Waste-to-Energy growth in the Circular Economy with EQTEC PLC

David Palumbo, CEO of EQTEC PLC (LON:EQT), outlines the market opportunity for EQTEC and their Waste-to-Energy technology in an interview with UK Investor Magazine.

EQTEC PLC are a waste technology company listed on London’s AIM and have recently unveiled a number of strategic partnerships to utilise their waste-to-energy technology.

The most recent of these was with German EPC company ewerGy to develop a portfolio of gasification projects in Greece and the Balkans.

EQTEC’s technology uses feedstock such as refuse and farmers waste in their gasification processes to create an energy sources.

The company has a diverse revenue generation channels including technology sales, engineering contracts and maintenance fees. EQTEC also take stakes in operations by providing the equipment which they can then charge services fees on.

By early 2020 more revenue had been generated than for the whole of 2019, demonstrating the growth in EQTEC’s business model.

Summarising the business model, Jon Levinson of SI Capital wrote in a note:

“Projects tend to be bespoke, but the core characteristic start with a long-term local supply of waste in need of elimination and conversion. EQT joins with partners such as the waste operators, EPC (Engineer Procure and Construct) contractors and capital providers, as they collaborate to build sustainable waste elimination and clean energy infrastructure.

“EQTEC supplies the waste elimination and energy recovery technology and provides engineering and design services to the projects. Post commissioning also providing O&M (Operation & Maintenance) Services so generating recurring revenues over the project’s life. Profit margins will vary from contract, but we anticipate an average of around 15%.”

Lloyds share price: is it now time to buy?

Lloyds shares (LON:LLOY) are not alone in experiencing sharp declines due to the coronavirus COVID-19 pandemic and investors will be accessing a number of shares now ‘on sale’.

The Lloyds share price has dropped a significantly since the beginning of 2020 with shares down over 40% from the start of 2020 to the middle of March.

The drop is inextricably linked to the spread of coronavirus, and the market scrambling to price in the decline in economic activity.

However, historical analysis of shares and markets during periods of panic highlights that in almost all circumstances going back to the Great Depression, shares overreact to the downside during the onset of negative news, before recovering towards prior valuation averages.

Lloyds share price

Lloyds share price as shares are currently trading at just 9.6X historical earnings. This compares to a long term FTSE 100 average of around 17x. Value investors would argue the low PE Ratio signals a buying opportunity, but this doesn’t reflect the drop in earnings in 2020, which cause earnings ratios to increase for 2020 FY. This won’t be a surprise to the markets, however, and investors will eventually look past COVID-19, just as they looked past PPI payments and the restructuring costs caused by the financial crisis.Economic fears

Lloyds’ profitability is directly linked to the strength of economy and borrowing demand by business and companies, which is collapsing as coronavirus fears cause panic among consumers and the government restricts everyday activities. Notwithstanding the economic pain driving downside in Lloyds, this pain is deemed necessary by governments to help combat the spread of coronavirus. Further volatility in shares should be expected as we move towards a peak in new COVID-19 cases and restriction on populations are increased. “We know you have to hurt the economy to stop the virus. But the damage is probably going to be temporary, and we’re going to see a recovery probably in the back half of this year,” said Art Hogan, Chief Market Strategist at National Securities in an interview with CNBC. As well as relying in strong economic activity for sustained profitability, Lloyds is also a facilitator of economic activity. The UK government have said they stand ready to support the economy and have introduced the most significant package of financial support measures made by a peacetime government. Through the new Coronavirus Business Interruption Scheme, the UK government will underwrite risky loans to business made by banks such as Lloyds. This will provide support for Lloyds’ underlying lending business as they offering payment holidays for personal loans and mortgages. These measures will avert the worst case scenario for banks and investors should note we are facing a medical crisis as opposed to a financial crisis similar to 2008. Banks such as Lloyds are structurally sound but profitability is set to be dented for a quarter or two. This will be temporary, and just as the economic slowdown was quickly priced into the Lloyd share price, markets will react with buying on any positivity in the battle against COVID-19.Shefa Gems move towards commercial mining with award of Certificate of Discovery

Shefa Gems (LON:SEFA) have been awarded a Certificate for Discovery by the Ministry of National Infrastructures of the State of Israel, a significant milestone in Shefa Gem’s development of Kishon Mid Reach mine.

