DS Smith confirmed its H2 adjusted operating profit stood at £272m

DS Smith (LON:SMDS), the UK cardboard manufacturer, announced on Tuesday that it saw record H2 growth as it benefitted from a boom in online shopping during the pandemic.

The surge offset an initial downturn due to Covid-19 lockdowns, the company added.

Throughout 2020, the coronavirus pandemic hastened the growth of its e-commerce business, in addition to demand for more sustainable products.

DS Smith, supplier of cardboard to some of the world’s most prominent brands, including Amazon and Unilever, confirmed its H2 adjusted operating profit stood at £272m, up from £230m in H1.

“It is our highest growth rate ever achieved. We are pleased with that growth in the COVID era,” Chief Executive Officer Miles Roberts said.

DS Smith also confirmed its statutory profit dropped by 38% to £231m for the 12 months ending in April, down from £368m a year earlier as the pandemic affected its operating at the beginning of the year.

Full-year revenue is down to £5.976bn from £6,043bn a year before.

Ben Nuttall, industrials sector Senior Analyst at Third Bridge commented on DS Smith’s results announcement this morning:

“DS Smith has a number of major challenges. First, DS Smith operates primarily in secondary packaging markets, packaging that is used in supply chains, rather than primary packaging that the customer sees. E-commerce growth is growing rapidly but from a small base, and environmental concerns are taken into consideration in the supply chain but not nearly in the same way that end consumers are. Second, DS Smith is short paper, this means that they buy more paper to make boxes with than they sell, compared to Mondi which is long paper. For DS Smith they hoped that this would flatten peaks and troughs in sales, however, in times when the market for paper is tight, such as the current situation, the danger is not being able to secure enough paper to make boxes with for customers,” said Nuttall.

“Corrugated box volumes have started to accelerate with 8.2% growth in the second half of 2021, but DS Smith had a relatively lacklustre start to 2020, the year of online shopping, despite supplying cardboard boxes to Amazon and having a product that is very environmentally friendly compared to plastic. New box volume growth in H2 was promising and have been driven by FMCG customer gains.”

“DS Smiths revenue growth came in at negative 1%, roughly in line with expectations, but with adjusted operating profit down 24% around 6% under expectations. Over the year it shows the challenges of dealing with rising input costs during times of high volatility.”

Oakley Capital will combine PRIMAVERA with Ekon, one of its current portfolio companies

Oakley Capital Investments (LON:OCI), the listed trust that provides access to Oakley Capital’s private equity funds, has announced that Oakley Capital has reached an agreement to acquire PRIMAVERA Business Software Solutions, a Portuguese company.

Oakley will combines PRIMAVERA with Ekon, one of its current portfolio companies, a Spanish provider of Enterprise Resource Planning (ERP) software to create a new group by the name of Grupo Primavera.

Subject to regulatory approval, the group will be the largest independent provider of business software in Iberia.

Having been founded in 1993, PRIMAVERA offers ERP and cloud solutions to more than 32,000 SMEs across Portugal and Portuguese-speaking African countries.

“The newly established group will be the largest independent software platform serving SMEs in Iberia, with over 55,000 customers, c.€60 million of revenues and double-digit annual growth, driven by the rapid adoption of Software as a Service (“SaaS”) solutions. Grupo Primavera will be led by Santiago Solanas, an industry veteran with over 30 years’ experience in global roles in the software industry, including leadership positions at Cisco in France and Southern Europe, Sage Iberia, as well as in Microsoft and Oracle,” Oakley Capital said in a statement on Tuesday.

Grupo Primavera’s plan is to accelerate its deployment of cloud solutions organically through investment in product development and go-to-market initiatives, as well as through further acquisitions.

Peter Dubens, Managing Partner of Oakley Capital, commented on the deal:

“This is another example of Oakley’s ability to invest in founder-owned technology businesses and execute buy-and-build strategies. With the adoption of cloud technology in Iberia being behind the rest of Europe, we see significant value and further potential in growing the largest independent business software platform to service SMEs within the region.”

