FTSE 100 falls as negative oil prices raise fears of wider market turmoil

The FTSE 100 fell on Tuesday as global markets tried to make sense of an oil market that traded negatively for the first time in history.

In the US trade overnight, the front month May WTI oil contract traded as low as $40.23 per barrel before recovering to trade in positive figures as the contract approached expiry.

The FTSE 100 was down 2% to 5,696 in mid afternoon trading on Tuesday as London’s leading index was dragged lower by commodity shares.

Admiral refunds customers for driving less during COVID-19 crisis

Admiral said on Tuesday that it will be providing a refund to its customers as they are staying at home and driving less during the COVID-19 crisis.

The UK government announced stricter lockdown rules last month to encourage people to stay indoors and practice social distancing.

Admiral will automatically issue a £25 refund to all customers for each car and van covered with its insurance.

The British insurer said that it is expecting fewer claims seeing as there have been a reduced number of cars on the road over the lockdown period.

A total of £110 million in refunds will be returned to 4.4 million vehicles.

Admiral added that it is supporting its staff during this period of uncertainty by continuing to pay all employees their full salary, and no staff are being furloughed.

“During this challenging period, our main priorities have been helping our customers, supporting our local community and protecting the wellbeing of our staff, which is why we have introduced these initiatives to give something back to the customers and communities we serve,” Cristina Nestares, CEO of UK Insurance at Admiral, said in a company statement.

“This is an unprecedented time when people across the country are driving significantly less than before the lockdown, and we expect this to lead to a fall in the number of claims we are seeing.”

“We want to give the money we would have used to pay these claims back to our loyal customers in this difficult time. We have also already reflected this change in driving behaviour in our pricing for customers and will continue to do so.”

Cristina Nestares continued: “The Admiral Stay At Home Refund was launched to recognise the considerable efforts people are making by staying home as much as possible and as a result driving less. Customers don’t have to contact us to receive this, we’ll be in touch with them in the coming weeks to explain how we’ll refund them.”

Just Eat to deliver free food parcels to vulnerable people

Just Eat revealed this week that it will deliver free meals to vulnerable people and those who have been isolated following the outbreak of COVID-19 in the UK.

As the crisis continues to develop in the UK, many people are vulnerable to the illness and have had to take special care when social distancing.

The UK government introduced stricter lockdown rules last month to ensure everyone follows social distancing rules.

With many finding themselves isolated and lonely during a time of significant uncertainty, Just Eat has teamed up with the charity FoodCycle to deliver food parcels to those most in need.

The service will be supported by delivery partner Stuart, Just Eat said.

In addition to this measure to help those impacted by the virus, Just Eat recently introduced discounted meals for NHS workers.

“As the UK’s leading food delivery business, we’re committed to doing our bit and supporting the vulnerable in our communities,” Andrew Kenny, UK Managing Director at Just Eat, said in a statement.

“With millions doing the right thing and staying at home, this service has never been more important. We are proud to be able to provide continued support to FoodCycle, and make a difference for those who need it the most,” Andrew Kenny continued.

David Saenz, Chief Operating Officer at Stuart, also provided a comment: “We are excited to be partnering with FoodCycle and Just Eat to help deliver meals to the most vulnerable members of the community in Birmingham. Being able to work together with our courier partners on such a rewarding mission is a privilege. At a time like this, we are thrilled to contribute to all of the efforts being made UK-wide to support each other.”

FoodCycle usually provides community meals using surplus food, but the service has now been adapted to adhere to the UK’s social distancing rules.

The service will now be delivery-only and will provide food parcels made up of donated surplus food.

John Lewis Partnership warns trading hit by COVID-19

The John Lewis Partnership said on Tuesday that its short term trading has been “significantly affected” by the COVID-19 crisis.

As the outbreak of the illness continues to spread in the UK, the government has introduced stricter lockdown measures, closing all non-essential shops.

Sales at John Lewis have declined by 17% year-on-year since the middle of March, and have dropped by 7% year-on-year since 26 January.

As all of its stores are shut, online sales at John Lewis have risen by 84% since the middle of March, with high demand for products related to working and living at home.

However, the John Lewis Partnership said that this has not been enough to offset the loss made by the closure of its stores.