Shefa have been analysing exploration viability of the mine and today’s announcement paves the way the to commercial mining in the future.

The positive news was reflected by an initial 20% jump in Shefa’s share price on Wednesday to 3.00p.

Instrumental to the decision to award the certificate was Shefa’s prior discovery of their Carmel SapphireTM, a gem unique to Shefa known as a conundrum mineral rich in titanium. The discovery of such a mineral has not been made anywhere else in the world and provides Shefa with a strong footing for further development and eventual production.

The Carmel SapphireTM won Gem of the Year 2018 from International Mineralogical Association.

The next step for Shefa Gems is the application for mining rights with the Israel Lands Authority, following the preparation of a mining plan.

Vered Toledo, CEO of Shefa Gems, said:

“This is a pivotal moment for Shefa Gems. I would like to thank all our shareholders who have expressed confidence in the Company’s activities over the years. After a great deal of hard work by the team, including our network of international expert consultants, Shefa Gems, a pioneer in precious stones exploration, has demonstrated both the commercial potential and the scientific significance of the unique gem stones hidden in the rocks and soils across the regions of Mount Carmel, and the northern valleys of Israel.”

“The Company is now poised to move into an exciting new mine development phase. While there remains exploration work to discover the primary sources, the principal focus now changes to planning and developing the mine and to establishing integrated sales and marketing channels. I look forward to reporting to our shareholders as we progress towards mine development.”

COVID-19: Superdry struggles with store closures

Superdry plc (LON:SDRY) shares crashed on Wednesday after the company issued a warning concerning the evolving COVID-19 outbreak.

Shares in the fashion retailer were down by over 21% during trading on Wednesday.

Superdry said that it is experiencing “unprecedented challenges” as the virus continues to spread.

In order to mitigate the impact of the illness, the company has temporarily closed stores in many countries.

Superdry added that, because this will significantly impact trading, it will not be able to meet its guidance.

As uncertainty surrounding the outbreak of the virus continues, the company will not be providing formal guidance for the 2020 financial year.

Currently, 78 stores across Europe are affected by government closures, Superdry said, which makes up the majority of its European store estate.

Most stores in the UK and the US remain open, but footfall has reduced significantly during a time when people are being told to stay at home and self-isolate.

“Given the performance to date, we do not expect the decline in sales from our retail stores to be fully mitigated by sales through our Ecommerce channel, which remains fully open for business. Whilst we are also pursuing cost saving measures across the business, we do not expect these to be sufficient to offset the sales decline,” Superdry said in a statement.

“Along with everyone else, Superdry is experiencing major disruption to our business operations and recovery as we seek to protect our staff and customers from COVID-19,” Julian Dunkerton, Chief Executive Officer, said.

“We are taking mitigating action wherever we can but the situation is very fluid and uncertain, and we are working to put in place additional financing to secure our recovery,” the Chief Executive Officer continued.

Julian Dunkerton added: “We also welcome the measures announced by the Chancellor yesterday to support UK businesses. The safety of our staff and customers remains our number one priority and we continue to take all appropriate action in line with local government advice. Together, we’re going to make our way through this unprecedented challenge, and I’m confident we can reset the brand and deliver on our transformation plans.”

Shares in Superdry plc (LON:SDRY) were down on Wednesday, trading at -21.66% as of 13:21 GMT.

COVID-19: tips and advice on social distancing

As the COVID-19 outbreak continues to evolve in the UK, I have decided to do my bit to help contain the spread of the virus by staying indoors and reducing social interaction.

This hasn’t been easy for me; as someone who goes to the gym several times a week, enjoys dining out and spending time in bars and pubs, it’s been difficult to adopt this new lifestyle.