José Dionísio and Jorge Batista, CEOs and Co-Founders of PRIMAVERA, added:

“We are very excited about the new path that we are taking by creating an independent Iberian business software champion. This is a project with great potential, bringing together companies with a wide range of experience and leadership within the sector. We have been approached by many potential partners over the years, but it is with Oakley Capital and Santiago Solanas that we decided to take this step due to the exciting project they presented to us.”

Morrisons have rejected the offer from Clayton, Dublier and Rice

The Morrisons share price (LON:MRW) surged by 34% on Monday as an American private equity company put forward a £5.5bn bid for the supermarket.

The FTSE 250 company did not entertain the offer from Clayton, Dublier and Rice, although shareholders are expecting an improved offer in the near future.

The offer buoyed the FTSE 250 index, as the Morrisons share priced finished the day valued at 240.2p.

“After a year of feeding the nation Morrisons looks like it could be the subject of a feeding frenzy after turning down a takeover bid. Shares in the supermarket have ridden the roller coaster of anticipation today ending up 34.6% at 240.20, giving the FTSE 250 a much-needed boost,” said Danni Hewson, AJ Bell financial analyst.

“Morrisons’ rival stores seemed to be living vicariously with investors contemplating the future of the entire sector which increasingly seems to be undervalued with major changes to business practices possibly overlooked by some because of covid costs. Ocado and Sainsbury topped the day’s FTSE 100 risers,” Hewson added.

The NewYork-based company now has a period of four weeks to improve its offer.

Buyout firms have turned their attention to the UK’s supermarkets, which have seen their sales jump, although this has not been reflected in their respective stock values.

There has been some concerns regarding the takeover from the perspective of competitiveness. The Commons business, energy and industrial strategy committee will ask the Competition and Markets Authority to get assurances from Clayton, Dublier and Rice in the event of a deal taking place.

Morrisons owns 85% of close to 500 stores and has interests in farming and food production. Analysts argue that a number of factors, including its sizeable property portfolio, are not fully taken into account when considering the company’s share price.

According to The Times, research at Quest, suggests that Morrisons shares are worth 295p.

Nottinghamshire-based construction and infrastructure services provider NMCN (LON: NMCN) has secured a highly dilutive rescue fundraising after falling into financial difficulties The company continues to lose money and the terms reflect the dire financial position.

The share price had recovered ahead of the financing details, but once they were revealed it slumped 47.5p to 150p. Just over two years ago the share price was five times that level. The new shares are being issued at 20p each.

A £14m subscription is proposed, with a up to £5m more to come from an open offer. There is also a £10m c...

The once acquisitive SYSGroup (LSE:SYS) shares fell 3p to 43.5p and to a £21m Mkt Cap after reporting robust but unexciting final for the year to end March 2021. An 18% increase in Adjusted PBT to £2.1m was reported after a 7% fall in Revenue to £18.1m.

SYS manage IT Services and are a cloud hosting provider with 79% of its revenue recurring. The market for managed and cloud services is large, growing, and long term as it is driven by the structural move to cloud delivered solutions and IT outsourcing in general.

Covid has reiterated that almost all businesses will have no option o...

