A total of 194,456m of drilling from 230 drill holes has been completed since Newcrest commenced exploration activity

Greatland Gold (LON:GGP) has reported ‘excellent growth drilling results’ from its Havieron gold-copper deposit in the Paterson region of Western Australia.

New growth drilling results outside initial resource area include:

133m @ 7.0g/t Au & 0.05% Cu – HAD133W1

29.1m @ 9.7g/t Au & 0.29% Cu – HAD140

87m @ 1.8g/t Au & 0.05% Cu – HAD141

Drilling activities since the last update include new results from the Growth Drilling programme, which continue to support the potential for resource expansion of the Havieron gold-copper system.

The latest results comprise assays for twelve new drill holes from the Growth Drilling programme (not previously reported), with six holes returning significant assay intercepts in excess of 100 gram metres Au (Au ppm grade x length metres) with HAD133W1 at 133m @ 7.0g/t Au & 0.05% Cu for 945 gram meters being a top four Havieron intercept, and all holes intersecting mineralisation.

A further 18 holes have been completed and await assays, anticipated to be received and reported in the next update.

A total of 194,456m of drilling from 230 drill holes has been completed since Newcrest commenced exploration activity (excluding holes in progress or drill holes which have not been sampled).

Shaun Day, Chief Executive Officer of Greatland Gold, commented: “The Growth Drilling campaign at Havieron continues to deliver excellent results with significant intercepts of high-grade gold and copper outside the existing resource shell. These assay results have once again extended known mineralisation below the main South East Crescent zone and to the north-west in the Northern Breccia, adding further scale and value to the Havieron orebody.”

“With nearly 200,000 metres of drilling now completed, including extensive Growth Drilling in recent months, we have significantly enhanced our understanding of the orebody and the likelihood of delivering an upgrade to the Mineral Resource Estimate in the near-term.”

“Early works for the mine development are progressing to plan with the decline now advanced to over 120 metres from the Portal towards the top of the orebody.”

“The pace of construction activities and surface infrastructure at Havieron is intended to expedite future mining operations, enabling early free cash flows to be re-invested into further development. This supports our belief that the low-risk profile of Havieron makes it a globally unique opportunity for bringing a tier-one gold-copper mine into production.”

The Greatland Gold share price is down by 0.027% during the morning session on Thursday.

By Charles Luke, Investment Manager, Murray Income PLC

In a see-saw year for markets, income generation in the Murray Income Trust has held up well

Our key priorities in the Trust are to be ‘dependable’, ‘diversified’ and ‘differentiated’

We see better times ahead for the UK equity income sector

This has been a see-saw year for investment markets. In the early stages of the pandemic, investors focused their attention on companies with reliable growth. Since the vaccination programme has allowed economies to reopen, there has been a rotation to ‘recovery’ companies. As long-term investors, we need to look beyond these short-term shifts in markets to the true outlook for individual companies.

We have been both beneficiaries and victims of these market shifts. The focus on quality companies at Murray Income meant that the Trust proved resilient during the worst pandemic sell-offs, but it also meant that we lagged the sharp rally in November 2020. The same has been true for the income profile of the Trust. In general, the companies we hold continued to pay dividends throughout the crisis, in contrast to the wider market, which of course means that they haven’t participated to the same extent in the subsequent partial recovery.

As such, investors in the Trust have avoided the whipsaw of investment markets over the past 12 months. This is deliberate; one of our key aims on the Trust is to be ‘dependable’ – we aim to deliver consistent capital returns and income. This is why we focus on higher quality companies. While weaker companies may have short-term periods of share price growth, good quality companies are best placed to grow their earnings sustainably over time.

Perhaps more importantly, the market tends to underestimate the durability of returns from this type of business. Earnings streams are less volatile and stronger balance sheets allow companies to navigate tougher times more successfully. We have seen this through the pandemic.

How we assess quality

When assessing quality, we consider five attributes – the sustainability of a company’s business model, its financial strength, the capability and skill of the management team, the attractiveness of the industry in which it operates and an assessment of environmental, social and governance (ESG) risks and opportunities. We want to find companies that manage both risks and opportunities successfully.