However, for my family in Italy, this is nothing new. The nation was put on lockdown as the COVID-19 outbreak accelerated and it became Europe’s worst-affected country.

I have now spent almost a week indoors; here are a few tips which I have found to be particularly helpful.

1. A routine

It can be difficult to maintain a routine whilst you are working from home. However, it is important to maintain a routine even when you no longer have to do your usual commute. I still get up fairly early, shower, get dressed and eat breakfast. If the weather’s nice, I’ll have a warm drink outside in my garden to get some fresh air. Getting dressed out of your pyjamas is key here; I’m not saying you have to suit up, but getting dressed into comfortable clothing that isn’t pyjamas certainly helps me get into a more productive mindset.2. Avoid working from your bed

This moves on nicely to another helpful tip; avoid working from your bed. It can be really tempting to sleep in, open up your laptop and begin working from the comfort of your bed. However, this makes me personally feel really lethargic. I take it one step further and refuse to work from my bedroom, opting for my living room or kitchen instead.3. Exercise

Even if you’re confined to your home, it is still possible to get some exercise. Exercising from home can be as simple as a quick Youtube search for a home workout. Equally, you can easily purchase some home exercise equipment like dumbbells and barbells online. Gyms aren’t strictly banned, but I’m personally staying away as I don’t want to be responsible for possibly passing anything on to someone more vulnerable than me.4. Spend some time offline

Naturally, you won’t always feel up to jumping around your garden or living room, but I always try to spend a few hours offline each day. Reading, listening and watching the news can become really overwhelming. Of course it’s important to keep updated, but this doesn’t have to take up the majority of your time. I recommend spending a few hours a day away from your devices and doing a few different activities instead. This might include cooking, reading, doing yoga, cleaning, gardening (if you have a garden), learning that language you’ve always wanted to learn, or even doing something creative like painting or drawing. Regardless of the activity, I find it helpful to absorb zero news media for an hour or two a day. This doesn’t mean that you are in denial about the current situation; it means that you are taking care of your emotional wellbeing during a time when our physical health is at risk. Keeping away from busy crowds is recommended, but keeping away from busy news feeds can also be helpful.5. Keep in contact with your friends and family

Call them, talk to them, share stories… just because you’re indoors, it doesn’t mean you can’t socialise. You can find more advice on staying at home here.Government reveals plan to help businesses amid COVID-19

The government revealed yesterday a plan to help safeguard the British economy from the evolving outbreak of COVID-19.

As measures to contain the spread of the virus have been put in place, several businesses are being negatively hit.

Indeed, many people are staying indoors during a time when they are being told to self-isolate to protect themselves from infection.

This puts an enormous strain on businesses in areas such as hospitality, which rely on costumers to dine in their restaurants, bars and pubs.

Elsewhere, the travel industry is feeling the bite of containment measures such as travel bans.

On Tuesday, the British government announced a plan to help these businesses, including at least £330 billion in loans – equivalent to 15% of GDP.

This allows any business to access a government backed loan or credit, Chancellor Rishi Sunak said.

Chancellor Rishi Sunak also announced that, in the coming days, a support package specifically for airlines and airports will be discussed.

“We must act like any wartime government and do whatever it takes to support our economy,” said Boris Johnson in a Tuesday afternoon press conference.

The Chancellor also revealed the highlights of the plan in a thread of 11 tweets. I have selected a few to share:

https://platform.twitter.com/widgets.js1/ We will support jobs, we will support incomes, we will support businesses, we will help you protect your loved ones. We will do whatever it takes.

Today, I am making available an initial £330bn of guarantees – equivalent to 15% of our GDP. Measures include: — Rishi Sunak (@RishiSunak) March 17, 2020

https://platform.twitter.com/widgets.js2/ Any business who needs access to cash will be able to access a government-backed loan, on attractive terms.

If demand is greater than the initial £330bn I’m making available today, I will go further and provide as much capacity as required. — Rishi Sunak (@RishiSunak) March 17, 2020

https://platform.twitter.com/widgets.js3/ To support lending to small and medium sized businesses, I am extending the new Business Interruption Loan Scheme I announced at the Budget last week, so that rather than loans of £1.2m, it will now provide loans of up to £5m, with no interest due for the first six months.

