Barratt house building levels not yet at pre-pandemic levels

Barratt (LON:BDEV), the homebuilder, is expecting its profits to exceed expectations amid a booming housing market.

The housing sector has continued to reap the benefits from increased demand for housing and tax holidays.

The homebuilder built 17,243 homes during the year ended in June 2021. It is an increase of 5,000 homes compared to the year before.

For the year ended in June 2019, Barratt constructed 17,856 homes, which means the company is yet to surpass its pre-pandemic levels, despite the strong performance during the past year.

The FTSE 100 company is expecting to see its adjusted pre-tax profits come in slightly above analysts’ expectations which were between £860m-£899m.

David Thomas, chief executive of Barratt Homes, expressed his delight at the company’s results:

“It is thanks to the hard work, resilience and flexibility of our employees and sub-contractors that we made such excellent progress this year, whilst maintaining our high standards of quality and service.”

“We have seen continued strong demand for our high quality, energy efficient homes on well-designed developments, enabling us to deliver 17,243 home completions this year. Whilst these are still uncertain times, we enter the new financial year in a strong position and remain focussed on our medium term targets, including delivering 20,000 homes a year.”

The merger will bolster AstraZeneca’s offering of cancer medicines

AstraZeneca’s (LON:AZN) £28m bid for rival pharmaceutical company Alexion has been approved by the UK’s competition watchdog and is now expected to close in a week.

The merger will bolster AstraZeneca’s offering of cancer medicines, the company confirmed, and became subject to a review by the Competition and Markets Authority, as they were concerned about the impact of the deal on competition.

New shares issued to Alexion shareholders will begin trading in London, Stockholm and New York the day after the deal is completed.

Marc Dunoyer, Executive Director and Chief Financial Officer, said: “We are very pleased to have secured this critical final clearance from the UK Competition and Markets Authority for the acquisition of Alexion. We look forward to the imminent closing of the transaction so that we may pursue our shared ambition to bring more innovative medicines to patients worldwide and begin AstraZeneca’s next chapter of growth.”

Support came from shareholders of both companies who voted in favour of the deal as far back as May.

A reorganisation of the managerial structure is anticipated once the merger is completed.

The FTSE 100 pharmaceutical company confirmed its intention to provide an updated 2021 outlook for the combined company “in due course”.

We record the Podcast prior to the UK-Ukraine FinTech Summit taking place at the Ukrainian Embassy in London and available for everyone to tune into online:

Misha is the Co-founder of MonoBank, a Ukrainian banking app, whose success spurred him to subsequently co-found Koto, a banking app available to everyone in the UK.

MonoBank now has 4 million users in Ukraine and we discuss the environment that allowed Misha’s business to flourish including a strong pool of talent and the need to become profitable in a shorter time frame normally associated with similar companies such as Monzo here in the UK.

We also discuss the wider tech industry in Ukraine and how it has developed in recent years and how the relationship between the UK and Ukraine is set to grow in the coming years.

There have been 21 major bids for UK-quoted companies so far this year and eight of them have been AIM companies. May and June were particularly active, partly due to the bid for Morrisons. Peel Hunt believes the UK market offers lower valuations than some of the other major markets.

The bids and proposed bids are worth a total of £24.4bn. Only two of these bids have been completed (AFH Financial and RDI REIT), although most of the others are recommended. There are four possible bids that have not been finalised, including William Morrison Supermarkets (LON: MRW), Ultra Electronics (LON: ULE),...

There has been yet another profit upgrade following the latest trading statement by Hotel Chocolat (LON:HOTC). The chocolatier reported its initial trading figures for the full year and there was a 21% improvement on 2019-20 and 24% of the peak in 2018-19.

The share price increased by 11p to 385p, which is still nearly one pound below the level reached near to the end of 2020 and around three-quarters of the all-time high for the share price.

The latest ten weeks of trading up until 27 June produced growth of 63% when compared with last year’s poorest trading period during which all stores wer...

