{kind=link}

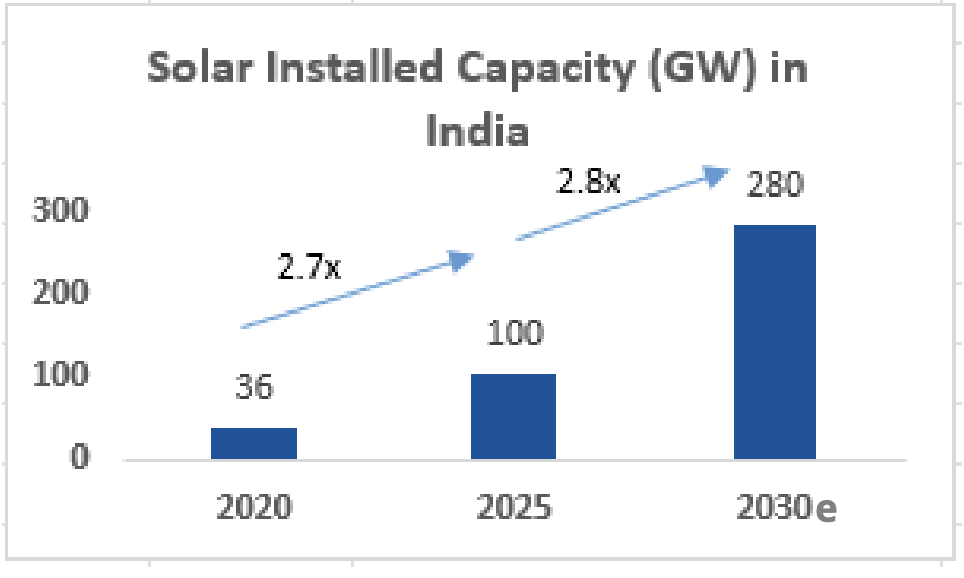

India stands at the cusp of an energy transformation. Once plagued by power shortages, the country now aims to become a global leader in renewable energy, targeting a massive 500 GW of renewable capacity by 2030, with solar energy contributing 280 GW to this ambitious goal. To give some context, UK’s renewable energy capacity stands at 60 GW in 2024. Traditionally a coal-driven energy market, this solar-first approach leverages India’s natural advantage of abundant sunshine and the continuously declining cost of solar power generation. With solar renewable energy cheaper than coalfired power, it presents a win-win positioning for India to simultaneously address climate change concerns while meeting the country’s growing demand for power.

Source: Govt of India – Press Information Bureau MNRE: Year End Review, Dec 20. MNRE: Press Release: 2100603, Feb 25. Grant Thornton Report, Achieving 500 GW of renewable energy capacity by 2030, 2024. e indicates estimate.

