Components supplier Dewhurst (LON:DWHT) suffered from both falling sales and profit in the half year to March, sending shares plummeting at market open.

Profit before tax fell 4 percent to £2.8 million, down from £3 million this time last year, with revenue taking a 5 percent hit to land at £24.7 million. Operating profit also fell 19 percent to £2.5 million, with the company warning that the slump may well continue into the second half.

A strong pound was largely responsible for the fall, as well as a lack of demand for keypads, one of its key sales drivers.

“Although keypad sales have picked up a little in the last couple of months we do expect a declining trend on these products over the long term,” the company said.

“The second half may see a period of consolidation, but on balance we are encouraged by the future growth prospects for the group,” the company added.

The group maintained its interim dividend at 3.5 pence. Shares in Dewhurst are currently trading down 14.44 percent at 800.00 (0920GMT).

Shares in Toshiba (TYO:6502) jumped on Wednesday on the announcement of a share buyback plan worth around 700 billion yen.

The share buyback was designed to fulfill the promise made to its investors to share some of the profits made from the $18 billion sale of its memory chip business.

The group finalised the sale of the memory business to a consortium led by Bain Capital earlier this month. The deal came as a relief to investors, after financial struggles driven by the doomed Westinghouse nuclear business meant the company came close to delisting.

The scale of the buyback exceeds what some in the market expected, which was around 600 billion yen. The timing of the announcement is earlier than we had expected, so the first impression is positive,” Mizuho Securities analyst Takeshi Tanaka said in a note to clients.

Shares rose around 11 percent when the news was released, and are currently trading up 6.65 percent at 337JPY (0901GMT).

Dixons Carphone (LON:DC) shares plummeted over 4 percent at market open on Wednesday, after admitting to a huge data breach affecting 1.2 million people.

Hackers “attempted to compromise” 5.9 million payment cards, but Dixons Carphone said only 105,000 cards without chip-and-pin protection had been leaked.

The group added that there was no evidence that any of the cards had been used fraudulently following the breach, but chief executive Alex Baldock said it was “extremely disappointed” by the data breach and “sorry for any upset”.

“The protection of our data has to be at the heart of our business, and we’ve fallen short here.

“We’ve taken action to close off this unauthorised access and though we have currently no evidence of fraud as a result of these incidents, we are taking this extremely seriously,” he added.

The news comes as a further blow to Dixons Carphone investors, just a month after it warned that it had been affected by the tough market conditions and said it may suffer a sharp fall in profits.

Shares in the company are currently trading down 4.12 percent at 189.60 (0842GMT).

Waste management company Biffa reported a 33 percent rise in profit on Wednesday, alongside the announcement that CEO Ian Wakelin would be stepping down.

Underlying after tax profit rose 33.8 percent to £47.9 million, with net revenue jumping 8.8 percent to £977.7 million. Underlying earnings rose 8.9 percent to £150 million, with underlying operating profit rose 10 percent to £81.2 million.

CEO Ian Wakelin also announced that he would be stepping down from his position, to be replaced by CFO Michael Topham.

Wakelin said: “I have thoroughly enjoyed the last eight years and will leave satisfied that we have achieved a great deal including successfully bringing the business back to the stock market.

“I would like to thank all of my colleagues across the business for their support and commitment over the years. Biffa is a great business with a great future ahead of it.”

Shares in Biffa (LON:BIFF) are currently trading down 0.83 percent at 239.50 (0823GMT).

British accessories brand Mulberry reported a fall in UK sales in the 10 weeks to June, but announced a new move into South Korea designed to take advantage of the Asian market.

Pre-tax profit fell 8 percent to £7.5 million, mainly linked to the startup costs of the group’s expansion in Asia, with revenue rising 1 percent to £169.7 million. Without these costs, pre-tax profit from existing business rose 36 percent to £11.3 million.

The UK market remained week, with the group reporting a 9 percent fall in sales on the back of “lower footfall and fewer tourists, as more widely reported”.

“We have made significant progress during the year on our international strategy, creating new Mulberry subsidiaries in China, Hong Kong, Taiwan and Japan,” chief executive chief executive Thierry Andretta said.

The group then announced its decision to merge with SHK in Korea to create Mulberry Korea.

“Our international business is growing and following the completion of this set up phase in Asia, we will focus on omni-channel, digital partnerships and marketing investment in the region.”

“Although the UK market remains challenging, we will continue to invest in our strategy to develop Mulberry into a global luxury brand to deliver increased shareholder value.”

Mulberry will own 60 per cent of the share capital of the newly created entity, with SHK owning the remaining 40 per cent stake, and it is expected to start trading by autumn of this year.

Sponsored by LendingCrowd

There’s no such thing as a risk-free investment. However, as all savvy investors know, diversification helps to manage risk and improve your opportunity for higher returns.

A typical portfolio might include a mix of cash savings, stocks and shares, bonds and property. Increasingly, investors are turning to peer-to-peer (P2P) loans to further diversify their holdings while achieving attractive returns.

