Facebook revenue surpasses analysts’ expectations for the quarter

Facebook (NASDAQ:FB) on Wednesday revealed that it expects its revenue growth to slow “significantly” in H2 of 2021.

During the three months to 30 June the social media company’s revenue rose to $29bn (£21bn). The figure was up from $18.69bn compared to the same period a year before.

Th revenue figure surpassed analysts’ expectations of $27.9bn.

The tech giant reaped the rewards from lockdowns as its ads targeted people who were at home more often than usual.

However, as Facebook “laps” periods which previously saw high levels of growth, it expects to see a slowdown in its sales.

Facebook warned that revenue growth during Q3 and Q4 was likely to “decelerate significantly”. In after-hours trading on Wednesday the Facebook share price fell by 4%.

Year-to-date its share price has added 38.8%.

Facebook’s results come amid a string of strong performances from America’s tech giants, including Alphabet, Apple and Microsoft, over the past quarter.

Facebook now has 2.9bn monthly users and owns WhatsApp and Instagram.

Hargreaves Services (LON: HSP) has put out a string of trading statements since it was recommended during April. A strong performance from the German associate boosted profit in the year to May 2021, while the longer-term prospects for the core operations are good.

Last year was a tough one for Hargreaves Services, but it remained profitable and cash generative.

Hargreaves Services is no longer involved in coal or British Steel. That hit the contribution of the environmental, logistics and minerals business. The mechanical and electrical engineering and materials handling businesses increased ...

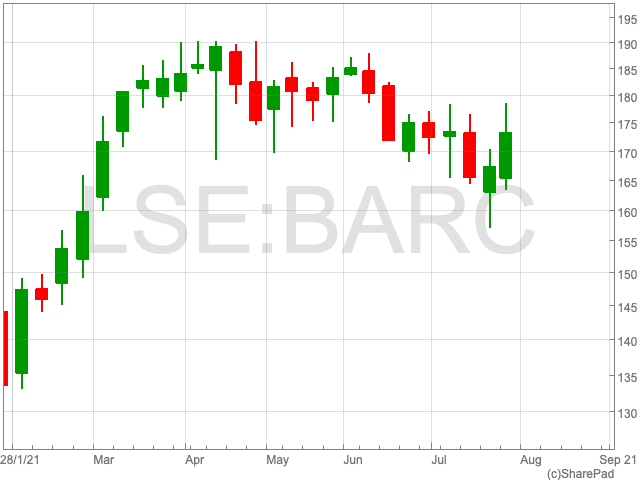

Barclays (LON:BARC) topped the FTSE100 on Wednesday after its quarterly numbers sounded the right notes with news on dividends, share buybacks and a greater than expected release of provisions set aside to cover any potential loan losses relating to Covid. During the afternoon the Barclays share price is up by 3.74%, bringing it into the green over the past month.

Following a hot start to 2021 for the bank, the Barclays share price plateaued from the middle of March onwards. However, with today’s news, investors will be hoping now is a turning point for the Barclays share price to regain momentum.

Dividend

Firstly, a key reason for today’s jump is Barclays confirming it will be resuming its dividend payout, in addition to announcing a £500m share buyback.

After the Bank of England gave the green light for payouts to resume back in July, Barclays confirmed its shareholders will receive an interim dividend of 2p per share.

The FTSE 100 bank will also buy back £500m of its own shares. This is on its expectation that impairments will remain below historical levels on the improved outlook of the UK economy.

Profits

Secondly, Barclays is able to commit to a shareholder payout as its profit levels far exceeded its own expectations.

Barclays’ profit before tax increased by 52% to £1.6bn, well ahead of estimates of £1.2bn. Its profits came about thanks largely to its investment banking arm, which thrived during the pandemic. First half feed rose by 27% to £1.7bn on merger and acquisitions and stock market flotations.

UK Outlook

The improving outlook of the UK economy helped the Barclays share price. As restrictions are mostly lifted, while cases are set to fall for the seventh consecutive day, the banking giant was able to release £1bn in bad debt provisions. It had initially set the money aside to cover pandemic-induced defaults.

