The UK Investor Magazine was delighted to welcome Fawzi Hanano, Chief Development Officer at Cornish Metals, to discuss recent progress at their South Crofty tin mine.

London AIM and Toronto Venture listed Cornish Metals is on a mission to bring mining back to the South Crofty underground tin mine located in Cornwall. The mine closed in 1998 after a 400 year production record.

A Bitcoin payment processor is a service that assists merchants who are accepting Bitcoin and other cryptocurrencies, by converting that revenue stream into a clear, predictable cash flow. Rather than manage wallets and blockchain confirmations directly, the business links its website or app to a processor that generates payment details, following transactions on the network, updating order statues. In most cases, the processor also automatically converts incoming crypto into fiat or stablecoins, so a merchant can see its sales in a familiar currency without having to worry about volatility.

For the customer, paying with a Bitcoin payment processor is broadly the same as making a payment by any other online means: they select crypto at checkout, are shown how much crypto to pay and then simply transfer funds from their wallet using a QR code or address. The processor watches the blockchain and when the transaction gets enough confirmations, it replies a simple “paid” or “failed” status to merchant’s system. If something goes awry – perhaps the customer sends too little or too much – the processor can flag the problem and assist in remedying the payment without requiring support to wade through raw transaction data.

The primary service that Bitcoin payment processors provide to merchants is that of a specialized acquiring service for digital assets. It shortens the intermediaries that stand between buyer and seller, thus helping to reduce transaction costs as well as minimize the risk of declines from banks or card networks. Faster settlement, less payment blocking and ability to reach buyers in countries with relatively undeveloped banking systems all add up to a big trigger for successful checkouts. In addition, processors often provide added tools – dashboards, API integration, webhooks and reporting – that give finance and support teams (as well as developers) the ability to track crypto payments with the same kind of clarity and control they have over more traditional methods.

This publication is intended to be of general interest only and does not constitute legal, regulatory, tax, accounting, investment or other advice nor is it an offer to buy or sell shares in the Company (or any other investments mentioned herein).

Nothing in this publication should be construed as a personal recommendation to invest in the Company (or any other investment mentioned herein) and no assessment has been made as to the suitability of such investments for any investor. In making a decision to invest prospective investors may not rely on the information in this document. Such information is subject to change and does not constitute all the information necessary to adequately evaluate the consequences of investing in the Company.

Theshares in the Company are listed on the London Stock Exchange and their price is affected by supply and demand and is therefore not necessarily the same as the value of the underlying assets. Changes in currency rates of exchange may have an adverse effect on the value of the Company’s shares (and any income derived from them). Any change in the tax status of the Company could affect the value of the Company’s shares or its ability to provide returns to its investors. Levels and bases of taxation are subject to change and will depend on your personal circumstances.

Past performance is not a reliable indicator of future returns. Any return estimates or indications of past performance cited in this document are for information purposes only and can in no way be construed as a guarantee of future performance. No representation or warranty is given as to the performance of the Company’s shares and there is no guarantee that the Company will achieve its investment objective.

Over the fourth financial quarter, the Net Asset Value (NAV) rose by +7.1%, bringing the return for the year to +8.3%.1 Investment performance is therefore ahead of the run rate implicit in the CPI+4% objective over both the quarter and for Majedie’s financial year as a whole. Returns were driven by bottom-up positions in areas as diverse as Chinese and European equities, specialist credit, and supply-constrained commodities. We believe this combination of nonconsensual fundamental ideas, sourced through our proprietary ideas network, makes Majedie a high-quality, repeatable, and complementary proposition for its shareholders.

Majedie’s portfolio holdings are marked-to-market regularly; its distinctive ‘liquid endowment’ approach does not include any allocations to private equity, venture capital or other hard-to value illiquid assets.

With major stock-market indices now fully valued, we believe the most attractive opportunities lie in overlooked international markets, select credit situations, and targeted real assets where structural imbalances exist between supply and demand.

Market Commentary

In many respects, the quarter had an old-fashioned feel, with corporate earnings and central banks setting the tone. Most asset classes posted gains: global equities, as measured by the MSCI ACWI, rose +7.3%.

