Online wine retailer Naked Wine (LON: WINE) had a good Covid lockdown but it is finding it difficult in more normal times. Although a £3m pre-tax profit was reported for the year to March 2022, Naked Wine is set to fall back into loss this year.

Subscriptions boomed when people had to stay at home and could not go out to buy wine or drink in pubs and restaurants. Once signed up the new Angels (subscribers) were expected to continue to be subscriber members.

However, economic uncertainty and inflation mean that ending a Naked Wine subscription could become a way of saving money that is required to cover higher energy and food prices. Last year, repeat customer sales retention fell from 88% to 80% and it is lower than the year before the pandemic. There was a 9% increase in active Angels to 964,000, though.

The five-year forecast payback of the investment in acquiring new customers has declined from 2.6 times to 1.5 times. The year one payback has declined from 82% to 68%.

In 2021-22, US sales fell but were slightly higher in constant currency terms, while UK sales were 10% ahead. The US improved its profit contribution, but only because less was spent on acquiring new customers.

Even last year, people were taking up the introductory offer and then cancelling memberships and there is a new customer recruitment strategy in the UK. The plan is to attract fewer new Angels but improve the quality of customer added. More is being spent on brand marketing and that may help.

Forecast

Peel Hunt has downgraded its 2022-23 expectations from a £1.3m pre-tax profit to a £6.9m loss, even though revenues are forecast to improve from £350.3m to £375.2m, which is at the higher end of the guidance range.

The balance sheet is strong with £39.8m in the bank even though inventories were increased from £76m to £142m. There is a new $60m credit facility.

The share price has fallen by 36.7% to 182p on the back of the 2021-22 results. This shows how unforgiving the market is to even small disappointments.

In the 24 weeks to 17 June 2022, the revenues of leisure products and toys distributor Tandem Group (LON: TND) have fallen by nearly one-third and Cenkos has downgraded its 2022 forecast revenues by £8m to £30m. the share price fell by one-fifth to 240p. Bicycle and home and garden product sales have more than halved so far this year. Pre-tax profit expectations have been slashed from £3.6m to £1.4m and this means that Tandem is likely to go from a net cash position to net debt of £2.6m. There has been an improvement in trading in recent weeks, but the outlook remains uncertain. Construction of the new Birmingham warehouse is on track.

Virtual reality software developer Engage XR (LON: EXR) has announced two partners for its enterprise focused Metaverse, ENGAGE Link. They are HITC, which will be in the enterprise plaza, and The Vitual Human Interaction Lab at Stanford University, which is in the education plaza. ENGAGE Link should launch in the fourth quarter of 2022. The core ENGAGE platform is generating increasing revenues and D’Carrick Co has renewed for three years at a total value of €300,000, an increase from €70,000 a year. The Engage XR share price has been rising for a week and today it added 14% to 14.25p.

Contact centres operator iEnergizer (LON: IBPO) released results for the year to March 2022 and proposed a final dividend of 13.8p a share. That takes the total for the year to 21.92p a share, an increase of 55%. The share price rose 9% to 490.5p. Total revenues were nearly one-third higher at $265.2m and pre-tax profit was 55% ahead at $83.2m. Net debt fell from $115.9m to $100m. Growth should continue with new customers and contract extensions. There was no more news about the strategic review or talks with Mumbai-based BPEA Advisors Private Ltd concerning a potential bid. Canaccord Genuity has been appointed joint broker.

Bango (LON: BGO) has signed an agreement with an unnamed multinational technology company, which will use the Bango platform for carrier billing and bundling services for app store payments and subscription services. This will not have an impact on the current financial year. Bango shares rose 11.5% to 141p.

Argentina-focused oil and gas company Phoenix Global Resources (LON: PGR) has risen a further 0.55p to 6.55p following news earlier in the week concerning discussions with 84% shareholder Mercuria Energy Group about a cancellation of its AIM quotation and a cash offer to purchase shares from independent shareholders at 7.5p each.

Ex-dividends

Support services provider Tribal Group (LON: TRB) is paying a 1.3p a share final dividend and the share price fell 2p to 86p.

Identification services provider GB Group (GBG) is paying a 3.81p a share final dividend and the share price declined 7.5p to 435.7p.