Meanwhile, Waitrose has seen sales grow by 8% since 26 January and cupboard essentials have been particularly popular.

“Our short term trading has though been significantly affected, principally because of the closure of all 50 John Lewis branches,” Chairman Sharon White told partners in a statement.

“John Lewis online remains open – providing essential goods and services to enable customers to live well at home – and online sales are substantially up on last year. But it has not been enough to offset the loss of shop trade. Demand at Waitrose has risen sharply but operating costs have increased too, especially as we have expanded online delivery,” the Chairman continued.

The retailer added that, given the uncertainty surrounding the duration of the COVID-19 crisis, its full year performance is difficult to predict.

Looking ahead, the John Lewis Partnership warned that the worst case scenario for the full year involves sales at John Lewis declining by 35%, with Waitrose seeing a decline of less than 5%.

The British government introduced stricter lockdown measures at the end of last month in order to help contain the spread of the illness. Many fear the economic implications of these measures, as non-essential stores have been closed.

BP share price falls as WTI oil trades in negative territory

The BP share price (LON:BP) fell over 5% on Tuesday morning as the market attempted to navigate a world where oil can trade in negative territory.

The front month May WTI oil contract fell as low as -$40.23 per barrel oil in futures markets overnight, the first time in history oil has traded negatively.

This means oil traders were in effect paying people $40 to take oil away from them.

It must, however, be noted that the market in the May WTI contract was extremely illiquid as most traders had already begun trading the June contract before the May contract expires today.

Notwithstanding the oil contract dynamics, the negative oil prices caused ripples in equity markets with the BP share price falling over 5% in early trade.

Shares in oil major peers Total, Eni and Royal Dutch Shell all suffered as well.

WTI Oil

Many analysts pointed to the trading liquidity shifting to the June WTI contract where prices were still in excess of $20 and appeared to be trading normally. However the sharp decline in oil prices for immediate delivery raised fears the physical market was facing huge problems as US storage neared capacity. “With storage facilities filling up fast, particularly at the WTI pricing point, Cushing, there are fears that there will be nowhere to store it,” ANZ Research report in a research note. Such as situation will be devastating for oil producers and refineries in the short term as the coronavirus lockdown threatens to force the closure of operations. This would likely hit the shares of oil producers heavily, including the BP share price. However, this scenario is not inevitable as President Trump starts to plan for the reopening of the economy which would reignite demand for oil and potential avoid facilities filling up completely. A drop in the number of coronavirus deaths across the globe has led to governments outlining plans for an easing back into normal activity. Although this won’t be a magic bullet for oil and the BP share price, it will certainly ease downside pressure, possibly leading to a sharp rebound in prices.Premier Foods shares soar as sales grow

Premier Foods (LON:PFD) shares soared on Monday as the company saw sales rise in March amid the outbreak of COVID-19.

Shares in the owner of the Mr Kipling brand were up by more than 20% during trading on Monday.

The company said that UK sales are expected to have grown by roughly 7.3% in the fourth quarter and 15.1% in March.

“The trading performance in the fourth quarter continued the positive momentum seen in previous quarters and volumes in March rose sharply to fulfil increased consumer demand during the outbreak of COVID-19,” Premier Foods said in a statement.

As the outbreak of the illness continues to spread, many consumers have stockpiled products to ensure that they have what they need.

Premier Foods said that it has seen “a dramatic short-term peak in volumes across many of its categories during March”.

The company added that volumes have begun to reduce from the “exceptional levels” experienced last month, though they are still expected to be higher than usual.

“This reflects more meals being eaten at home than usual due to recent measures set out by HM Government and hence increased demand for the group’s product ranges,” the company continued.

Indeed, the government introduced stricter social distancing measures last month, encouraging people to stay indoors unless absolutely necessary.

“The group also takes its responsibility as a major UK food manufacturer very seriously and is working closely with its customers to ensure maximum availability of its product ranges for consumers,” Premier Foods continued.

“During this challenging time, the company’s manufacturing and distribution operations are working at maximum capacity and coping well with this recent elevated level of demand, and customer service levels continue to be high.”

Shares in Premier Foods plc (LON:PFD) were up on Monday, trading at +22.32% as of 14:25 BST.