Economists had initially forecast that the rate of inflation would be 4.9%

The rate inflation rose again last month, going against the Federal Reserve‘s notion that recent high levels of inflation are ‘transitory’.

In June, the consumer price index increased by 5.4% year-on-year, the quickest rate since August 2008, and well above the 5% figure from.

Economists had initially forecast that the rate of inflation would be 4.9%.

It is still early to determine whether the recent uptick in US inflation is transitory or structural, according to Daniel Casali, Chief Investment Strategist at Tilney Smith & Williamson. However, core CPI inflation (ex-food and energy) has trended up to its highest level in 30 years and increases the risk that inflation could be structurally higher in future.

“Breaking down the data, just three categories (shelter, used car prices and transportation services) accounted for 76% of the annual increase in core CPI for June. The sharp price gains for used cars and transportation services (e.g. airfares) are driven by supply issues and should be resolved once output picks up after economic reopening,” said Casali.

“However, the shelter CPI component (including rents) accelerated to 2.6% year-on-year, its highest level for a year, from 2.2% in May. Accelerating shelter prices is more of a concern given that it accounts for 42% of core CPI inflation basket and it can move higher from here. That’s because landlords may view the opening-up of the economy as an opportunity to raise rental prices and could include a premium as insurance against potential future eviction moratoriums by the government in the event of rising Covid cases.”

For a while now, the Federal Reserve has described the price rises as ‘transitory’, sending the message that inflation will settle as lockdowns ease and supply balances out with pent-up levels of demand.

However, a number of investors are concerned that inflation could be here to stay well beyond the Fed’s expectations.

JPMorgan Chase (NYSE:JPM) released its Q2 financial results on Tuesday, setting a marker ahead of earnings week in the US.

The banking giant confirmed its profit during the second quarter more than doubled, while its revenue also beat expectations.

JP Morgan‘s net income increased to $11.95bn, up from $4.69bn compared to same period a year ago.

It is true that their results at this stage look strong in part thanks to being on the back of the economic crisis caused by the pandemic. However, Will Howlett, equity analyst at Quilter Cheviot, says the investment bank is in a fundamentally good position:

“The big US Investment banks including JPM hold top tier positions in seemingly almost everything, which gives them resilience in good times and in bad. JPM is a bellwether for other US banks, so today’s results should set the marker for similarly strong earnings from other large US banks throughout the week,” said Howlett.

Howlett also said loan growth is an area to focus on over the coming quarters, while average loans are flat year-on-year in the second quarter.

“Consumer credit demand is pretty poor at the moment, a reflection of the fact that consumers have built up their savings during the pandemic, helped by federal stimulus cheques, and have used these savings to pay down their credit cards and other borrowing. Likewise with interest rates so low, net interest income is at a low point in the cycle and this will be restricting bank profitability,” Howlett said.

From here, all eyes will be on the strength of the recovery in the States, and the knock-on impact on loan demand and consumer spending, “particularly with concerns that record levels of deal-making boosting the investment bank are unsustainable”, said Howlett.

“From a share price perspective, US banks tend to follow the yield on 10-year US Treasuries. As a consequence, US banks have been underperforming over recent months given the move in yields since the first quarter, but this is simply a relative weakness after a strong recovery from the lows of last year.”

Some parents took an an extra job or postponed their retirement to support their children

Parents give their children close to £3,000-per-year to help their grown-up children with the cost of living.

According to a study by Equity Release Supermarket of 1,000 parents, with children who had left home, 75% of them continued to give financial support for their children.

Many take on an extra job, begin working again, or even postpone their retirement in order to provide the necessary support.

Nearly 25% of parents assist their children’s studies, while 22% have a desire to get their children onto the housing ladder.

Parents specifically stepped in this year as the pandemic caused their children to struggle financially.

Mark Gregory, founder and CEO at Equity Release Supermarket, which commissioned the study, said: “Despite children growing up and moving out of the family home to live their own lives, many still have to rely on their parents or grandparents for financial support.”