Patent translation services and software company RWS (LON: RWS) is paying a 2.25p a share interim dividend and the share price slipped 4.5p to 349.9p.

Lloyd’s insurance underwriting services provider Helios Underwriting (LON: HUW) is paying a 3p a share final dividend and the share price is unchanged at 162.5p.

Photonics company Gooch & Housego (LON: GHH) is paying a 4.7p a share interim dividend and the shares have risen 15p to 901p.

Government borrowing hit £14 billion in May 2022, representing a £4 billion decrease against 2021 levels, however the borrowing rate was £8.5 billion higher than pre-pandemic levels in May 2019.

The Office of National Statistics (ONS) reported £66.6 billion in central government receipts, representing a year-on-year rise of £3.4 billion, including £48.3 billion in tax receipts.

The report confirmed a central government current expenditure fall of £2.2 billion to £74 billion against May 2021, with the additional £3.1 billion of cost debt interest repayments made in the year-to-date offset by a reduction of £4.9 billion in paid subsidies.

Central government debt hit £7.6 billion, with the RPI on index-linked gilts contributing £5 billion over and above the accrued coupon payments and other components of debt interest.

According to the ONS, May saw the third-highest debt interest payment made by central government in any single month and the highest payment made in any May on record.

“There is nowhere inflation is not making its presence felt and the hike in interest payments on the government’s debt mountain is a prime example – a hike of 70% compared to the same period last year, a record for the month thanks to all those index-linked gilts,” said AJ Bell financial analyst Laura Suter.

“With inflation already at a 40-year high and the expectation that the peak is still to come, the OBR is forecasting that the cost of servicing the debt will hit £87bn this financial year, a cautionary note that is undoubtedly stuck to every whiteboard in the Treasury.”

Public sector net borrowing excluding public sector banks was £14.0 billion in May 2022, the third-highest May borrowing since monthly records began in 1993.

— Office for National Statistics (ONS) (@ONS) June 23, 2022

Public sector net borrowing excluding public sector banks (PSNB ex) dropped £6.4 billion to £35.9 billion year-on-year, however the level was £19.8 billion higher than May 2019.

The ONS announced a central government net cash requirement drop of £12.3 billion to £11.5 billion in May, bringing the total for the financial year to May 2022 to £13.9 billion.

The report added that PSND ex was £2,363.2 billion at the end of May, with an increase of £170.1 billion. The total represented approximately 95.8% of GDP with an increase of 0.5% compared to May 2021.

The ONS also noted PSND ex excluding the Bank of England (PSND ex BoE) rose by £88 billion to £2,041.8 billion, representing around 82.8% of GDP and a reduction of 2.1% GDP year-on-year.

“People are feeling the pinch, the Government has already stepped in with billions of pounds worth of support but there are plenty of voices warning that the help might not be enough to get households through what could be a long, cold winter,” said Suter.

“Pay is the topic du jour and one that’s not going to go away. Employers are in a sticky situation, if they don’t offer their workforce an increase that covers the worst of the inflation uplift they risk good people jumping ship or becoming embroiled in drawn out disputes that spill over into strike action.”

“What is responsible – helping people now or helping the people in the future? The past couple of years have been trying and expensive but the next months are shaping up to be more uncomfortable than anything Covid threw at us.”

Argo Blockchain shares have suffered terribly this year as Bitcoin languishes and other cryptocurrencies capitulate.

The price of Bitcoin has tumbled dramatically in the last week, with the famous cryptocurrency trading briefly trading below $18,000 over the weekend to top off a year of steady declines.

As one would expect from a company inextricably linked to the price of Bitcoin, Argo Blockchain shares have tracked Bitcoin to the downside.

Argo Blockchain shares are currently down 61% year-to-date and are worth around a tenth of what they were at their peak.

Anyone that bought near the peak will unfortunately be deep in the red, but have Argo shares avoided the complete disaster of seeing its price of trading significantly below the 20p-30p range? Argo Blockchain shares spent much of late 2020 trading between 20p-30p and most early stage investors would have bought into prior to the price breaking through this level.

Argo Blockchain Financials

Argo Blockchain has arguably made significant operational steps forward.