Oil sinks to lowest level since 1982

US West Texas Intermediate WTI Oil has sunk to $11.01 per barrel, the lowest level since 1982.

Oil has been under pressure throughout the COVID-19crisis and today’s selloff marks a new milestone for 2020’s decline.

However, while the headline figure of oil falling to $11.01 suggests a shock to global markets, the underlying market dynamics suggests this isn’t the case.

The WTI oil contract priced at $11.01 is the front month May contract which is due to expire on Tuesday.

This means that as of tomorrow, when the May contract expires, WTI prices will be quoted from the June contract. The June contract is trading at $22, around double the price of the May contract.

The sharp drop in WTI oil prices to record lows today is more a case of futures traders exiting positions in the May contract in a low volume market to avoid taking physical delivery.

Each month trader’s shift to the next month along the contract curve near the expiry of the front month as this is where the market liquidity naturally shifts to as traders exit positions to avoid holding a position when the contract expires.

WTI Oil

So while WTI is printing the lowest level since 1982, this isn’t a true reflection of the oil market which will be quoted at $22 as of tomorrow. Despite today’s price largely being a consequence of market dynamics and the contract expiring, it makes the price no less remarkable and is a sign that oil traders really don’t want to be taking delivery of American oil in the current market. The IEA have recently issued a report that highlighted a severe lack of demand could lead to storage facilities becoming full. This would undoubtedly be disastrous for the price of oil and some analysts have said the price of oil could even turn negative as oil producers have to pay people to take it away.FTSE 100 takes a breather after a week of strong gains

The FTSE 100 and other major European indices took a break from recent gains on Monday as the market digested a slowdown in the number of new coronavirus deaths.

The FTSE 100 was broadly flat in early trade on Monday with London’s leading index trading in a tight range around 5,800 for most of the morning.

The number of people who sadly died with coronavirus fell in the world’s largest economies over the weekend as the United States recorded 1,629 deaths on Sunday, considerably lower than the 2,000+ deaths that were reported last week.

Many European countries have also reported a fall in the number of new cases and deaths. The slowdown in new cases has given countries such as Germany and Spain the confidence to outline plans to start reopening their economies.

However, some analysts are still cautioning over the impact of coronavirus on the global economy and adjusting their investment exposure accordingly.

“We have increased our preference to be overweight government bonds, reflecting our view central banks will continue to act to maintain easy monetary conditions, and at the same time allow fiscal space to be created without higher yields,” said Michael Grady, head of investment strategy and chief economist at Aviva Investors.

“Our modest underweight equity allocation reflects our concern that economic weakness will translate into historically weak corporate earnings in 2020, which we do not think markets are fully discounting at this time.”

Other investors, such as Bridgewater Associates’ Ray Dalio, have said they are avoiding bonds in favour of buying opportunities they see in equities. Ray Dalio has also said ‘cash is trash’ – a view that would suggest now is the time to making investments.

US earnings season started last week with major US banks reporting lower profits and warning on the outlook. However, many of the banks’ shares rose, providing support for the argument the negative impact on the coronavirus on corporate earnings is largely priced in.

UK Government launches £1.25bn start-up support package

The UK government has announced a much needed £1.25bn support package for the UK’s start-ups.

The package is broken down into two elements; a £500m fund designed for small businesses and the provision of £750m in grants and loans from Innovate UK.

To qualify for support, companies must have already raised £250,000 in equity investment through private investment channels within the last 5 years.

Rishi Sunak’s announcement to assist start-up businesses comes after it became apparent the treasury’s initial stimulus package wouldn’t filter down to the UK’s fastest growing and most innovative companies.

The banks are ultimately in control of distributing the government’s £350 billion aid package for businesses. With only 80% of the value of loans being guaranteed by the government, banks still have to accept some risk so haven’t approved loans on the scale needed to support smaller businesses. Many other countries have guaranteed 100% of loans to businesses.

The latest package is aimed at those companies engaged in high levels of R&D and may not yet be producing enough revenue to cover costs.

These innovative companies typically operate in the technology and knowledge intensive sectors and face closure if they are unable to secure capital.