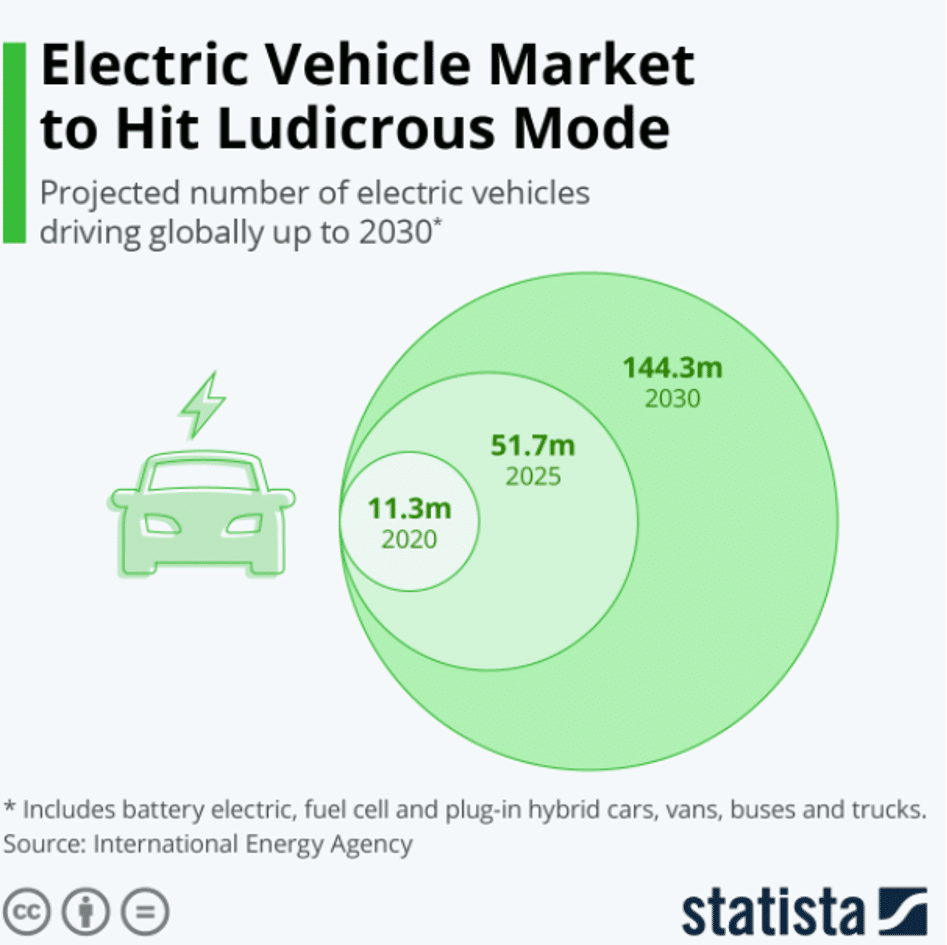

The projected number of electric vehicles on the road is of 51.7 million by 2025 and 144.3 million by 2030. The question is, who will manage to grab a decent portion of the market? What will become of Tesla? And what are real threats to the electric vehicle market?

Source: Statista, International Energy Agency

Short overview of electric cars:

Electric vehicles are automobiles that use energy stored in rechargeable batteries for movement as opposed to traditional gasoline. Electric vehicles can have a battery range of about 350 miles or 550 km. Most electric vehicles use lithium-ion batteries. The benefits of electric cars over combustion engines in addition to being emission free are that they are quieter, have lower recharge costs, faster acceleration and are safer if accidents occur as their lower center of gravity increases driving stability.

The main challenges yet to overcome are the comparatively high price of the vehicles, long recharge time and limited reach, fire concerns around the battery in accidents, and a so far limited variety of electric vehicles.

What Are the Environmental Reasons Against Electric Cars?

Environmental unfriendly battery production

Battery production for electric cars involves standard practices that aren’t environmentally stable. Electric vehicles are typically heavier and produce more road, brake, and tire dust. But the effects of this can be countered by regenerative braking. Electric vehicles often require rare-earth elements like neodymium, dysprosium, and others. They also use up lithium and cobalt. Like the factory production of other items, factory production of electric vehicles leads to the emission of some greenhouse gases and some air pollution.

Some studies have shown that the factory production of electric vehicles is often more severe on the environment than the factory production of conventional vehicles.

There have been issues about improper disposal or recycling of old batteries.

More than half of the cobalt used in electric vehicles comes from the Democratic Republic of Congo. Most of this cobalt is mined by the hands of children and adults. A lot of unpaid child labor is involved under hazardous conditions.

Minerals like lithium, cobalt, and manganese used in electric vehicles are now being mined from the sea. This is increasingly affecting biodiversity and causing harm to marine life.

