Retailer TheWorks.co.uk (LON: WRKS) is closing its online channel and moving to a non-transactional website. Online is making a small and reducing contribution to revenues. There will be exceptional costs of £2m. There are plans to open more stores. Like-for-like growth has been 3.3% this year and the company expects to meet market EBITDA expectations of £11m, or £13.5m for continuing activities. Without the online loss, 2026-27 EBITDA has been upgraded from £12.7m to £15m. The share price rebounded 16.5% to 43p.

Spreadex has increased its interest in Geo Exploration (LON: GEO) from 9.79% to 10.9%, including 8.79% held via financial instruments. The share price increased 12.55 to 0.1125p.

Emmerson (LON: EML) has raised £750,000 at 2p/share and retail offer could raise up to £100,000. The cash will fund work in Morocco while Emmerson goes through the arbitration process over the Khemisset potash project in Morocco. The share price improved 4.88% to 2.15p.

Healthy snacks producer Tooru (LON: TOO) has secured new listings and distribution agreements in the UK and Switzerland. Stock availability has been improved for Pulsin. Shareholders are being offered discounts on Oaf gluten free, Juvela and Pulsin products. The share price rose 4.76% to 0.22p.

FALLERS

Sound Energy (LON: SOU) has raised £500,000 at 5p/share and secured a €1.3m term loan facility agreement, which has an interest rate of 205 each 120 days. The loan drawn down and interest is payable by the end of 2026. The Tendrara phase 1 Micro-LNG development has fully tested and commissioned the Tendrara gas gathering system. Commercial gas sales could start in the third quarter because of delays in the delivery of equipment for the plant. A joint venture will develop solar power plants in Morocco. The share price slumped 38.2% to 5.25p.

Kefi Gold and Copper (LON: KEFI) has raised £34m at 1.2p/share. A retail offer could raise a further £1m. The cash will go towards completing the $330m funding for the Tulu Kapi project in Ethiopia and there is extra cash available for working capital. The share price slipped 10.6% to 1.2475p.

Heinrich Müller and Luis Felipe Azevedo, who is replacing his father, have been appointed to the board of Jangada Mines (LON: JAN). they will help to build a Brazil-focused gold resource company. The share price declined 5.26% to 1.35p.

Atlantic Lithium (LON: ALL) says the Ewoyaa lithium mining lease has been ratified by the Parliament of Ghana. This provides exclusive rights for mining and production for an initial 15 years. The spodumene royalties range from 5% for a spodumene price of up to $1,500/tonne to 12% for a price above $3,200/tonne. The share price fell 5.39% to 17.975p.

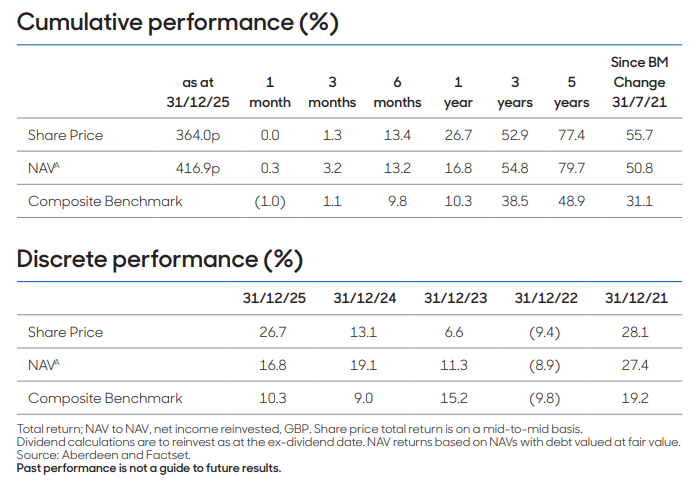

Temple Bar Investment Trust, the investment trust that focuses on intrinsic value and long-term growth by investing primarily in UK-listed securities, has today announced annual results for the year ended 31 December 2025.

The trust delivered a net asset value total return of 33.9% over the year, way ahead of its benchmark FTSE All-Share Index, which returned 24%. The share price total return was even stronger at 45.3%, helped by a sharp narrowing of the discount and a move into a premium.

Since Redwheel took over portfolio management at the end of October 2020, the total NAV total has returned 199.8% versus 103.7% for the benchmark. This is a highly commendable outperformance of 8.9 percentage points a year.