Gerard Grech, Chief Executive, Tech Nation, highlighted the importance of startup sfor the UK as he said “Tech startups and scaleups are crucial to the UK’s future growth, jobs and innovation. The £500M Future Fund and £750M for loans and grants for R&D for startups is a bold intervention, and although the full implementation details are to still be released, it is likely to give the sector a welcome boost in these unprecedented times. How to target the money effectively should be the next priority.”

“Start-ups and scale-ups vary in their financial structuring and their regional location. It will be important to get the balance just right, across the UK and also across the different models of investments, from angel invested companies to VC-funded firms.”

“The UK’s tech sector has achieved a huge amount in the past 10 years. In 2019, a staggering 33% of all European tech investment was in the UK – the third highest in the world. We must keep building on this success story”

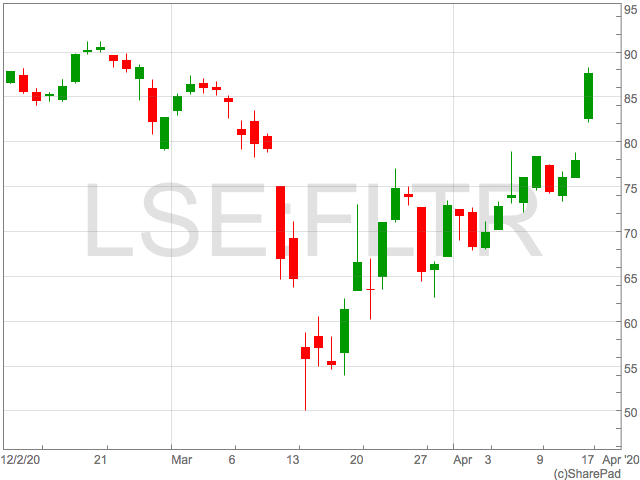

Flutter Entertainment shares complete V-shaped recovery

Shares in the owner of Betfair and Paddy Power, Flutter Entertainment (LON:FLTR), have completed a remarkable V-shaped recovery following the sharp selloff due to coronavirus.

With the heavily touted V-shaped recovery in the global economy looking increasingly unlikely, the FTSE 100 gambling company has at least provided its investors with a strong recovery.

The recovery has completed with a 13% increase on Friday as a reaction to the betting group’s Q1 trading update.

Flutter’s Q1 revenue grew 29% to £547m from £478m in 2019, helped by strong performance in the gaming division.

With sporting events being heavily disrupted due to coronavirus lockdowns, Flutter’s strong performance was a surprise to markets and shares hit a 5-week high on the back of the announcement.

The rally took shares back above 85p and completed a sharp recovery from the selloff that started in early May.

Flutter Entertainment CEO, Peter Jackson, commented on the results.

“The Group performed very well in the period prior to the disruption to sporting events in mid-March. We delivered strong customer growth across each of our brands and benefitted from favourable sports results across our sportsbooks. Following the widespread cancellation of sporting events, Group revenues have been more resilient than we initially expected, helped by the continuation of horse racing in Australia and the US. Gaming continues to perform well across the Group.”

“During this unprecedented time, we are keenly aware of our heightened responsibility to ensure that we do all we can to promote responsible gambling. We have stepped up our own practices and are collaborating with our peers within the Betting and Gaming Council to continue to raise standards across the sector. We are also working hard to provide all the support we can to our employees and I would like to thank them for their ongoing commitment and support for each other during this difficult period.”

“While the current disruption is truly exceptional, it underlines the importance of product and geographic diversification. As such, the strategic logic of our combination with The Stars Group remains compelling. Following approval of the deal yesterday by the Irish Competition and Consumer Protection Commission, we look forward to completing the transaction in Q2 upon receipt of outstanding shareholder and regulatory approvals.”

The recovery has completed with a 13% increase on Friday as a reaction to the betting group’s Q1 trading update.

Flutter’s Q1 revenue grew 29% to £547m from £478m in 2019, helped by strong performance in the gaming division.

With sporting events being heavily disrupted due to coronavirus lockdowns, Flutter’s strong performance was a surprise to markets and shares hit a 5-week high on the back of the announcement.

The rally took shares back above 85p and completed a sharp recovery from the selloff that started in early May.

