so well is hopes that the US economy will keep humming along, buoyed by monetary stimulus from the US Federal Reserve and more fiscal stimulus from Congress – even if the latter is still log-jammed on Capitol Hill in Washington and at risk of being blocked by two Democratic Senators,” says Hewson.

Hewson also drew attention to the alignment between Ashtead share price and the Institute for Supply Management’s purchasing managers’ index for manufacturing.

Source: ISM, Refinitiv data

Ashtead’s Q1 statement should be an informative one and analysts and shareholders will look to two headline figures.

“The first is sales. On a stated basis, revenues rose 23% year-on-year in the fourth quarter of the last financial year, the first growth in five quarters. Analysts are looking for 10% sales growth for the whole year to April 2022, slightly ahead of management’s guidance for an increase of between 6% and 9%.”

US retail sales

US retail sales disappointed in July, missing forecast, as sales fell 1.5% month-on-month.

“Investors may be tempted to think “so what?” This is a messy dataset right now, owing to the pandemic. Moreover, retail sales are higher than they were before the pandemic started in the first quarter of 2020 and it is easy to argue that the drop in July is due to the outbreak of the Delta variant Stateside,” says Hewson.

However, there could be more to things than meets the eye. Several individual states have individual states already withdrawn the enhanced $300 weekly unemployment benefit and that is due to end nationwide at the end of September. “Could it be that pending is easing as stimulus is easing?” questions Hewson.

The question now is what will happen when stimulus cheques are cut off? “What will happen when the rental eviction bans and mortgage payment forbearance schemes come to an end?” Hewson adds.

“That might drive a fresh surge in employment as people have to go to work, say some. It may lead to a plunge in retail spending, say others.”

ECB shows signs it will begin withdrawing assistance

The European Central Bank (ECB) confirmed on Thursday that it is scaling back its bond puchases over the next three months.

It is a sign that the EU will now slightly withdraw the aid it provided to the eurozone in an effort to support the economy during the coronavirus pandemic.

The ECB left no stone unturned last year in an effort to achieve growth. Now, with the subsequent levels of inflation and growth, senior officials at the central bank have been under pressure to dial back the measures.

Ahead of the ECB’s monetary policy meeting today, opinion was divided over what the outcome would be an its impact on the Euro.

Since the end of august the Euro has been outperforming the US dollar, however, only to a limited extent.

There was a subdued response from the Euro following the ECB’s announcement today

Commenting on the market reaction as attention turns to President Lagarde’s press conference, Shane O’Neill, Head of Interest Rates at Validus Risk Management, said: “As expected, the ECB did not change its main interest rates or the size of its PEPP envelope, which remains at EUR1,850 billion. The PEPP will continue until at least March 2022, but the monthly pace of purchases will be adjusted to a “moderately” slower pace compared to the current EUR80bio/month.”

“EURUSD is virtually unchanged on the news and market attention will now turn to the press conference, where President Lagarde is sure to receive many questions on the specifics on the PEPP going forward.”

“Decisions about your portfolio are far better made with firm investment principles, rather than superstitions in mind” says Fidelity director

According to Fidelity International, investors who ‘sold in May’ have missed out on the opportunity to increase their returns during the summer months.

A number of markets climbed by more than 20% in this time period.

The notion of selling in May is based on the premise that equity markets will go through a seasonal decline during the summer.

Therefore investors sell their holdings at the beginning of May and stay away from the markets until mid-September.

Contrary to this view, a number of markets around the world enjoyed fruitful summers. The FTSE All Share index rose by 4.52% between 1 May and 31 August while the Nasdaq is up by 21.58%.

Of the six markets included in Fidelity’s analysis, just the Nikkei 225 fell during the period by 2.30%.

Market index

Returns, 1 May-31 August 2021

FTSE All Share

4.52%

FTSE 100

3.64%

Nasdaq

21.58%

S&P 500

8.70%

Dax 30

4.62%

Nikkei 225

-2.30%

The adage remains as unpredictable a guide for investors as ever, with Fidelity International’s analysis revealing 2021 is the 18th occasion in 30 years that it has fallen short for the FTSE All Share.