Our focus on environmental, social and governance factors is part of this quality assessment. A company cannot be high quality if it neglects its environmental impact, for example, or mistreats its employees. We have an on-desk ESG specialist and an internal ESG team, whose research is available to all analysts in the company and is a fundamental part of our decision-making.

Diversification is integral to avoiding the worst of market volatility. The pandemic has shown how problems can emerge unexpectedly and hit previously rock-solid industries. As such, it is important not to put all our eggs in one basket. This is also vital when generating income. At Murray Income Trust, we look to diversify across the UK market – from larger to medium-sized companies. We can add up to 20% in overseas listings, which brings in new sectors and ideas that may be underrepresented in the UK market. These factors – a focus on high quality, diversification, ESG and this overseas exposure – help to differentiate the Trust from its peers.

The equity income sector

This approach has helped us navigate a challenging time for the equity income sector in recent years. Dividends from companies held in the Trust have been very resilient and we believe the equity income sector is generally in better health post-pandemic. Companies that were previously over-distributing have pared dividends back to more realistic levels and earnings are encouraging.

While the past few years have been tough, it is important to remember that academic evidence shows that over the long-term, a significant part of stock market returns come from dividends and their re-investment. Our priority is to find those companies growing their earnings and dividends over the long-term. In an ever-changing world, the market is likely to prize companies with strong business models and structural growth.

The UK equity market still has a valuation advantage over many of its peers. It may have recovered somewhat since the Brexit deal, but it has lagged for several years and international investors are still only lightly invested in the UK. This should change as Brexit is increasingly in the rear view mirror and corporate earnings improve. There is still considerable scope for a bounce-back trade in the UK. At Murray Income Trust, we are positioning to benefit from that.

Murray Income Trust is now in its 47thyear of consecutive dividend increases to shareholders. 2020 was certainly among the toughest, but we see many reasons to be optimistic about the year ahead.

Discrete performance (%)

Year ending

30/06/21

30/06/20

30/06/19

30/06/18

30/06/17

Share Price

18.5

(5.8)

13.2

3.3

23.5

Net Asset Value

20.8

(5.3)

7.9

3.9

16.7

FTSE All-Share

21.5

(13.0)

0.6

9.0

18.1

Five year dividend table (p)

Financial year

2020

2019

2018

2017

2016

Total dividend (p)

34.25

34.00

33.25

32.75

32.25

Important information

Risk factors you should consider prior to investing:

The value of investments and the income from them can fall and investors may get back less than the amount invested.

Past performance is not a guide to future results.

Investment in the Company may not be appropriate for investors who plan to withdraw their money within 5 years.

The Company may borrow to finance further investment (gearing). The use of gearing is likely to lead to volatility in the Net Asset Value (NAV) meaning that any movement in the value of the company’s assets will result in a magnified movement in the NAV.

The Company may accumulate investment positions which represent more than normal trading volumes which may make it difficult to realise investments and may lead to volatility in the market price of the Company’s shares.

The Company may charge expenses to capital which may erode the capital value of the investment.

Derivatives may be used, subject to restrictions set out for the Company, in order to manage risk and generate income. The market in derivatives can be volatile and there is a higher than average risk of loss.

There is no guarantee that the market price of the Company’s shares will fully reflect their underlying Net Asset Value.

As with all stock exchange investments the value of the Company’s shares purchased will immediately fall by the difference between the buying and selling prices, the bid-offer spread. If trading volumes fall, the bid-offer spread can widen.

Certain trusts may seek to invest in higher yielding securities such as bonds, which are subject to credit risk, market price risk and interest rate risk. Unlike income from a single bond, the level of income from an investment trust is not fixed and may fluctuate.

Yields are estimated figures and may fluctuate, there are no guarantees that future dividends will match or exceed historic dividends and certain investors may be subject to further tax on dividends.