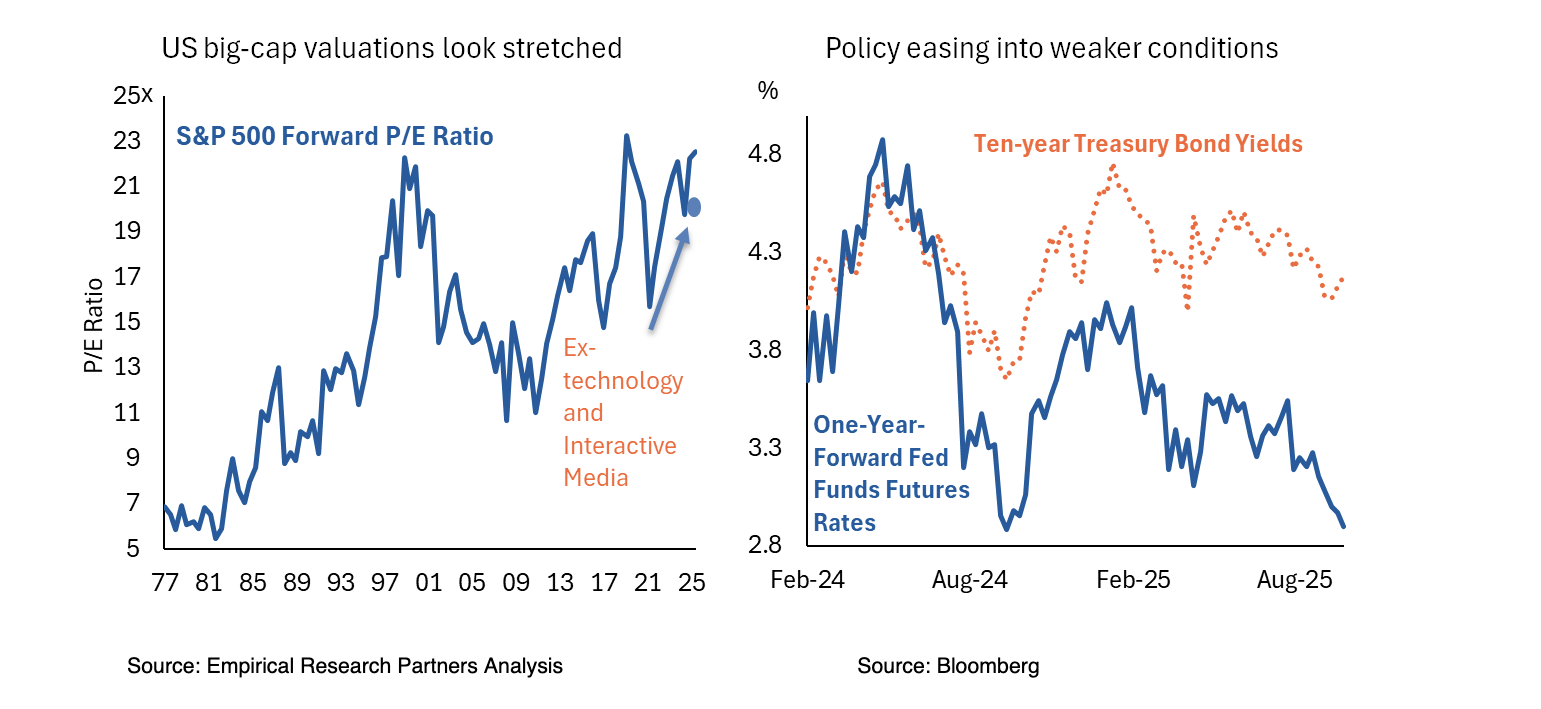

Emerging markets led the way, as China extended its recovery amid signs that stimulus was gaining traction and policymakers reaffirmed the stock market’s importance as a policy tool. Among developed markets, Japan stood out, advancing on the back of robust GDP growth, a weaker yen and a renewed trade accord that saw US tariffs fall from 25% to 15%. In the United States, most of the progress came from multiple expansion rather than earnings growth. With the S&P 500 now trading at 22x forward earnings, valuations once again appear stretched. Growth stocks (+8.6%) outpaced value (+6.0%), and for once small caps fared well as investors began to anticipate rate cuts.

Softer US labour and inflation data duly paved the way for a 25bps rate cut in September – the Fed’s first since 2024. Chair Jerome Powell hinted at further easing, albeit data dependent. In the UK, inflation overshot while growth undershot, sending gilt yields to 27-year highs. France’s budget tensions unsettled bond markets despite the ECB lowering its 2025 inflation forecast to 2.1%.