Lifting the lid on performance in what was a strong year for UK stocks, Temple Bar’s returns were driven primarily by stock selection rather than broader market movements, as demonstrated by the outperformance of the benchmark and driven by the portfolio manager’s focus on company fundamentals, valuation discipline, and active engagement with investee companies.

The trust noted that profits were taken in several strong performers during the year, notably in banks and insurance stocks, with the proceeds recycled into new positions including Johnson Matthey and Smith & Nephew.

According to Temple Bar’s latest fact sheet, top holdings as of 28 February were BT (5%), Shell (4.8%), BP (4.1%), Marks & Spencer (4.0%), and NatWest (3.9%).

Investors will be delighted to see the dividend rise 33.3% to 15 pence per share, representing a yield of 4% at the year-end. Those investors buying now will have a yield of around 4.1% after the recent bout of volatility.

Plans are to increase quarterly payments to 3.9 pence per share in 2026, taking the full-year total to 15.6 pence.

Of that total, 3 pence per share will be funded from capital reserves, a policy introduced to reflect the growing proportion of UK corporate distributions being returned through share buybacks rather than dividends.

In their commentary on recent performance, the trust acknowledged that UK equity valuations have risen but noted this was from a very low post-COVID starting point, and that UK-listed companies continue to trade at significant discounts to international peers. This underpins their strategy.

“The combination of strong performance, a rising dividend and increased marketing has led to significant demand for the Company’s shares, particularly from retail investment platforms such as interactive investor and Hargreaves Lansdown,” said Charles Cade, Chairman of Temple Bar Investment Trust.

“This has helped move the Company’s share price to a premium to Net Asset Value per share. I am pleased to report that as a result, the Company was able to re-issue 5,045,000 shares out of treasury during the year at an average premium of 3.0%, raising £18.6m. Since 31 December 2025 to 18 March 2026, further shares have been re-issued from treasury and as a result, the Company’s market capitalisation is £1.1bn at the time of writing, up from £776m at the start of 2025.

“In our last annual report, we highlighted that the Board monitors the Company’s investable universe to ensure that the Portfolio Manager has a large enough opportunity set to build a diversified portfolio of attractively valued investments. At present, the Portfolio Manager continues to believe that the opportunity set is large enough under the Company’s current investment restrictions. However, should the universe of UK listed companies continue to reduce materially, the Board may in the future propose a broadening of the investment policy to increase the ability of our Portfolio Manager to access overseas opportunities beyond the current 30% limit.”

Investors pay extra fees for active management. As a result, they’re likely to feel disappointed – if not thoroughly deceived – if they find an actively managed fund conspicuously mirrors its benchmark.

The debate over how much a portfolio should differ from its underlying index in order to avoid accusations of “tracking” has been raging for years. It’s now two decades since some kind of answer first began to emerge, courtesy of a pair of finance professors at Yale University.

Published in 2006, Martijn Cremers and Antti Petajisto’s groundbreaking research coined the term “active share”. This describes the proportion of a portfolio’s holdings that deviate from its benchmark index.

A pure index fund has an active share of 0%, while a fund that has zero overlap with its benchmark has an active share of 100%. Cremers and Petajisto proposed that funds with an active share of between 20% and 60% should be classed as what are now commonly branded “closet trackers”.

Aberdeen Asia Focus generally has an active share in the upper 90s relative to the MSCI AC Asia ex Japan Small Cap Index, reflecting a high degree of deviation from the benchmark rather than any indication of reduced investment risk.

The explanation for this is simple enough: the fundamental purpose of deviating from a benchmark is to outperform it. In other words, we don’t want to be the market – we want to beat it. But does a fund like ours hope to outperform merely on the strength of being contrarian or is there a more rigorous approach at play here?

The importance of digging deeper

I hope you won’t be too surprised to learn that, at least as far as we’re concerned, the latter is the case. In our opinion, a high active share is a consequence of informed stock-picking – and informed stock-picking, in turn, is in large part a consequence of direct engagement.

Particularly in a market like Asia, many investment teams prefer to observe from a distance. They often rely on quantitative data and the work of third-party analysts to identify companies worthy of inclusion in portfolios.

It’s right to say this can succeed. It’s perfectly possible for investors to earn an acceptable return from a passively managed, quant-driven index fund.

Yet it could be argued that numbers alone might not tell the whole story. For instance, an apparently impressive financial statement might conceal the weaknesses of a business that has done well over the short term but has no meaningful plan for the way ahead.

In addition, many of Asia’s smaller companies – the arena in which we invest – attract no third-party analysis in the first place. There might be an abundance of numbers out there, but it doesn’t automatically follow that someone will obligingly crunch them.