Other important information:

Issued by Aberdeen Asset Managers Limited which is authorised and regulated by the Financial Conduct Authority in the United Kingdom. Registered Office: 10 Queen’s Terrace, Aberdeen AB10 1XL. Registered in Scotland No. 108419. An investment trust should be considered only as part of a balanced portfolio. Under no circumstances should this information be considered as an offer or solicitation to deal in investments.

Investment managers, both in the UK and US, are saying that companies without sustainable supply chains will receive less investment over the next decade.

This is according to a study carried out by procurement consultancy Proxima, who expect to see the share prices of the applicable businesses fall.

The report, published on 8 September, analyses supply chain sustainability through the lens of the investment manager.

The research found that over eight in 10 (85%) investment managers believe that businesses who do not implement supply chain sustainability initiatives will see share prices fall as a result over the next decade.

Investors are concerned about inaction, with 84% also stating that issues with supplychain sustainability and ESG standards are a risk to their investments.

There is overwhelming evidence that supply chain sustainability is at the top of the investor’s agenda with 97% of investment managers telling the firm they consider the sustainability standards of a business’ supply chain when making investment decisions.

Simon Geale, Executive Vice President at Proxima, said: “It is clear that investors have supply chain sustainability in their sights as we look to build a better post-pandemic world.”

“The concept of how a business can create value is changing, and business leaders are seeking to balance short term profit with progressing a broader range of ESG factors that will create sustained value in the mid-term. This trend is only set to continue and will dominate the coming decade; therefore, action now can create first mover advantage.”

“Supply chains are going to be at the heart of the change. They can be complex, and frequently are, but ultimately remain a key part of the solution along with innovation and collaboration. It’s vital that a business brings in the expertise it needs to address the challenge.”

Creating a family Trust is a route to establishing generational wealth.

It can do this by offering tax benefits and ensuring a family’s wealth is only used for suitable purposes.

What is a Family Trust?

It is a legal entity set up by an individual, or a ‘settlor’, to allow beneficiaries to benefit from funds. The beneficiary does not have to be the funds’ legal owner.

A trustee is then selected to manage the trust on behalf of the beneficiaries.

“A trust allows funds to continue to be protected should a Settlor become unable to manage their own affairs and even beyond a Settlor’s death,” said Peter Skelly, Senior Manager at ZEDRA, a wealth management company.

“If you are considering creating a family Trust, it can feel like a daunting task. The options available can seem overwhelming in terms of understanding what benefits a family Trust provides, what you should – and shouldn’t – put in the Trust, deciding who should be your Beneficiaries, and choosing your Trustees.”

“Trusts can be complicated structures with complex tax implications, so it’s important to seek expert advice if you’re considering setting one up,” Skelly added.

How Does a Trust Work?

With funds you do not need, you can gift them into the care of your trustees.

These funds are held specifically for the benefit of your selected beneficiaries. Typically this is children, grandchildren and future generations. The trustee is responsible for ensuring that the funds are invested and paid out according to the stipulations dictated.

“The Trustees will be steered by the Letter of Wishes you leave to them, which provides guidance to them on your overall goals and desires for the funds, as well as the circumstances of the Beneficiaries over the term of the Trust fund. They can then use their discretion to provide assistance at sensible times,” says Skelly.

“For example, when the time comes for the purchase of a first car or deposit on a first home, your family Trust will be there to assist and provide the support your loved ones need at crucial times.”

How to Create a Trust

A trust is created by a legal document called a trust deed. This sets out the terms on which your selected trustees must act and provides the basis on which they can use the funds for your beneficiaries in the future.

“Before creating your family Trust, you should carefully consider the Terms of the Trust Deed, choose your Trustees, and decide which assets you can afford to gift into it.”

Portfolios have been actively re-positioned following the pandemic

Temple Bar’s(LON: TMPL)new managers, Nick Purves and Ian Lance, have made a number of changes to the fund since taking over the mandate last November. The value-oriented investment trust has made a decent recovery, but despite the gains they still believe that UK shares continue to be valued at a marked discount to world equities.

One area that Purves and Lance have added to is the energy sector that is dominated by key holdings BP and Royal Dutch Shell, which they believe will be able to reduce their carbon emissio...

