Great Southern Copper shares were up 3.7% to 4.2p in early afternoon trading on Monday, after the company announced the identification of several shallow and buried targets for follow-up exploration at its San Lorenzo copper-gold project in Chile.

The mining firm issued its report following the processing and interpretation of its ground magnetic data for its coastal cordillera-based project, on the back of a completed 63.6 km ground magnetics survey, which was designed to enhance Great Southern Copper’s geological understanding of the operation.

The processing and interpretation of the data was carried out by Perth-based Australian company ExploreGeo.

Great Southern Copper confirmed that the data revealed additional structural detail and areas of magnetite-destructive alteration, along with highlighted areas indicating the presence of buried intrusives.

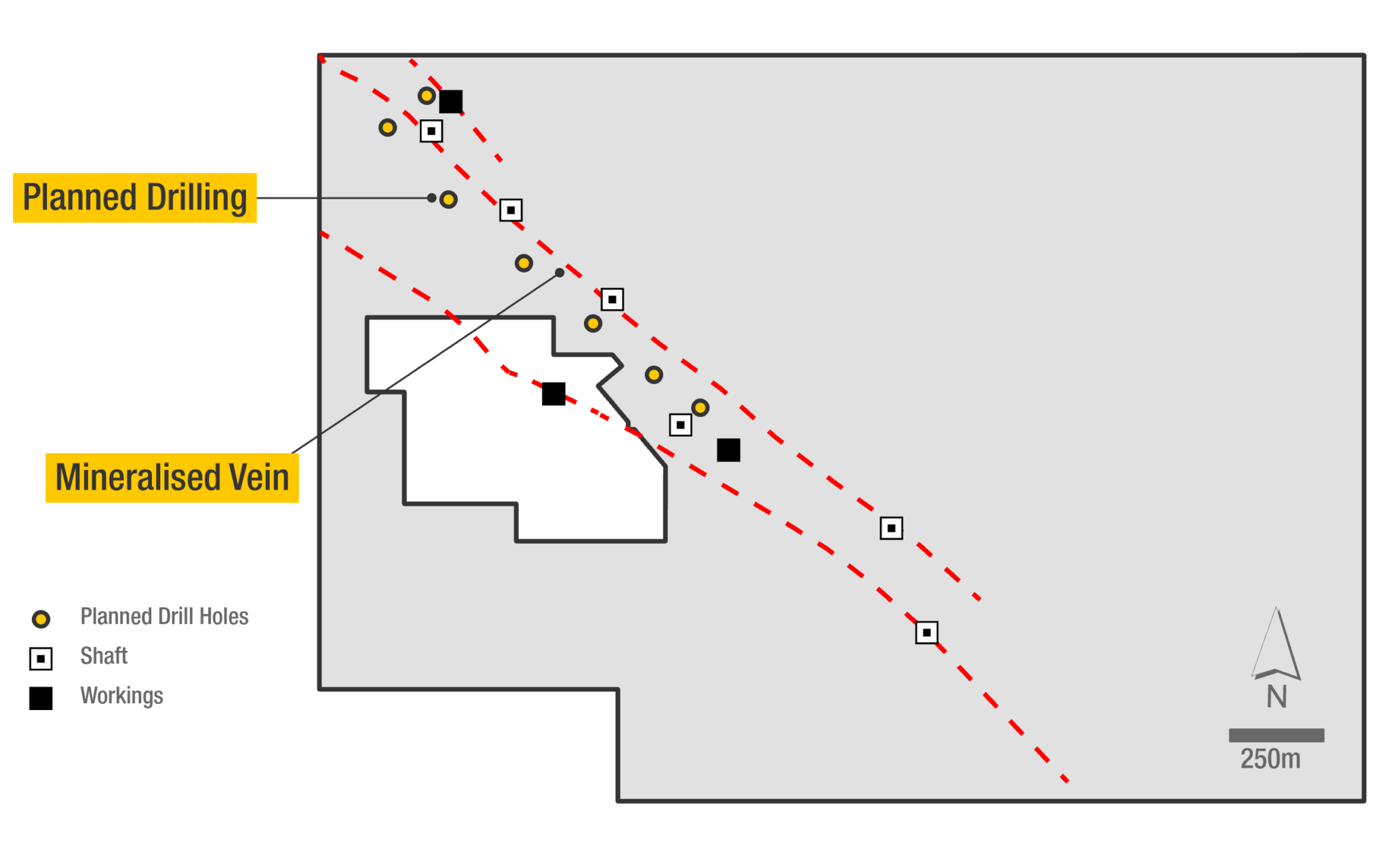

The feedback reportedly identified seven new areas of interest in the magnetic interpretation, which have been ranked for follow-up exploration work, alongside 13 near-surface anomalies, interpreted as possibly either zones of higher vein density or small intrusions.

The company further discovered potential zones of late magnetite destructive alteration throughout areas of lower magnetic response enveloping the inner calc-potassic alteration.

Great Southern Copper also highlighted a possible buried monzonitic intrusive that could represent the parent pluton to the series of mineralised monzonitic dykes and plugs mapped at the surface, with follow-up exploration in the area listed as a high priority due to the relation between the monzonite intrusions and mineralisation noted in other sections of the project.

“The results from the recent ground magnetic survey identified multiple new targets worthy of further exploration and enhances our geological understanding of the San Lorenzo project,” said Great Southern Copper CEO Sam Garrett.

“With ground-truthing of the anomalies and interpretation underway by our team on site, plans are progressing well for the company’s first reconnaissance exploration drilling programme at San Lorenzo.”

“Negotiations with drilling contractors are underway to secure rig availability and we hope to be mobilising a rig to site before the end of June 2022.”