Some companies seem to perpetually disappoint investors. Periods of hope are succeeded by yet another delay or problem. This means that when things are starting to appear more positive there is scepticism.

One company that has been on AIM more than two decades has managed to disappoint and just as importantly kept on coming back to the market for more cash appears to be finally on a positive course. It should be able to generate enough cash to ensure that there will be no requirement for a cash call for the businesses that are currently operated by the company.

The peak adjusted share price of...

Ireland-based industrial property and offices investor Yew Grove REIT (LON: YEW) managed to cover the additional costs of moving to the main Euronext market in Dublin from the Growth Market due to REIT regulation requirements. The AIM quotation is being retained.

The market move cost €900,000 and after that cost the interim pre-tax profit before property gains was still €2.52m on revenues of €6m. NAV edged up to €1.0064 cents a share.

Rental income has held up well with 99% of rents collected in the first half. There was also 20,000 square feet of vacant space lent earlier in the year. The ann...

Altus Strategies (LON: ALS) has reached a new point in its development. The acquisition of a mining royalty in Chile provides near-term income for the company, which has previously focused on developing mining projects.

This deal will provide cash to help to cover group overheads and it will be completed on 1 September. There could be further royalty deals.

Altus Strategies together with its 50/50 joint venture partner EMX Royalty is buying a 43% interest in SLM California, which owns a 1.944% net smelter royalty in the producing Caserones copper-molybdenum mine in Chile for $68.2m. The open p...

Individual traders, also known as the “retail” segment of the stock market, have been participating more in the financial markets as millions of people deemed investing as a potentially entertaining and rewarding activity during the pandemic.

In the United States alone, estimates point to retail investors accounting for at least a fifth of the daily trading volume of individual stocks while the latest short-squeezing frenzythat took place in February-March 2021 emphasized the extent of the impact that a now more prominently present group of individual investors could have in the price of a group of stocks.

That said, has a similar situation happened in the United Kingdom as well? Or is this a US-only thing?

In the following article, we take a look at the factors driving the retail trading boom in the United States while also assessing some trading statistics from the United Kingdom to see if the situation is similar or entirely different in the UK market.

Factors driving the US retail trading boom

One of the first variables driving an increase in the participation of retail investors in the financial markets is a reduction in trading costs. In this regard, platforms like eToro and Robinhood have pioneered this movement and, since the UK is among the list of eToro supported countries, British traders have also been able to benefit from this trend.

Moreover, the combination of government stimulus checks along with the increasing popularity of stock trading and investing in social media prompted millions of people to turn to the stock market with the expectation of multiplying those funds to a point that they become what some people have deemed as “life-changing gains”.

One of the markets that has attracted the interest of retail investors is the cryptocurrency market as reflected by the price of Bitcoin (BTC), which surged from an average of $10,000 per coin before the pandemic to an all-time high of more than $60,000 amid an increasing participation of both retail and institutional traders during the pandemic.

Meanwhile, in 2021, one of the strangest phenomenons that have emerged in the financial markets is the appearance of the so-called “meme stocks”, which are individual stocks that have attracted the interest of retail traders who spent their time sharing ideas in the popular Reddit messaging board Wall Street Bets.

This messaging board became a place where investors discussed their investment theses on multiple individual issues and back in February many posts that emphasized the possibility of performing a short-squeeze on a small group of stocks started to come up, including those of the global movie theater chain AMC Entertainment (AMC) and the used video game retail store chain GameStop (GME) – both of which were heavily shorted by institutional participants.

A successful short-squeeze took place with both names, and with many others for that purpose, and the investment landscape seems to have changed since then as now these “meme stocks” have become a recurring topic of conversation even in mainstream media talk shows due to the large gains that some investors have realized by trading these stocks while the move also inflicted some pain to the institutional funds that were betting against these companies.

As a result of this social phenomenon, retail investors have grown bolder, more knowledgeable, and perhaps even wealthier, and they now identify themselves as a paradigm-disrupting movement that is tipping Wall Street’s balance to help ‘the little guy’.

Is the UK stock market seeing a similar trend?

During the pandemic, the number of retail accounts in the United Kingdom seems to have grown as indicated by the performance of firms that provide brokerage services within the country like Hargreaves Lansdown.