Coinbase CEO expresses concerns at treatment by SEC over long Twitter thread

The US Securities and Exchange Commission has warned Coinbase (NASDAQ:COIN) that it could face a legal challenge if it launches its proposed digital asset lending service.

Additionally, the regulator issued subpoenas to the crypto exchange seeking additional information.

In a detailed Twitter thread Coinbase CEO divulged his view on Coinbase’s actions while setting out the stool for his company in terms of its stance.

1/ Some really sketchy behavior coming out of the SEC recently. Story time…

“They are refusing to offer any opinion in writing to the industry on what should be allowed and why, and instead are engaging in intimidation tactics behind closed doors,” he wrote. “Whatever their theory is here, it feels like a reach/land grab vs other regulators.”

The tool in question, by the name of Lend, is constructed to allow Coinbase customers to earn interest on specific digital assets.

Paul Grewal, Coinbase’s chief legal officer, said it categorised the Lend product a security “but wouldn’t say why or how they’d reached that conclusion”.

The Nasdaq-listed crypto exchange announced back in June that it would be launching the product.

The SEC reacted by opening an investigation into the exchange and issuing it with subpoenas, Grewal said.

“Despite Coinbase keeping Lend off the market and providing detailed information, the SEC still won’t explain why they see a problem,” Grewal said. “Rather they have now told us that if we launch Lend they intend to sue.”

TP Icap saw a bounce in trading at the start of the pandemic

The huge shift in culture towards working from home has resulted in traders have less appetite for risk.

That is the view of TP Icap, one of the world’s largest brokers, as reported by The Times.

The company, which facilitates transactions in financial markets, said that its clients had been more cautious during the pandemic.

Senior staff at TP Icap said some traders were more hesitant towards specific trades, citing internet connections which could impact the audit trails for deals.

“You’re at risk in anything that’s high velocity of there being a breakdown,” Robin Stewart, TP Icap’s finance chief, said. “You could misreport it because your internet might go down.”

There have been murmurs among banks over putting in place tighter risk limits due to the challenges of monitoring traders’ activities when they are working remotely.

The reduced risk-taking led to a quieter period for markets over the first half of 2021.

TP Icap saw a bounce at the start of the pandemic, when trading activity boomed high volatility. However, more recently it has been held back as calmer conditions returned.

The broker’s share price fell by 21p, or 10.7%, after it said that its full-year operating margin was likely to fall year-on-year due to lower revenues and sterling’s strength against the dollar.

The FTSE 100 fell 0.8% to 7,090 while the major markets in mainland Europe suffered declines greater than 1% early on Wednesday.

“Economic growth fears have cast a black cloud over global markets, leading to some hefty share price declines across Europe on Wednesday,” says Russ Mould, investment director at AJ Bell.

Only five stocks on the FTSE 100 were in positive territory, led by Smiths Group which has received a better offer for its medical arm.

“Healthcare, industrials, real estate and financials led the FTSE 100 lower,” Mould added.

“Investors on the whole have enjoyed a fairly decent run this year, but now attention is turning from the post-lockdown spending splurge to how corporate earnings might fare next year.”

“There is a sense that some of the market forecasts have been too optimistic and so there could be some share price disappointment unless we see GDP figures pick up and the Covid Delta variant stops causing so much trouble.”

FTSE 100 Top Movers

B&M European Value Retail (3.81%), Smiths Group (1.58%) and Polymetal International (0.85%) are the top risers on the UK index on Wednesday morning.

While at the other end, Informa (-2.88%), Land Securities (-2.6%) and Taylor Wimpey (-2.43%), made the most substantial declines out of the FTSE 100 companies.

Zephyr will finish year having ‘exceeded expectations’ says CEO

Zephyr Energy (LON:ZPHR) confirmed on Wednesday that it reached an agreement for further investments in the Williston Basin, North Dakota.

The technology-led exploration & production company also revealed its plans to increase its working interests via a deal with Purified Resource Partners.

Zephyr Energy presently holds minority interests in seven non-operated production wells in the Williston Basin and has grown its portfolio through two further acquisitions.