Argo Blockchain reported a Q1 revenue rise of 9% to £14.9 million year-on-year, driven by the group’s hash rate growth, which served to offset lower Bitcoin prices in the term, along with an adjusted EBITDA rise of 24% to £14.5 million in its Q1 2022 results.

This followed a 291% jump in 2021 revenue to £74.2 million. With Argo trading 34p the company is valued at only 2x turnover which for many growth companies would suggest deep value.

However, the emphasis for Argo is on their margins and the cost of mining a Bitcoin versus prevailing market prices.

Argo Blockchain confirmed an average cost per Bitcoin mined of $9,779, which currently provides the firm with a gross profit in excess of 100% on the cost of mining the cryptocurrency. This metric is key because if we see Bitcoin fall beneath $9,779 their mining operations will become uneconomical.

Argo Blockchain began mining Bitcoin from its new Helios facility in May, and said it expected to increase its hash rate to 5.5 EH/s by the close of 2022.

The company mined 470 Bitcoin and Bitcoin equivalents, representing a 21% leap in the last year. The group had HODL of 2,700 Bitcoin and equivalents as of 31 March 2022, with a value at the current price of Bitcoin at $55.9 million.

Argo Blockchain currently has a historical PE ratio of 4.6. This does suggest value but these earnings were recorded when Bitcoin was much higher. Any profit margins could be quickly wiped if we see a significant move below $20,000.

However, analyst point to the prior moves in Bitcoin that were reversed over time to eventually see the crypto move to fresh all time highs.

“There is some encouragement for battered Bitcoin investors in the previous price performance of the cryptocurrency. It has suffered crypto winters before and come back to have its day in the sun,” said AJ Bell head of investment analysis Laith Khalaf.

“Indeed, Bitcoin’s worst recent performance saw the cryptocurrency fall by 83% in the year to December 2018. It then went on to reach fresh record highs in 2020 and 2021.”

“So it wouldn’t be a total surprise to see Bitcoin stage a Lazarus-like recovery.”

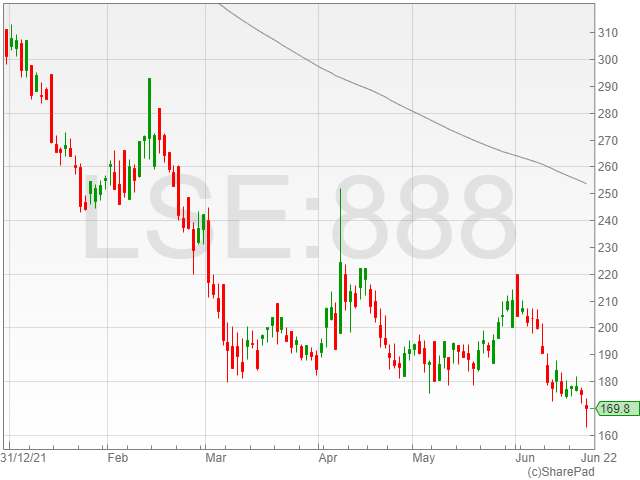

888 Holdings shares were down 2.7% to 170.4p in early morning trading on Thursday, following a reported £690 million in revenue and £109 million EBITDA generated by the company for the twelve months ending 28 February 2022.

The group confirmed William Hill brought in £1.3 billion in revenue and £238 million in adjusted EBITDA for the financial period.

888 Holdings commented that the performance of both businesses largely reflected a constitution of trends outlined in its 29 April 2022 prospectus, with the impact of retail reopening and positive performances across a slate of regulated countries offset by closure in the Netherlands and the effect of additional safer gambling measures in the UK Online sectors of its business.

888 Holdings highlighted an expected revenue between £330 million to £335 million for the six months ended 30 June 2022, broadly meeting board expectations.

The firm noted again that the growth in certain European markets had been offset by the impact of safer gambling measures and its temporary exit from the Netherlands.

William Hill revenue for the 26 weeks ended 28 June 2022 is anticipated between £620 million and £630 million, with capex for 2022 expected to be slightly higher for 888 Holdings and William Hill year-on-year.

The 888 Holdings board has reportedly set a goal of hitting a pro forma net leverage ratio at of below 3.0x in the medium term.