— Rishi Sunak (@RishiSunak) March 17, 2020

https://platform.twitter.com/widgets.js4/ I announced last week that for businesses in the retail, hospitality and leisure sectors, with a rateable value of less than £51,000, they will pay no business rates this year. Today, I provided those businesses with an additional cash grant of up to £25,000 per business.

— Rishi Sunak (@RishiSunak) March 17, 2020

BMW expects COVID-19 hit, shares down

BMW Group (ETR:BMW) shares dropped on Wednesday after the company issued a statement concerning to the evolving COVID-19 outbreak.

Shares in the German company were down by almost 6% during Wednesday morning trade.

BMW said that the uncertainty surrounding the spread of COVID-19 makes it difficult to accurately forecast the group’s business performance for the 2020 financial year.

As the virus continues to spread and containment measures begin to be implemented, BMW is expecting a negative impact on delivery volumes in all major markets across the 2020 year as a whole.

Additionally, the group said that automotive segment deliveries to customers worldwide in 2020 will be significantly lower than the level from the year prior.

EBIT margin of the automotive segment is expected to lie within a range of 2% to 4%, BMW added.

The company continued to add that it expects group profit before tax to be “significantly lower” than in 2019.

“Solidarity and responsible action are called for. In our society it is the duty of the strong to protect the weak. The BMW Group therefore fully supports the measures aimed at containing the spread of coronavirus,” the Chairman of the Board of Management of BMW, Oliver Zipse, said concerning the spread of COVID-19.

Oliver Zipse continued: “We take our responsibility seriously, both when it comes to ensuring the protection and health of our employees and to achieving the best possible balance in terms of profitability. One thing is certain: coronavirus is here now, but there will also be a time after coronavirus. The approach we are taking clearly reflects the BMW Group’s ability to react quickly and flexibly.”

“New technologies are key to the future of mobility. Up to 2025, we intend to invest more than 30 billion euros in research and development to underscore our position as an innovation leader. This also expresses our confidence for the future business development,” Oliver Zipse said.

This week, the British government accelerated measures to respond to the outbreak of COVID-19.

Shares in BMW AG (ETR:BMW) were down on Wednesday, trading at -6.44% as of 10:04 CET.

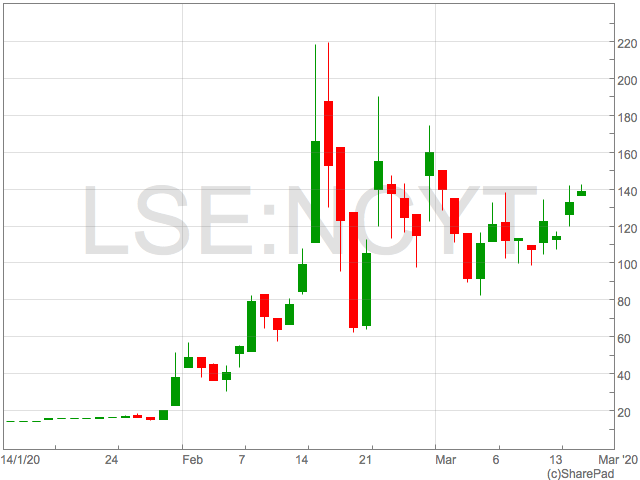

Novacyt continues to provide opportunity in the face of uncertainty

Shares in Novacyt (LON:NYCT) have continued to be a beacon of light for investors this week as the company announced an initial deal with Public Health England (PHE) for their COVID-19 testing kits.

Novacyt said its Primerdesign business unit had received a £1 million order for their coronavirus testing kits from the UK government who will test the kits in eight hospitals over four weeks.

The order from PHE order means Novacyt have received £3.7 million of orders for its testing kit, an amount it says usually represents eight months of it’s sales.

There is a consensus the wider testing of coronavirus is key to bringing the spread under control.