Politically, though, there seems to only be one possible scenario for non combustion cars: They will be the only vehicle allowed in Western countries, with London for example expanding their ultra low emission zone this October, making it unaffordable to drive with older combustion style cars, and Britain pledging to be combustion free by 2035. The European Union is aiming to have 30 million electric cars on the road by 2030. This will cut CO2 emissions by 45%.

The rise in the share price of Tesla might have been the most talked about phenomenon in 2020 – yet there has been one sleeping giant that has been posed to take over.

Can hydrogen kill the electricity surge?

Hydrogen has been described as the future for the car industry and SPACS involving Hydrogen projects are in high demand.

The hydrogen fuel cell electric vehicle (FCEV), which simply runs on pressurised hydrogen from a fuelling station, produces zero carbon emissions from its exhaust.

Hydrogen vehicles are automobiles that use hydrogen fuel for power instead of petrol (gasoline) or diesel-like regular vehicles. Hydrogen vehicles convert the chemical energy of hydrogen to mechanical energy. They do this by either combining hydrogen with oxygen in a fuel cell or by burning hydrogen in an internal combustion engine.

The need to find applicable use cases for fuel cells and the possibility of obtaining cheap hydrogen from water are some of the factors driving research into hydrogen cars.

Toyota, BMW, and Daimler are investing about $10 billion into research on hydrogen vehicles and infrastructure. The USA and other countries are sponsoring research grants and investments into hydrogen cars.

Is hydrogen really a viable threat to electric cars?

The main perceived benefit is the zero carbon emission. However, the steam methane reformation method of producing hydrogen emits as much carbon per mile as regular gasoline cars. About 98% of commercially produced hydrogen uses the steam methane reformation process that emits harmful carbon dioxide.

Studies in 2009 and 2014 revealed that hydrogen cars would emit more carbon than petrol cars over the course of their lifetime.

Over 97% of hydrogen is produced by reforming steam methane or natural gas. This emits harmful carbon dioxide fumes that contribute to global warming and the depletion of the ozone layer.

Research is being conducted to produce hydrogen using renewable energy sources.

The remaining flaw, however, is that converting the energy to and from hydrogen batteries is inefficient. Adding up the conversion processes leads to only 38% of the original energy being used.

A report by BloombergNEF concluded:

Volkswagen ,meanwhile, made a statement comparing the energy efficiency of the technologies. “The conclusion is clear” said the company. “In the case of the passenger car, everything speaks in favour of the battery and practically nothing speaks in favour of hydrogen.”

Hydrogen vehicles will require new hydrogen filling stations, which cost $1-2 millionto establish.

There are currently only 48 public hydrogen filling stations in the US, with most of them located in California. In contrast, the number of available electric charging stations and charging outlets is over 40,000 and 99,000 respectively.

There are additional costs for transporting the hydrogen if the hydrogen is not produced onsite.

Hydrogen has high combustion energy with low ignition energy. Also, hydrogen tends to leak easily from tanks. You can’t store hydrogen at home to fill up your car due to the stringent requirements and the high combustion energy of hydrogen. There are strict codes and technical standards that must be observed in the production and storage of hydrogen. This makes it a tough industry to enter. Hydrogen fuel cells require expensive and rare catalysts like platinum to work.

Which Companies/Organizations/Governments Are Investing in Electric Cars?

In 2020, General Motors announced that it would spend more on the development of electric cars than it spends on diesel and petrol vehicles. The company aims to have 40% of its new cars in the United States as electric vehicles by 2025.

Audi plans to offer only electric vehicles by 2035. Apple is also reportedly working on an electric vehicle.

What are the opportunities that can outpace Tesla this year?

Tesla’s combined market cap is larger than that of the biggest automakers combined, and while its technology and innovation is superior right now, there are viable options to consider that could outperform Tesla this year.

Hedge funds are also betting on Nio, the Chinese electric vehicle maker.