“As a result, parents often sacrifice their own savings, equity, or later life plans in order to provide for their children, whether that be general lifestyle items, helping with a new house deposit, or indeed purchasing their first home.”

“In fact our study found that 42 per cent of parents admitted funding their children is a habit they would like to break in order to improve their own bank balance.

“However there are potential options available that would allow adults to support their children whilst also fulfilling their own financial wishes, which is where equity release could come into play as one potential solution.”

Other factors, including the European football championships and pent-up demand gave an additional boost to figures which were released today.

The British Retail Consortium, when carrying out its monthly update, said retail sales were 13.1% higher in June when compared to the same month in 2019, before the pandemic. Over the whole of Q2, retail sales increased by 10.4% compared to the second quarter of 2019.

Restrictions on foreign holidays also meant that money would be spent on retail purchases within the UK as an alternative for those seeking to enjoy themselves without travelling abroad.

Helen Dickinson, Chief Executive of the British Retail Consortium, said:

“The second quarter of 2021 saw exceptional growth as the gradual unlocking of the UK economy encouraged a release of pent-up demand built up over previous lockdowns. In June, while growth in food sales begun to slow, non-food sales were bolstered by growing consumer confidence and the continued unleashing of consumer demand.”

“With many people taking staycations, or cheaper UK-based holidays, many have found they have a little extra to spend at the shops, with strong growth in-store in June. Fashion and footwear did well while the sun was out in the first half of June, while the start of Euro 2020 provided a boost for TVs, snack food and beer,” she added.

Despite the positivity around the announcement, some challenges remain, as many businesses are attempting to make up for lost time. The lack of tourists arriving from abroad and people carrying on working from homes means that many cities are seeing fewer people walk by.

“Consumer comfort with the next stage of the roadmap will be key to the ongoing success of retail. Many customers are looking forward to a return to a more normal shopping experience, while others may be discouraged by the change in face covering rules. The government will need to reassure the public on safety, while pushing forward with its hugely successful vaccination programme,” Dickinson said.

English football fans are bitterly disappointed by the final result of Euro 2020, but reaching the final marked a turnaround in English football. The long-awaited catch-up trade in UK shares could be the next big turnaround.

——————————

First, let’s be clear – there is no clear link between a national football team winning or being runners up in the European Championship and the performance of that country’s shares… so do not invest on that basis. Not to mention, the FTSE 100 and FTSE 250 indices contain many companies with headquarters outside of England.

So even if you’re feeling proud of the boys in white… do not invest on that basis.

BUT it might just be that the turnaround in British investments coincides with the turnaround in English football.

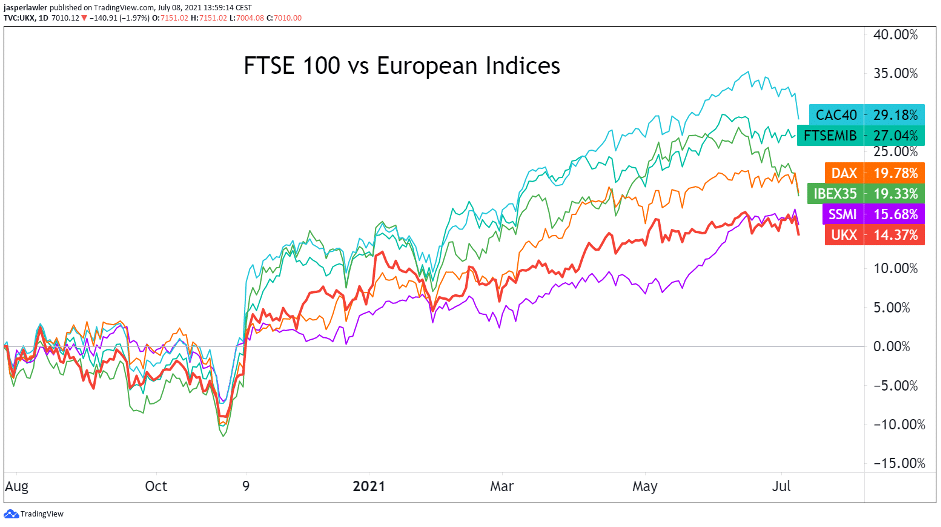

What’s been happening to the FTSE 100?