Flutter Entertainment CEO, Peter Jackson, commented on the results.

“The Group performed very well in the period prior to the disruption to sporting events in mid-March. We delivered strong customer growth across each of our brands and benefitted from favourable sports results across our sportsbooks. Following the widespread cancellation of sporting events, Group revenues have been more resilient than we initially expected, helped by the continuation of horse racing in Australia and the US. Gaming continues to perform well across the Group.”

“During this unprecedented time, we are keenly aware of our heightened responsibility to ensure that we do all we can to promote responsible gambling. We have stepped up our own practices and are collaborating with our peers within the Betting and Gaming Council to continue to raise standards across the sector. We are also working hard to provide all the support we can to our employees and I would like to thank them for their ongoing commitment and support for each other during this difficult period.”

“While the current disruption is truly exceptional, it underlines the importance of product and geographic diversification. As such, the strategic logic of our combination with The Stars Group remains compelling. Following approval of the deal yesterday by the Irish Competition and Consumer Protection Commission, we look forward to completing the transaction in Q2 upon receipt of outstanding shareholder and regulatory approvals.”

The recovery has completed with a 13% increase on Friday as a reaction to the betting group’s Q1 trading update.

Flutter’s Q1 revenue grew 29% to £547m from £478m in 2019, helped by strong performance in the gaming division.

With sporting events being heavily disrupted due to coronavirus lockdowns, Flutter’s strong performance was a surprise to markets and shares hit a 5-week high on the back of the announcement.

The rally took shares back above 85p and completed a sharp recovery from the selloff that started in early May.

Flutter Entertainment CEO, Peter Jackson, commented on the results.

“The Group performed very well in the period prior to the disruption to sporting events in mid-March. We delivered strong customer growth across each of our brands and benefitted from favourable sports results across our sportsbooks. Following the widespread cancellation of sporting events, Group revenues have been more resilient than we initially expected, helped by the continuation of horse racing in Australia and the US. Gaming continues to perform well across the Group.”

“During this unprecedented time, we are keenly aware of our heightened responsibility to ensure that we do all we can to promote responsible gambling. We have stepped up our own practices and are collaborating with our peers within the Betting and Gaming Council to continue to raise standards across the sector. We are also working hard to provide all the support we can to our employees and I would like to thank them for their ongoing commitment and support for each other during this difficult period.”

“While the current disruption is truly exceptional, it underlines the importance of product and geographic diversification. As such, the strategic logic of our combination with The Stars Group remains compelling. Following approval of the deal yesterday by the Irish Competition and Consumer Protection Commission, we look forward to completing the transaction in Q2 upon receipt of outstanding shareholder and regulatory approvals.”

The recovery has completed with a 13% increase on Friday as a reaction to the betting group’s Q1 trading update.

Flutter’s Q1 revenue grew 29% to £547m from £478m in 2019, helped by strong performance in the gaming division.

With sporting events being heavily disrupted due to coronavirus lockdowns, Flutter’s strong performance was a surprise to markets and shares hit a 5-week high on the back of the announcement.

The rally took shares back above 85p and completed a sharp recovery from the selloff that started in early May.

Flutter Entertainment CEO, Peter Jackson, commented on the results.

“The Group performed very well in the period prior to the disruption to sporting events in mid-March. We delivered strong customer growth across each of our brands and benefitted from favourable sports results across our sportsbooks. Following the widespread cancellation of sporting events, Group revenues have been more resilient than we initially expected, helped by the continuation of horse racing in Australia and the US. Gaming continues to perform well across the Group.”

“During this unprecedented time, we are keenly aware of our heightened responsibility to ensure that we do all we can to promote responsible gambling. We have stepped up our own practices and are collaborating with our peers within the Betting and Gaming Council to continue to raise standards across the sector. We are also working hard to provide all the support we can to our employees and I would like to thank them for their ongoing commitment and support for each other during this difficult period.”

“While the current disruption is truly exceptional, it underlines the importance of product and geographic diversification. As such, the strategic logic of our combination with The Stars Group remains compelling. Following approval of the deal yesterday by the Irish Competition and Consumer Protection Commission, we look forward to completing the transaction in Q2 upon receipt of outstanding shareholder and regulatory approvals.”