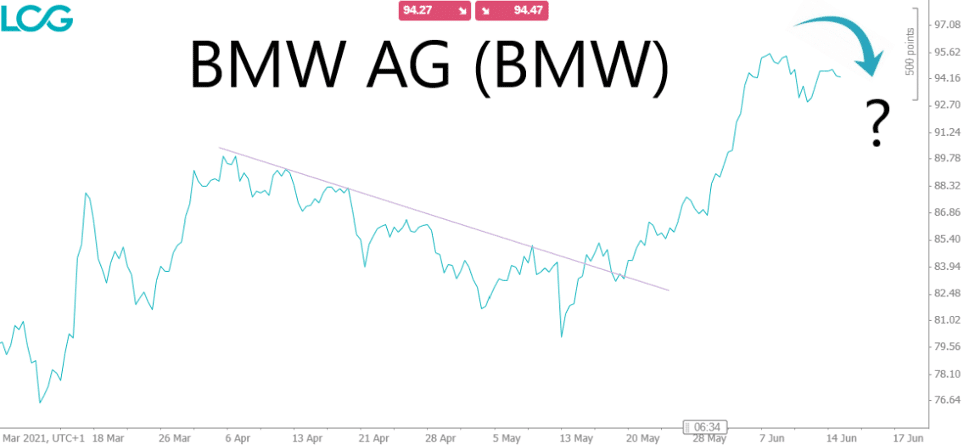

The narrative around electric vehicles is clear, questions is, how can we increase our chances of picking the right horse? Technical analysis shows us the following:

Past performance is not an indication of future performance

A rotation to traditional car makers has occurred over the past months, yet the rally has slowed and as we can see for German carmaker BMW, the price has dropped below the early June high. Can this be an opportunity for other pure electric vehicle makers to swoop up market share?

Past performance is not an indication of future performance

In the six month NIO Inc chart you can see a clear bullish trend emerging as of May and June, possibly breaking the down trend that’s been in place throughout 2021. Closing over 46.9 could mean a progression to 54.3, and failing to meet this level could lead to a correction towards the exponential moving average around 45.21.

Open an LCG Trading account and get access to charting tools, and stay up to date with analysis, including LCG’s guide to the industries around electric vehicles that have even greater potential than EV shares themselves.

Spread betting and CFD trading carry a high level of risk to your capital and can result in loss of your deposits. CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. Please note that 78% of our retail investor accounts lose money when trading CFDs. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing money.

The information provided within this communication has been prepared by London Capital Group Limited (LCG) and is intended for informative purposes only. It is not intended for investment, or commercial advice or an offer or solicitation for the purchase or sale of any financial instrument. Any opinions, news, research, analysis, prices, other information or links to third-party contained within this communication is provided as general market commentary and does not constitute investment advice and is not intended for any form of commercial use. LCG shall not accept liability for any loss, damager including, but without limitation, to any loss or profit which may arise directly or indirectly from use of or reliance on such information.

The information in this article is not directed at residents of EU as well as Australia, Belgium, Canada, New Zealand, Singapore or the United States, and is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

London Capital Group (LCG) is a company registered in England and Wales under registered number: 3218125. LCG is authorised and regulated by the Financial Conduct Authority (FCA) under the firm reference number of: 182110. The registered address for LCG is: 80 Cheapside, London EC2V 6EE.

The FTSE 100 ground out modest gains early on Monday as it rebounded from a sell off late last week.

The gains in London were in stark contrast to a tumultuous Asian session which saw interest rate fears rock equities.

“Asian markets slumped heavily as investors continued to react to last week’s US Federal Reserve meeting which has curdled sentiment by raising the prospect of earlier than expected rate rises,” said AJ Bell investment director Russ Mould.

“Having scaled the highest peaks in recent months, Japan’s Nikkei index notched up a chunky fall of more than 3% on Monday.”

“The FTSE 100 notched up a far more modest fall, having already endured a fair bit of damage at the end of last week linked to concerns about rate rises.”

