Ferrexpo reported the company’s production report for the first quarter of 2022 leading the iron ore miner’s shares to gain 8% to 181p in early morning trade on Friday.

Ferrexpo had a total iron ore pellet output of 2.7m tonnes in the first quarter of 2022, down 11% from Q4 2021 due to operational and logistical restrictions resulting from Russia’s invasion of Ukraine, which is ongoing.

The group’s output continues to be fully composed of high-grade iron ore, with a Fe content of 65% or more.

The group’s logistics routes to Europe through rail and barge remain open, however, operations at the Black Sea port of Pivdennyi remain halted.

As of 31 March 2022, Ferrexpo had a net cash position of roughly $159m, with consistently available financing lines having a minor influence on the debt position.

The group has managed to maintain an acceptable liquidity balance between offshore and onshore funds, ensuring that payments for the group’s staff, operations, and tax obligations are completely paid on schedule.

Ferrexpo’s top focus continues to be the safety of its employees.

The miner will continue to produce and transport its goods in compliance with the Government of Ukraine’s call for economic operations to continue as long as the capability continues and it is safe to do so.

Jim North, Chief Executive Officer, Ferrexpo said, “The safety of our workforce remains our highest priority.”

“Our operations and local communities are outside the main conflict zones within Ukraine, enabling us to continue our activities, including the delivery of iron ore pellets to customers in Europe via rail and barge, which have historically represented approximately 50% of sales.”

“The port of Pivdennyi in southwest Ukraine, where the Group’s berth is located, remains closed, and we are reviewing alternative methods of delivering our products to seaborne markets.”

The oncology drug development consultancy, Physiomics signed on the Servier Group, an international pharmaceutical company headquartered in France, as a new client on Friday.

Servier’s key therapy areas include cancer, with a particular emphasis on immunotherapies and monoclonal antibodies for difficult-to-treat diseases with significant unmet medical needs.

Physiomics will use its Virtual Tumour software platform to study and simulate the effect of a range of immuno-oncology combinations in development utilising Servier medicines in pre-clinical and clinical settings.

The project will be completed in the next 7-8 months, according to the forecast.

“We are delighted to have been selected by Servier, one of France’s leading pharmaceutical companies with a truly global outlook as its partner for this modelling and simulation project focused on pre-clinical and translational modelling of a novel immuno-oncology agent in development. We look forward to working with its talented scientists,” said Physiomics CEO, Dr Jim Millen.

Ajax Resources is a shell seeking energy and natural resources assets. There is no specific geography mentioned in the prospectus. Management would seek to help the existing management of the asset to fully exploit it and generate cash.

The share price started trading at 5p and ended the day at 4.75p (4.25p/5.25p). There were just over £13,000 worth of shares traded in three trades.

The pro forma net assets are 2.6p a share. That means that the shares are trading at a 82.7% premium to pro forma net assets. That is high enough for the time being.

==========

Ajax Resources (LON: AJAX)

Natural re...

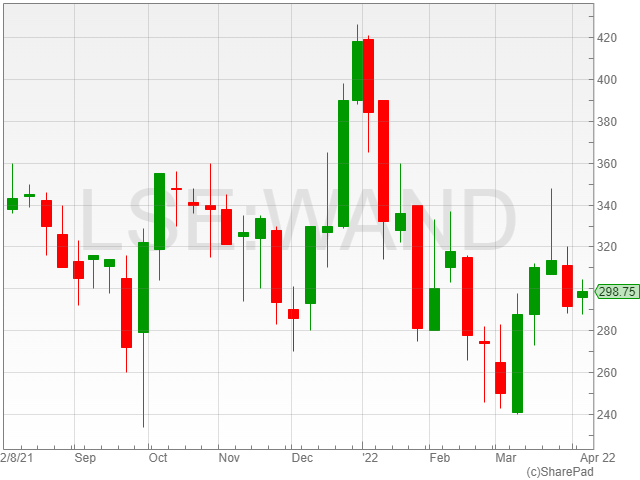

WANdisco announced a $213,000 contract win with a leading personal computer vendor on Thursday.

