| Instant access Cash ISA rate | 1 year ISA rate | 2 year Isa rate | |

| Barclays | 0.40% | 1.00% | N/A |

| Lloyds Bank | 0.05% | N/A | 0.65% |

| Santander | 0.20% | N/A | 0.75% |

| HSBC | 0.50%* | N/A | N/A |

| Halifax | 0.05%** | N/A | 0.55% |

| TSB Bank | 0.24% | N/A | 1.05% |

| Natwest | 0.20% | 0.30% | 0.35% |

| Nationwide | 0.30% | 0.50% | 0.60% |

| RBS | 0.35% | 0.30% | 0.35% |

| Yorkshire Bank & Virgin Money | 0.50% | 1.36% | N/A |

| AVERAGE | 0.24% | 0.69% | 0.61% |

Average Cash ISA savers will earn just £12 in interest with UK’s 10 biggest banks

Cash ISAs continue to provide savers with disappointing savings rates as interest rates remain at record lows.

With an average amount of £5,114 saved in Cash ISAs it means the average interest from the UK’s top banks would provide interest of just £12.77, research from RateSetter found.

Data compiled by Rate Setter

*0.05% from 1 May 2020. 0.5% used in calculations.

**0.1% from 1 July 2020. 0.24% used in calculations.

Rhydian Lewis, CEO at RateSetter, said:

“Cash ISAs provide certainty on the returns they deliver – but with interest rates closing in on zero, this essentially guarantees your money will fall in value once inflation is factored in.

“However, people should not give up on the prospect of growing their money in the coming year. There are still inflation-beating ISA investment options out there which offer shelter from the turbulence of the stock market, such as the Innovative Finance ISA.”

The Innovative Finance ISA provides exposure to a range of underlying assets such as property or small business loans and typically provides much higher returns than Cash ISAs. The higher yields do of course come with a higher level of risk and aren’t suitable for all savers.

Stocks & Shares ISAs may also prove a popular alternative to Cash ISAs in 2020 as shares trades at some of the lowest levels for years, providing savers and investors with a number of bargains.

Lloyds share price sinks after it cuts dividend on advice from Bank of England

The Lloyds share price (LON:LLOY) sank on Wednesday after the UK banks announced it would be cutting its dividends with immediate effect.

Lloyds will not pay any dividends from 2019 and will cancel future payments in 2020 to conserve cash during the coronavirus crisis.

Lloyds share price

The news sent the Lloyds share price down as much as 6% in an immediate market reaction. Such news will be a body blow to Lloyd’s investors who have enjoyed a progressive dividend policy that has made Lloyds one of the most popular shares for income among retail investors. The Lloyds dividend cut came after UK banks received letters from the Bank of England’s Prudential Regulation Authority outlining advice to cut dividends as well as stopping cash bonuses for senior staff. Lloyds released the news to investors with a statement on their dividend: “In order to help us to serve the needs of businesses and households through the extraordinary challenges presented by Covid-19, the board has decided that until the end of 2020 we will undertake no quarterly or interim dividend payments, accrual of dividends, or share buybacks on ordinary shares. “In addition, in response to a request from the PRA and to preserve additional capital for use in serving our clients, the board has agreed to cancel payment of the final 2019 dividend in relation to ordinary shares. Accordingly, resolution 17 in relation to the declaration of that dividend will be withdrawn from the AGM, scheduled to take place on 21 May 2020. Our board will decide on any dividend policy and amounts at year-end 2020.” While the cut in dividends will be a blow to investors in the short-term, once the coronavirus induced economic slowdown subsides it is likely the bank will resume paying dividends. Lloyds and other UK banks are in a strong financial positions following the adoption of stringent capital ratio so whilst the economic slowdown may hinder profitability it won’t have the devastating impact the financial crisis did.UK Banks cut dividends after advice from the Bank of England’s PRA

UK Banks including Lloyds, RBS, Barclays, HSBC and Standard Chartered have cut their cut dividends after advice from the Prudential Regulation Authority (PRA).