In 2020 alone, the company reportedly added a total of 188,000 clients to its platform– a number that far exceed the average for the four preceding years while other statistics point to 20% of the total volume of FTSE All Shares orders being traced back to retail accounts during the first six months of 2020.

Even though the short-squeezing frenzy seems to be a US thing, the participation of retail investors in the UK does seem to have accelerated last year, although perhaps not to the extent seen in the United States.

Moving forward, experts are expecting to see a drop in retail trading volumes in the UK as this activity may no longer captivate the attention of people once other more traditional forms of entertainment become available once the pandemic situation ceases.

Telematics services provider Trakm8 (LON: TRAK) is on course to breakeven this year, following a period of disappointing trading. The share price has been in the doldrums for years and if the company can achieve the forecast profit for 2022-23 then it could bounce back.

Covid-19 delayed the return to profit even though the cost base has been reduced. It will happen next year if it does not happen this year. The main sources of revenues are fleet owners and insurance companies, that offer discounts to people who have the Trakm8 technology installed in their vehicle.

Trakm8 went through an acqui...

Aviation services provider John Menzies (LON: MNZS) is set to publish interim figures on 1 September. The trading statement at the end of July stated that trading is slightly ahead of expectations. That led to forecast upgrades and the results will provide further guidance to the prospects for the full year.

Europe has been a weaker market, but other regions have been stronger and have gained contracts. Cost control has helped Menzies to do much better in the first half of this year, although the comparatives were particularly weak due to Covid-19 lockdowns.

In the six months to June 2021, net...

It has been a slow process but linen hire company Johnson Service Group (LON: JSG) is finally on the way back to profit. Workwear demand held up fairly well but the linen hire for hotels and catering was hard hit by lockdowns.

The recovery is gaining momentum. Hotel and catering demand in June was back to more than 70% of previous levels – that is more than double the level three months before. Workwear demand is nearly back to normal levels. There will be more trading news with the interim results on 1 September.

Management should guide investors about the continued recovery over the summer m...

Jay Powell firmly suggested on Friday that the US Federal Reserve could begin to pull back on its large-scale pandemic-induced stimulus measures this year.

The Fed chair said that the bank has completed one of its two goals required to justify decreasing its support, adding that “progress” was being made on the other.

Powell reaffirmed his view that the US economy has rebounded strongly following the pandemic, while he said he is confident America is heading in the right direction to pull back on its high levels of support.

“My view is that the ‘substantial further progress’ test has been met for inflation,” Powell said on Friday. “There has also been clear progress toward maximum employment.”

Previous report suggests that officials at the Fed think that now is an appropriate time to begin “tapering” the bond-buying measures this year, which Powell has now agreed with.

“This year’s Jackson Hole agenda has focused on the word “uneven” and is reading ever more altruistic”, said Hinesh Patel, portfolio manager at Quilter Investors. “Monetary policy setters, researchers and influencers will be discussing frameworks that will influence our lives over the next decade, not just to get us through the pandemic. Powell’s speech is evidence that central banks are looking beyond the surge in Delta cases globally.”

“Since the global financial crisis, monetary policy and fiscal policy have been at a tug of war but today they clearly operate in tandem akin to synchronised swimming. The Federal Reserve has clearly decided now is the time for the fiscal response to take up more of the slack,” said Patel.

“Powell has been incredibly clear that tapering is coming later this year and they should now be prepared enough to avoid any sort of tantrum. But central banks will have to ultimately hold the hands of financial markets as we transition to a new era of monetary policy to ensure credit conditions remain optimal.”

Dollar

The US Dollar Index (DXY), which measures the greenback against a range of competing currencies, rose to 92.79 on Friday, a new four-day high.

The index made additional ground in response to aforementioned hawkish remarks from Powell.

The greenback surged until the beginning of this week, with the dollar index hitting a nine-month-high of 93.734 on Friday, on fears over the Delta variant’s economic impact.

Vasileios Gkionakis, global head of FX strategy at Lombard Odier Group, told Reuters that there’s been skittishness over growth and sector rotations, which has boosted the dollar because of its safe-haven status.

“In the short term, we’re still going to be trading in ranges, with upside bias,” Gkionakis added.

Gold

As Jerome Powell made his remarks about potentially pull stimulus measures this year, the price of gold rose to $1,800 per ounce.

$Gold prices pushed to $1,800 an ounce in initial reaction to #Powell's comments. December futures last traded at $1,800.90 an ounce, up 0.30% on the day.