The software company commented that its LiveData Migrator solution would help its new customer to migrate a subset of data sourced from its existing Hadoop environment to cloud-native systems which can be run within the public cloud.

The group said that its current opportunity is to migrate 1.35 petabytes of data, with the figure set to grow over time with normal production usage, which means that there is reportedly potential for revenues to grow higher as more data is migrated.

According to WANdisco, the new customer selected its technology due to its capability to keep the data up-to-date without the requirement to manually refresh the new environment, which gave it the edge over its competition.

The group highlighted that its real-time updating gave it the advantage of less business disruption, alongside data consistency and security over the process.

“There is a clear business need for companies across sectors to move increasing amounts of data to cloud native systems,” said WANdisco CEO David Richards.

“Our LDM solution supports complete and continuous replication of data sets at any scale, ensuring these critical migrations can take place quickly with zero business disruption.”

“This capability makes WANdisco well placed to continue converting on a strong pipeline of cloud migration opportunities.”

The news follows the company’s $720,000 commit-to-consumer contract with a top-ten global retailer to use its LiveData migrator solution to create a focused work environment tailored for machine learning and other analytical tasks.

“We are delighted to announce another deal with one of our key retail customers, representing yet another proof point of the strong demand we are seeing from organisations across various sectors to migrate data to the cloud,” said Richards in a corporate statement released yesterday.

WANdisco shares fell 1.1% to 299.5p in late afternoon trading despite the positive update.

This deal marks the renewable infrastructure company’s second renewable energy acquisition in Spain.

The wind farm, which has been operating since May 2021, is located in Soria, Castilla y Leon, Spain, and consists of six GE-137 turbines. Long-term operations and maintenance will continue to be provided by GE.

The Soliedra Wind Farm is now contracted as a merchant asset, however, it has the option to contract the power produced through a corporate PPA in the future.

Greencoat Renewables’ total borrowings will account for 40% of its Gross Asset Value following the transaction.

Paul O’Donnell, Partner at Greencoat Capital said, “We are delighted to secure such a high-quality asset from Alfanar and have sight of further value-accretive opportunities in Spain.”

“As the renewable generation market continues to develop, we expect to see greater opportunity in the unsubsidised renewables market and believe Greencoat Renewables is well positioned to benefit both across mainland Europe and in Ireland.”

Jamal Wadi, Managing Director, Alfanar Global Development stated, “We have been in Spain for many years now and are committed to its energy transition. This deal marks another milestone in our ambitious plans for the European markets.”

Cadence Minerals shares were up 0.9% to 18.2p in late afternoon trading on Thursday after the company announced that DEV Mineraco S.A had resumed the sale and shipment of its iron ore stockpiles from the Amapa Project in Brazil.

The mining group said that the shipment represents the first iron ore export since the firm vested its 27% equity interest in the Amapa Iron Ore Project in early 2022.

The two firms own the mine through joint-venture company Pedra Branca Alliance, which owns 100% of DEV Mineraco S.A’s equity.

Cadence Minerals confirmed that it currently expects the shipment’s completion in April, with DEV set to continue with the shipment and sale of the 58% iron ore stockpile in the current economic conditions.

The company also said that DEV has continued to provide ship loading and transport services for the third party owned stockpile at its port.

SEEEN’s video monetization technology and YouTube optimisation services, which are supplied through its MultiChannel Network (MCN), have gained new customers in important vertical markets, building on earlier customer success in the fourth quarter of 2021.

SEEEN’s Contracts

A7FL Sports League

The A7FL Sports League, which debuted in 2014, is a US sports league that aims to provide an alternative to the NFL.

The season of the A7FL has just begun, and SEEEN’s services are expected to improve viewership of the league on its site and social media as it strives to reach a younger audience.

A7FL also hopes to boost engagement and revenue by monetizing crucial moments in its video output.

The A7FL customer win expands on SEEEN’s previous work with Sumitomo for the Rugby World Cup and the group’s MCN network’s own auto racing videos.

UK Financial Markets Publisher

SEEEN has also announced a new CreatorSuite customer who will use the software to power all of the videos on a UK-based financial markets publisher’s website.

The publisher plans to employ SEEEN’s CreatorSuite technology to boost the number of videos watched by the publisher’s 1 million monthly users while also improving advertising and subscription prospects.

