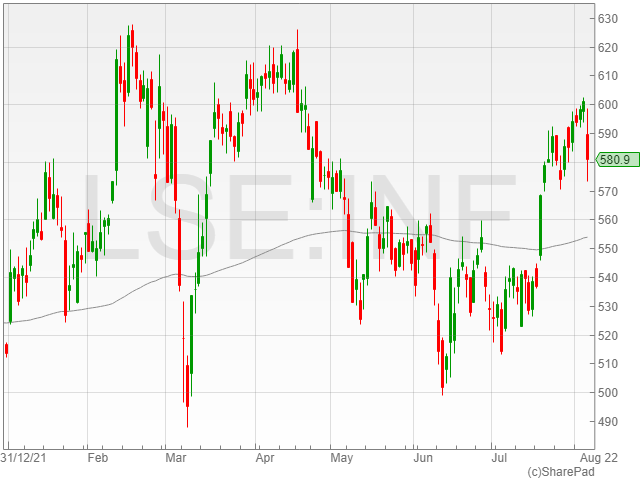

Informa shares fell 3.5% to 579.6p in late morning trading on Thursday, despite a 59.1% HY1 2022 revenue increase to £1 billion compared to £688.9 million the last year.

The exhibitions group confirmed an adjusted operating profit climb of 226.6% to £234.5 million against £71.8 million in HY1 2021 as a result of strong revenue and effective cost management.

Informa reported a statutory operating profit of £90.9 million compared to a £55.4 million loss in the previous year, due to higher revenues, lower Covid-19 exceptional costs and profit growth on divestment.

The company mentioned a higher free cash flow of £178.4 million from £134.1 million, including a doubled capital reinvestment into digital services and enhanced technology capabilities.

Its GAP II strategy also served to boost its revenues and profits across the interim period, with its investment programme reportedly progressing according to schedule.

“As outlined in our recent Market Update, Informa’s first half results underline the benefits of our GAP II strategy, with strong growth in revenues, profits and cash,” said Informa CEO Stephen A. Carter.

“We remain on track to achieve the upper-end of 2022 guidance, with good forward visibility in Subscriptions, Exhibitors, Delegates and Digital Services, whilst continuing to deliver accelerated shareholder returns, additional growth investment and further targeted expansion.”

Informa also resumed its dividends on the strength of its balance sheet and confidence in future cash flow growth, recommending a dividend of 3p per share for the HY1 2022 period.