The PRA advised banks to scrap all outstanding dividends from 2019 and suspend all further pay outs in 2020 to maintain high levels of cash through the coronavirus health crisis.

In a letter to Barclays CEO Jes Staley the Bank of England’s PRA said the “The PRA welcomes the consideration given by you and your firm to suspending dividends and buybacks on ordinary shares until the end of 2020.”

The letter also detailed instructions on how Barclays should release the news to the market which saw UK banks make an almost coordinated series of releases.

Barclays were due to pay investors £1 billion in dividends on Friday, which will now be cancelled.

In addition to cutting dividends, banks were advised not pay cash dividends to senior staff. Lloyds said in a statement: “In order to help us to serve the needs of businesses and households through the extraordinary challenges presented by Covid-19, the board has decided that until the end of 2020 we will undertake no quarterly or interim dividend payments, accrual of dividends, or share buybacks on ordinary shares. “In addition, in response to a request from the PRA and to preserve additional capital for use in serving our clients, the board has agreed to cancel payment of the final 2019 dividend in relation to ordinary shares. Accordingly, resolution 17 in relation to the declaration of that dividend will be withdrawn from the AGM, scheduled to take place on 21 May 2020. Our board will decide on any dividend policy and amounts at year-end 2020.” Shares in the UK banks were all down over 6% in early trade on Wednesday with HSBC the most heavily hit, down over 8%. HSBC managed to avoid many of the worst effects of the financial crisis and today’s cut in dividend will be a big shock to investors. Banks are set to report updates to the market at the end of April.This letter from regulator to Barclays boss, saying cancel all dividends and bonuses, would have been utterly unthinkable before 2008 banking crisis. Banks now treated precisely as they should always have been, namely as agents of state policy when the going gets tough https://t.co/5OeUDeQwTZ

— Robert Peston (@Peston) March 31, 2020

Synairgen shares surge on commencement of Coronavirus treatment trial

Shares in Synairgen (LON:SNG) jumped on Tuesday after the UK-based biotech company announced it had commenced trails for a COVID-19 treatment.

The AIM listed company had begun trials for SNG001 which is an inhaled formulation of interferon-beta-1a, a protein impacted by COVID-19.

Interferon beta is a naturally occurring protein which drives the body’s natural antiviral responses.

The trial will initially involve 100 patients in a double blind test using a placebo.

Following the announcement, shares in Synairgen rose by 11% to 69p, valuing the company at £83 million.

Synairgen treatment

Evidence has shown a deficiency in Interferon beta production by the lung could be responsible for the severe lung problems COVID-19 patients are suffering. Synairgen highlighted in a release that this was what made COVID-19 so dangerous for older people, those with diabetes and existing lung or heart problems. The Synairgen treatment will help promote the bodie’s own immune system by promoting natural production of this protein. Synairgen’s trial will commence in on trail site initially run by the University Hospital Southampton NHS Foundation Trust. There will be a further six sites commencing trial doses shortly. Richard Marsden, CEO of Synairgen, commented: “We are delighted to get this trial underway with the dosing of the first patient. The team has worked tirelessly and intensively with the relevant authorities and collaborators to get to this stage, and we now look forward to recruiting more patients and completing the trial as soon as possible. A successful outcome from this trial in COVID-19 patients would be a very important step towards a major breakthrough in the fight against this coronavirus pandemic.” Synairgen have recently raised £14 million through a heavily oversubscribed placing of 40,000,000 shares to fund further expansion of their trials and research. Synairgen is one of a number of UK-listed companies and hundreds globally that offer promise in the fight against COVID-19. Novacyt has spear headed the UK effort to improve testing and has begun trails with Public Health England. However, Synairgen offers a different proposition in a treatment for COVID-19, which if successful would be monumental for patient recovery rates. Needless to say this would be a multi-billion pound development for Synairgen and could see shares at many multiples of current levels.WPP shares rise after COVID-19 reassurance

Shares in WPP (LON:WPP) rose on Tuesday after the advertising company released an update on operations during the coronavirus outbreak.