“We have a simple message for all countries Test, test, test. Test every suspected case,” said Dr Tedros Adhanom Ghebreyesus, Director General of the World Health Organisation.

He continued “if they test positive, isolate them and find out who they have been in contact with two days before they developed symptoms and test those people, too.”

There have been two main problems with this thus far, firstly government were slow to increase the number of tests and the second, and most relevant to Novacyt, is the lack of available tests.

It is impossible to make any forecasts of how many people will need to be tested globally or in the UK and with some officials predicting many multiples more have COVID-19 than current records, the potential demand is significant.

While this has investors excited, some analysts are cautioning that Novacyt are not alone in the pursuit of testing kit development.

“The race for the testing kits is far hotter than the vaccines at the moment, largely due to the testing time for a vaccine. I would, however, err on the side of caution as there are plenty of other companies in the race for testing kits but the recent news on Novacyt’s PHE deal is a big a positive, as is the WHO message of “test test test,” said John Woolfitt, Director of Trading at Atlantic Capital Markets.

Novacyt shares

The AIM-listed pharmaceutical company starting making announcements about the development of their testing kits at the end of January, when shares were trading at just 20p. Shares have since rocketed and reached intraday highs above 215p, before falling back. However, shares have enjoyed renewed buying pressure this week sending shares back over 140p for a period. Test, test, test

Test, test, test

There is a consensus the wider testing of coronavirus is key to bringing the spread under control.

“We have a simple message for all countries Test, test, test. Test every suspected case,” said Dr Tedros Adhanom Ghebreyesus, Director General of the World Health Organisation.

He continued “if they test positive, isolate them and find out who they have been in contact with two days before they developed symptoms and test those people, too.”

There have been two main problems with this thus far, firstly government were slow to increase the number of tests and the second, and most relevant to Novacyt, is the lack of available tests.

It is impossible to make any forecasts of how many people will need to be tested globally or in the UK and with some officials predicting many multiples more have COVID-19 than current records, the potential demand is significant.

While this has investors excited, some analysts are cautioning that Novacyt are not alone in the pursuit of testing kit development.

“The race for the testing kits is far hotter than the vaccines at the moment, largely due to the testing time for a vaccine. I would, however, err on the side of caution as there are plenty of other companies in the race for testing kits but the recent news on Novacyt’s PHE deal is a big a positive, as is the WHO message of “test test test,” said John Woolfitt, Director of Trading at Atlantic Capital Markets.

Laura Ashley collapses as COVID-19 hits

Laura Ashley Holdings plc (LON:ALY) shares crashed on Tuesday after the company announced that it has filed for administration.

Shares crashed over 60% following the news.

The British retailer said that the COVID-19 outbreak has had an “immediate and significant impact” on trading.

As the virus continues to spread across the world, many businesses have been hit hard and have issued warnings concerning the situation.

But for Laura Ashley, which was already struggling prior to the outbreak of the virus, the situation has been critical.

During a time where people are being encouraged to stay indoors and self-isolate, footfall is bound to be lower on the high street.

“For the seven weeks up to 13th March, trading for the Laura Ashley business improved by 24% year-on-year and the directors were encouraged by this strong performance. However, the COVID-19 outbreak has had an immediate and significant impact on trading, and ongoing developments indicate that this will be a sustained national situation,” Laura Ashley said.

“Accordingly, the Company regrets to announce that the directors of the Company, and of the named subsidiaries, have today filed notices of intention to appoint Robert Lewis and Zelf Hussain as administrators. If administrators are appointed in respect of the Company, given the Group’s creditor position, the Company is not certain whether there would be any surplus assets available to shareholders of the Company,” the company continued.

Elsewhere, the travel industry has been hit particularly hard by the COVID-19 outbreak as demand for travel has decreased and as countries, such as Italy, have been put on lockdown.

Over in the UK, the British government has been accelerating measures to contain the spread of the virus.

Shares in Laura Ashley Holdings plc (LON:ALY) were down on Tuesday, trading at -60.18% as of 11:15 GMT.