The UK has a wide choice of P2P platforms, offering you the opportunity to generate inflation-beating returns by joining forces with other investors and lending to consumers, property developers and businesses of all sizes. Some providers let you choose individual loans to invest in, while others automatically spread your money across a variety of loans.

Consumer-focused P2P platforms lend to people who won’t – or can’t – get a bank loan, so you need to consider whether you’re comfortable with this lack of diversity. You’re probably already investing in the property market, either with your own home or through buy-to-let. Do you want even more exposure to this sector?

LendingCrowd believes that lending to creditworthy small businesses across a wide range of sectors gives you the best opportunity to diversify within the P2P asset class

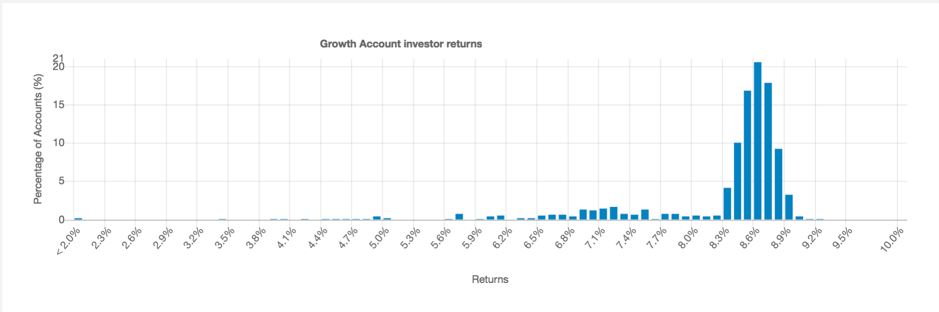

LendingCrowd Growth Account returns

Annualised return for all current LendingCrowd Growth Accounts that have been open for at least three months

Liquidity – the ability to convert assets into cash – is another important factor to consider. As an investor, you’re aiming to generate a return on your money, either for a specific goal or for a rainy day. But what happens when that proverbial rainy day arrives?

Property can take months to sell, but if you invest in a property fund you may want – or need – to access your money within a few days. This isn’t normally a problem, because funds hold cash for this very reason. However, following the Brexit vote in 2016, a rush for withdrawals saw properties sold at knock-down prices, causing some fund managers to temporarily prevent investors from withdrawing their cash altogether.

A key benefit of LendingCrowd is that you’re not locked in when you invest. The platform offers a secondary market, enabling you to sell loan holdings to other investors. Under normal market conditions, even large portfolios are sold down in a week.

Investors also need to consider correlation. You don’t want the value of all your investments to fall at exactly the same time. That’s why fund managers often hold government bonds to provide a source of stable returns, as these tend to rise in value when equities fall.

However, in the current low interest rate environment, gilts and cash struggle to provide returns above inflation, while stocks and shares tend to follow the same global economic trends in these times of increasing globalisation.

Business debt funding represents an excellent way for investors to diversify into a new asset class that doesn’t correlate with the fluctuations of the global stock markets yet provides inflation-beating returns. With P2P platforms such as LendingCrowd, you can build diverse portfolios of business loans by investing as little as £1,000.

LendingCrowd gives you instant access to a diverse range of sectors, from agriculture and healthcare to retail and transport. Each borrower is carefully assessed by its expert Credit Team, who ensure only the most creditworthy businesses are approved for loans.

With a LendingCrowd Growth Account, you can earn a target return of 6%* a year by opening an account with as little as £1,000 to instantly create a diversified portfolio of secured business loans. Your capital and interest repayments are reinvested automatically, increasing your diversification over time.

Analysis of LendingCrowd’s current loan book shows that no one sector accounts for more than 15% of its total lending. For example, loans to agricultural business make up less than 3% of overall lending by value, while manufacturing and engineering accounts for 7.1% and healthcare 7.3%. By taking this diversified and balanced approach, Growth Account investors have achieved an average return of 8.5% over the past 12 months. Remember that past performance is not a guide to future returns.

You can hold all of LendingCrowd’s accounts within its Innovative Finance ISA for tax-free** returns.

Sign up as a LendingCrowd investor before 29 June 2018 and you can earn up to £500 cashback when you invest within 14 days. Terms apply – find out more at www.lendingcrowd.com*Capital at risk. Target rate is variable, net of ongoing repayment fees and bad debt and before the 1% capital withdrawal fee. The ability to sell your investments depends on other investors buying your loans.**Tax treatment depends on the individual circumstances of each investor and may be subject to change in future.

UK wage growth has unexpectedly slipped to 2.8 percent, falling short of analyst expectations.

The Office for National Statistics has reported the 0.1 percent fall for the first three months in April despite unemployment falling to 1.42 million.

Economists had predicted a steady wage growth for the three months to April

The decline in wage growth has raised doubts over whether the Bank of England plans to raise interest rates over the coming summer.

The Bank of England has previously suggested that it will raise rates this year if the economy bounces back as it has expected.

The hike is increasingly unexpected following the slowing wage growth and poor manufacturing data for April.

Howard Archer of the EY Item Club said: “Strong employment but softer earnings growth will likely keep uncertainty high about the prospects of an August interest rate hike by the Bank of England.”