In an update that was generally taken well by the market the company highlighted a strong start of to 2020 and their ability to continue operations through remote working.

Shares in WPP were up over 7% on Tuesday morning.

Although the advertising agency said it had experienced cancellations and sales declines in some areas, it had seen growing demand for strategic communications while government and NGO bookings remained robust.

In an effort to conserve cash, WPP adopted measures similar to many companies in ceasing their share buyback programme and have scrapped the 37.3p Q4 2019 dividend.

This is expected to save £1.1 billion in cash. The company also announced cost cutting measures to the tune of £700-800 million.

Mark Read, Chief Executive Officer, WPP commented:

“The actions we have taken in the last 18 months to streamline and simplify WPP, together with raising £3.2 billion in asset disposals, have put WPP in a strong financial position. It is clear that the companies in the strongest financial position will be best placed to protect their people, serve their clients and benefit their shareholders during a period of great uncertainty, which is why we are taking the steps we are outlining today.”

“Across WPP we now have close to 95% of our people working effectively and productively away from their offices. I am very proud of the response from our people, who are looking out for each other and going the extra mile for clients while demonstrating the creativity, collaboration and resilience that will be key to the enduring success of WPP. At the same time, we are supporting many governments and international health organisations on communications programmes to limit the impact of COVID-19 on our communities. The important role we are playing in helping our clients navigate a difficult time gives us great confidence in the long-term future of the company.”

WPP are set to release their first quarter trading 29th April 2020.Royal Dutch Shell updates 2020 outlook

Oil giant Royal Dutch Shell (LON:RDSB) have updated their 2020 outlook following the spread of the coronavirus.

In a brief update that covered Shell’s business units including integrated gas, upstream and oil products, the main take away was a possible $400-800 million in impairment charges.

“As a result of COVID-19, we have seen and expect significant uncertainty with macro-economic conditions with regards to prices and demand for oil, gas and related products.”

“The impact of the dynamically evolving business environment on first quarter results is being primarily reflected in March with a relatively minor impact in the first two months,” Shell said in a statement.

The adverse update was a result of a drop in oil prices causing Shell to make amendments to their average oil price forecasts for early 2020. A price war between Russia and Saudi Arabia threatens to increase oil supply just at the time demand is set to be severely reduced by coronavirus, driving prices lower.

The oil products businesses was also expected to see weaker margins in the refining business. In terms of production, Shell said they expected output to be between 2,650 and 2,720 thousand barrels of oil equivalent per day

The update comes shortly after Shell announced they would be cutting costs and stopping their share buyback programme in an effort to conserve cash.

In a prior statement, Ben van Beurden, Chief Executive Officer of Royal Dutch Shell said he was confident Shell could successfully navigate the slump in prices and demand.

“As well as protecting our staff and customers in this difficult time, we are also taking immediate steps to ensure the financial strength and resilience of our business,” he said.

“The combination of steeply falling oil demand and rapidly increasing supply may be unique, but Shell has weathered market volatility many times in the past.”

Shares in Royal Dutch Shell (LON:RDSB) rose 6% in early trade on Tuesday following the annoucement.