This is why an on-the-ground presence can deliver such valuable insight. In our view, “being there” – genuinely getting to grips with places, people, policies and practices – is vital to identifying unrecognised opportunities in some of the world’s most exciting economies.

The hunt for hidden gems

So what exactly do we hope to learn when we carry out site visits and conduct face-to-face discussions with senior managers in Asia? Ultimately, we’re looking for compelling evidence that a company is capable of long-term growth.

Again, especially in an era when disclosure pressures are mounting and AI is transforming how information is gathered and processed. you might think a raft of readily available data should tell the tale. Sure enough, it can play a significant role.

Yet it’s almost always instructive to get a first-hand look “backstage”. In our experience, discovering whether the image a business projects is an accurate reflection of what’s going on behind the scenes can be extremely useful.

Maybe above all, in-person dialogue is tough to beat. Meeting with executives and asking them questions – some straightforward, some awkward – is one of the most powerful means of establishing whether a company truly has a strategic vision for the future.

It’s important to note that active share can be “gamed”. It’s sometimes cited as a classic example of Goodhart’s Law – named after economist Charles Goodhart, who posited that a measure stops being useful when it becomes a target. However, this is likely to occur only if managers select off-benchmark stocks purely so they can present investors with an eye-catching active share percentage.

That’s not how we do things. Our commitment to direct engagement underlines our determination to be genuinely different – not just for the sake of it but because we firmly believe there’s real merit in seeking out Asia’s hidden gems.

Investment objective

The Company aims to maximise total return to shareholders over the long

term from a portfolio made up predominantly of quoted smaller companies in

the economies of Asia excluding Japan.

Comparative benchmark

With effect from 1 August 2021 the MSCI AC Asia ex Japan Small Cap Index

(currency adjusted) was adopted as the comparative index and performance

is also measured against the peer group. Given the Manager’s investment style,

it is likely that performance will diverge, possibly quite dramatically in either

direction, from the comparative index. The Manager seeks to minimise risk by

using in depth research and does not see divergence from an index as risk.

Important information

The value of investments, and the income from them, can go down as well as up and investors may get back less than the amount invested.

Past performance is not a guide to future results.

Emerging markets tend to be more volatile than mature markets and the value of your investment could move sharply up or down.

Investment in the Company may not be appropriate for investors who plan to withdraw their money within 5 years.

The Company may borrow to finance further investment (gearing). The use of gearing is likely to lead to volatility in the Net Asset Value (NAV) meaning that any movement in the value of the company’s assets will result in a magnified movement in the NAV.

The Company may accumulate investment positions which represent more than normal trading volumes which may make it difficult to realise investments and may lead to volatility in the market price of the Company’s shares.

The Company may charge expenses to capital which may erode the capital value of the investment.

The Company invests in smaller companies which are likely to carry a higher degree of risk than larger companies.

Movements in exchange rates will impact on both the level of income received and the capital value of your investment.

There is no guarantee that the market price of the Company’s shares will fully reflect their underlying Net Asset Value.

As with all stock exchange investments the value of the Company’s shares purchased will immediately fall by the difference between the buying and selling prices, the bid-offer spread. If trading volumes fall, the bid-offer spread can widen.

The Company invests in emerging markets which tend to be more volatile than mature markets and the value of your investment could move sharply up or down.

Specialist funds which invest in small markets or sectors of industry are likely to be more volatile than more diversified trusts.

Yields are estimated figures and may fluctuate, there are no guarantees that future dividends will match or exceed historic dividends and certain investors may be subject to further tax on dividends.

Other important information:

The details contained here are for information purposes only and should not be considered as an offer, investment recommendation, or solicitation to deal in any investments or funds and does not constitute investment research, investment recommendation or investment advice in any jurisdiction. Any data contained herein which is attributed to a third party (“Third Party Data”) is the property of (a) third party supplier(s) (the “Owner”) and is licensed for use with Aberdeen. Third Party Data may not be copied or distributed. Third Party Data is provided “as is” and is not warranted to be accurate, complete or timely. To the extent permitted by applicable law, none of the Owner, Aberdeen, or any other third party (including any third party involved in providing and/or compiling Third Party Data) shall have any liability for Third Party Data or for any use made of Third Party Data. Neither the Owner nor any other third party sponsors, endorses or promotes the fund or product to which Third Party Data relates.

The Aberdeen Asia Focus PLC Key Information Document can be obtained here.

