Card Factory (LON: CARD) has swung into a loss for the six months to July 31 as sales fell 48.6% to £100.5m.

Despite the loss, which was compared to a £22.2m in the same period a year earlier, the group has said second-half sales are looking positive.

Card Factory will not be providing a forecast for the rest of the year amid the uncertainty of new lockdown fears.

The group saw strong online sales over the holidays Valentine’s Day, Mother’s Day, and Father’s Day.

Paul Moody, Executive Chairman, commented:

“I am extremely proud of all colleagues working across every part of our business for the significant contribution they have made throughout this period of unprecedented disruption. In particular, for their unrelenting focus in driving the very successful phased store-reopening programme. The combination of our unique customer insight, vertically integrated business model and market leading position continues to ensure that we are well positioned to meet the increased online demand, supply our commercial partners and to present the optimum ranges in our stores.”

“We are pleased with both the trading performance as our stores have reopened and the positive feedback from customers who are visiting less frequently, but spending more. Recognising the uncertainty of the impact of further Covid-19 measures and changes in consumer behaviour in the short term, we are focused on a flawless execution of Christmas and the implementation of our refreshed strategy.”

Card Factory shares (LON: CARD) are trading +0.54% at 37,15 (0938GMT).

Greggs (LON: GRG) survived August, which it called a “difficult” trading month thanks to warmer weather and missing out on the government’s Eat Out to Help Out scheme.

In the 12 weeks to 26 September, the bakery chain averaged 71.2% of sales compared to the same period a year previously.

The group, however, intends to open new stores this year, which will be located away from city centres.

Reassuring investors, Greggs said: “Our immediate priority is to complete the consultation with colleagues on the proposed changes to resource levels.

“We will do this with regard to our values and the best long-term interests of the business as a whole. We will update on the expected financial impact of these changes when the consultation ends in November.”

Greggs struggled amid the pandemic and stores closed as crowds were difficult to keep socially distanced. Compared to a £40m profit in 2019, the group recorded a £60m first-half loss.

The group has reviewed the business and will be carrying out job losses and reducing working hours for many employees.

In this current financial year, Greggs has closed 11 shops to give a total of 2,039.

Shares in Greggs (LON: GRG) are trading -3.28% at 1.179,00 (0911GMT).

Cancer diagnostics developer ANGLE (LON: AGL) is getting nearer to FDA approval for its Parsortix liquid biopsy test. Angle would be the first company to receive FDA Class II clearance for a device harvesting intact circulating tumour cells CTC), making the technology highly valuable.

The specific approval would cover breast cancer. Clearance would allow Parsortix to be used in drug trials as well as the continued monitoring of patients who have been successfully treated.

Parsortix can capture circulating tumour cells, which can then be analysed.

FDA approval

It always seems to take longer tha...

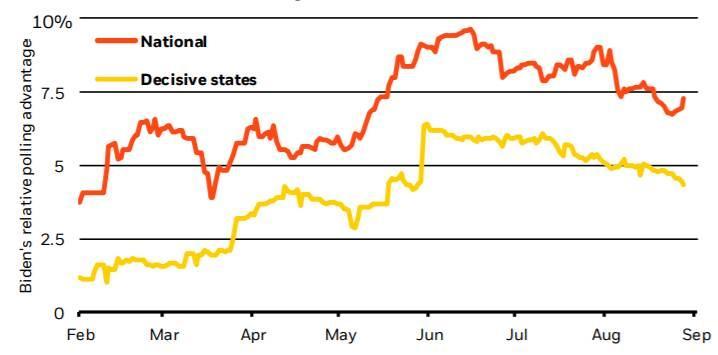

US investment management blue chip, BlackRock (NYSE:BLK) posted commentary on Monday afternoon, which stated that Democratic candidate, Joe Biden, currently appears to have an edge in the race to become president.

In what the company described as a highly ‘consequential election’, Biden looks to be leading Trump by seven percentage points in the recent national polling data. This lead, as ‘stable’ as it has appeared, is set against a tumultuous backdrop of economic uncertainty and public safety concerns – and therefore anything can still happen.

BlackRock Investment Institute, with data from FiveThirtyEight.

Indeed, and likely what many predicted, his lead has narrowed in key electoral states. This could well give Trump a path to re-election, with the incumbent president timing his poor handling of the virus well, with enough time for the debate focus to be shifted onto social issues and national security.

Among BlackRock’s three plausible scenarios for the election, they predict: 1) a Democratic sweep of the White House and Congress (with Democrats winning control of the Senate); 2) a Biden win with a divided Congress; and 3) a status quo Trump win. What is interesting, though, is that they also note the challenge that record-high mail-in voting will pose to vote counting, with potential delays and legal challenges on the cards.

Blackrock identifies three policy areas to watch

As far as policy differentiations are concerned, we might see Trump and Biden as diametrically opposed, but BlackRock notes three particular divergences to take note of.