The Next share price may never recover

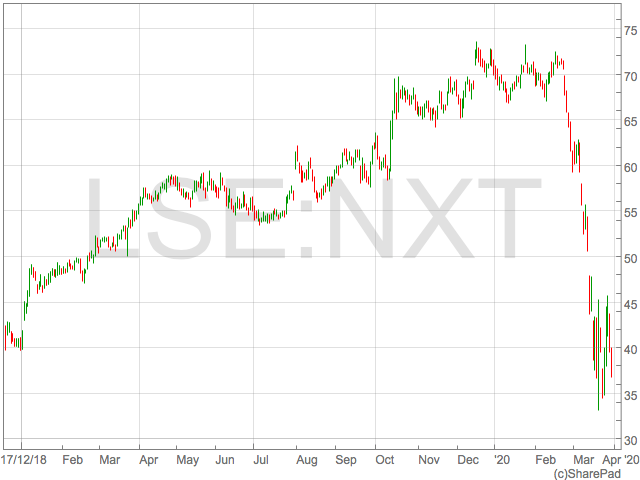

The Next share price (LON:NXT) fell heavily during the volatility caused by the spread of coronavirus and joined the raft of companies falling over 50% from their recent highs.

With such a sharp fall, shares in Next now have to nearly double to once again reach recent highs, but a culmination of changes to consumer behaviour and damage to Next as a brand could inhibit share price appreciation from current levels.

Unethical behaviour

The reputational damage to companies perceived to have behaved unethically or immorally during the coronavirus spread may well be punished by customers and investors after the crisis. This could very well be the case for Next. Next came under well-publicised pressure from workers to cease operations at their warehouses after Next management refused to close, instead offering workers an additional 20% to remain at work. This was met with an angry backlash from workers and politicians which led to Next ceasing it’s entire online operations. In a brief and abrupt released to the market, Next said: “NEXT has listened very carefully to its colleagues working in Warehousing and Distribution Operations to fulfil Online orders. It is clear that many increasingly feel they should be at home in the current climate.” “NEXT has therefore taken the difficult decision to temporarily close its Online, Warehousing and Distribution Operations from this evening, Thursday 26 March 2020. NEXT will not be taking any more Online orders after this time until further notice.” With stores already closed, Next is now unable to make any sales to customers and will have to refund any recent purchases that have not been delivered.

Next Mismanagement

Many companies will be forgiven for poor results during the spread of coronavirus. It has impacted every single company on the planet in ways that were impossible foresee. However, Next is now in a position where it can not make any sales, which isn’t the case for most of it’s competitors, especially in the online space. ASOS has gone full throttle with push notifications promoting sales, Top Shop have introduced a 30% sales for loungewear and created ‘Conference Call’ styles, and Boohoo’s PrettyLittleThing is running a 50%-70% sale. Whilst margins will be compressed by discounts, Next’s competitors will maintain some levels of revenue as visitors to Next’s website are meet with ‘Sorry We Are Closed’ message. Next’s competitors are not immune from criticism for continuing operations but have managed to keep their businesses running for the time being. Ocado, for example, ordered 100,000 testing kits for its employees. The ability for other online business to keep going further highlights mismanagement by Next and the market will likely continue to punish them for this.Next shares

With recent highs of 7,340p, Next shares would have to rally 86% to regain the losses. This may be asking too much, even in normal circumstances, given that Next only managed to improve profit before tax by 0.8% in the year to January 2020. Although the FTSE 100 listed company has seen a big increase in its online business in recent years, it was slow to adopt a strong online offering and has largely been left behind. Next now has a dented reputation and will have to attract a consumer even more accustomed to online shopping after periods of self isolation imposed on them by coronavirus. Crucially, these were periods when Next were shut for business.YouGov: over 50% expect recession

New data revealed on Monday that more than half of people expect the British economy to be in recession within a year.

The data from YouGov reflects the economic fears caused by the outbreak of COVID-19.

Many countries have either been placed on total lockdown or closed all non-essential shops, restaurants and bars in order to contain the spread of the illness.

In order to assist those in the UK suffering economically, the British government has revealed plans to help businesses as the virus outbreak continues to evolve.

“Now almost three quarters expect that Britain’s economy will be in depression (19%) or recession (52%) within a year,” YouGov said in a report.

Meanwhile, only 1% believe that the economy will be booming within one year.

There is still much uncertainty over how long the national lockdowns and closures will last for.

