First Property shares (LON: FPO) were down over 5% on Thursday as the group reported a 30.2% drop in pre-tax profits.

For the six months to 30 September 2020, the group reported a fall in profits from £3.0m to £2.1m.

The group reduced net debt from £57.19m in March to £19.83 and also increased net cash reserves to £21.21m.

Commenting on the results, Ben Habib, Chief Executive of First Property Group, said: “The sale of Cha ubińskiego 8 (CH8) in April released some GBP17 million in cash and put the Group in a strong position from which to navigate the economic fallout of the COVID pandemic.

“As a consequence of the sale there has been a reduction in rental income, which is the primary reason for the reduction in earnings reported today.

“This reduction should be temporary and last only until we reinvest the cash. We expect to do so in association with clients of the Group. Our aim is to invest some 10-20% of the equity required in any acquisition which, when coupled with bank debt, should enable us to acquire up to some GBP300 million in property.

“There is a great deal of flux in the market at the moment and we expect interesting opportunities to emerge next year,” he added.

Trading platform, IG Prime, published a white paper laying out the views of 253 hedge fund managers, on which sectors are most likely to grow over the next twelve months.

Within the 41-page document, titled ‘Hedge fund trends: Covid-19 vs the global financial crisis’, 73% of those surveyed said that health and pharma will increase in value – making it hedge fund managers’ top ranked sector for growth over the next year. This, the report states, should come as little surprise given the attention and resources thrown behind COVID vaccine candidates, as well as treatments and PPE.

Similarly – and perhaps surprising to some – the airline and travel sectors ranked as the third most likely sector to grow during 2021, within 50% of hedge fund managers and 82% of UK investors backing a resurgence in the pandemic-suffering sector.

With EasyJet recording a 200% increase in flight and holiday package searches over the Christmas period, the easing of travel restrictions should provide a boost over the year-to-year transition period – though the longevity of these relaxed measures remains to be seen.

IG said that financiers’ outlooks were largely positive, with 52% of hedge fund managers and 94% of UK investors surveyed saying that it was ‘very unlikely’ that COVID will affect their funds’ performances over the next ten years.

Here is the full list of hedge fund managers views on the likelihood of an increase in value over the next 12 months will be for the following sectors:

Tech service provider to the promotional products industry, The Pebble Group (AIM:PEBB), watched its shares soar on Thursday as it published a performance update illustrating determined performance during the pandemic, and revealing that full-year results were on track to meet market expectations.

Its Facilisgroup segment – an ecommerce platform for promo products businesses in North America – performed ‘robustly’ through the COVID crisis. Its number pf participating partners rose from 149 to 169 during the year-to-date, with an additional 6 contracted and awaiting implementation.

Gross Merchandise Value processes by it partners are now expected to hit $1 billion by the end of 2020, which would make Facilisgroup a ‘major consolidator’ in the promo [products industry. Similarly, partners’ sales are returning to pre-pandemic levels, with this indicating a positive outlook for the promo products industry in 2021.

The company’s statement added: “We continue to invest in Facilisgroup to further improve its valued services to Partners and Preferred Suppliers and are increasingly positive about the business’ prospects.”

Its Brand Addition segment – which provides promo products and related services to large brands – have ‘continued to improve’ since the update delivered in September, with the two major clients secured in Q1 now successfully launched and contributing to FY20 revenue.

So far during the second half of 2020, sales orders have averaged 70% of the previous year, though the company noted that there was positive momentum going into 2021.

Pebble Group stated: “We believe this demonstrates the inherent strength of our clients’ businesses and their appetite for our products and services. Client retention has remained strong with all major clients that entered the COVID-19 affected period in March 2020 continuing to be clients today.”

In total, the company said its balance sheet remains strong. Having paid off £6.5 million of its £10 million credit facility since its last update, the group said it expects to have repaid all of the outstanding sum by the end of the year. It added that it expects its cash balance to be similar to the prior year position of £8.9 million, after a settlement of £2.4 million of IPO costs included in the previous year’s balance.

Looking ahead, the Pebble Group outlook read: “Facilisgroup continues to deliver in line with expectations and we are actively seeking opportunities to build on this success by strengthening its services organically and through acquisition.”

“The current trend in order patterns of Brand Addition’s blue-chip client base gives us real confidence as we approach 2021.”

“Coupled with a strong balance sheet and the long-term nature of our Partner and client relationships, we are confident in managing the Group responsibly through the current volatility, meeting market expectations for FY 20 and continuing to deliver on the Group’s strategy in FY 21 and beyond.”