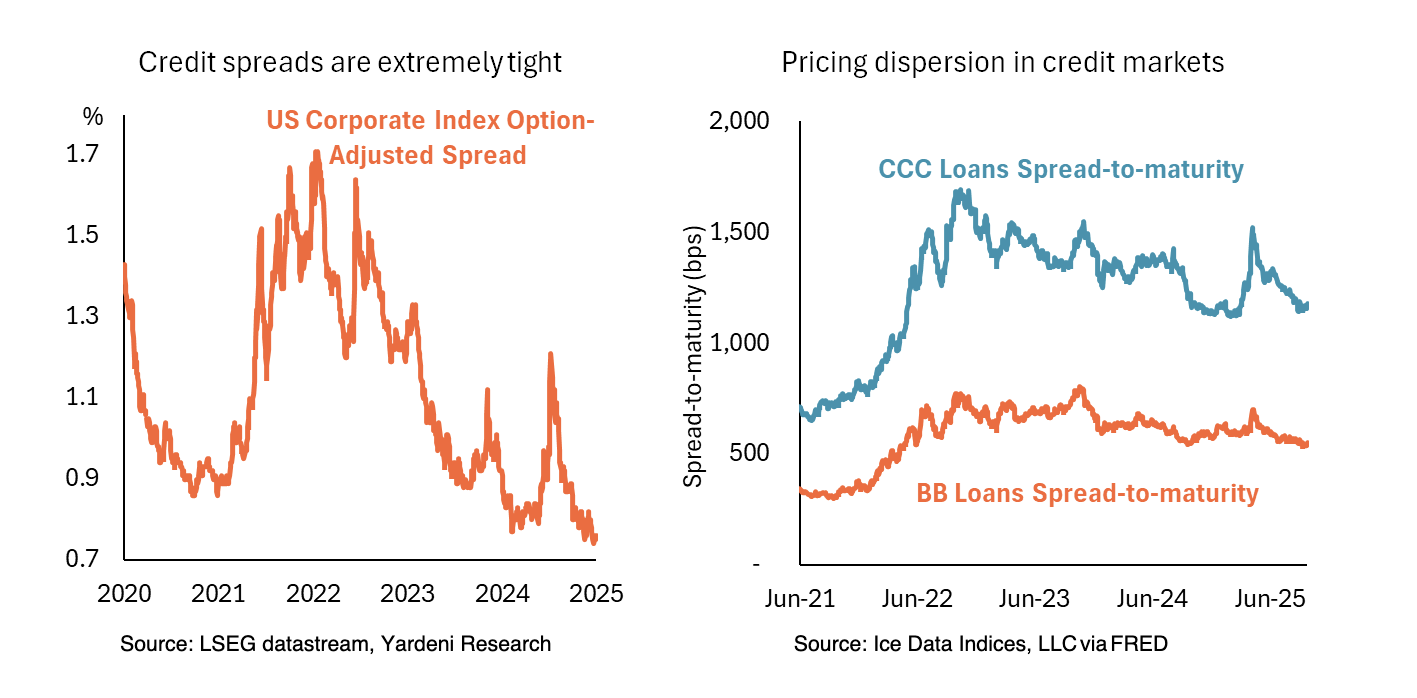

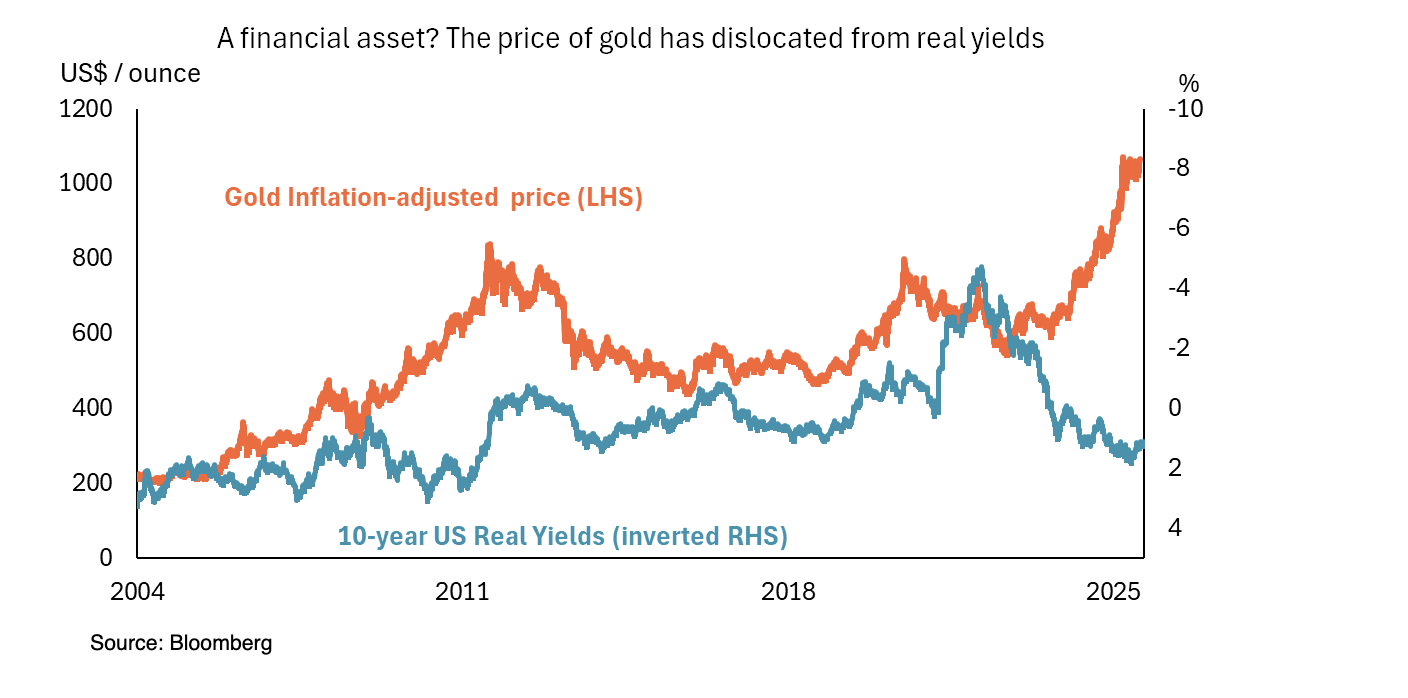

Credit spreads in developed markets have tightened to multi-year lows, while EM debt and Treasuries gained from the easing trend. Commodities diverged: oil and gas weakened, but gold continued its steady ascent. A softer dollar rounded off the quarter, lending further support to emerging-market currencies.

The Portfolio and Outlook

The portfolio is structured with the aim of achieving long-term growth, but returns will depend on market conditions, even as we take a circumspect view of broader markets. The largest constituents of major indices appear expensive and, in our judgement, offer little margin of safety. A generation of investors has grown accustomed to capital gains from the S&P 500 and private equity, sees the US dollar as a one-way trade, and government bonds, or “par” credit, as dependable sources of income and protection. Many portfolios are thus heavily concentrated in these familiar areas. By contrast, the assets we find most attractive remain largely absent from mainstream allocations. Years of under-investment have created scarcity and, with it, opportunity.

Our most rewarding investments have often come from areas where expectations are depressed and fundamentals improving. In such situations, even modest progress can have an outsized impact, because rising earnings often attract higher valuation multiples. Conversely, when starting valuations are stretched, small disappointments can trigger disproportionate losses. Our experience suggests that, especially at valuation extremes, it is the rate of change in earnings expectations that matters more than their absolute cadence. Today, most opportunities lie in a middle ground: neither so cheap as to ensure success, nor egregiously expensive. That is when discipline counts. Rather than rely on subjective judgements about valuation, we (and our external managers) seek situations where the market is mispricing reality, ideally with an identifiable catalyst to correct the anomaly.

We have avoided chasing ‘story’ stocks and other speculative assets that bounced back after this year’s tariff-induced volatility, many of which we feel are vulnerable to negative rate-of change. Our investment approach seeks to minimize the risk of permanent capital loss while aiming for returns independent of benchmarks. We prefer bottom-up opportunities in international markets, midcaps and eclectic value situations where fundamentals are improving from a low base.

Asia: reform and renewal

Low expectations and improving fundamentals are most evident in Asia. Barely a year ago, many allocators had written off China as ‘un-investable’, convinced they understood the country’s structural challenges better than its own policymakers. Today, the same fickle allocators are increasingly fearful of missing out. China’s authorities have acted to revive domestic demand, curb uneconomic competition (‘involution’) and channel investment toward strategic technologies. The country’s massive build-out of AI infrastructure is viewed less as a business venture than investment in a national utility, designed to raise productivity and social resilience. We aim to capture this ‘slow bull market’, which appears to be built on sturdier foundations than the liquidity-fuelled rally of 2015.