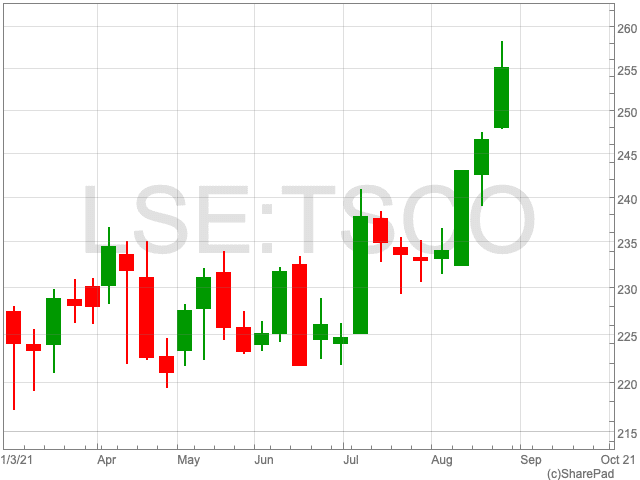

The Tesco share price (LON:TSCO), up by 0.79% on Friday, is set to close out its fourth consecutive week in the green. The supermarket chain has now added 8.79% in the past month. However, it remains some way off its level in February, when Tesco paid out £5bn to shareholders via a special dividend with the proceeds of the sale of its business arms in Malaysia and Thailand. On 12 February, the Tesco share price was at 304.76p, while today it stands at 255p per share. With close attention being paid to UK supermarkets by American private equity firms, investors will be keeping a close eye on the Tesco share price.

Takeover Talk

The Morrisons buyout has brought eyes to the sector, with both Tesco and Sainsbury’s seeing their stock values rise in recent weeks. However, while US private equity firms are keen on Morrisons, Tesco is a different proposition entirely. Over the past two years, Morrisons has been underperforming vs Tesco, meaning it represents better value for Clayton, Dubilier & Rice et al.

Analysts

A range of analysts, as reported by Stockopedia, have a positive outlook on the FTSE 100 company. Among seven analysts currently covering Tesco, seven have given a ‘buy’ recommendation, three a ‘hold’ and zero a ‘sell’. This may come as encouraging news to those holding the stock, although it must be noted that analysts are susceptible to fallibility just like investors.

Dynamo Motor Company manufacture The Dynamo Taxi, according to GOV.UK, the world’s only 100% electric zero emissions London black cab.

We are based in the automotive heartland that is Coventry.

Working in association with Nissan and in view of a legislation change on January 1st 2018, whereby Taxis could only be licensed in London if they were capable of travelling more than 30 miles with zero emissions, Dynamo created a first to market vehicle which currently only has one competitor, this being LEVC, which is a range extended vehicle i.e petrol and battery.

In the UK there are nearly 70,000 taxis of which some 4,000 have already converted to electric. Dynamo is competing for the other 66,000, worth around £4 billion, who over the next 10 years, driven by financial gain and a growing desire to improve the environment, will opt for an electric taxi.

Our Taxi uses Nissan’s fully electric eNV200 Evalia MPV as a donor vehicle that Dynamo converts to a fully certified and compliant London Black Cab.

FUNDRAISING –Limited Time to Invest

Dynamo is currently fundraising through Seedrs and has hit over 85% of target with over 600 investors. With the campaign closing on September 8th, now is the time to join us before it is too late and play an active part in reducing pollution whilst investing into an exciting EV company. To find out more and make your investment please visit www.seedrs.com/.dynamotaxi

AUTOMOTIVE TREND – Green Economy

The EV market is expected to grow at a CAGR of 33.6% from 2020 to reach $2,495.4 billion by 2027.

By volume, the EV market is expected to reach 233.9 million units by 2027, at a CAGR of 21.7%.

Global EV sales skyrocketed 43% to a total of 3.24 million vehicles sold compared to 2.26 million in the year 2019.

Compound Annual Growth Rate – (CAGR).