However, the bank warned: “the outlook remains uncertain and subject to change depending on the evolution and persistence of the Covid-19 pandemic”.

While the results smashed expectations, which was reflected by the jump in the Barclays share price, investors may not yet be in the clear.

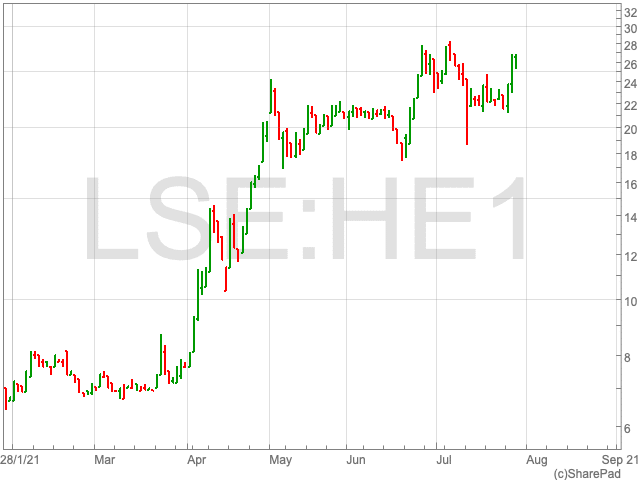

The Helium One share price (LON:HE1) is up by 18.04% over the pst five days as the helium exploration company revealed some positive news regarding drilling results. The Helium One share price has been on an outstanding run since the beginning of the year, adding 223.1% in the period. Following a mini-dip, which started at the end of June and finished at the end of July, investors will be hoping the Helium One share price can kick on. Chief Executive Officer David Minchin certainly has confidence in his company’s strategy.

Drilling Results

Earlier in July, Helium One identified helium gas in the Red Sandstone Group between 552m and 561m. However, there were delays in drilling due to parting of drill pipe in the midst of drilling the gas show.

Two things can be learned from this event which impacted the Helium One share price recently and will continue to do so. Firstly, there is a great deal of potential at the Tai-1 well. Secondly, however, while the company is in its early stages, things do not, and will not always, go smoothly. This will result in an element of volatility in the Helium One share price, which also has the potential for a longer-term upwards trajectory.

On this occasion, the drilling set the company back a few weeks, although it will not hope to make a habit of such delays, which could weigh down on Helium One’s overall development.

“The sidetrack has been a success, so we can now start to push to our target depth, and we’ll be, obviously, keeping the market informed as the drill hole progresses and we move on first exploration drill into our first discovery drill,” said Minchin.

Strategy

Helium One is a helium exploration company, with its main focus being on its flagship project in the Rukwa basin in Tanzania. The AIM-listed firm has so far acquired 4,500 square kms of sought after ‘helium prospective land’.

“We’ve got a 100 best estimates un-risked prospective helium resources of 138 billion cubic feet, we’ve measured the gas coming up to surface at 10.6% helium, which positions us well to be a potentially strategic player in provision of this important commodity into the next century,” David Minchin said.

Investors with an eye on the Helium One share price will be well served by understanding the future impact of helium on the world economy, in addition to Helium One’s ability to find and supply the commodity effectively.

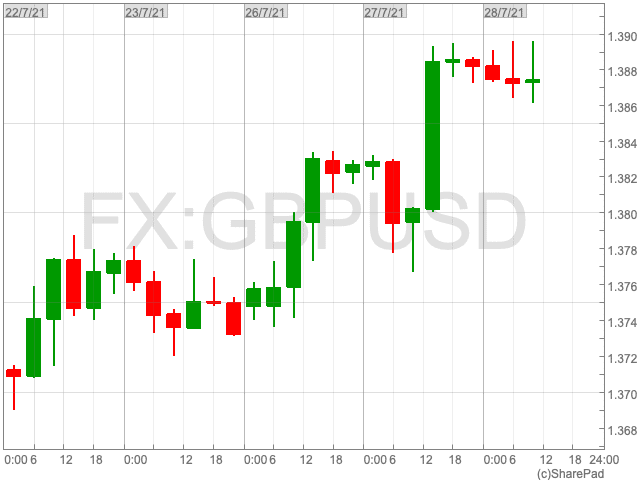

Just after lunchtime on Wednesday cable stands at $1.3869

The pound has sharply risen against the dollar over the past five days, with a big move coming yesterday afternoon.