Following the update, the company’s shares rallied by 20.66%, to 104.38p apiece 26/11/20. This is below its post-lockdown high of 115.00p, but ahead of its recent nadir of 71.00p a share.

TClarke PLC shares (LON: CTO) surged almost 13% on Thursday as the group released its latest trading statement.

The group said in a statement that trading has been resilient and that trading continues in line with expectations for the full year ending 31 December 2020.

TClarke PLC anticipates turnover for 2020 to be circa £240m. Over the second half of the year, the group has won new projects from clients and the forward order book has increased by 17% to £422m.

Mark Lawrence, the group’s chief executive said: “TClarke has once again demonstrated the direct benefits of our excellent reputation within our industry that has helped drive our clients’ continued confidence to work with us and award the Group significant new projects.

“Looking to the future, we have a well-balanced approach to winning work with projects from a range of sectors and I am delighted that we have been so successful in the Healthcare and Technology sectors in particular.

“The UK Government recently announced a long-term commitment to developing further green initiatives covering clean energy, transport, nature and innovative technologies, that will help the UK to forge ahead with eradicating its contribution to climate change by 2050. TClarke is well positioned to benefit from these initiatives and is already working on a wide range of exciting projects that support these moves.”

Alan Green joins the UK Investor Magazine Podcast as we explore the key influences on the FTSE 100 including vaccines, Brexit, Sterling and Rishi Sunak’s latest spending plans.

We also discuss in detail Power Metal Resources (POW), Venture Life Group (VLG) and Itaconix (ITX).

Mulberry shares (LON: MUL) opened higher after the group posted reduced half-year losses in twenty-six weeks ended 26 September 2020.

In the latest trading update, the luxury retailer said that sales were hit by the most recent lockdown and fell by 19% in the eight weeks to October.

As store closures and reduced demand amid the pandemic hit the retailer, revenue was down by 29% to £48m. Digital sales increased by 68% from £13.9m to £23.4m.

Mulberry chief executive, Thierry Andretta, said:

“I am proud that in spite of the devastating effects of the global pandemic, we have made further progress on our long-term strategy to build Mulberry as a sustainable global luxury brand. This is focused around: a truly omni-channel network and market leading digital platform, increased presence in Asia, and a relentless focus on innovation and sustainability, offering our customers beautiful products, made to last in our Somerset factories.

“This strategy enabled us to withstand some of the pressures that we, and indeed the wider retail and hospitality sectors, have been faced with. In particular, using our market leading global digital network to replace retail sales with digital wherever possible, achieving high growth in China and Korea, and reacting quickly to flex our agile supply chain, enhancing market reactivity and reducing lead time, to match the increase in digital demand.

“In spite of all of these self-help measures, we cannot avoid the fact that the damage the coronavirus has caused to business, decimating high streets and the tourism industry, is severe. For this reason, in order to ensure that the business was able to navigate through this difficult time, we took the painful decision to implement a far-reaching cost reduction and optimisation programme.

“As we look to the future, we remain confident in our strategy and in the relevance and durability of the Mulberry brand. There are of course many obstacles ahead, not least the upcoming changes to tax-free shopping in the UK that could hamper the wider retail and economic recovery, but we are grateful to be able to open our doors again in England on 2 December and to be able to trade across all our platforms in this crucial Christmas trading period. I would like to take this opportunity to thank my colleagues for their resilience, their hard work and their dedication to Mulberry.”

Mitchells & Butlers (LON: MAB) said today that it has cut 1,300 jobs this year after the group reported a £123m pre-tax loss for the year to 26 September.

The pub and bar operator, which owns chains including Toby Carvery, All Bar One, and Harvester. The group said that store closures and lower levels of sales amid the pandemic led the group to swing from a £177m profit in the same period a year ago.

Earlier this year, Mitchells & Butlers said that it would close 20 of its 1,700 sites across the UK.

“Throughout a very uncertain and challenging year our businesses and teams have adapted quickly, creating a safe environment for guests and putting us in a strong position to benefit when consumers are able to eat out again. We saw direct evidence of this from a strong trading period in July and August before further restrictions came into force,” said chief executive Phil Urban.

“With our great estate, balanced portfolio of brands and proven management team, we remain optimistic that we will be able to regain the momentum previously built and continue to achieve sustained market outperformance, when the current operating restrictions are eased.”

This year has seen the rise of hydrogen fuel cell backers such as Nikola Corp and Plug Power, and recent entries from forward-thinking blue chips like Hyundai. In fact, the latter is committed enough that in October, it announced that it would use around 70,000 ounces of platinum per year in its fuel cell stacks by 2030 – with this demand alone being equal to the total annual production of one of South Africa’s biggest platinum mines.