Likely nobody will be complaining about the performance of the UK stocks in their portfolio over the past 12 months. The FTSE 100 index (UKX) – an average of the share prices of top 100 British companies – is up 14% over the period. That is a very respectable annual return by historical standards. However, the other European major indices have fared better – most notably in France, where the CAC 40 index is up 29%, double that of its UK equivalent.

Chart constituents:

CAC 40 – France

FTSE MIB – Italy

DAX – Germany

IBEX 35 – Spain

SSMI – Switzerland

UKX – The United Kingdom

Indices trade ideas

It’s worth noting that these European indices are all available to trade as CFDs. If you believe the FTSE 100 is set do well, you can buy the UK 100 index CFDor if you wish to hedge your portfolio of UK stocks, you can sell the UK 100 CFD.

A third interesting trade idea is a ‘pair trade’ between indices. If you think UK stocks are due a period of outperformance over French stocks, you can simultaneously buy the UK 100 CFDand sell the France 40 CFD. Likewise, if you think the UK slump will continue, you can do the vice versa.

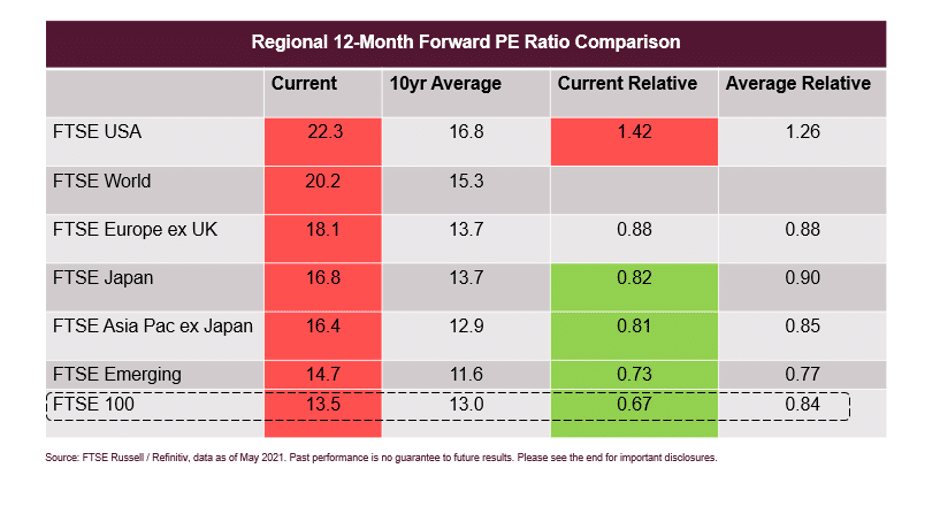

In a nutshell, UK stocks are dramatically undervalued versus their equivalents in Europe.

P/E’s are much lower in the UK – ie stock prices in the UK do not reflect company earnings as well as they do on the continent. And that’s saying something, because European shares are way undervalued versus the US.

Here’s the thing though – you don’t buy shares just because they are undervalued – because they are normally undervalued for a reason – and it often gets worse before it gets better.

So what could usher in the UK turnaround? Firstly….

Why the UK stock market underperformance?

We surely can’t blame it on a loss of national confidence because of football…

We attribute the underperformance to two things:

The industries represented in the index and their exposure to ‘value vs growth’ trades

Lingering Brexit uncertainty – especially as relates to financial services

FTSE 100 industry membership

The table below breaks down how many companies the FTSE 100 has from each industry group (sector).

Industry

Number of stocks

Basic Materials

10

Construction and Materials

1

Consumer Discretionary

19

Consumer Staples

10

Energy

2

Financials

20

Health Care

4

Industrials

19

Property

4

Technology

4

Telecommunications

2

Utilities

4

On the basis of the number of shares, the UK index is heavily geared towards consumer discretionary, financial, and industrial sectors.