“We suspect that there is an increased chance that the Bank of England will hold fire on interest rates until November given that the MPC wants to see clear, sustained evidence that the UK economy has improved from its first quarter relapse before hiking,” he added.

The Bank of England remains optimistic and is expecting wage growth to pick up and reach 3.5 percent by the end of 2020.

“Wage growth is stuck in the slow lane. At this rate pay packets won’t recover to their pre-recession levels for years,” Frances O’Grady, the TUC’s General Secretary.

“We need to speed things up. Extending collective bargaining would boost living standards and help workers get a fairer share of the wealth they create.”

The slowing wage growth is partly due to the lack of investment in new machinery and technology since the financial crisis and the public sector pay freeze followed by the 1 percent pay cap.

The FTSE 100 opened higher on Tuesday morning, before sinking to trade down around 0.20 percent.

This is in contrast to European markets, which have broadly had a positive start to the day, with the DAX Index up 0.15 percent and the IBEX up 0.066 percent.

Fiona Cincotta, Senior Market Analyst at City Index, commented:

“The FTSE opened higher but quickly started losing ground in early trade with Admiral Group, Barratt Development and Anglo American leading the way lower.

“In contrast, European markets were on the rise benefiting from a major divestment by the French hotel chain Casino and plans by food retailer Carrefour to work with Google on online shopping plans.”

The event on everyone’s lips is the meeting between President Trump and Kim Jong-Un, a hotly anticipated event after months of tension between the two leaders.

“The long-awaited meeting between President Trump and North Korean leader Kim Jong Un ended up on a positive note with the two heads of state signing a document committing to the complete removal of nuclear weapons from the Korean peninsula. The agreement could pave the way for the opening up of the country to the rest of the world and building of new business and trade links in Asia”, Cincotta said.

Retail shares

Retailers had a surprisingly strong morning on Tuesday, with Marks & Spencer, Burberry, Kingfisher and Primark-owner ABP trading up around 1 percent in early trading.

But Aim-listed online retailer Boohoo reported a strong set of results, but shares fell 4 percent after the results were not quite as high as anticipated by investors.

Centrica (LON:CNA), Evaz (LON:EVR) and Reckitt Benckiser (LON:RB.) were the biggest risers on the FTSE 100, with Barratt Developments (LON:BDEV), Berkeley Group Holdings (LON:BKG) and Persimmon (LON:PSN) being the biggest fallers.

ONS employment figures

The latest employment figures from the Office for National Statistics came as a pleasant surprise on Tuesday, recording 32.39 million people in work in the February-to-April period. This is 146,000 more than the previous quarter, and 440,000 more than in the same period a year earlier.

However, wages continued to grow slowly in the three months to April, with average earnings – excluding bonuses – up by 2.8 percent. This is lower than the 2.9 percent growth rate between January to March.

Bellway shares fell over 2 percent on Tuesday morning, despite reporting an increase in sales for the current year.

The group reported robust demand for its affordably priced homes, seeing a 5.4 percent increase in the reservation rate to 223 per week in the period from 1 February to 4 June.

It said it was likely to sell around 600 more homes than last year at over £280,000 each, with an operating margin of around 22 per cent. However, the group said that it expected full year guidance to stay the same.

“Demand is most pronounced for affordably priced family homes countrywide, with divisions operating in locations as dispersed as Scotland, Essex and the Midlands all continuing to show strong performance,” the company said.

“This has been another successful trading period for Bellway, in which the demand for new build homes remained strong, enabling the group to continue delivering its long term and sustainable strategy of increasing shareholder value through responsible volume growth,” executive chairman John Watson continued.

Shares in Bellway (LON:BWY) are currently trading down 2.14 percent at 3,336.40 (0948GMT).

Online fashion retailer Boohoo (LON:BOO) reported another stellar set of of results on Tuesday, boosted by strong figures from recent acquisition PrettyLittleThing.

Group revenue rose 53 percent to £183.6 million in the half year to May, with the biggest source of growth coming from PrettyLittleThing, which saw a massive 158 percent sales boost.

UK revenues grew by 49 percent, growing even faster in the US by 75 percent. Boohoo itself reported a revenues of £97.2 million, up 12 percent on last year’s Q1 record growth, with PrettyLittleThing revenue hitting £79.2 million.

The group said it expects revenue growth for the full year to be between 35 percent and 40 percent, with adjusted EBITDA margin between 9 and 10 percent.

Mahmud Kamani and Carol Kane, Boohoo’s joint CEOs, commented:

“We are very pleased with the group’s results for the first quarter of the financial year. Our multi-brand strategy is delivering above-market rates of growth globally. Significant market share gains have been achieved in all of our key focus markets, with our compelling combination of the latest fashion at incredible prices, backed by great customer service resonating strongly with our customers.

“We remain highly encouraged by our performance in the first quarter and confident of our expectations for the remainder of the year and beyond as we continue to execute on our winning strategy.”

Shares in Boohoo (LON:BOO) are currently trading 4.22 percent down however, despite the strong figures, at 210.81 (0930GMT).