Ed Monk, associate director for Personal Investing at Fidelity International, comments: “2021 would’ve been a painful time for anyone following the old adage to ‘sell in May’. The giant US market, in particular, has gone from strength to strength this year and has hit multiple new highs as the summer has progressed. With markets elevated it is understandable that investors will look for the moment when the tide can turn but these numbers show that, once again, staying invested has proved the best policy.”

Monk continues: “Decisions about your portfolio are far better made with firm investment principles, rather than superstitions in mind. As this year’s analysis shows, there’s no certainty that “selling in May” will pay. Investors who chose to exit the market over the summer will not only have missed out on the opportunity to boost their returns, but now face having to buy back in at a higher price.”

888 unsuccessfully tried to buy William Hill in 2016

888 Holdings mad a move towards becoming one of the dominant betting companies in the world as it acquired William Hill International for £2.2bn.

It said the deal would allow 888 to make £100m of annual cost synergies following the move which was part-funded by a £500m equity raise.

The FTSE 250 firm described the deal as being “a transformational opportunity for 888 to significantly increase its scale, further diversify its product mix and accelerate the upward shift of its revenue-growth profile”.

“William Hill himself used to take bets over the phone from the famously nocturnal racehorse owner Dorothy Paget after the races had been run, because he knew she was a wild gambler and had no chance of finding out which horses had already won, at a time when there were no licenced betting shops, let alone live radio or television broadcasts or mobile phones. 888 will be hoping it is on to a similar sure-fire winner with its acquisition of the European assets of the betting empire built by Mr Hill,” says AJ Bell Investment Director Russ Mould.

888 unsuccessfully tried to buy William Hill in 2016, as part of a complex three-way, £3 billion deal with Rank, when it nearly turned the tables on Hills, which had failed in a lunge for 888 the year before.

“888 will feel that patience has paid off, not least as the total bill this time is £2.2 billion. Moreover, the deal will hugely enhance 888’s size, share and competitive position, especially in the all-important online betting arena in regulated markets,” Mould said.

“In 2020, 888 recorded sales of $814 million and earnings before interest, taxes, depreciation and amortisation (EBITDA) of $156 million. Including William Hill International’s assets takes those historic figures to $2.5 billion and $464 million.”

“On top of that, 888 expects to generate $100 million in cost benefits and will doubtless also be looking to drive revenues higher through cross-selling games and services to existing and new customers,” said Mould.

888’s business mix is more heavily slanted toward games and casinos, William Hill’s more toward betting on horse racing and sports.

Some investors may be wondering whether 2020’s pandemic-and-lockdown online betting boom can be sustained, given the greater range of leisure and spending opportunities that are once more open to consumers.

“Tighter regulation also remains a potential concern, notably in the UK, where the Government continues to review the 2005 Gambling Act.”

The FTSE 100 has seen its third consecutive day of falls as concerns about global growth come to the fore.

The blue-chip index was down by 1.18% at 7,012.2 with energy, financials and miners among the worst performing sectors.

“All three driven by economic activity, which shows you how investors are thinking,” said Russ Mould, investment director at AJ Bell.

“International Consolidated Airlines was the biggest faller on the FTSE 100. The fact that EasyJet is raising more money to help to capitalise on growth opportunities would suggest that some of IAG’s peers are getting their ducks in a row to accelerate their recovery, whereas the British Airways owner is still plagued by high debts.”

“The ECB will be in focus later today as it is expected to update on any plans to taper bond purchases. The US Federal Reserve is unlikely to be in a rush to start easing its economic support measures following the very disappointing August jobs numbers, but will Europe finally be one step up on this point?” Mould added.

FTSE 100 Top Movers

Antofagasta (0.93%), Taylor Wimpey (0.78%) and Evraz (0.54%) are leading the way on the FTSE 100 during the morning session on Thursday.