Miners were among the losers on Monday as Asian concerns seeped into commodity prices.

“Any attempt at a rally in stock markets is going to struggle given the lack of news, and for the FTSE 100 some dollar weakness would be good to lift mining stocks from their current poor run,” said Chris Beauchamp, Chief Market Analyst at IG.

Rio Tinto was around 1% weaker and BHP barely in the green, up 0.2% at midday in London.

Morrisons Takeover

Morrisons shares jumped 30% in early trade on Monday following a £5.5bn takeover offer from a US private equity group.

Commenting on Morrison’s price action in Monday, AJ Bell investment director Russ Mould noted the Morrison’s share price was higher than the offer price, suggesting the market was preparing for a battle over Morrisons.

“The shares traded at 235p early on Monday which is higher than that 230p proposal from CD&R. The market therefore seems confident that the suitor will have to raise its offer price or someone else might step into the game and we’ll see a bidding war.”

“Amazon has long been touted as a potential buyer for Morrisons to help give it a much stronger foothold in the UK grocery markets so that’s an obvious name to watch.”

Wednesday’s AGM will see the launch of the new strategic plan for funerals and crematoria operator Dignity (LON: DTY). Management needs to indicate how it is going to tackle the debt pile and how the business is going to move ahead.

The current share price is 620p, which is more than double the level it was 12 months ago, but still much less than one-quarter of the peak. The board was overhauled earlier this year.

The higher level of deaths due to Covid-19 has provided a boost to business, but volumes will decline. There are also regulatory changes hanging over the business.

Net debt was £480....

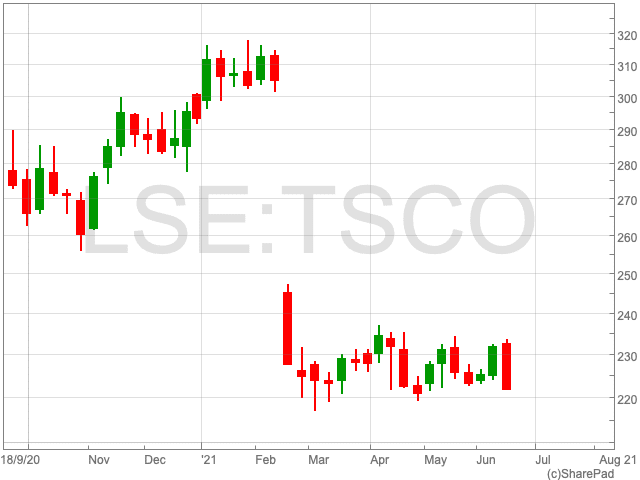

The Tesco share price (LON:TSCO) is down by 3.75% on Friday as the FTSE 100 company released its Q1 trading statement. Following a large drop in the stock’s value in February, due to the price effects of the £5bn special dividend, it has broadly traded sideways in 2021, rangebound between 220p and 240p per share. Since the beginning of the year the Tesco share price is down by 25.85% to 222.45p at the time of writing. This article will take a closer look at the company’s recent performance to give an insight into the supermarket’s broader outlook.

Trading Update

Tesco saw its underlying UK sales growth slow during Q1, in contrast to the same period a year ago when many rushed to the supermarket to bolster their supplies for the first lockdown.

For the quarter ending in May, the company’s sales rose by 0.5%, above analysts’ predictions of a drop of 1%. However, it was way down from a growth rate of 8.8% in the quarter before. Fuel sales rose by 68.1% in a signal of a recovery as the vaccine roll-out continues apace in the UK.

The Tesco share price received a boost as the firm retained its profit guidance for the 2021/22 fiscal year.

“Tesco’s first quarter 2021 figures were never going to live up to last year’s comparable period, as the three months to May included the period where the nation went crazy stockpiling food and drink as the pandemic took its grip. The supermarket saw 7.9% like-for-sales growth in Q1 2020, setting the bar very high this time around,” said Russ Mould, investment director at AJ Bell.