SEEEN’s earlier successes with publishers, most notably the financial markets publisher contract announced in 4Q 2021, is built on this customer contract.

US Web Publisher

A significant US digital publisher has also signed on to join SEEEN’S MCN. The MCN has a critical mass of 10,000 producers and receives over 10bn video views per year.

Regarding the customer’s YouTube content categories and calendar, the company will use its knowledge and give direct consulting services. The customer will benefit from two of SEEEN’s technological products, CreatorSuite and Dialog-To-Clip, as part of this deal.

CreatorSuite facilitates the development of re-mixed videos from existing footage, while Dialog-To-Clip speeds up the creation of YouTube Shorts from key phrases.

This contract recognises SEEEN’s solution for publishers to improve their YouTube presence with new videos and YouTube Shorts created with the company’s unique technology.

Akiko Mikumo, Interim Co-CEO, SEEEN commented, “The commercial momentum for CreatorSuite, highlighted in our recent trading update, continues and we have demonstrated we are also able to cross-sell our YouTube MCN and optimisation services to many of these customers.”

“Content providers and the advertising industry have been looking for a fresh set of solutions to market short form video content. We look forward to securing further contracts in these verticals, as well as leveraging our recently announced strategic partnership with Kinetiq to drive larger deals with multi-national clients,” added David Anton, Interim Co-CEO, SEEEN.

888 Holdings shares rose 18.5% to 227.6p in early afternoon trading after the company reported a price drop in William Hill’s non-US business from £2.2 billion to £1.95 billion.

The group said the alterations to the deal reflected the change in the macro-economic and regulatory environment since the transaction was first agreed, along with compliance issues including an ongoing review by the Gambling Commission of Great Britain (UKGC) impacting William Hill’s business dealings.

888 Holdings added that it expects the transaction to bring pre-tax cost synergies of at least £100 million, alongside £15 million in capex synergies by 2025.

The gambling firm noted that it presently anticipates the cumulative achievement of an estimated £5 million in synergies in 2022, with £54 million in 2023, £70 million in 2024 and £100 million in 2025.

The company also said it expects to incur one-time cash costs of around 100% of its annual pre-tax cost synergies, spread throughout the initial three years after the deal is completed.

888 Holdings confirmed that it has fully committed debt financing from several institutions, including J.P. Morgan Stanley, Mediobanca and Barclays Bank of around £2.1 billion, which will either take the form of senior secured term loans or alternative senior secured debt with the potential addition of junior debt and a fully-committed revolving credit facility of £150 million.

The betting company mentioned that in order to accelerate deleveraging, it is set to suspend dividend payments until the combined group’s net leverage ratio meets or is below 300%, or until the board decides to resume payments.

The technology innovator that delivers SaaS solutions, Access Intelligence signed several new contracts with companies such as Netflix and Nestle, according to its announcement on Thursday.

At the time of Access’ January trading update, the group mentioned the success it made in its core business. Since the beginning of the financial year, new clients have continued to join the company for its services.

Reddit, Amazon, Aston Martin, and KPMG are among those in EMEA and North America who have signed up with Access Intelligence.

Despite the obstacles pointed out earlier in the year by the group, new contract wins from major corporations such as Woodside Energy, Tiffany & Co, Netflix, Nestle, and Chevron, as well as new victories in the public sector working with government divisions in Singapore and Malaysia, are reassuring.

Access Intelligence launched Pulsar in Australia and New Zealand, and received a positive response from clients in the region, while in Southeast Asia, the group continues to refine its market positioning strategy in light of the country’s present socioeconomic conditions.

Joanna Arnold, Chief Executive Officer, Access Intelligence, said, “These contract wins demonstrate the strength of the combined Pulsar and Isentia offering to our clients.”

“We are delighted with the contract wins we have seen in Q1. We continue to trade in line with expectations and we look forward to updating shareholders further with the announcement of our full year figures to 30 November 2021 on 25 April 2022 “

Shell posted an updated outlook for Q1trading highlighting a write-down between $4bn and $5bn as a result of its losses associated with Russia on Thursday.