Issued by abrdn Fund Managers Limited, registered in England and Wales (740118) at 280 Bishopsgate, London EC2M 4AG. The company is authorised and regulated by the Financial Conduct Authority in the UK.

The Works shares surged on Friday after it announced it had shut down its online shop with immediate effect, declaring the loss-making channel “no longer sustainable” after years of problems with third-party fulfilment partners.

Shares were 19% higher at the time of writing.

The value retailer, which sells books, arts and crafts supplies, stationery and toys across more than 500 UK stores, said its website would become a non-transactional “shop window”, letting customers browse the range but directing them into stores to buy.

Online never accounted for much of the business, contributing less than 10% of group sales.

But operational failures at two separate fulfilment partners over the past two financial years had made it a thorn in the side of an otherwise thriving business, wiping out the progress the company had been making on the channel’s functionality and profitability.

The board said it had assessed a wide range of options before concluding the best course was to walk away entirely. Exceptional closure costs of around £2 million will be recognised in the current financial year, with the online operation treated as a discontinued business in the accounts.

The group will now refocus on its physical stores, where like-for-like sales are up 3.3 per cent year to date.

The company plans to open a net five new shops this year and ten more in FY27, with scope for a further 100 locations beyond that.

Full-year guidance for FY26 is unchanged at an adjusted EBITDA of £11.0 million on a total basis, and is restated to £13.5 million for continuing operations once online losses are stripped out.

FY27 guidance has been upgraded from £12.7 million to £15.0 million, reflecting both the improving core business and the removal of the drag from e-commerce.

The Works said it remains on track for its medium-term target of at least £22.5 million in EBITDA by FY30, and now expects to reach it with lower sales than the original £375 million goal.

“We have reached this decision after a thorough assessment of the options available and are confident that focussing on our successful bricks-and-mortar business is the right step to reduce risk, improve operational clarity and support long-term profitable growth. A website that enables customers to browse our products and seek inspiration will help to bring our brand to life and drive customers to our 500 stores,” said Gavin Peck, Chief Executive Officer of The Works.

“Our mission – to become the favourite destination for affordable, screen-free activities for the whole family – has never been more relevant and this, combined with ongoing delivery of our ‘Elevating The Works’ strategy, means we are well-positioned to achieve significant and profitable growth in the years to come.”

J D Wetherspoon posted a sharp drop in half-year profits despite healthy sales growth, as rising wages, repair bills, and business rates ravaged margins.

Revenue for the 26 weeks to 25 January 2026 rose 5.7% to £1,088 million, with like-for-like sales up 4.8 per cent.

Bar sales climbied 7%, while food edged up 1.3% nd slot machine income jumped 8.9%. Hotel room revenue dipped 0.6% after the company dropped third-party online booking agents due to high commission charges.

Revenue growth, by all accounts, was very respectable given the economic backdrop; however, it was wiped out by cost increases.

Wages alone rose by £28 million, repairs added £10 million, and business rates contributed a further £9 million. The result was a pre-tax profit before separately disclosed items of £22.4 million, down 31.9% from £32.9 million a year earlier. Operating profit fell 18.4% to £52.9 million.

Earnings per share dropped to 15.5p from 21.5p, while the interim dividend was held flat at 4.0p.

Wetherspoon shares were down 9% at the time of writing.

Chairman Tim Martin used the results to renew his long-running campaign for VAT parity with supermarkets, noting that while sales per pub are now 35 per cent above pre-pandemic levels, energy and wage costs have risen even faster.

He pointed to Morgan Stanley research showing pubs have lost half their beer trade since 2000, including roughly 15% since the pandemic.

“The latest ‘CGA RSM Hospitality Business Tracker’, for February 2026, said industry like-for-like sales were -0.2%. During this period, Wetherspoon like-for-like sales were +3.2%. This was the 42nd month in a row that Wetherspoon has outperformed the tracker,” said Tim Martin, the Chairman of J D Wetherspoon.

“As previously indicated, increases in national insurance and labour rates will result in cost increases of approximately £60 million per annum, and non-commodity energy costs will add £7 million. The ‘Extended Producer Responsibility’ tax, a levy on packaging will cost £2.4 million in the current year, an increase of £1.6 million. These cost increases will undoubtedly add to underlying inflation in the UK economy, although Wetherspoon, as always, will endeavour to keep price increases to a minimum.”