In a separate announcement, 888 Holdings confirmed it expected to market £1 billion aggregate principal amount of senior secured indebtedness, comprising a US dollar-denominated term loan B facility which is scheduled to mature in 2028 and euro-denominated senior secured fixed rate notes due on 2027, alongside euro-denominated senior secured floating rate notes due 2028.

Polymetal shares rose 4% to 187.2p in early morning trading on Thursday after the company reported a business update announcing its gold bullion concentrate sales continued as usual from Kazakhstan.

However, the mining group confirmed that its silver bullion accounted for less than 5% of its estimated 2022 sales, due to a lack of export channels. Polymetal said discussions were underway with a selection of commercial and industrial buyers to offload its accumulating silver inventory.

Polymetal mentioned a net debt increase to $2.3 billion on 1 June 2022 compared to $2 billion on 31 March 2022, which was reportedly driven by large working capital increases and accelerated procurement. The company said 74% of the total debt was denominated in US dollars.

The company added it had approximately $300 million in cash deposited with non-sanctioned financial institutions, alongside the maintenance of $400 million in undrawn credit lines from non-sanctioned banks, which is projected to cover expected debt repayments in the next six months.

Polymetal said it was currently financing short-term working capital requirements with US dollar-denominated debt at lower interest rates, and had recently secured $200 million in new revolving credit lines, with plans to sign an additional $300 million revolving credit facility in June.

The mining firm noted its operations in Kazakhstan and Russia continued without disruption with a production guidance of 1.7 moz for 2022, and its medium-term development projects POX-2, Kutyn, Urals Flotation and Prognoz were on track.

However, the company highlighted that sharp rouble appreciation and continued logistical challenges were contributing significant upward pressure on capital expenditures.

Polymetal also confirmed its 110-kV line linking its Nezhda mine to the regional grid had been successfully commissioned.

The group emphasised the difficulty of its situation concerning shareholder payouts, and commented that the board viewed share buybacks as unwise given the company’s current liquidity challenges and trading uncertainties.

Polymetal reported its dividend would be informed by its delays in establishing new sales channels and its resulting decline in operating cash flows, with its HY1 dividend scheduled to be announced with its results on 22 September 2022.

The company also announced the appointment of MHA MacIntyre Hudson LLP as a group auditor jointly with AO Business Solutions and Technologies as a component auditor for Polymetal. The group confirmed that the company was not subject to any sanctions currently in action against Russia-affiliated entities.

Roquefort Therapeutics (LON: ROQ) has announced its second acquisition in seven months. Cancer medicines company Oncogeni Ltd is being acquired for the issue of 50 million shares and there is a placing to raise £1.01m at 14p a share.

This is the second acquisition since Roquefort floated as a shell on the standard list back in March 2021. The original placing was at 5p a share. Last November, Lyramid was acquired for cash and shares and there was a £3m placing at 10p a share.

The group’s focus is early-stage biotech operations. The latest deal means that it has a portfolio of four cancer programs.

Oncogeni

Two pre-clinical families of innovative cell and RNA oncology medicines come with Oncogeni, as well as a laboratory facility in Stratford-upon-Avon.

Oncogeni’s founder, Nobel Laureate, Professor Sir Martin Evans is joining the board as is Ajan Reginald who will become the new chief executive.

The shareholder base will be widened with new shareholders including global pharmaceutical company Daiichi Sankyo and biotech investor CH Health.

Financial statements for the year to May 2022 show net assets of £14,556. There should be further information released when the proposed acquisition is finalised.

There are programmes for two existing technologies being developed by Roquefort Therapeutics. The ROQA1 and ROQA2 potential antibody programmes demonstrated significant anti-cancer activity in in vivo models of metastatic tumours. The other technology programme has demonstrated that lead oligonucleotide drug candidates significantly reduce Midkine mRNA levels in human cancer cells.

Xeros Technology Group shares fell 1.6% to 40.8p in late afternoon trading on Wednesday following an adjusted EBITDA loss of £6.3 million against £6.8 million, and a pre-tax operating loss of £6.9 million compared to £7.6 million in FY 2021.

The group reported a revenue growth of 23.1% to £500,000 from £400,000 year-on-year as a result of licence partner sales in HY2 2022 driving revenue growth and margin increase.