This commitment, though non-binding, may well be a sign of things to come. Though Nikola Corp investors are nervously awaiting confirmation of a $2 billion deal with GM, the idea that hydrogen fuel cells could operate a considerable portion of non-fossil-fuel market share within the next decade is not out of the question.

Indeed, this week marks the first ever European Hydrogen Week, which is designed to showcase the role of hydrogen fuel cells within achieving the EU’s ‘Green Deal’ objectives. Under the deal, there is an initiative which roadmaps new jobs and sustainable growth under a new, hydrogen ecosystem, which includes a pledge to install at least 40GW of hydrogen electrolysers by 2030. With this goal in mind, the EU plans to produce around 10 million tonnes of ‘green’ hydrogen per year.

The greatest limiting factor of hydrogen fuel cells – other than the process of achieving scale – is the initial shock factor of costs. Fortunately, the Platinum World Investment Council just reported that a more efficient and cost-effective platinum-iridium catalyst has just been developed.

The new technology requires 90% less iridium than previous Proton Exchange Membrane electrolysers, while performing ‘up to three times better’. According to the Platinum World Investment Council, the new technology: “not only reduces costs, making green hydrogen production at the scale envisaged by the EU’s Hydrogen Strategy more affordable, but also removes concerns about the availability of iridium, of which only a small amount is produced annually, ensuring PEM electrolysers remain at the forefront of electrolyser technology as the market expands.”

With the new catalyst technology, and its reduced iridium requirements, PEM electrolysers stand a better chance of widescale adoption – and in turn, this would bring increased demand for platinum. In fact, FTSE 100-listed chemical specialists, Johnson Matthey, believe that PEM electrolysis could achieve 30-60% market share.

The Platinum World Investment Council concluded by saying that: “Platinum’s role in the hydrogen economy is crucial both throughout the EU and beyond; it is used in fuel cells for fuel cell electric vehicles, as well as in the production of green hydrogen. The global platinum demand impact of announced green hydrogen policies is clearly sizeable over the longer-term; current EU and China green hydrogen generation capacity targets alone would require, cumulatively, between 300 koz and 600 koz of platinum by 2030.”

Following the commencement of the EU’s Hydrogen Week, platinum prices rose by 0.94% on Wednesday, up to over £725 per ounce.

On Wednesday, Chancellor Rishi Sunak set out his spending review detailing how much will be spent on public services, lamenting the “economic emergency” that the UK government faces as the coronavirus pandemic rages on. He explained the measures the government is putting in place to “protect people’s jobs and incomes”, with a £280 billion pledge to see the UK through this year alone.

What are the main points to take away from the spending review?

Kevin Courtney, Joint General Secretary of the National Education Union, stated that public sector employees were owed a pay rise by the government for their service during the coronavirus crisis:

“This is a predictable attempt at divide and rule in the middle of a pandemic. Police officers, prison officers, school support staff, teachers, head teachers, DWP workers, hospital ancillary staff, have all put their lives on the line this year and they all deserve a pay rise. So should the delivery drivers for big supermarkets. We are supposed to be all in this together as working people”.

Mr Sunak did, however, guarantee that 2.1 million public sector workers earning below the median wage of £24,000 will receive a £250 pay rise – although this is well former Labour leader Jeremy Corbyn’s proposition of a 10% pay rise for public servants, to “begin to make up the ground they’ve lost over the last ten years”.

More than 1 million NHS staff will reportedly be eligible for a raise.

In addition, the minimum wage – now rebranded as the National Living Wage – will see a 2.2% (19p) increase to £8.91 per hour for those aged 23 and over.

While Mr Sunak did not comment on the much-anticipated tax hike to accommodate extra government spending, the threat has by no means disappeared. Research by the Interactive Investor shows that most think it is still firmly on the cards.

What do investors make of a potential tax rise?

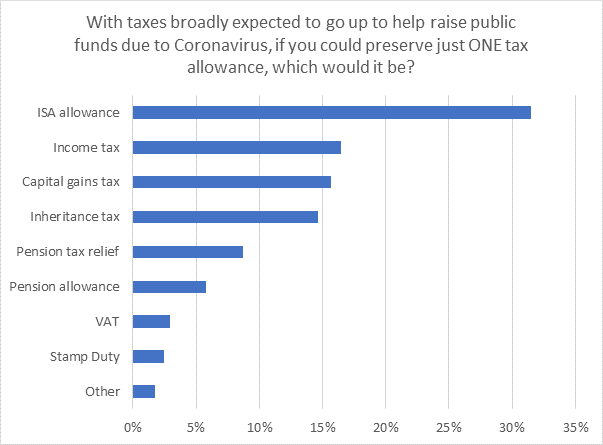

A snap poll orchestrated by the Interactive Investor – the UK’s leading flat-fee investment platform – ahead of the spending review’s release found that just under a third (31%) said that if they could preserve just one tax allowance, it would be the ISA allowance. Income and capital gains taxes settled in joint second place (16%), and inheritance tax (15%) in third.