First, and crucially: fiscal policy. The company says that under a Democrat clean sweep, the likelihood would be a new round of fiscal stimulus to spend on clean energy, transport and housing, as well as tax increases for companies and the wealthy. A Biden win with a Republican Senate would see less ambitious fiscal stimulus and infrastructure spending, alongside fewer tax changes.

BlackRock’s commentary adds that: “The net difference in fiscal spending between the two scenarios could be several percentage points of GDP over each of the next few years, we estimate. Fiscal spending under a second Trump term would be somewhere in the middle between those two scenarios.”

On the second policy issue, geopolitics, BlackRock states that under either scenario, a Biden win would likely mark a return back to ‘predictable’ trade and foreign policy, which would support emerging market assets and broader risk sentiment in the short-term. The company also believe that a Biden victory would not greatly impact US-China relations, as there is now bi-partisan support for a competitive stance on China in regard to tech, trade and investment. However, one big change would involve the US spear-heading the green stimulus effort.

BlackRock states that: “The U.S. would likely immediately rejoin the Paris Agreement and increase its emissions reduction goals. Its fiscal plans could help supercharge a globally coordinated green stimulus effort, adding to recent efforts by the European Union. A Trump win, by contrast, would likely lead to a doubling-down of the “America First” stance on trade and immigration.”

Finally, the company disregards the ‘tax-centric’ election logic, which states that a Democratic clean sweep would be seen as a market negative. Instead, in such an instance, BlackRock believes that investors would have to deal with higher taxes and tighter regulation, but that this would be balanced out by predictable foreign policy and greater fiscal support. The main implications, they say, will be in fixed income and leadership in equity markets, with long-term rates being pushed high and leading to a ‘modest steepening’ of the Treasury yield curve.

Also, while additional tax and regulations might pressure high cap companies, domestically-oriented small cap firms might benefit the most. Blackrock finishes by saying that:

“This scenario would add to reasons to prepare for a higher inflation regime and reinforces our strategic underweight of developed market nominal government bonds. The tectonic shift to sustainable investing will likely persist regardless of the result, but could be supercharged under a Democratic sweep scenario.”

With the Governor of the Bank of England, Andrew Bailey, making it clear that negative interest rates could be a real possibility, it is time for investors, savers and entrepreneurs to start factoring in what these controversial measures could mean.

Bank of England will have little interest in savers

Aside from being the mainstay of financial prudence, saving will be at the bottom of the agenda for the UK’s central bank. Instead, as is the way with most economic recoveries, the preferred route is to encourage people to spend the economy out of a slump.

And, while this may sound like a cheerier alternative to the fiscal retrenchment focus the UK took following the 2008 crash, it certainly isn’t something to celebrate as a saver. In the process of trying to increase liquidity, banks will be told to encourage their customers to go out and use their money, rather than save it. As stated by IW Capital CEO, Luke Davis:

“A policy maker at the Bank of England has defended the potential use of negative interest rates, calling results from other countries ‘encouraging’. The move could effectively mean that savers pay to have their money with banks and are incentivised to borrow money and increase their spending.”

And it isn’t just your average saver’s account that will see consumers lose rather than gain money. Indeed, other vehicles which typically offer income for putting your money aside, such as bonds, will likely see participants lose, rather than gain money.

“Many government bonds and investments are already offering investors what are effectively negative returns on their capital once inflation and other factors have been taken into account.” says Mr Davis.

Andrew Bailey’s words in favour of negative interest rates, having previously been opposed to them, has seen ‘record numbers’ of investors turn towards equities and alternative assets such as gold.

Negative interest rates positive for new beginnings

While certainly true that negative interest rates are harmful for all those currently trying to save for a house, holiday or other costly venture, they are good news for anyone willing to roll the dice and borrow money to get a new project started.

Mr Davis believes that part of the paradigm shift that could be witnesses, will be the move in focus from what were previously thought of as ‘safe’ assets, to illiquid assets.

The main thing to note, however, is that negative rates mean that it is the opportune moment to borrow money. One way people could capitalise on this is to take advantage of both the stamp duty holiday and negative rates simultaneously (assuming such a situation comes to pass). On the other hand, banks are being increasingly stingy with mortgage application approvals – in some cases requiring a 20% deposit for properties where they would traditionally only ask for half that level of commitment.

Another way to take advantage of cheap borrowing would be to either expand or start up a business. This, Mr Davis states, is the perfect time for start-ups and SMEs to continue adapting, and take advantage of the opportunities offered by an economic rebound:

“There are a huge number of SMEs that have adapted quickly to the pandemic and the changes it has ushered in. Many are now primed to grow, create jobs and increase value for investors. There is huge volatility in markets at moment which is putting some investors off – but thinking long-term can offer a refreshing change of perspective.”

In what has been a bright start to the week for the FTSE 100 index, among the frontrunners of the top risers crib sheet were property developer stocks, who have likely enjoyed a period in which house buyers and retail consumers released pent-up demand.

There were also gains in financials with HSBC rising 9% after a Chinese insurer increased their stake in the bank. Lloyds and Natwest Group both finished the day over 7% stronger.