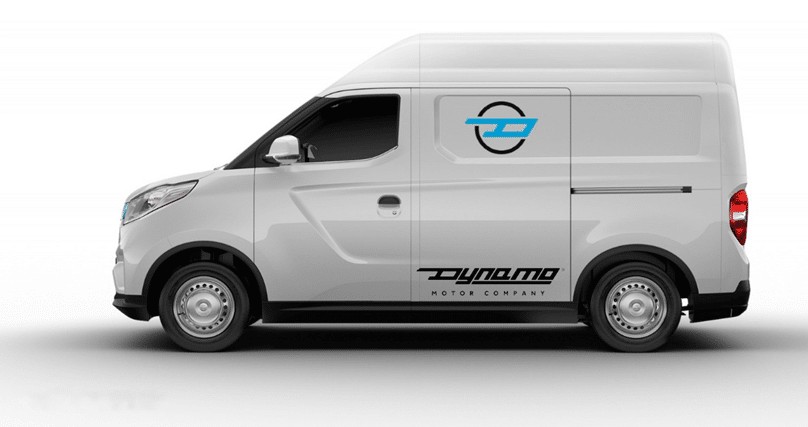

SECOND PRODUCT– Don’t go long, go up!

With £1.5 million investment secured from our partner Gluon Mobility Ventures (formed by Max Delamain and Per Regnarsson, owners of Gluon Capital and long-term investors and advisors in the sustainable energy markets), Dynamo have accelerated strategic diversification development plans and brought forward our second product, working with Maxus, a fully electric increased cargo volume (m³) last mile delivery van for launch August 2021.

Dynamo has entered this market with an innovative product whereby cargo volume increases to 6 cubic metres on a Short Wheelbase Van enabling better ease of use in congested traffic, better parking attributes and of course an option for couriers to load larger volume parcels.

Coronavirus accelerated the transition to an increased level of purchases online, which is something we believe will be maintained and as such, last mile delivery vehicles will therefore increase in numbers on the road.

Working with our experienced engineers we have developed an option for fleet owners that offers them greater flexibility and brings forth our slogan, don’t go long, go up!

SUBSTANTIAL ACCOMPLISHMENTS TO DATE– Keeping Pace in the EV Era

Dynamo attained international converter status within Nissan Motors in 2017 meaning that Dynamo could officially convert and sell Nissan products.

Whole vehicle type approval (M1 Certification) was attained in August 2019.

Transport for London Taxi Approval was attained in August 2019.

The Dynamo Taxi was launched with Nissan at City Hall October 2019 and is still the world’s only certified 100% electric zero emission black cab.

The Mayor of London who attended the launch said this of The Dynamo Taxi “London’s black cabs are known around the world, which is why I am pleased to launch the first all-electric London black cab by Dynamo. Working with cabbies to go electric is a key part of our plans to improve London’s air quality. The Dynamo Taxi will accelerate the retirement of polluting diesel taxis from city streets across the UK, improving air quality, helping to tackle the climate emergency and to create a green economy”.

The product has so far had over £10,000,000 spent on its development.

In September 2020 after €560,000 investment at Nissan’s Barcelona Plant, the first vehicle built specifically for Dynamo, whereby Nissan completed some of the conversion steps was delivered to Dynamo. This collaborative working enabled Dynamo to speed up production.

Dynamo has to date sold 250 vehicles with sales being in London, Liverpool, Coventry, Sheffield and Nottingham. Dynamo now has a waiting list for future deliveries.

March 2021, Dynamo received an order from the Welsh Government for 50 ‘try before you buy’ Taxis. The last of these taxis were delivered in May 2021 and Dynamo have now received subsequent orders from Wales.

The launch of Dynamo’s second product, working with Maxus, a fully electric increased cargo volume (m³) last mile delivery van in August 2021.

USE OF PROCEEDS– Putting your money to work

Acquisition of donor vehicles from Nissan.

Acquisition of additional parts and equipment from a localised supply chain.

Dynamo will increase its workforce, therefore incur recruitment costs.

The launch and productionization of Dynamo’s second product, the fully electric Maxus increased cargo volume (m³) last mile delivery van.

Dynamo is currently working with the Nissan / Renault Alliance to develop a second Taxi product.

Dynamo will fund its diversification strategy and will increase its relationships with large automotive manufacturers as well as operate in other market sectors.

You have the opportunity to play an active part in a changing automotive world, where carbon neutral targets for 2030 have created huge business opportunities for companies like Dynamo that manufacture electric vehicle solutions. Change is not coming, it is here, so join us as together we play a part in reducing pollution and build a sustainable U.K. manufacturing company that embodies what the green economy is all about.

If you would like to invest now or find more information, then please use the following link.