The Solar Value Chain in India

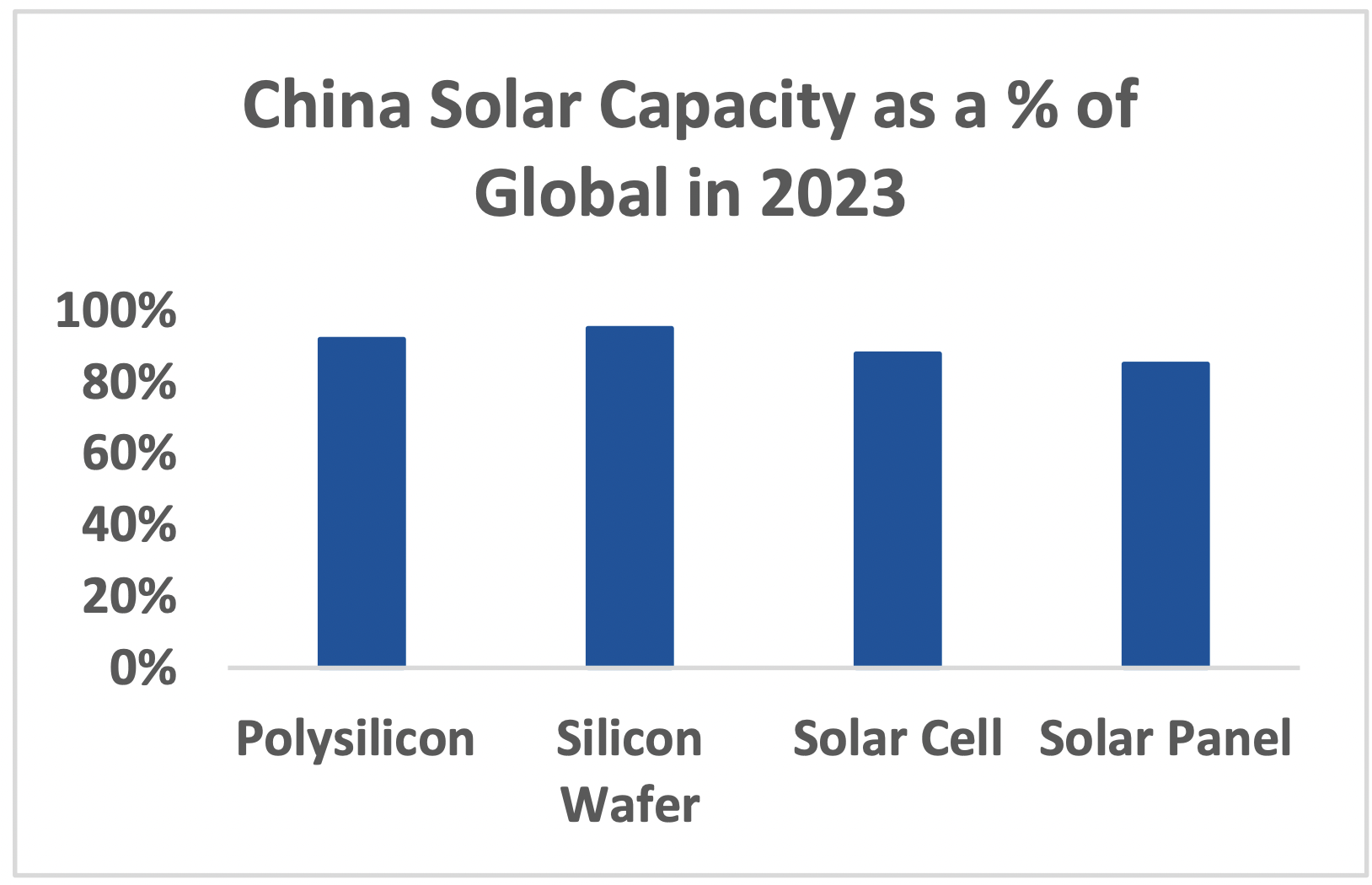

The solar industry value chain consists of multiple stages: polysilicon production, ingot and wafer manufacturing, solar cell production, and finally, panel assembly. Currently, most Indian companies operate only in the final stage of solar panel assembly—the least technologically and capital-intensive part of the manufacturing process. This limited participation in the value chain creates significant vulnerability and dependence on imports, particularly from China, which controls approximately 80% of the global solar supply chain.

This dependence is now changing with backward integration into silicon wafer and solar cell manufacturing becoming the new buzzwords among Indian companies. With companies having achieved scale and profitability in panel manufacturing along with end product prices stabilising, companies no longer see price declines as a risk to their capital investment and are thus investing in capital expenditure. This vertical integration process is accelerating thanks to the government. Not only has the government provided a long-term vision on the size of the opportunity, but it has also actively incentivised the growth of the industry through various initiatives such as domestic content requirements for government projects, substantial import duties (40% on imported solar panels and 25% on imported solar cells), and Production Linked Incentives (PLI) to encourage manufacturing scale-up. New market opportunities have also been created by incentivising solar pump and rooftop solar projects in both rural and urban India.

In an effort to understand Indian companies’ positioning, we visited the plants of two leading companies, Adani Solar and Waaree Energies and were amazed by the sheer scale and size of the state-of-the-art fully automated plants. Their investments demonstrate the seriousness with which Indian players are approaching vertical integration and technological advancement in this sector.