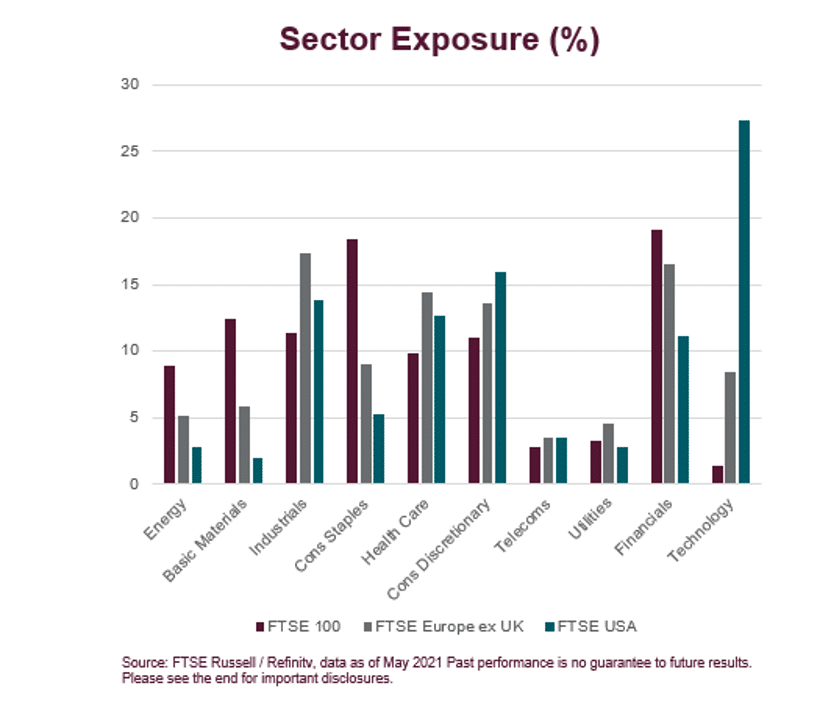

Sector exposure can also be looked at according to weighting on the index. The below chart contrasts the UK, Europe and the US. Here the standout sector is technology, where the US is in a different universe to the UK.

Technology represents ‘growth’ stocks – while sectors like banks and miners represent ‘cyclical or value’ stocks

Brexit

The UK has now formally left the European Union and there has not been in a resulting crash in the economy or the stock market- of course. But questions remain, especially because the Brexit deal did not cover financial services – Britain’s biggest contributor to GDP.

In February, Amsterdam saw more equity trading than London- though London has since taken back the crown, it is illustrative of the changes afoot.

Uncertainty for Britain’s financial sector clearly has direct implications for investing in the 20 companies on the FTSE 100 involved in finance – but it also indirectly impacts other sectors through the currency. With the British pound lingering around 1.40 to the US dollar (GBP/USD), and at risk of more geopolitical uncertainty, international investors will be less inclined to invest in UK assets.

How does the British catch-up happen?

Firstly, let’s establish what won’t do it. The FTSE 100 is not going to be composed of technology and growth stocks overnight. This will take some long-term structural shift in the economy to yield big companies in these fields. New centres of excellence in London, Manchester and around Oxford and Cambridge universities will hopefully deliver, but not in the near term.

So what can change?