Xeros Technology noted a reduction in administrative expenses of 4.8% to £7.2 million compared to £7.6 million and a net cash outflow from operations reduction of 8.3% to £5.8 million against £6.3 million. The company mentioned cash at 31 May 2022 of £4.3 million.

The firm announced a selection of highlights across the year, including the first licence of its XFilter to a leading domestic washing machine component supplier and the planned domestic launch of its machine technology by a leading Indian manufacturer in Q4 2022.

Xeros Technology also reported its Denim Finish technology had been trialled by multiple major retail brands and its new Xeros brand identity and marketing programme had been launched to drive growth.

The group confirmed its cash burn rate remained at planned levels of £500,000 per month in the financial year.

The company mentioned its revenue was entirely in the hands of third parties, which rendered its intake difficult to predict. However, Xeros Technology said it expected to achieve EBITDA profitability and cash breakeven in 2024 based on its existing and targeted contracts.

The firm added that it expected further levels of investment to fund its business in FY 2023, with its board currently working on plans to secure the necessary investments.

“This has been a year of significant progress in embedding Xeros’ technologies into product lines of key licensing partners laying a strong foundation for future growth,” said Xeros chairman Klaas de Boer.

“The transformation of the Xeros brand and the supporting marketing programme are key to accelerating the commercialisation of our transformational technologies.”

Landore Resources shares fell 4.5% to 20.2p in late afternoon trading on Wednesday, after the company announced a widened post-tax loss of £3.9 million from £2.5 million in FY 2021.

The mining group reported that operating expenses were in line with its budget and expectations, with financing secured of £3.5 million in February 2021 by the issuance of shares for 30p per share.

Landore Resources confirmed no debt and commented it was capable of raising additional equity where required to execute its development plans.

The company highlighted several of its ongoing operations at its Junior Lake property, including its BAM gold deposit, in which a total of 353 NQ and HQ diamond drill holes for approximately 69,857 metres had been completed with a discovery rate of 21 ounces of gold for every metre drilled.

“During 2021 all of Landore Resources’ exploration efforts were focussed on the Junior Lake property; drilling to further infill, extend and deepen the BAM Gold resource to 1,496,000 ounces of gold – a considerable increase of 481,000 ounces (47%) from the 2019 Mineral Resources Estimate,” said CEO Bill Humphries.

The firm also mentioned its battery metals deposit, which currently hosts two defined deposits in B4-7 and VW with a combined 55,581 tonnes of Nickel Equivalent Metals and potential for growth. The group is currently reviewing the deposits with the aim of maximising its value for the electric vehicles sector.

Landore Resources said its planned works for 2022 included recommencement of drilling at the BAM gold deposit in July, alongside drilling the highly prospective Felix area along strike and to the west for gold and battery metals.

The company is also scheduled to kick off drilling on the Lamaune gold deposit to advance it to defined resource status.

The mining group added it had plans to commence feasibility studies in HY2 2022 on the BAM gold deposit as the resource passed the one million ounce target.

“On behalf of my fellow directors I wish to thank our shareholders for their continued support together with Landore’s Management and Exploration team for their dedication and perseverance in advancing our highly prospective Junior Lake Property,” said Humphries.

The FTSE 100 was down over 1.5% in early afternoon trading on Wednesday in light of the Office of National Statistics’ (ONS) latest inflation figures for May, which saw UK CPI hit another 40-year record of 9.1%.

The reading was in line with economists expectations and markets are bracing for a further squeeze on consumers this summer.

“There may have been a bit of relief this morning that UK consumer price inflation, while still at decades-long highs, was nonetheless bang in line with expectations,” said AJ Bell investment director Russ Mould.

“However, this relief will have rapidly dissipated as it dawned that retail prices are now experiencing double-digit increases and factory gate prices are above forecasts and the highest since the 1970s.”

“The FTSE 100, which has held up better than many of its global peers, is now flirting with a drop below the 7,000 mark for the first time since the March sell-off.”

— UK Investor Magazine (@UKInvestorMAG) June 22, 2022

All eyes are primed to turn to the US Federal Reserve and chairman Jerome Powell for hints of the institution’s next move on monetary policy.

“Inflation will also be on the agenda when US Federal Reserve chair Jerome Powell testifies before lawmakers in Washington,” said Mould.