The estate stood at 794 managed pubs at the period end, with plans to open around 15 more this year. Wetherspoon’s franchise programme is also gaining traction — eight new franchised sites opened in the half, taking the total to 16, with another 15 to 20 expected this financial year.

Sancus Lending (LON: LEND) has agreed an extension of the redemption date for preference shares from 23 November 2026 to 11 February 2031. They will no longer be at a fixed interest rate of 15% and instead there will be a floating rate. Some will be redesignated as Euro preference. The preference shares holder will also subscribe for £750,000 of bonds. Sancus Lending reported a 2025 pre-tax profit of £1.2m, including gains of £2.6m on buying back some zero dividend preference shares. The share price jumped 43.8% to 1.15p.

Strategic Minerals (LON: SML) is raising £4.7m at 3.5p/share and despite the discount the share price gained 11.9% to 4.7p. A prominent international investor approached the company. The cash will be spent on the Redmoor Tungsten-Tin-Copper project in Cornwall.

Video games publisher and distributor tinyBuild (LON: TBLD) grew 2025 revenues by 17% and gross profit by 59%. Revenues were slightly below expectations, but EBITDA was higher than expected at $5.6m. The company has seven titles in the Steam Top 200 Wishlist Chart. Net cash if $4.6m. The share price rebounded 8% to 6.75p.

Eco Animal Health (LON: EAH) says revenues will grow 8% in 2025-26 and EBITDA will be much better than expected. Latin America revenues recovered and North America did better than expected. Gross margins have improved. New product launches should help revenues to continue to grow. The share price increased 7.25% to 103.5p.

Stephen Lucas has increased his stake in bars and escape rooms operator XP Factory (LON: XPF) from 4.92% to 6.21%. The share price recovered 6.98% to 11.5p.

Africa-focused oil and gas company Afentra (LON: AET), along with Sonangol and Etablissements Maurel & Prom S.A., is jointly acquiring Etu Energias’ 10% stake in block 3/05 and 13.33% stake in block 3/05A in Angola. Afentra will buy 3.33% and 3.66% of these bocks respectively. This will cost $15.2m, plus contingent consideration of up to $6.74m. The effective date of the transaction will be the end of 2023. Afentra has also launched a strategic review following bid approaches. The share price rose 6.38% to 71.7p.

FALLERS

Shares in Galantas Gold (LON: GAL) slipped 17.8% to 30p following yesterday’s announcement that it had started the first drill programme at the Indiana gold project in Chile. There are 17 holes planned.

Catenai (LON: CTAI) investee company Alludium has secured its first paying customers since it launched its AI Agent operating system. The Catenai share price fell 11.8% to 0.335p.

Ex-dividends

Craneware (LON: CRW) is paying an interim dividend of 15p/share and the share price fell 55p to £13.75.

Hargreaves Services (LON: HSP) is paying an interim dividend of 19.5p/share and the share price declined 17p to 743p.

Nichols (LON: NICL) is paying a final dividend of 18.7p/share and the share price slid 31p to 933p.

NWF (NWF) is paying an interim dividend of 1p/share and the share price dipped 2.5p to 132.5p.

Tristel (LON: TSTL) is paying an interim dividend of 5.68p/share and the share price decreased 7.5p to 380p.

The FTSE 100 sank on Thursday as investors reacted to soaring oil prices after major oil and gas fields were struck in the Middle East, signalling a dangerous escalation in the conflict.

London’s leading index tumbled 1.9% as both sides targeted major oil and gas fields and increased fears of a substantial shock to global energy markets that could send waves through the global economy.

Susannah Streeter, Chief Investment Strategist, Wealth Club, said: “Fears of a sustained energy shock have resurfaced after the escalation in the Iran war sent oil and gas prices soaring.”

“The prospect of a longer, more drawn-out conflict is in sharp focus, as both sides ratchet up attacks on energy infrastructure. Downbeat sentiment is spreading fast, with London’s Footsie opening around 1% lower as investors assess the repercussions for the global economy.”

Concerns around an oil shock were compounded by the Federal Reserve’s interest rate meeting and press conference that offered little in the way of reassurance for investors worried about the trajectory of rates.

The Bank of England turned the screws on markets when it said it expected inflation to rise while keeping rates on hold on Thursday.

“The Fed and Bank of England are in a state of limbo while they wait to see if the Middle East crisis will trigger a long-lasting inflation shock,” said Dan Coatsworth, head of markets at AJ Bell.

“There simply isn’t enough data to make an informed decision on whether to put up rates to deal with the likely aftershock of the Middle East crisis – namely, a new inflation spike.”