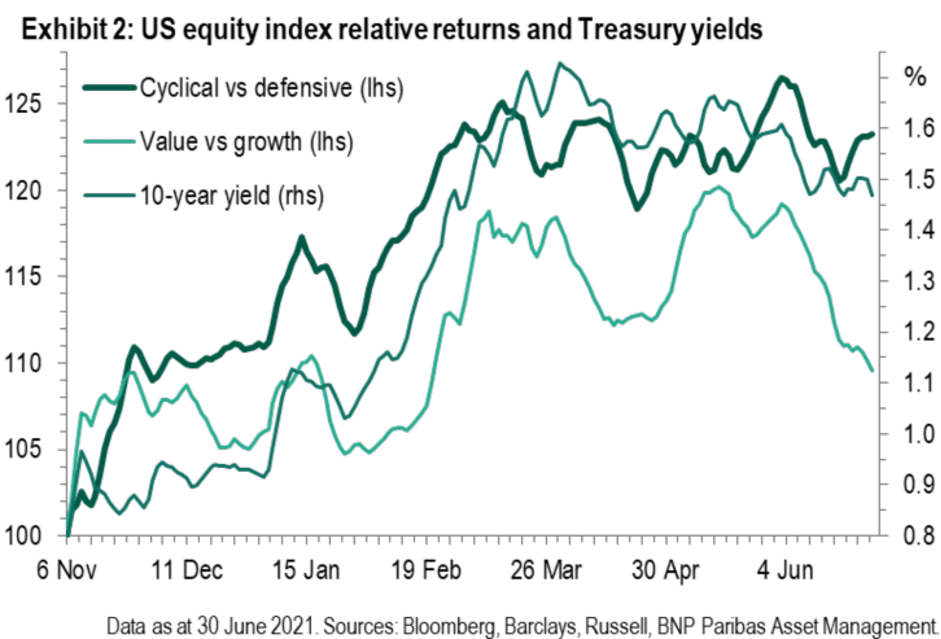

The Reflation trade

In the last two months, bond yields as well as the ‘value vs growth trade’ has gone flat (see chart below). In that same period, UK stock markets have also turned cold because UK stocks fall largely in the cyclical / value camp, as we already outlined.

The Federal Reserve calling inflation expectations ‘transitory’ caused a sharp reversal in bond yields, which encouraged investors to buy the dip in growth stocks.

But there is a rising belief that while inflation may cool off short term, higher inflation will be more durable.

“Every day I see evidence of inflation not being transitory, and I have concern that the Fed is falling behind,” – Mohammed El-Erian

“We’re seeing very substantial inflation… We’re raising prices, people are raising prices to us. And it’s being accepted.” – Warren Buffett

“With employment, the Fed wants to see outcomes, with inflation, they insist it’s transitory. It’s an intellectual incongruity that risks damaging their credibility if they’re wrong.” – Paul Tudor Jones

Value stocks have not sold off heavily- it is appears to be more of a pause, implying possibly more gains to come.

If economic data starts to corroborate what these top investors are warning about inflation, then that could prompt the bounce in bond yields and value trades that will support a return to form for the FTSE 100.

Financial services

The UK and EU agreeing a beneficial deal for the City of London is probably not something to hang your hat on, but still some return of certainty is likely – and that will support investor belief in the UK economy and improve valuations in some major components of the FTSE 100.

LCG offers CFDs in all the largest UK company shares as well as global indices. Register for a CFD trading account with LCG

Spread betting and CFD trading carry a high level of risk to your capital and can result in loss of your deposits. CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. Please note that 78% of our retail investor accounts lose money when trading CFDs. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing money.

The information provided within this communication has been prepared by London Capital Group Limited (LCG) and is intended for informative purposes only. It is not intended for investment, or commercial advice or an offer or solicitation for the purchase or sale of any financial instrument. Any opinions, news, research, analysis, prices, other information or links to third-party contained within this communication is provided as general market commentary and does not constitute investment advice and is not intended for any form of commercial use. LCG shall not accept liability for any loss, damager including, but without limitation, to any loss or profit which may arise directly or indirectly from use of or reliance on such information.

The information in this article is not directed at residents of EU as well as Australia, Belgium, Canada, New Zealand, Singapore or the United States, and is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

London Capital Group (LCG) is a company registered in England and Wales under registered number: 3218125. LCG is authorised and regulated by the Financial Conduct Authority (FCA) under the firm reference number of: 182110. The registered address for LCG is: 80 Cheapside, London EC2V 6EE.