Covid cases fell in the UK, allowing the pound to win back some gains, while orders for durable goods fell short of Wall Street’s expectations, giving the US economy a headache.

Positive economic data has been coming out of the UK, as well as the eurozone, which is giving investor’s a renewed appetite for risk.

Just after lunchtime in the UK on Wednesday cable stands at $1.3869,

In the UK, Covid cases are set to fall for the seventh day in a row, which is propping up the pound, although there are fears that cases could rise again in the near future.

The pound strengthening is a continuation of the trend that started in December when the UK and EU put pen to paper on a trade deal in the aftermath of Brexit.

Since the middle of March, the pound is up against the euro by 13.1%.

In terms of the dollar, the upcoming Fed meeting where the US central bank will discuss its monetary policy will influence sentiment around the greenback over the coming weeks.

Alan Green joins the UK Investor Magazine Podcast for our latest instalment of UK equities and global markets. We discuss Barclays (LON:BARC), Power Metal Resources (LON:POW) and Tertiary Minerals (LON:TYM)

We start with looking at US Tech stocks in Apple and Alphabet and go through the numbers from their bumper quarterly updates. Both produced revenue figures that surpassed analyst estimates in a strong quarter for two of the world’s largest technology companies.

Given the strong results from Apple and Alphabet, we explore whether we may be reaching the top of the earnings cycle as we come out of the pandemic and if a period of weaker growth could cause waves in equities.

Barclays (LON:BARC) also reported a huge jump in profits as they released half year profits that rose to £5bn helped by the reversal of COVID provisions and strong investment banking activity. Barclays also increased their dividend and we look forward to what investors could expect from Barclays and other UK banks in terms of payouts in the future.

We also explore Power Metal Resources (LON:POW) and Tertiary Minerals (LON:TYM).

Oakley Capital Investments(LON:OCI) confirmed its portfolio strength drove an 11% NAV uplift as the investment company released a trading update for the six months ending in June 2021.

NAV Growth

Oakley Capital Investments’ (OCI) unaudited NAV at the end of June was £804m, amounting to a NAV per share of 445p. The total NAV per share return, including dividends, is 11% since December 2020 and 26% since June 2020.

Performance

Oakley Funds sustained its solid performance levels and EBITDA growth, while the impact of Covid-19 continues to take a toll on its operations. Of its current portfolio, 14 companies equalling 52% of NAV grew their revenues at or above exceptions during the six month period. Four companies accounting for 14% of NAV saw a modest impact on financial performance due to Covid, while three companies which make up 29% of NAV, continue to be significantly impacted, the company said.

Investments

Over the past six months, OCI made a total look-through investment of £95m which, aside from some minor follow-on investments, was attributable to the acquisition of four new platform investments: idealista (Fund IV), Dexters (Fund IV), ICP Education (Fund IV) and ECOMMERCE ONE (Origin Fund).

Cash and Cash Commitments

Balance sheet – OCI has no leverage and had cash on the balance sheet of £172 million at 30 June 2021, comprising 21% of NAV

Recent commitments – OCI’s total commitment to the Oakley Capital Origin Fund, which closed in January 2021, was €129 (£111) million

Total outstanding commitments – outstanding Oakley Fund commitments are £438 million

OCI is a Specialist Fund Segment traded investment vehicle that aims to provide shareholders with consistent long-term capital growth in excess of the FTSE All-Share Index by providing liquid access to private equity returns through investment in the Oakley Funds.

Concern’s remain over ITV’s advertising revenue streams in the long-term

ITV (LON:ITV) confirmed it received its highest advertising revenues in its near 70-year history as the UK broadcaster emerged from the coronavirus pandemic.

ITV confirmed that its advertising revenue for June surged by 115% year-on-year, as its total revenue rose by 25% over the first six months of 2021 to £1.8bn.