Down at the other end, IAG (-3.61%), Prudential (-3.05%) and Melrose Industries (-3.05%), have made the most substantial losses.

EasyJet

EasyJet has confirmed it rejected a takeover offer as it set out plans to raise £1.2bn from investors in an effort to cope with a more sustained downturn in the airline industry.

The firm said the all-share approach undervalued the business, adding that the potential bidder is no longer interested in a deal.

Instead, via a rights issue, EasyJet will seek to improve its balance sheet and also seek out growth opportunities that could occur over the next few years as it expects the European airline industry to make a recovery.

EasyJet deploying strategy to steal market share from rival airlines

EasyJet has confirmed it rejected a takeover offer as it set out plans to raise £1.2bn from investors in an effort to cope with a more sustained downturn in the airline industry.

The firm said the all-share approach undervalued the business, adding that the potential bidder is no longer interested in a deal.

Instead, via a rights issue, EasyJet will seek to improve its balance sheet and also seek out growth opportunities that could occur over the next few years as it expects the European airline industry to make a recovery.

By restructuring its short-haul operations, EasyJet will be looking to take market share away from IAG.

It will do this, as an example, by expanding its presence at key airports and acquiring additional landing slots, according to the company’s chief executive Johan Lundgren.

“This capital increase will allow us to build on our fundamental operational strengths and network strategy for our customers as well as accelerate long-term value creation for our shareholders,” he said.

Under the fully underwritten rights issue, shareholders will be able to buy 31 new shares for every 47 existing shares at a price of 410p each, a 36% discount on the theoretical ex-rights price of 638p a share at yesterday’s closing price, The Times reported.

The EasyJet share price is down by 9.28% during the morning session on Thursday.

Morrisons shareholders will reach a decision following auction in October

Morrisons has reported a fall in profits on Thursday, however it has been overshadowed by ongoing talks with both of its US private equity suitors, in addition the UK’s Takeover Panel.

In August, the grocer’s board recommended that shareholders get behind an offer by Clayton, Dubilier & Rice (CD&R) that would value the supermarket chain at £7bn.

However, rival private equity firm Fortress, which has had previous offers usurped by CD&R, could yet make an improved bid.

Morrisons confirmed via a statement that is is operating with the view that either firm could make an offer that is “further increased or otherwise revised, a competitive situation continues to exist”.

Following an auction set to take place on 18 October, the supermarket chain will reach a decision on whether to recommend the CD&R or Fortress offer to its shareholders.

While there are no certainties in life, Susannah Streeter, senior investment and market analyst Hargreaves Lansdown said “it looks like the higher bid from Clayton Dubliier and Rice might now be on a smooth conveyor belt to approval with the company recommending its offer of 285p per share.”

“There is of course still a chance Fortress will wade in with a higher offer and these latest results will offer plenty of food for thought over whether an even higher bid is justified. There is a disappointing headline number with profit before tax and exceptionals falling 37% to £105 million in the first half. The closure of in-store cafes and lost sales in fuel and takeaway snacks was an £80 million hit and extra Covid expenses nibbled away another £41 million.”

Morrisons believes these troublesome costs will largely evaporate in the second half and profit for the year will beat last year’s £431 million.

“Certainly two year like for like sales growth of 8.4% is encouraging,” says Streeter.

“Also the acceleration of the Morrisons rebrand roll out to McColls stores and the expansion of Morrisons on Amazon is a welcome trend, with opportunities to significantly increase online sales. But there could be hiccups on the way to a higher profit trajectory, given the looming supply chain issues for the industry. Morrisons says it has a plan up its sleeve to mitigate potential cost increases, and stock shortages, but it’s hard to forecast just how tough the next few months may be. However with uncertainty looming Morrisons won’t want to look past its sell by date, so there is likely to be intense focus now on getting a deal signed, sealed and delivered .’’