“His comments will be closely followed for clues on what the Fed might do next with monetary policy and whether the risks of a recession in the world’s largest economy are increasing.”

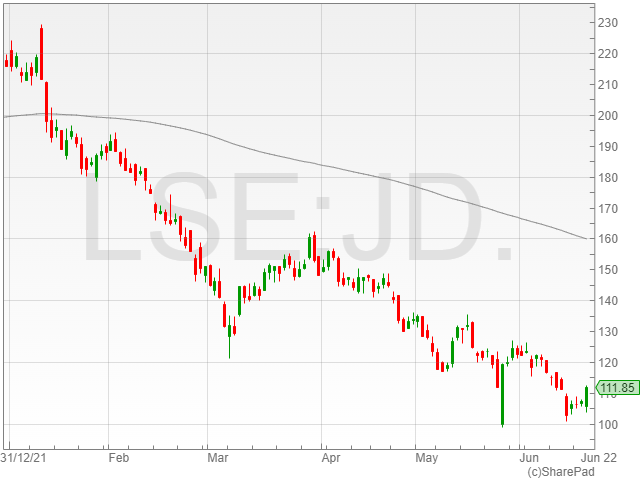

JD Sports Fashion

JD Sports Fashion shares gained 4.9% to 112p on a strong slate on results, including revenues of £8.5 billion and record pre-tax profits before exceptional items of £947.2 million.

However, analysts warned that the company’s good news only accounted for its results before the Ukraine war, and economic volatility combined with the rising cost of living is set to see JD Sports expect no growth in FY 2023.

— UK Investor Magazine (@UKInvestorMAG) June 22, 2022

“While JD Sports has reported a record set of results, it must be noted that this financial period ended before the Ukraine crisis unfolded and inflation surged higher,” said Mould.

“Therefore, it is not representative of the current environment in which consumers are under considerable financial pressure and are losing confidence with regards to the economic outlook, which will curb their ability and willingness to keep spending at levels seen in 2021.”

“This headwind is clear to see in the retailer’s forward earnings guidance. After seeing pre-tax profit more than double in the past financial year, JD now expects no profit growth at all in the current year.”

Natwest shares rise as Oil Price Falls

Natwest shares rose 4.1% to 230.5p after the UK government confirmed it would continue to sell down its stake in the bank for the next year.

The trading plan reported in July 2021 is set to end no later than 11 August 2023 and will continue under the management of Morgan Stanley with unchanged conditions.

Meanwhile, Shell and BP took a hit as the price of oil dipped below $110 per barrel to $109 for benchmark Brent Crude, with shares falling 3.1% to 2,084.2p and 2.7% to 384.6p, respectively.

Berkeley Group and Housing Market

Berkeley Group shares fell 3.5% despite a pre-tax profit growth of 6.4% to £551.5 million and a revenue climb of 6.6% to £2.3 billion year-on-year on the back of the strong housing market in FY 2022.

However, with interest rates rising to 1.25% and inflation speeding rapidly towards 11% in October, it appears the cost of living crisis might serve to bring the housing market back to ground level.

The housing giant’s drop in cash from £1 billion to slightly above £250 million might also give investors reason to be nervous over the firm’s prospects in FY 2023.

Berkeley Group profits climb to £551.5m, higher prices absorb cost inflationhttps://t.co/YLjyT4V3md

— UK Investor Magazine (@UKInvestorMAG) June 22, 2022

“Berkeley is known as the cream of the crop when it comes to housebuilders and its latest update suggests it is continuing to deliver on its strategy which involves taking brownfield land and turning it into desirable housing developments,” said Mould.

“It’s worth noting the significant drop in its net cash position from more than £1 billion to a little more than £250 million.”

“While this was used to invest for future growth and Berkeley still enjoys a healthy buffer, there may be some concern among shareholders that the company doesn’t have more cash on hand to help sustain capital returns if there is a pronounced downturn in the housing market.”

Housebuilder shares across the market dropped as the cost of living crisis threatened the gravity-defying industry, with Persimmon sliding 2.5% to 1,802.5p, Barratt shares dipping 0.8% to 456p and Taylor Wimpey shares dropping 1.7% to 115.2p.