CLIQ Digital (ETR:CLIQ) sell subscription-based streaming services that bundle movies & series, music, audiobooks, sports and games to consumers globally and are now creating shareholder value through increased revenue.

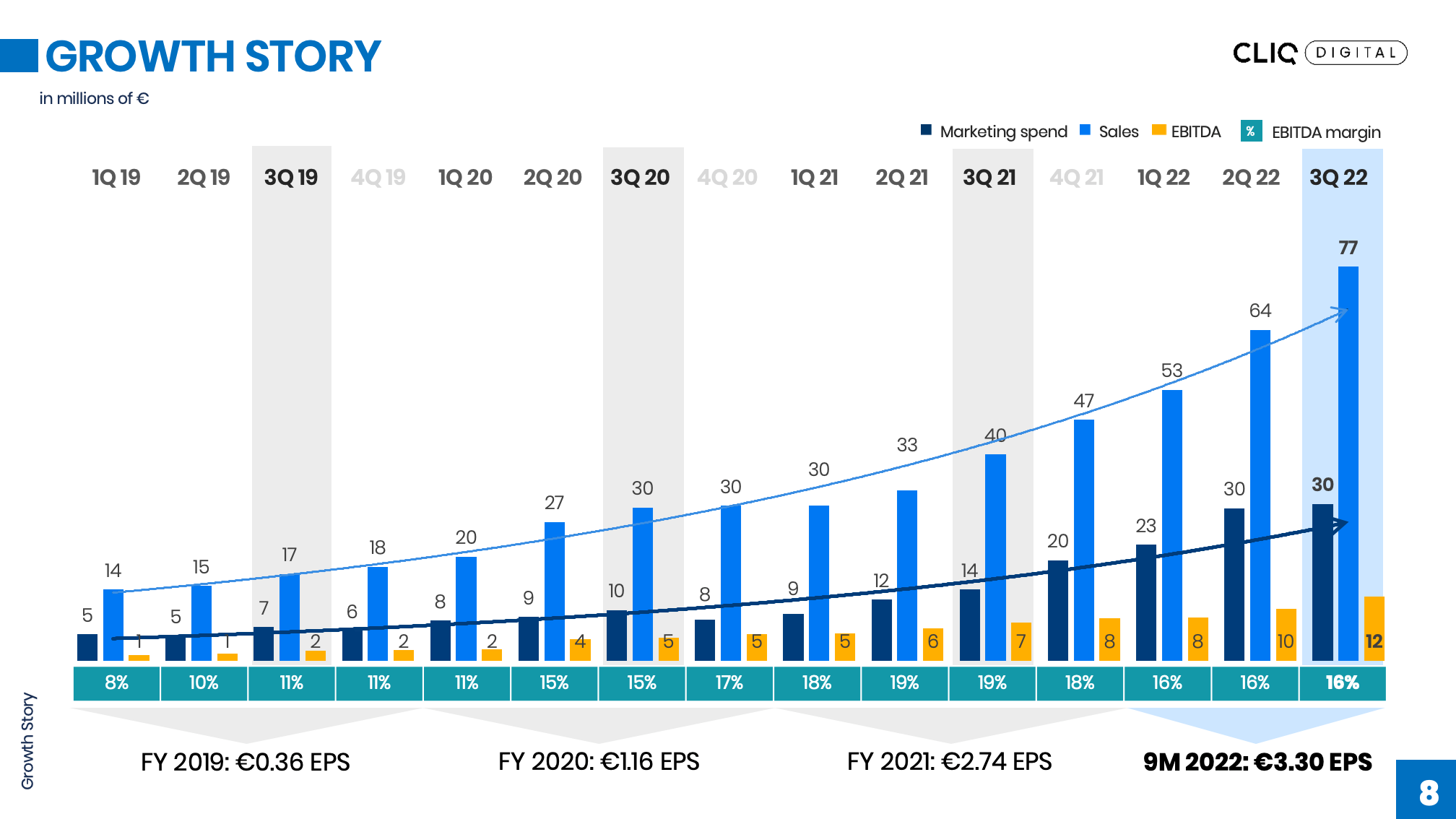

CLIQ Digital have produced consistent revenue growth since the beginning of 2019 and in the most recent quarter recorded a bumper 91% increase in sales.

CLIQ shares are up 54% over the past year to €28.50 and analysts see additional upside to their median fair value price target of €70.

The company is due to report next week and results will be closely watched for further progress in their key profitability metrics to support their already attractive valuation.

Established market position

CLIQ’s success lies in their approach to marketing by sparking the interest of the online consumer in numerous streaming services via a well-designed banner, followed by a membership offer which includes a free trial period. To gain traction in a market with a number of incumbent streaming competitors, CLIQ have taken a more personalised approach to securing memberships.

The strategy has been a two-pronged approach in the targeting of individuals with direct personalised marketing and the creation of services appealing to different groups of media consumers.

Their approach has gained them 1.8 million paid memberships and €8.3m operating free cash flow.

CLIQ Digital have carved out a niche in the streaming market

CLIQ licences its streaming content from partners across those multiple categories. The company stores, bundles and curates digital content in its digital content warehouse. Within the CLIQ Tech Hub data-driven marketing and business knowledge is combined with the company’s digital content warehouse. This enables CLIQ to create attractive streaming services.

Over the years, CLIQ have become experts in online advertising and currently have 1.8 million paid memberships on numerous streaming services across 30+ countries.

CLIQ’s strong track record in building streaming services has brought it closer to achieving its dream: cliq.de – the company’s most advanced all-in-one streaming service for the mass market, which makes streaming content accessible to everyone in Germany.

CLIQ Digital recognises the power of targeted advertising

The mass marketing approach is not appropriate for specialised streaming service. This is one of the reasons CLIQ is selling a bundled streaming service which includes movies & series, music, audiobooks, sports and games. The all-in-one streaming service enables CLIQ to target a wide variety of consumers with the streaming content they like. Direct marketing focuses on effective cost per acquisition as opposed to expensive brand building.

To facilitate their long-term growth ambitions, CLIQ have developed an intricate marketing strategy that focuses on converting customers in a cost-effective manner from online advertising campaigns.

Consistently increasing revenue

CLIQ is debt free and have supported their growth through significant increases in revenue. Sales grew 91% in Q3 2022 compared to the same period a year ago. EBITDA grew 68% over the same period.

The company will report 2022 preliminary results 31st January.