Japan remains one of the most compelling reform stories globally. Corporate governance continues to improve, with management teams increasingly responsive to shareholder pressure for efficiency and returns.

Absolute Return Credit Markets

Spreads on conventional investment-grade and high-yield debt sit near two-decade lows, meaning investors have seldom been paid less for taking-on the risk of default. Private credit (to which Majedie’s portfolio has no exposure) may promise higher yields but, in our view, in many cases it does not represent true value.

Our approach to credit is very different. We focus on asymmetric situations where downside should be limited to the recovery of principal, and where upside potential is considerable. Through our longstanding relationships with leading stressed and distressed investors, we seek to capitalise on divergence between the price of credit instruments of differing quality buckets. In US leveraged loans, for example, BB-rated bonds yield only 2.6% more than ‘risk free’ Treasuries of similar duration, whereas spreads on CCC paper are some 12.6%. This differential, twice the level of 2021, creates a very attractive setup for long-short credit managers because it allows them to mitigate market risk inexpensively, while pursuing situation-specific opportunities with higher return potential.

Real Assets: scarcity over sentiment

As long-term investors, we like tangible, cash-generating assets, the price of which depends on fundamental supply and demand considerations. This mindset steers us toward copper and uranium, two commodities that are scarce and strategically vital. They both sit at the nexus of global electrification, AI-related energy demand and essential investment in defence infrastructure.

As for gold, we understand its conceptual appeal and recognise that central banks are building reserves as confidence in the Dollar erodes. However, we have always struggled to make a fundamental case for owning an asset that has neither utility, nor cash flow. Interestingly, the historical link between gold and real interest rates appears to have broken down, perhaps reflecting that speculation may be partly behind the price action this year.

Summary

Majedie’s portfolio is built around high-conviction, non-consensual opportunities. In many cases, these can be described as ‘rate-of-change’ situations, where fundamentals are quietly improving but expectations remain low. Just as importantly, we have sought to avoid areas where expectations are so high that even a modest disappointment could be severely punished by the markets.

Whilst undoubtedly challenging, we believe environments like these often produce the most attractive asymmetry between risk and reward. With major indices now appearing fully valued, the most compelling opportunities lie in overlooked international markets, specialist credit, and real assets where structural imbalances persist. Majedie’s differentiated, bottom-up approach is designed to capture these mispriced situations with discipline and conviction.

ITM Power has landed a significant contract to supply electrolyser technology for two major energy infrastructure projects in Germany.

The deal with Stablegrid Group covers a combined capacity of 710 MW over two projects designed specifically to stabilise the grid.

The projects represent an innovative approach to managing Germany’s increasingly complex electricity grid, with both facilities operating exclusively for grid balancing and smoothing out the mismatches between renewable energy supply and demand.

This “predispatch” system, dubbed “Netzbrücke” or “grid bridge,” aims to dramatically reduce costly grid interventions.

Currently, German taxpayers face annual bills of 2-3 billion Euros due to redispatch operations, according to ITM Power’s update on Friday.

The first project, “Netzbrücke 410,” will see ITM Power deliver a 30 MW green hydrogen production facility in Rüstringen.

The second larger project involves installing 680 MW of indoor electrolyser capacity, with pre-FEED work beginning in January 2026 and a final investment decision expected in 2028.

“Partnering with Stablegrid on these landmark grid balancing projects in Germany reinforces ITM’s position at the forefront of the energy transition in Europe’s largest economy,” said Dennis Schulz, CEO of ITM Power.

GenIP has received 57 new report orders from returning clients. The orders come from two major US research universities and a UK institution.

The AI-powered innovation intelligence company secured 50 Invention Evaluator report orders from two US universities with strong commercialisation track records.

One institution ranks consistently in the National Academy of Inventors’ “Top 100 US Universities Granted Utility Patents”. The other operates one of America’s most active university innovation hubs, tracking thousands of invention disclosures, patent filings and spinoff ventures annually.

A UK university that first engaged GenIP in June 2025 has placed a further seven report orders.

The repeat business validates GenIP’s AI-enabled analytical products in supporting technology transfer decisions, the company said.

Melissa Cruz, GenIP’s CEO, noted the company is seeing increased inbound referrals from universities reporting improvements in licensing workflows after adopting GenIP’s evaluations.

“The continued return of leading institutions reinforces the market’s need for faster, more reliable decision-support in technology commercialization,” said Melissa Cruz, CEO of GenIP.

“We are also seeing a rise in inbound referrals from universities that have reported meaningful improvements in their licensing workflows after adopting our evaluations. This combination of repeat business and organic referrals gives us strong confidence in our growth trajectory as we expand our AI-powered product suite and support more clients globally.”

Over the past decade, India’s key growth narratives have centred around three pillars: 1) favourable demographics 2) structural reforms and 3) robust digital infrastructure development. One of the positive fallouts of this is the exponential surge in assets of India’s mutual fund sector.

Transformation of Indian Investment Culture

Historically, Indian families preferred investing in traditional assets like gold, real estate, or bank deposits, leaving equity markets predominantly to international investors. This landscape has fundamentally shifted as millions of households now embrace investing in equity, evolving from conservative savers into proactive wealth builders.

The domestic Mutual Fund industry has experienced significant expansion over last two decades, with Assets Under Management (AUM) multiplying approximately 44 times to reach US$773 billion by March 2025! In the last 5 years itself, it has grown more than 3 times. This tremendous growth stems from sustained capital inflows, currently averaging around $4 billion monthly, with gross inflows through Systematic Investment Plans (SIP) alone contributing over US$3 billion per month. SIPs represent an investment methodology by which a person can contribute fixed amounts to selected mutual fund schemes on monthly, quarterly, or annual basis, typically spanning six months to several years.