Following Moscow’s invasion of Ukraine, Western corporations such as Shell quickly withdrew from Russia, dissolving trading connections and winding down joint ventures leading to a rough start to 2022 for the oil and gas company.

Shell shares have been bouncing with Russian oil bans, however, the rise in oil prices has cushioned the blow.

Shell had previously estimated the write-down to amount to $3.4bn on its exit from Russia due to contractual obligations, credit losses and receivable write-downs.

The post-tax impact from impairment of non-current assets and extra costs connected to Shell’s Russian activities is expected to be $4bn to $5bn for the first quarter of 2022 according to the results.

Shell has a market cap of approximately $210bn and it explained that the write-down will not impact the company’s earnings.

Shell has not renewed Russian oil contracts and will only do so if directed by the government, however it is legally obligated to take delivery of crude purchased under contracts made before the invasion.

Shell’s Results

Integrated Gas including Renewables and Energy Solutions

The company’s maintenance activities, including the planned reversal of one of the trains at Pearl GTL, are estimated to drive production between 860 and 910 thousand barrels of oil equivalent per day (kboe/d). The Canadian Shales assets are expected to produce around 50 kboe/d, according to the forecast.

Shell’s LNG liquefaction volumes are projected to be between 7.7 million tonnes (mt) and 8.3mt.

In comparison to the fourth quarter of 2021, trading and optimization results for Integrated Gas are estimated to be better, and the underlying Opex is estimated to be between $1.7bn and $1.9bn for the oil and gas company in Q1 2022.

The company’s depreciation before taxes is projected to be between $1.2bn and $1.4bn. The tax bill is likely to be in the range of $700m to $1.1bn for Shell.

Shell’s renewables and energy solutions are estimated to contribute between $100m and $600m of the overall Integrated Gas adjusted earnings.

Upstream

Between 1,900 and 2,050 kboe/d are predicted to be produced by Shell. The projection includes a 50 kboe/d drop as a result of the transfer of Canada Shales assets to Integrated Gas.

The company’s underlying Opex is estimated to be in the range of $2.3bn to $2.7bn with pre-tax depreciation projected to be between $2.8bn and $3.1bn and the tax bill is expected to range between $2.8bn to $3.3bn.

Oil Products

The marketing results for Shell are estimated to be in line with Q4 2021, with the underlying Opex estimated to be in the range of $1.8bn to $2.0bn and daily sales volume estimated to range between 2.2m and 2.6m barrels.

In terms of the product results of the company, trading and optimisation results are predicted to be much higher than Q4 2021.

The group’s estimated refining profit is around $10.23 per barrel, up from $6.55 per barrel in the fourth quarter of 2021.

Due to fewer turnaround events, refinery utilisation for Shell is predicted to be between 70% and 74%, higher than Q4 2021.

The underlying Opex is estimated to be in the range of $1.6bn to $2bn for Shell, with daily sales volume estimated to range between 1.5m and 2.3m barrels.

The company’s pre-tax depreciation is estimated to range between $700m and $900m, with around half of that going to marketing and the other half to refining and trading.

The tax bill is projected to be between $400m and $700m, with marketing accounting for 20%-30% and refining and trading accounting for 70%-80%.

The pipeline business will be shifted from marketing to the refining and trading sub-segment in the first quarter of 2022 as part of the continuing re-segmentation initiatives.

Chemicals

Shell’s chemicals margins are likely to be flat compared to Q4 2021, owing to lower unit margins due to higher feedstock and utility costs, which will be compensated by higher utilisation.

The volume of chemicals sold is projected to range between 3.1mt and 3.6mt in Q1 2022.

Due to fewer turnaround events, chemical manufacturing plant utilisation is predicted to be between 78% and 82% in Q4 2022, which is higher compared to 2021 for Shell.

The underlying Opex for Shell is projected to be in the range of $800m to $1bn and depreciation is projected to cost between $250m and $300m before taxes.

The company expects credit of up to $100m from the taxation charge and due to higher feedstock and utility costs offset by improved utilisation, adjusted earnings are estimated to be in line with the fourth quarter of 2021.

Shell shares have dropped 1.6% to 2,098p following the announcement of the $4bn write-downs caused by the exit from Russia.