Land Securities soars

Leading the charge on Monday was the UK’s largest commercial property development and investment company, Land Securities (LON:LAND), who saw their shares rally over 8.30%.

This rally came despite the company reporting consecutive loss-making periods, as well as following the lead of many others, and cancelling its dividend to conserve cash during the ongoing pandemic.

At present, the company’s shares are up 7.85% or 38.50p, to 528.90p a share 28/09/20 12:30 GMT. The current price is 38% below where it was a year ago today.

Analysts currently maintain a ‘Hold’ stance on Land Securities stock, as well as a 12-month consensus target price of 732.14p a share. It was also given a 54.31% ‘Underperform’ rating by Marketbeat‘s community and has a p/e ratio of 8.77.

British Land Company booms

Following close behind, fellow commercial property developer, British Land Company (LON:BLND), posted a 7% bounce on Monday morning.

This, much like Land Securities, followed underwhelming trading updates, and what was likely a difficult time for retail-focused commercial property landlords.

The company’s shares are currently up by 6.68% or 21.50p, to 343.50p apiece 28/09/20 12:30 GMT. This price is short of where it was on the same day last year by about 41%.

Again, much like Land Securities, analysts maintain a ‘Hold’ stance on British Land, with an equal number of ‘Buy’ and ‘Sell’ ratings falling either side. It was also given a 12-month consensus target price of 471.62p, a 51.57% ‘Underperform’ rating by Marketbeat’s community, and a p/e ratio of 9.85.

The outlook for property developers

Despite recent trading being more promising, the Times and FT have both run stories suggesting that recent price optimism will likely subside in the coming months, with the CEBR predicting that property prices could fall by as much as 14% in 2021.

As far as commercial property developers are concerned, the looming potential of a second lockdown can only be bad news, with many tenants waiting for the government to grant rent holidays or deferrals. The increased shift to digitalisation will also be tricky to manoeuvre, with high street bigwigs such as Theo Paphitis calling for business rate relief to continue indefinitely.

Aldi has revealed plans to create 4,000 jobs and open 100 new stores in the UK.

Thanks to surging sales amid the Coronavirus pandemic, the discount-grocery chain has already created 3,000 new permanent roles in the UK.

Aldi is launching a £1.3bn investment drive in the UK, where it is currently the fifth-largest grocer.

“With the UK’s economic outlook increasingly uncertain, families are more concerned about their grocery bills than ever,” said Giles Hurley, the chief executive for Aldi UK and Ireland.

“We’ve seen before that our customers need us most in times of financial hardship, which is why our commitment to remain Britain’s lowest-priced supermarket is more important than ever.”

Over this year, the supermarket chain will have created 8,000 new jobs. On this announcement, the supermarket reported a 8.3% rise in sales to £12.3bn.

Aldi launched a click and collect service last week.

“The business performance has been very, very solid… but we also recognise customer habits are changing and that we need to evolve our business to meet the new demands and we’re actively doing that,” said Hurley.

“We have a unique model, a set of efficiency principles unrivalled in the market, and that it is my firm belief that we can apply those principles to picking and packing stock in a very efficient way for customers… I’m very excited about it,” he added.

Reach shares (LON: RCH) shot up 20% on Monday as the publishing group announced plans to suspended its interim dividend.

The publisher of the Mirror and the Express had revenue fall 17.5% £290.8m in the six months to 28 June, compared to the £352.6m profit in the same period a year earlier.

Operating profit also fell from £71.3m to £54.9m.

Reach has suspended its interim dividend “due to Covid-19 uncertainty”.

“We have seen a strong recovery in the digital advertising market since the worst impacts of COVID-19 in April which has driven a return to healthy digital revenue growth since July, assisted by increased customer engagement and loyalty,” Jim Mullen, the group’s chief executive.

“Following the implementation of the major parts of the transformation programme, Reach now has a strong foundation to drive the next phase of the customer value strategy with increased efficiency and agility in our advertising and editorial operations,” he added.

Shares in Reach (LON: RCH) are trading +20.93% at 78,00 (0845GMT).

Hugh Osmond, who reversed Pizza Express into a listed shell three decades ago, has floated his latest restaurant group on AIM. On the first day of trading the Various Eateries (LON: VARE) share price fell from the placing level of 73p to 69.5p. The flotation was confirmed just before the latest tightening of lockdown restrictions in the UK and that might have affected early dealings.

Osmond believes that this is a time when acquisition opportunities, either sites or groups of restaurants, are likely to come about and Various Eateries will have the cash to take advantage.

Various Eateries raise...

Online fashion retailer boohoo (LON: BOO) has published the independent report on its suppliers in Leicester and the share price recovered 50p to 374.5p, compared with a year high of 433.5p and well above the level when criticism started. Management has accepted the findings and recommendation of the report.

The 234 page report is critical of boohoo and its processes and says that the allegations about suppliers in Leicester were substantially true. There have already been six suppliers terminated and others suspended.

More than 150 audits of suppliers have already been carried out. Suspended ...