Production from the seven wells was, net to Zephyr, 509 barrels of oil equivalent per day during August 2021.

Four of the wells continue to be brought into full production, with oil production still rising, water cuts reducing and stable gas oil ratios.

Zephyr’s first acquisition purchased 72.5 net acres, resulting in an average 5.6% working interest in four drilled but uncompleted wells operated by Prima Exploration Inc. which target production from the Middle Bakken reservoir in Richland County, Montana, U.S.

The second acquisition purchased an average 3.1% WI in 11 wells (one currently being drilled and 10 DUC wells) operated by Whiting Petroleum Corporation (“Whiting”), all of which target the Middle Bakken reservoir in Mountrail County, North Dakota.

Colin Harrington, Chief Executive of Zephyr, said: “While the safe and successful completion of the State 16-2 LN-CC well on our Paradox project remains the Company’s top priority, I’m delighted to report continued progress and significant growth on the non-operated side of our business.”

“As we outlined to Shareholders in January, Zephyr’s key goal for 2021 was to establish production and positive cash flow – either through our existing portfolio, via acquisition, or through a combination of both. We will end 2021 having significantly exceeded my expectations,” Harrington added.

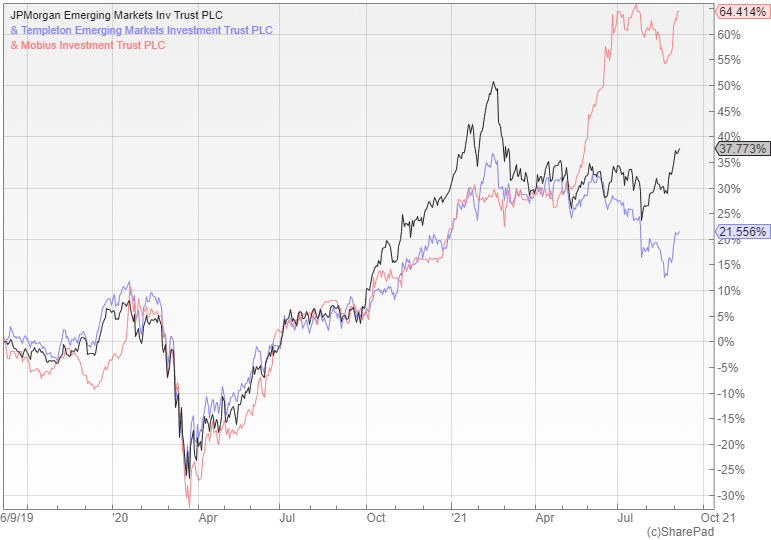

The region could be a major beneficiary of the pickup in global economic growth

Emerging market share prices have lagged behind their developed market counterparts since the pandemic inspired sell-off in March 2020 and could offer a buying opportunity. Some of these countries are currently being held back by the delta variant, but the longer term picture is more favourable with the expansion of the working age labour force and expanding middle class boosting their growth prospects, although China remains a key influence.

For those who want exposure to the sector the broker Winterflood recommends the £1.6bn JPMorgan Emerging Markets (LON: JMG) and the £2.2bn Templeton Emerging Markets (LON: TEM).

JMG provides a core exposure to global emerging market equities and is managed by the highly experienced Austin Forey who can draw on the extensive resources of JPMorgan in the region. Forey invests in high quality growth companies that Winterflood believe will allow it to outperform over the long run and has built up an excellent track record during his 27 year tenure.

Templeton is seen by many as the flagship trust in the sector due to its history, size and profile that allows it to attract both institutional and retail investors. It has a long-term, value-oriented approach based on bottom up stock picking, which makes it a good complimentary holding to the JPMorgan trust.

Those who are comfortable with a higher level of risk might want to consider the £152m Mobius Investment Trust (LON: MMIT) that holds a concentrated portfolio of 28 small and mid-cap stocks from across the region. It has done exceptionally well over the last 18 months due to strong stock selection and the managers are well motivated to succeed given that they hold around 15% of the shares.