The FTSE 100 saw a sleepy session of trading on Tuesday, with the index rising 0.1% to 7,419.5 in early afternoon trading.

The market dodged the panic across the Asian markets, however, US House Speaker Nancy Pelosi’s visit to Taiwan set off renewed alarm bells as geopolitical tensions flared.

“The FTSE 100 was in consolidation mode on Tuesday morning, trading broadly flat but avoiding the falls seen in Asia overnight,” said AJ Bell investment director Russ Mould.

“As if the market needed something new to worry about, there is now renewed concern about relations between the USA and China as Nancy Pelosi is primed for a visit to Taiwan.”

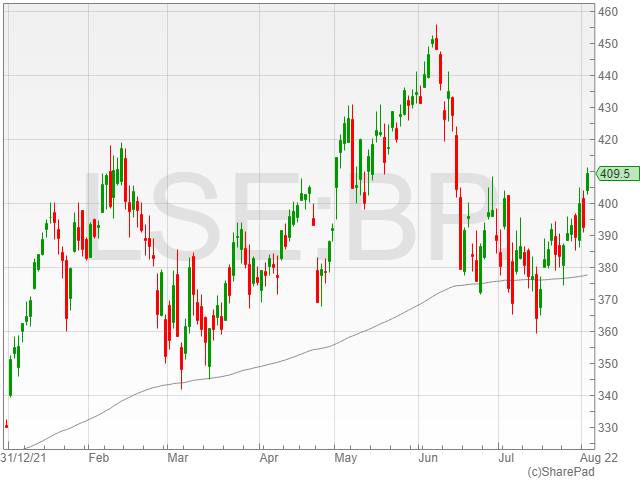

BP

BP shares gained 3.4% to 405.8p after the oil and gas giant reported a banner Q2, with an 85% surge in revenues to $69.5 billion and a $9.3 billion profit after its $20.4 billion loss related to its Rosneft stake in Q1.

BP also announced the launch of a $3.5 billion share buyback scheduled for completion before its Q3 results, straight after the close of its $2.5 billion share buyback in Q2.

The company hiked its dividend 10% to 6c compared to 5.4c the last year.

“BP’s expecting higher oil prices to continue into the third quarter and whilst that’s not good news for consumers, who are battling with higher energy and petrol prices already, it’s good news for cash flows,” said Hargreaves Lansdown equity analyst Matt Britzman.

“In the accommodative environment we’re seeing, BP’s able to push up its dividend and push on with a fresh $3.5bn buyback having only just finished a $2.5bn programme.”

“Markets reacted favourably to what was a set of results that beat estimates across pretty much all metrics.”

Fresnillo

Fresnillo shares sank 5.6% to 687p, falling to the bottom of the FTSE 100 after the gold mining company reported a slate of poor results in HY1 2022.

The mining giant announced a revenue drop of 14.2% to $1.2 billion and a gross profit decrease of 39.7% to $365.9 million, alongside an EBITDA decline of 38.5% to $459.1 million.

Fresnillo blamed its bad results on lower gold volumes and falling silver prices.

The company slashed its dividend 65.7% to 3.4c per share compared to 9c the year before.

Housing market shows signs of slowdown

The housing market saw prices climb 11% in their 12th consecutive month of growth, however the sector appears to have shown initial signs of a slowdown in the months ahead.

The latest report from Nationwide revealed an 11% rise against a 10.7% climb in June, but cracks of weakness in the market included a fall in mortgage approvals as the cost of living crisis started to weigh down the gravity-defying industry.

The market has also been set on alert for the approaching Bank of England meeting, which is expected to hike interest rates as high as 0.5% in a move to tackle soaring inflation and possibly pump the brakes on the runaway housing market.

“Zoopla figures published earlier today there are early signs that the market is starting to slow,” said Hargreaves Lansdown senior pensions and retirement analyst Helen Morrissey.

“Mortgage approvals are starting to decline so we can expect to see activity become more muted as people tighten their belts as their bills continue to increase.”

“The prospect of further interest rate increases on the horizon may also make people think twice about whether they can afford to move home.”

Housing stocks took a hit, with Taylor Wimpey falling 3.9% to 122.9p, Barratt Developments decreasing 3.8% to 486.4p, Berkeley Group Holdings sliding 3.5% to 4,145p and Persimmon dropping 3.1% to 1,843.7p.