Its broadcast revenues initially took a big hit when the pandemic happened as large companies were forced to reign in their levels of spending. There has been a reversal in this trend as the economy has opened back up as businesses are now competing for position.

“A bullish set of results from ITV shouldn’t come as a surprise. The reopening of the economy is a natural driver for companies to increase advertising and so ITV’s associated revenue has grown by a decent rate,” said Danni Hewson, financial analyst at AJ Bell.

The company’s blockbuster show Love Island is back on the nation’s screens, “which means another rush by advertisers to bag a slot in the commercial breaks,” said Danni Hewson, financial analyst at AJ Bell.

While there has been a shot-term spurt of growth, Hewson remains less convinced over the UK broadcaster’s outlook.

“This is fine now, but ITV’s position longer term remains uncertain. There is structural shift of advertising away from TV and towards online channels.”

“ITV may have done well in the past year thanks to people being at home during the pandemic and who, having exhausted everything on Netflix, found themselves watching traditional TV channels again.”

“However, there is a real risk that was a one-off event, and streaming programmes and films on-demand will rule once more. That places even more pressure on ITV to come up with must-watch shows. As such, it will have to plough significant amounts of money into the studios arm to enrichen its content,” said Hewson.

Just before 11am on Wednesday, the ITV share price is pretty much unchanged from yesterday’s close, sitting at 119.38p.

The FTSE 100 crept above 7,000 as UK markets opened on Wednesday, with strength among UK-facing banks offset by weakness in miners and pharma stocks.

“Barclays topped the FTSE risers after its quarterly numbers sounded the right notes with news on dividends, share buybacks and a greater than expected release of provisions set aside to cover any potential loan losses relating to Covid,” says Danni Hewson, financial analyst at AJ Bell.

“The second quarter earnings season is proving to be a mixed bag for markets, with investors looking past many impressive top line figures and digging deeper into the numbers to find anything they can to worry about.”

“It says a lot when a big-name stock like Apple doesn’t see a share price jump on better-than-expected quarterly earnings,” says Hewson said.

Microsoft also beat expectations, yet its shares barely moved in after-hours trading as good headline news on earnings was offset by concerns about a slowdown in the rate of growth for its Azure cloud computing operations.

“As always, investors will want to know the central bank’s latest view on the outlook for the US economy and whether it is time to tinker with policy support measures.”

The spread of the Delta virus variant in recent weeks and months could give the Fed reason to make no changes to its policy.

FTSE 100 Top Movers

St James’s Place (5.32%), Fresnillo (4.68%) and IAG (4.12%), each making strong gains, led the way on the FTSE 100 during the morning session on Wednesday.

HSBC (-1.79%), BHP (-1.58%) and Reckitt (-1.43%) are Wednesday’s three biggest losers heading into the second half of the week.

Santander’s revenue during Q2 rose by 6% to €11.3bn

Strong demand for used cars in the US and homes in the UK allowed the Spanish Banco Santander to secure a strong increase in its Q2 profits.

For the second quarter ending in June the banking giant reported a net profit of €2bn, compared to a loss of over €11bn year-on-year as it stomached write downs on the value of a number of its operations.

Santander’s revenue during Q2 rose by 6% to €11.3bn, while its expenses rose at a more gradual pace by 4%.

Out of all of Santander’s key markets, it generated the largest underlying profit from America during the first half of 2021, in addition to making a series of acquisitions in recent weeks. This comes as a surprise to many who expected Santander to gradually ease away from the US market as its competitors have done.

Santander’s car financing operation is one of the biggest in America, and soaring used car prices have pushed its profit levels in the region.

In addition to the US, Santander performed strongly in the UK, where it is one of the top mortgage providers. The bank benefited from Britain’s booming housing market, which performed above expectations during the pandemic on support from the UK government.

Nathan Bostock, chief executive officer, commented: “we have delivered another strong financial performance while continuing to support our customers, colleagues and communities through the challenges of the pandemic. The results are testament to the hard work of our teams and reflect the strategic decisions we have taken over recent years as well as the economic recovery.”

“We have delivered good growth in net interest income and strong mortgage lending. At the same time, we have continued to focus on enhancing our customer experience and improving efficiency,” Bostock added.