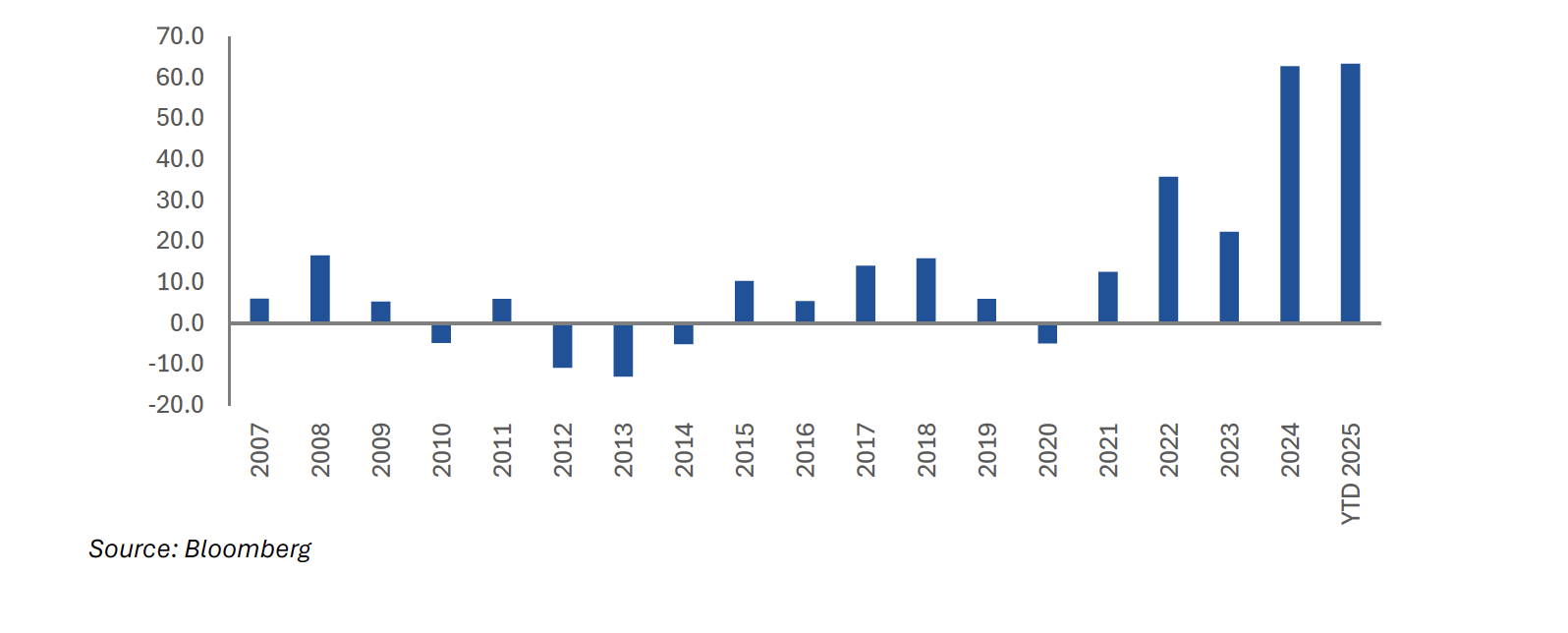

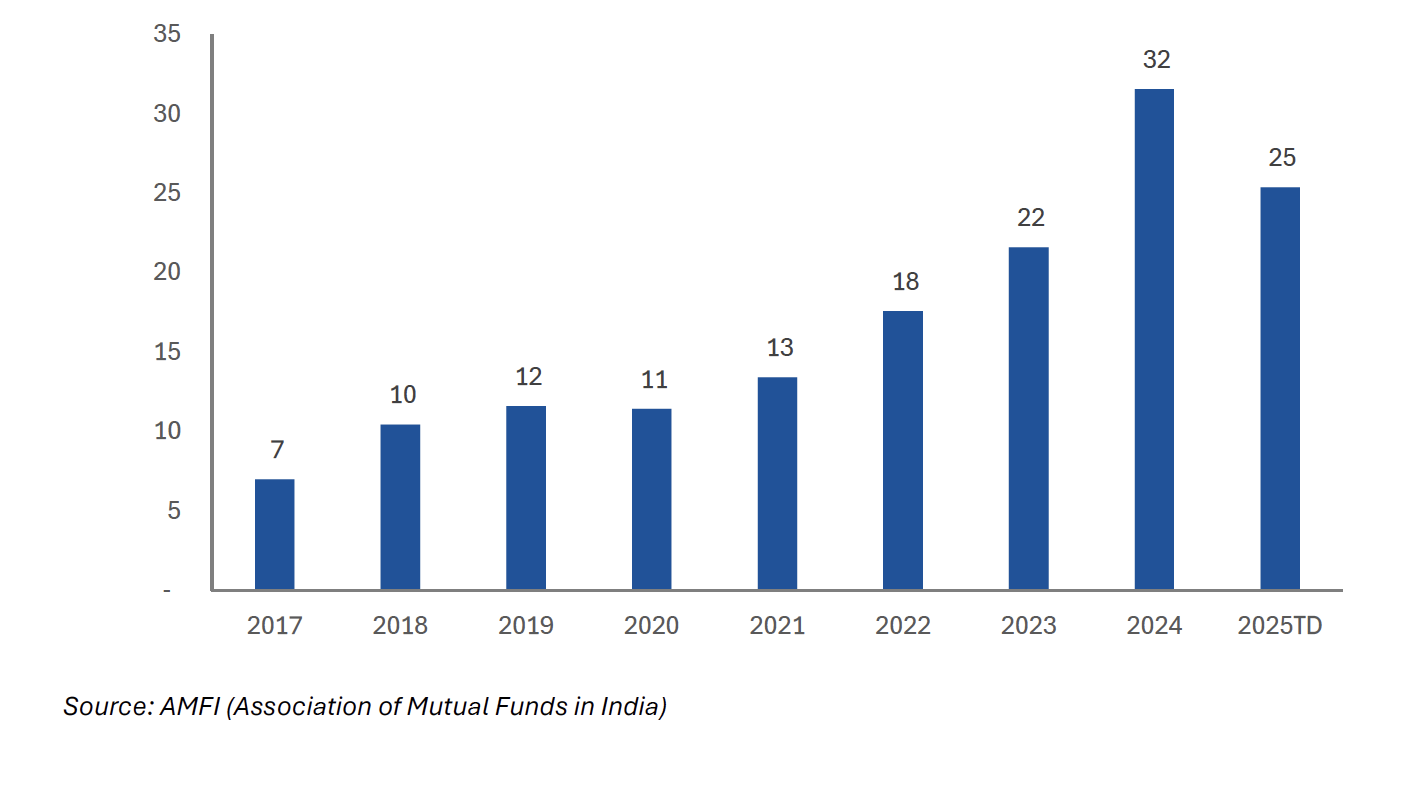

The corporate equity ownership structure reflects this dramatic transformation. Foreign Portfolio Investors (FPI)’s stake at 18.8% in NSE500 companies as of March 2025 is at a decade low, while domestic institutions have reached a record high of 19.2%. In fact, since 2021, domestic institutions have invested over US$192 billion compared to FPIs being net sellers of approximately US$8 billion, highlighting this remarkable reversal.

Figure 1: Domestic Institutional Equity Flows over the years (US$ bn)

Catalytic Events and Digital Revolution

Several pivotal events reshaped this landscape beginning with 2016’s demonetization, which triggered a reallocation of resources from physical to financial assets and led to change in mindset on hoarding cash. Simultaneously, fintech applications emerged during India’s mobile internet expansion, fostering increased digital transaction adoption and confidence. The 2021 COVID-19 lockdowns, combined with elevated savings rates, further accelerated investor migration toward equity markets and mutual funds.

But a lot of credit should go to active marketing by the industry. Since 2017, the Association of Mutual Funds in India (AMFI) has been carrying out an investor education campaign “Mutual Fund Sahi Hai” (Mutual Fund is the Right Choice). Visibility is high, as AMFI strategically positions its advertisements during the Indian Premier League (IPL). The 2025 edition of IPL had over 1 billion viewers across television and digital platforms.

AMFI’s comprehensive marketing initiatives encouraged serious SIP consideration among investors. Mutual funds emphasized affordability with entry points as low as Rs500 (£5), enhancing accessibility and adoption. Consequently, SIP contributions have emerged as the primary driver of sustained inflows, growing from approximately US$350 million a month a decade ago to over US$3 billion a month currently. Active SIP accounts have exceeded 95 million, representing 20% of the industry’s total AUM.

Leading distributors identify liquidity and small ticket sizes as crucial criteria favouring mutual funds over alternative investment options. Retail investors are now looking at investing over a 5–10-year investment horizons, and these are now being looked at akin to an EMI, but for wealth creation. These concepts have resonated with retail investors, resulting in higher mutual fund inflows even during high volatility periods.

Figure 2: Inflows through Systematic Investment Plans (US$ bn)

Digital Infrastructure and Democratisation

The above would not have been possible without the digital revolution which has fundamentally transformed investor behaviour patterns. Tech-savvy younger generations increasingly utilize online platforms and mobile applications for mutual fund investments. User-friendly interfaces have democratized investing, making it accessible to broader population segments, while mutual funds now provide convenient platforms for seamless investment tracking and redemption.