“With unprecedented Government measures to crackdown on the spread of COVID-19 shutting small and large businesses across the country and confining Britons to their homes, it’s unsurprising that consumer confidence has been knocked,” Oliver Rowe, Director of Reputation Research at YouGov, commented on the data.

“But with little prospect of a solution in the next couple of months Britons are starting to believe that the economy will slide into recession or depression,” Oliver Rowe continued.

Kay Neufeld, Head of Macroeconomics at the Centre for Economics and Business Research, also commented: “The spread of coronavirus has dominated the headlines in recent weeks as Governments across the globe have taken drastic measures to protect their citizens. The data released in the coming days and weeks will show the significant economic costs associated with these measures.”

“Government mandated closures of non-essential shops, pubs, restaurants and other establishments will have a devastating effect on several industries and in particular on the leisure and hospitality sectors,” Kay Neufeld added.

Barclays to become “net zero bank” by 2050

Barclays (LON:BARC) announced on Monday that it will aim to be a “net zero bank” by 2050.

Shares in the bank were down by over 4% during trading on Monday.

The bank has also committed to align all of its financing activities with the goals and timelines of the Paris Agreement.

“The alignment of Barclays’ portfolio will start with the energy and power sectors, and will cover all sectors over time,” the bank said in a statement.

“Barclays will provide the transparent targets required to judge its progress and will report on them regularly, starting from 2021,” it continued.

Many have been joining the fight against climate change as the climate crisis continues to grow.

Last year, the UK government became the first G7 nation to write into law a target for net zero emissions.

The bank joins a list of companies making similar pledges. Earlier this year, BP (LON:BP) announced its plans to become net carbon zero by 2050.

Meanwhile, International Airlines Group (LON:IAG) has also said it will commit to achieving net zero carbon emissions by 2050.

On Monday, Barclays said that its shareholders will be asked to endorse this commitment through the passing of a resolution that the bank will propose to shareholders at its AGM.

“In developing its approach, Barclays has engaged extensively with its shareholders, as well as with stakeholders from across society more broadly,” the bank said.

Shares in Barclays plc (LON:BARC) were down on Monday, trading at -4.21% as of 12:30 BST.

COVID-19: EasyJet grounds entire fleet

EasyJet shares (LON: EZJ) fell on Monday after the low-cost airline announced that it has grounded its entire fleet of aircraft.

Shares in the airline were down by over 7% during trading on Monday.

“As a result of the unprecedented travel restrictions imposed by governments in response to the coronavirus pandemic and the implementation of national lockdowns across many European countries, easyJet has, today, fully grounded its entire fleet of aircraft,” the airline said in a statement.

The aviation industry has been hit particularly hard by the outbreak of COVID-19 as many nations have been placed under lockdown in an attempt to contain the spread of the illness.

Earlier this month, Europe’s worst-affected nation, Italy, was placed under lockdown.

This caused EasyJet rival Ryanair (LON:RYA) to announce that it will be lowering its passenger target for 2020.

On Monday, EasyJet said in a statement: “Over recent days easyJet has been helping to repatriate customers, having operated more than 650 rescue flights to date, returning home more than 45,000 customers. The last of these rescue flights were operated on Sunday 29 March. We will continue to work with government bodies to operate additional rescue flights as requested.”

The airline continued to add that it is uncertain when it will restart commercial flights.

EasyJet will continue to evaluate the situation based on regulations and demand. It will update the market when it has a clearer picture of the future.

“I am extremely proud of the way in which people across easyJet have given their absolute best at such a challenging time, including so many crew who have volunteered to operate rescue flights to bring our customers home,” Johan Lundgren, easyJet CEO, said.

“We are working tirelessly to ensure that easyJet continues to be well positioned to overcome the challenges of coronavirus,” the CEO continued.

Shares in EasyJet plc (LON:EZJ) were down on Monday, trading at -7.63% as of 11:55 BST.