The degree of uncertainty was reflected in the extent of losses for FTSE 100 companies on Thursday. At the time of writing, 97 of the FTSE 100’s 100 constituents were trading in the red.

Miners were among the most heavily hit with Fresnillo sinking 7.8% and Anglo American losing 7.3%.

NatWest shares were down 7%, but this also included the impact of the stock trading ex-dividend.

BP was the top riser, in part because of higher oil prices, but largely due to news it had offloaded a refinery in its push to streamline the business and reduce costs.

“BP’s decision to offload the Gelsenkirchen refinery in Germany is another positive step toward streamlining the business and reducing debt.,” explained Derren Nathan, head of equity research, Hargreaves Lansdown.

“The immediate impact on the debt pile hasn’t been revealed, but plans to reduce capacity at this outdated facility have been touted previously, and margin improvement has been hard to come by. The disposal removes a further $1bn of operating costs, while elevated commodity prices may have helped BP gain a better price.”

BP shares were 2.5% higher at the time of writing.

On Tuesday 26th August last year, I featured again the shares of Ashtead Technology (LON:AT.), then with its shares at 344p, it was capitalised at £276m.

The shares went on to score Lows of 297p last November and repeated in January this year, since when they have rebounded to 445p – showing that there is quite an active market range for the company’s equity.

On Tuesday of this week the group reported an impressive set of Final Results for the year to end-December 2025.

In reaction, the shares bounced up from 367p to 408p, easing to 393p on profit-taking

The Business

Now capitalised at £317m, ...

Strategic Minerals has raised £4.7 million through a direct share subscription to accelerate development of its Redmoor tungsten-tin-copper project in Cornwall.

The AIM-listed company issued 134.3 million new ordinary shares at 3.5 pence each, representing a 16.7% discount to the closing mid-market price on 18 March.

The company says the placing was conducted after a ‘prominent international investor’ approached it directly. This investor led the round.

The board described the investment as a strategically important moment.

Net proceeds will be directed towards Redmoor, which Strategic Minerals regards as its flagship UK asset. The placing comes as tungsten prices soar amid disruption to global trade due to the conflict in the Middle East.

“Having been approached by a prominent international investor, the Board decided to take the opportunity to fast-track the already accelerated development of the Redmoor Tungsten-Tin-Copper Project,” said Charles Manners, Executive Chair of Strategic Minerals.

“Underpinned by favourable pricing for all our minerals, this investment represents a clear endorsement of the Company’s high-quality asset base, and its objective to develop Redmoor and the surrounding area into a leading source of strategic and critical minerals here in the UK to provide resilience to western world supply chains.

“We are delighted to welcome the investor to our register and are grateful for their support and confidence in the Company.”

The company belives the project has the potential to supply around 30% of Europe’s tungsten demand.

IG Group has reported record full-year revenue of £1.12 billion, up 7 per cent, as the online trading platform continued to attract new customers at a pace.

Net trading revenue rose 10 per cent to just over £1 billion.

However, EBITDA margins dipped to 47.3 per cent from 49.9% a year earlier, with the group citing lower interest income as rates fell and increased spending on marketing, product development, and strategic initiatives aimed at longer-term growth.

EBITDA edged up 1% to £531 million, while adjusted earnings per share rose 5 per cent to 115.3p, helped by ongoing buybacks. A new £125 million share buyback programme was announced alongside the results.

The buyback may be one of the key drivers in IG’s 5% rally in early trading on Thursday.

Investors will also be interested to see that active clients surged 174% to 742,100, though the bulk of that jump came from the Freetrade acquisition.

On an organic basis, active customers grew 6 per cent. First trades leapt 81% to 128,800 on a reported basis, suggesting IG is pulling in new users well beyond the Freetrade book.

IG’s 742,100 active customers as of 31 December 2025 put it ahead of AJ Bell’s 644,000. For context, AJ Bell generated £317.8 million from this client base in the year to September 2025.

IG’s momentum has continued into 2026. Revenue for the three months to February came in at £274 million, up 2%, with active customers climbing to 753,000. Assets under administration on the platform reached £19.5 billion.

IG has also been busy on product, launching zero-commission mutual funds and SIPPs through Freetrade and rolling out a spot crypto offering in Australia following its January acquisition of the exchange Independent Reserve.

IG expects total revenue of around £300 million for the quarter to March, up roughly 7% year on year, driven by heightened volatility around the conflict in the Middle East.