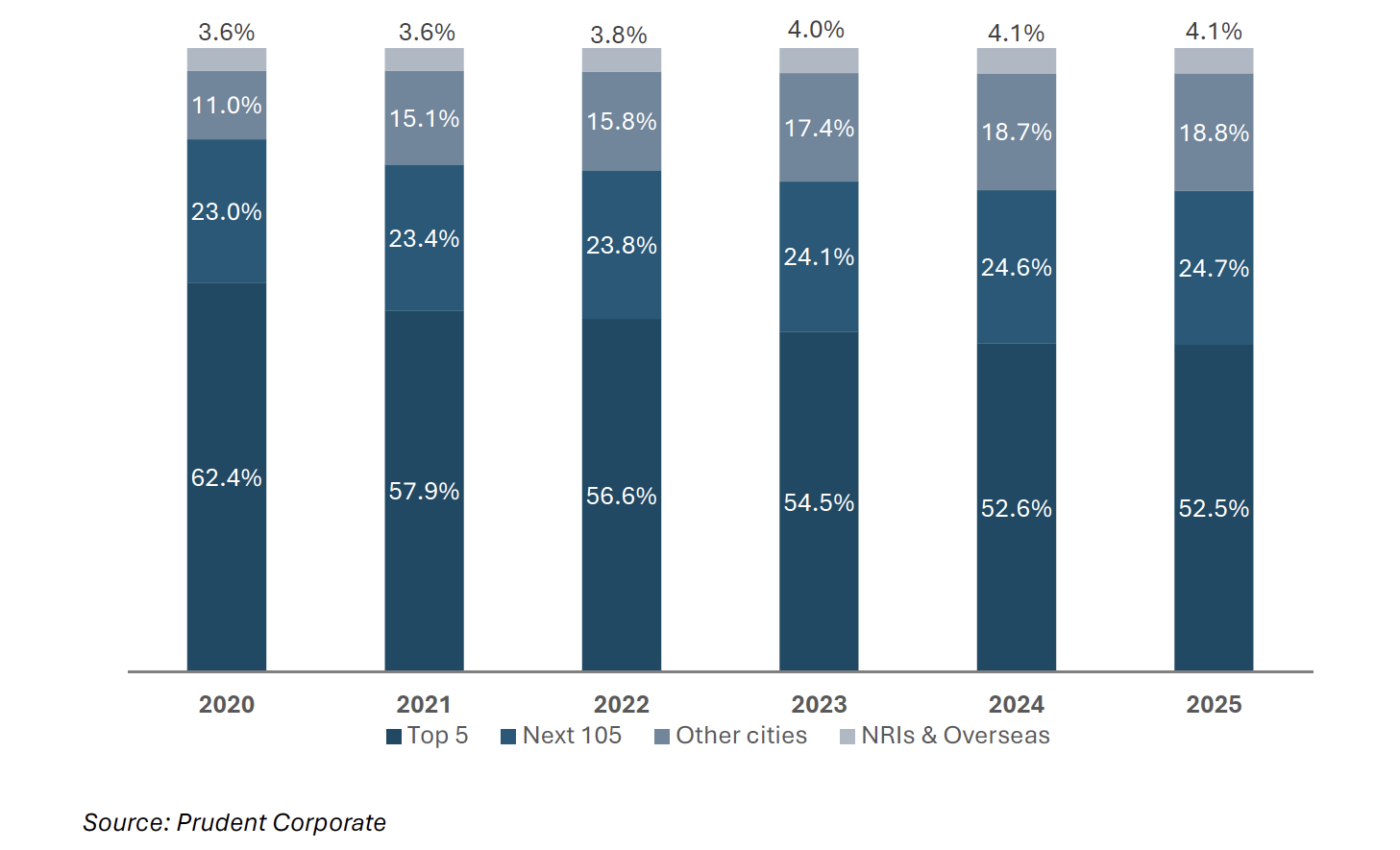

Reflecting the capital markets’ digital transformation, India’s top three brokers are all online/digital platforms: Groww, Zerodha and Angel One. As digital transactions accelerated, mutual funds expanded distribution networks nationwide, increasing participation from smaller towns and semi-urban areas.

According to AMFI data, the top 5 cities’ share declined from 62% in 2020 to 52% in 2025, while contribution from towns beyond the top 110 cities increased from 11% to approximately 19% during the same period. This trend demonstrates investment diversification beyond major metropolitan centres, indicating enhanced financial inclusion and investment activity in smaller cities.

Figure 3: Rising penetration in urban & semi-urban cities

Is it sustainable?

The question we often ask ourselves is whether these domestic flows are sustainable? Even after the strong inflows, mutual fund industry’s current AUM-to-GDP ratio stands at just approximately 20% compared to the US at 100%+, indicating ample room for growth. Mutual funds represent only about 12% of Indian household financial assets (March 2025) versus 20%+ in the USA. Going by macroeconomic factors like young demographics, digitally native population, and higher economic growth, these flows look sustainable.

Notably, mutual fund inflows have demonstrated resilience over the past year despite negative equity returns (-5% for BSE Sensex as of September 30, 2025) and increased volatility from geopolitical disruptions. However, prolonged market consolidation and subdued returns could potentially moderate future flows.

Gareth Powell, Head of Healthcare at Polar Capital, explains why he believes sentiment in the healthcare sector may be bottoming out after almost three years of headwinds.

He highlights three key drivers supporting his outlook: strong volume growth, broad new product cycles, and renewed M&A momentum. With US policy concerns easing, valuations near multi-decade lows, and investor interest starting to return, he sees good reason to be optimistic about the potential for a healthcare recovery.

Poolbeg Pharma (LON: POLB) has been granted a patent for POLB 001 by the European Patent Office. This covers the treatment for severe influenza and there are other potentially patentable uses. The share price gained 10.1% to 4.05p.

Rail and transport data software and services provider Tracsis (LON: TRCS) reported full year figures in line with its trading statement. Tracsis remains highly profitable despite uncertainty in the rail sector and is ready to take advantage when there is more certainty of funding. The share price increased 8.53% to 350p.

US focused oil and gas company Zephyr Energy (LON: ZPHR) says there are growing levels of interest in gas from the Paradox Basin in Utah and the process of securing farm in partners continues. Debt refinancing means that borrowings with the existing provider are $22.1m and a further $2m has been lent by another lender at an interest rate of 14%/year and it can convert at 3.75p/share. The share price improved 6.25% to 2.55p.

Eyewear supplier Inspecs (LON: SPEC) says trading improved in October with order books 10% higher than one year ago. US tariff disruption will affect the timing of shipments. Full year revenues of £191m and EBITDA of £17.7m are expected. The share price recovered 4.82% to 74p.

Video games developer Everplay (LON: EVPL) has appointed Mikkel Weider as chief executive. He was the founder of Nordisk Games and has been on the boards of other games companies. The share price has risen 3.67% to 353.5p.

Ampeak Energy (LON: AMP) has received the final £3.5m of the £8.5m loan from Cardiff Capital Region. This will enable the development of the 480MWh AW2 project at the Uskmouth Energy Park, where Ampeak has a 50% stake. The share price is 1.45% higher at 3.5p.

FALLERS

Industrial equipment distributor HC Slingsby (LON: SLNG) is asking for shareholder approval to leave AIM. The shares are illiquid and the cost of being on AIM adds to the company’s loss. There is already support from shareholders owning 73.2% of the shares. HC Slingsby transferred from the Main Market to AIM on 24 May 2005. It has been on the Londo Stock Exchange for many decades. The cancellation could be on 23 December. No matched bargain facility is planned. The share price dived 52% to 60p.

Whisky supplier Artisanal Spirits (LON: ART) has been hit by the US government shutdown, having already been hampered by tariffs. It is taking more than six weeks to gain approval from the US authorities for new product labels. This means that $3.2m of shipments will not clear customs this year. This will reduce EBITDA by £2m. The US strategy is being changed and the contract with the current distributor will end in March 2026. There will be a stock provision of more than $2m. Full year underlying revenues ae expected to be flat, excluding one-offs. The share price declined 19.8% to 32.5p.