Only 9% of investors said that they would prioritise pension tax relief from efforts to help raise public funds, 6% the pension tax allowance, 3% VAT, 2% Stamp Duty, while another 2% of respondents cited other forms of taxation.

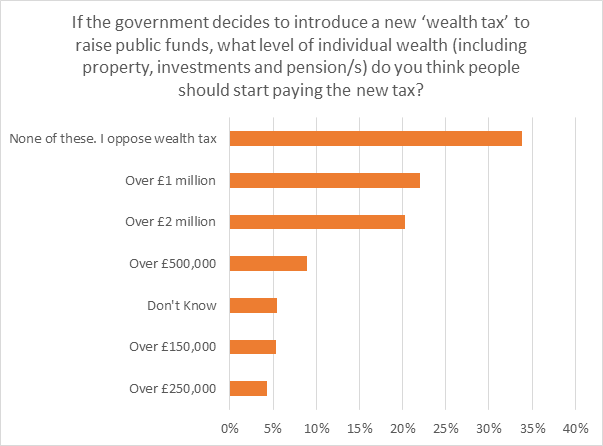

When asked who should pay for any new wealth taxes to raise public funds, just over two-fifths (22%) said “those with assets worth £1 million or more”, while 20% believe the starting threshold should be £2 million, and 9% said “over £500,000”. Only 5% said that the new tax should apply to “those with assets worth £150,000”, and fewer (4%) prefer the £250,000 threshold.

However, the largest percentage of respondents (34%) said that they were opposed to “any form” of wealth tax. The remainder (5%) said that they didn’t know.

Research and chart courtesy of Interactive Investor, 25 November 2020.

Research and chart courtesy of Interactive Investor, 25 November 2020.

Becky O’Connor, Head of Pensions and Savings at Interactive Investor, commented on the findings:

“With so many question marks around where the money will come from for this gigantic multi-billion pandemic bailout, investors will be waiting with bated breath for next year’s Spring Budget to see where the axe will fall.

“This could be a good time to make sure investments are as tax-efficient as possible, using ISAs and SIPPs and maximising any allowances if that’s possible – and with unemployment set to soar further, it’s time to start shoring up your finances if you haven’t yet started. If you can’t save more, it’s worth looking at areas where you can save money, by shopping around for better deals in all aspects of your life”.

Myron Jobson, Personal Finance Campaigner for Interactive Investor, added that the government’s ambitious measures will inevitably trickle down into the public pocket:

“Savers and investors will be breathing a sigh of relief as the much-mooted ‘wealth tax’ failed to materialise in the Spending Review. However, it is surely a question of when, not if a tax hike will be announced as part of efforts to address the Government’s WW2-sized public borrowing bill for its Covid-19 economic support packages.

“The extent of the economic uncertainty means that the Chancellor focused on the direction of public spending for the next 12 months. A cocktail of spending cuts and tax rises to get the UK economy back on an even keel from the damage done by the coronavirus crisis remains on the cards. The announced public sector pay freezes is a tell-tale sign of the difficult measures to come”.

House prices will likely fall early next year when the stamp duty holiday ends and the furlough scheme winds down.

The Office for Budget Responsibility has said the current boom since the first lockdown will come to a close as the UK will see a spike in unemployment.

“House prices fell briefly as the pandemic struck, but recent indicators suggest they have subsequently recovered quite strongly,” said the Office for Budget Responsibility.

“This follows the easing of public health restrictions and the stamp duty holiday for residential property transactions that took effect on 8 July 2020. House prices are expected to fall back in 2021, driven by end of the stamp duty holiday and the hit to household incomes from the labour market adjustment that we assume will follow the end of the Coronavirus Job Retention Scheme.

“Despite a steady recovery from 2022 onwards, the level of house prices remains around 17 per cent lower at the forecast horizon compared to our March forecast,” it added.

However, the housing boom is expected to continue into the first three months of 2021 before the stamp duty holiday and furlough scheme ends.

The property website Zoopla has estimated a further 100,000 houses to be sold in the first three months of next year. The number of new sales is currently 38% higher than it was a year ago.

Richard Donnell, director of research and insight at Zoopla, explained: “It has been a rollercoaster year for the housing market which is ending on a strong note with demand and sales agreed still more than 30% higher than this time last year.”