From an investor’s perspective, the Indian market offers diverse investment opportunities across the solar ecosystem with pure-play manufacturers, independent power producers (IPPs) that develop and operate solar plants, as well as engineering,= procurement, and construction (EPC) companies that implement solar projects. This variety allows investors to participate in different segments of the value chain according to their risk appetite and return expectations.

The story doesn’t stop here. India’s vision is to not only be self-reliant but also become an important export hub for renewables in the world for those looking for an alternative source to Chinese solar products. The US is one of the biggest importers of solar cells and panels. With restrictions on China, this opens up a great avenue for India and it is highly profitable too. In FY24, India’s solar products exports to the US were almost $2bn.

So, is it all Sunshine?

Having interacted with a dozen of the listed companies across the ecosystem, our main concern remains China and its dominance across the value chain ranging from polysilicon to cells.

Source: CLSA, CPIA, Companies, Dec 23

Irrational behaviour can have a domino effect. The dependency is not only in the supply chain but also in technological know-how where China is a leader and innovator. As Indian companies backward integrate, the capital intensity also increases, putting at greater risk the investment whenever there is a change in technology, which typically happens every five years. Our other concern stems from domestic competition. The entry barrier in module manufacturing is low, with the capital expenditure for 1GW of solar module manufacturing capacity at approximately $31 million (INR 2.5 bn). This has attracted a lot of companies, including first-time entrepreneurs, to set up capacities. Hence, it is a highly competitive industry. With the entire ecosystem backward integrating, the buyer/seller equation is itself undergoing a change. Supply is catching up with demand quickly. Consolidation seems inevitable.

The key question remains how we participate in this theme of renewables. We have absolutely no doubt that solar renewable energy is the answer to meeting India’s rising power demand of 6-7% per annum. Solar addresses all the fundamental requirements of cost, time, ease of usage, scalability and, of course, ample sunshine. As the industry evolves, we are in a wait-and-watch mode, closely tracking the business models and leaving no stone unturned to identify the eventual winners. There also remains an extended ecosystem of transmission, battery, glass and other inputs riding piggyback on the solar growth story.

Important Information:

The information in this document does not constitute or contain an offer or invitation for the sale or purchase of any shares in the Fund in any jurisdiction, is not intended to form the basis of any investment decision, does not constitute any recommendation by the Fund, its directors, agents or advisers, is unaudited and provided for information purposes only and may include information from third party sources which has not been independently verified. Interests in the Fund have not been and will not be registered under any securities laws of the United States of America or its territories or possessions or areas subject to its jurisdiction, and may not be offered for sale or sold to nationals or residents thereof except pursuant to an exemption from the registration requirements of the U.S. Securities Act of 1933, as amended (the “Securities Act”), and any applicable state laws. While all reasonable care has been taken in the preparation of this document, no warranty is given on the accuracy of the information contained herein, nor is any responsibility or liability accepted for any errors of fact or any opinions expressed

herein. Past performance is not a guide to future performance and investment markets and conditions can change rapidly. Emerging market equities can be more volatile than those of developed markets and equities in general are more volatile than bonds and cash. The value of your investment may go down as well as up and there is no guarantee that you will get back the amount that you invested. Currency movements may also have an adverse effect on the capital value of your investment. Investing in a country specific fund may be less liquid and more volatile than investing in a diversified fund in the developed markets. This Fund should be seen as a long term investment and you should read the London Stock Exchange Listing Prospectus published in December 2017 (the ”Prospectus”) whilst paying particular attention to the risk factors section before making an investment. Please refer to the Prospectus for specific risk factors. Where reference to a specific Class of security is made, it is for illustrative purposes only and should not be regarded as a recommendation to buy or sell that security. This document is issued by RGI Fund Management (referred to as River Global) and views expressed in this document reflect the views of River Global and adviser Saltoro Investment Advisors Pvt Ltd as at the date of publication. This information may not be reproduced, redistributed or copied in whole or in part without the express consent of River Global and River Global Investors LLP is authorised and regulated by the Financial Conduct Authority in the United Kingdom. River Global Investors LLP is a signatory to the UN Principles of Responsible Investment.