That might explain why Tesco is trying to push two-year figures in its latest update, to emphasis the unusual nature of last year’s performance and to convince the market that its business hasn’t ground to a halt.

“To its credit, 1% like-for-like growth on a one-year basis is not a disaster. It implies that Tesco is holding its own against tough competition in the grocery space and no doubt retained lots of the customers it won in 2020 from having wider availability of online delivery slots than its peers,” Mould said.

The issue of inflation remains a concern that Tesco may have to face up to. It may have to decide if it can pass on all the extra costs to customers or risk a squeeze on profit margins.

“The forthcoming launch of Russian discount supermarket Mere in the UK will add to the competition, so Tesco needs to be very careful that any changes to its prices don’t alienate its customers,” Mould said.

While Tesco is not the most exciting company in the world, it provides and essential service, and shows an appetite to innovate. That, in addition to its 4.3% annual dividend yield, means the Tesco share price could be considered a good bet for the near future.

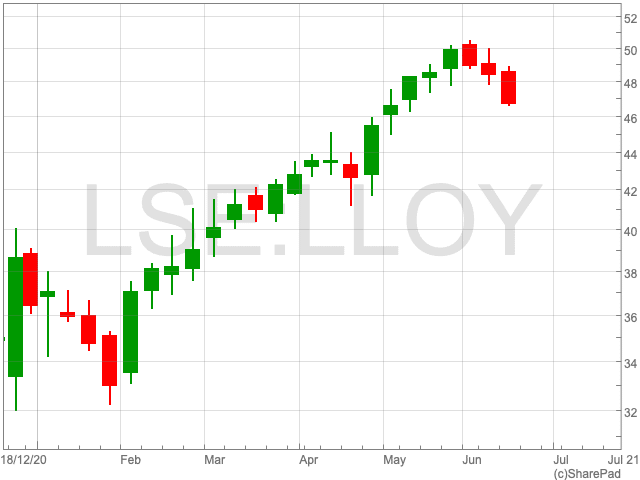

Despite being down by 3.84% over the past week, the Lloyds share price has been on an impressive run in 2021. Since the turn of the year it is up by over 34% at the time of writing. Despite a bumbling January amid the third UK lockdown, the Lloyds share price has seen a steady progression from there onwards. For the past month Lloyds has been trading between 46p and 50p, and investors are curious about where it will go next.

However, there are a number of factors at play which could influence the direction of the FTSE 100 bank in the near-term. In particular is the matter of when the UK fully reopens and the continued question marks over major central banks’ monetary policies.

UK Recovery

The UK economy appears to be well poised for a recovery. Britain most prominent business lobby on Friday increased its forecast for economic growth this year. The CBI has confirmed that it believes that UK GDP will rise by 8.2% in 2021, this is 1.8% higher than its previous estimate.

This bodes well for the Lloyds share price as its outlook is of course aligned with the overall performance of the UK economy.

Interest Rates

One concern for the Lloyds share price could be the prospect of continued low interest rates. Low interest rates mean that banks find it harder to generate profits on the money they are lending.

It is possible that the Bank of England could raise its interest rates sooner than thought as inflation surged past the central bank’s target for the first time in nearly two years. Furthermore, the US Federal Reserve suggested it may begin increasing interest rates earlier than anticipated.

However, Paul Dales at Capital Economics suggested that interest rates would not go above their 0.1% low until 2024: “There is a greater level of uncertainty about prices at present, with a possibility that inflation will turn out to be higher if staff shortages persist, triggering stronger wage rises, while cost increases continue to be passed on to consumers. However, with price pressures expected to ease next year and inflation to stabilise around 2%, it is likely that the Bank of England will hold fire and not raise interest rates before 2023.”

Price Target

Analysts at both Barclays and JP Morgan raised their price targets for the Lloyds share price earlier this month. Barclays upgraded its price target to 60p, an increase of 5p, while JP Morgan lifted it from 54p to 59p.