Ex-dividends

Caledonia Mining Corp (LON: CMCL) is paying a quarterly dividend of 14 cents/share and the share price is unchanged at 2160p.

Cavendish Financial (LON: CAV) is paying an interim dividend of 0.3p/share and the share price dipped 0.25p to 10p.

Fonix (LON: FNX) is paying a final dividend of 5.9p/share and the share price slipped 4p to 189p.

FRP Advisory Group (LON: FRP) is paying a dividend of 1p/share and the share price improved 1.5p to 144p.

Greencoat Renewables (LON: GRP) is paying a dividend of 1.7 cents/share and the share price fell 1.7 cents to 67.1 cents.

Young & Co’s Brewery A shares (LON: YNGA) is paying a interim dividend of 12.22p/share and the share price fell 9.5p to 748.5p.

Young & Co’s Brewery shares (LON: YNGN) is paying an interim dividend of 12.22p/share and the share price rose 5p to 635p.

Yu Group (LON: YU.) is paying an interim dividend of 22p/share and the share price declined 35p to 1485p.

The FTSE 100 was sharply higher on Thursday after AI giant Nvidia beat earnings estimates in the US overnight, and Halma and Games Workshop compounded the uptick in sentiment with strong updates.

The FTSE 100 rose on the developments, trading 0.8% higher at the time of writing.

After a couple of weeks of jittery markets and concerns about AI, global equity investors were provided the reassurance they needed overnight as Nvidia reported Q3 revenues of $57bn and, most importantly, issued positive guidance.

“While bubble fears won’t be completely dispelled by last night’s Nvidia earnings, signs of robust demand mean that investors are able to see the upside from here,” said Chris Beauchamp, Chief Market Analyst at IG.

“The 15% stock price drop into earnings, and the accompanying 5% drop in indices, seemed to clear the air nicely, taking out some excessively frothy sentiment. Overall the bulls got what they wanted last night, while bearish investors (hello, Michael Burry) will still be able to argue that such exuberant spending will ultimately end in tears.”

Cloud data centre firms that buy and rent out Nvidia GPUs, including CoreWeave and Nebius, were sharply higher in the US premarket as the AI trade looked to be back on.

Rebounding sentiment around AI fed into a global equity rally, with around 75% of the FTSE 100 constituents trading in positive territory on Thursday.

Games Workshop was the FTSE 100’s top riser, surging 12%, after saying profit before tax would be at least £135m in 2026, up from £126m in 2025.

“A typically short but ultimately sweet trading update from Games Workshop has fired up enthusiasm for the stock in the market today,” said Russ Mould, investment director at AJ Bell.

“Despite a difficult economic backdrop, the company expects to deliver meaningful growth in profit and revenue in the first half of its financial year.

“Games Workshop’s resilience is underpinned by dedicated fans who collect figures and play its games. This success has led to a valuable library of intellectual property, from which it has been able to drive extra revenue. Some may be impatient with the pace of Games Workshop’s efforts to tap into this potential but the company, quite rightly, is protective of its IP and hesitant about agreeing deals which might alienate devotees and tarnish its reputation.”

Halma shares were up around 12% following the release of half-year results that showed revenue rocketed 15% higher during the period. Investors were also clearly delighted to see adjusted profit before tax surge 29%.

JD Sports was the FTSE 100’s top faller as investors digested another lacklustre trading update that pointed to slowing like-for-like sales. Shares were down 3% at the time of writing.

Morningstar believes the UK market is a hidden gem for investors, highlighting its low valuations and the Bank of England’s ability to cut interest rates in its Global Outlook for 2026 report.

UK stocks delivered 20% gains in 2025, among the best globally, yet negative media headlines continue to hold back investors from taking meaningful positions in UK assets, according to Morningstar. Fund flow data shows persistent outflows from UK equity funds throughout 2024 and 2025.

The research house notes that UK equities trade at a price-to-earnings ratio of just 14x, approximately half that of the US, while offering dividend yields that exceed other G7 markets.

From an economic perspective, Morningstar expects meaningful monetary easing throughout 2026 and beyond as labor market conditions cool. With economic conditions getting gloomier by the day, the Bank of England now has greater scope to lower interest rates, which should help put the economy back on track. They expect that lower interest rates will help growth return to its trend pace of around 1.7% in the coming years.

“With economic slack widening, the Bank of England has scope to cut interest rates meaningfully in 2026 – with the full extent of monetary easing not fully priced into money markets, in our view,” explained Grant Slade, Economist at Morningstar.

“With meaningful cuts to public spending unlikely in next week’s budget, we think the UK’s debt metrics are unlikely to materially improve in coming years. Still, we think some of the negativity surrounding the UK’s fiscal profile and its likely impact on medium-term economic performance is overdone.”

UK small-cap stocks remain one of the most undervalued segments, attracting interest from corporate and private equity buyers. Morningsta highlights recent examples, including Carlsberg’s acquisition of Britvic and Thoma Bravo’s takeover of Darktrace.

Morningstar also drew attention to the UK housing sector as offering value, with builders such as Persimmon, Barratt Redrow, and Taylor Wimpey trading at attractive levels. Any reduction in interest rates should act as a meaningful tailwind for the sector, the firm notes.

Looking at gilts, UK government bonds have suffered from concerns about fiscal stability, but Morningstar suggests that much of the weakness stems from liquidity and supply-and-demand dynamics.

Interestingly, demand from defined-benefit pension buyers has fallen by around 50% in recent years, creating a roughly 40 basis points premium in 10-year gilt yields relative to fair value.

For long-term investors, locking in this yield could prove rewarding as markets reprice to reflect normalized conditions, according to the report.