Chinese electric vehicle manufacturer Xpeng (NYSE:XPEV) watched its shares climb by around 25% on Monday, following news that it had made a significant tech announcement, and released a limited-edition model of its P-7 Sedan at the Guangzhou auto show.

Having posted positive earnings last Friday, and seen its shares rise more than 10%, the company also announced that it had produced more than 10,000 of its smart EV P7 models in October. This production announcement was ahead of expectations, and will help cement the company’s credibility versus the likes of competitors such as NIO, Nikola Corp, Lucid, and of course, Tesla.

During the same auto show that it unveiled the limited edition P7 model, Xpeng also announced that it had upgraded its driver-assist tech for its 2021 production models, and they will now feature lidar sensors. These sensors are part of a new system, described by the company as the “next-generation autonomous driving architecture,” featuring cameras, radar, lidar units, a high-grade computer and ultrasonic sensors.

While many automakers already offer hands-free driving technology, Xpeng CEO, He Xiaopeng, said that they are the first company to offer lidar sensors on a production model, and the architecture as a whole will allow users to hands-free driving in low-speed urban settings.

Looking ahead, the future could be bright for the company. Though fears about the risks posed by China’s political makeup are valid, they also assist the EV growth situation. With the country keen to reduce its oil and gas import costs and forecast fossil fuel usage expected to be down 70% by 2030, the future of transport seems to be swinging decisively in favour of electric vehicles.

Chinese EV sales were up by 12.5% year-on-year in October, and there will be hopes that Trump trade war conditions will subside once Biden takes office next January (though BlackRock remain sceptical on this).

Xpeng also benefits from having an ambitious CEO, He Xiaopeng, who sold his last company for $4 billion back in 2014, and, having taken charge of Xpeng back in 2017, now enjoys the backing of e-commerce giant, Alibaba.

What really matters, though, will be whether Xpeng can maintain its growth, or whether it’s just a flash in the pan. Having seen its share price rise from $0.20 to over $66 between September and November, the company is off to a strong start.

We have to stress though, this is just the ‘start’. Performance and projections remain strong, but consumer attitudes can change on a dime (especially in a trendy theme like EVs), and there is always risk when investing in a Chinese company, listed in New York. With that being said – if the company emulates the Tesla or NIO rally, it will be a haymaker for its early backers.

Shares at roadside recovery firm AA plc (LON:AA) were down almost 5% on Monday evening as Sky News reported that the company’s board is set to recommend a private equity takeover to help reduce its £2.6 billion debt mountain.

The motoring group is reportedly being considered for a £218 million takeover proposal from TowerBrook Capital Partners and Warburg Pincus, with both firms offering to pay 35p a share and invest an additional £380 million to put towards paying off AA’s outstanding debt.

To put that into context, when AA first floated the stock market in 2014, its shares stood at 250p and its total share value stood at about £1.4 billion.

According to UK takeover rules, a deal must be reached by 5pm on Tuesday. It is understood that Rick Haythornthwaite – former chairman of British Gas owner Centrica – will chair the AA following the acquisition. He also currently chairs Mastercard and the Creative Industries Federation.

The AA said in a statement to The Guardian:

“The board, having considered carefully the viability of a range of alternative potential debt and equity refinancing options together with its financial advisers, has indicated to the consortium that it would be willing to recommend a cash offer on the terms of the proposal. Accordingly, the company is engaged in advanced discussions with the consortium in relation to the possible offer”.

Across its almost 3 million members, Basingstoke-based AA was launched in 1905 as the Automobile Association and once styled itself as the UK’s “fourth emergency service”. The firm boasts 3,000 patrol vehicles and primarily provides roadside assistance, as well as home and car insurance, and driving lessons.

AA shares were not impressed by the news on Monday, down 4.77% to 31.95p at the market’s close 23/11/2020, although a marked improvement from the company’s annual nadir of just 13.52p during February.

Over the course of the year, shares have taken a 28.46% blow, but recent gains in the past month sent prices up 31.83% again. Its P/E ratio stands at 2.38 and its dividend yield a modest 1.88%.

The price of gold fell nearly 2% to a 4-month low on Monday after better-than-expected U.S. business activity data and optimism over the progress in Covid-19 vaccine development sent investors turning away from their safe haven assets, as hopes mount that a swift economic recovery may be on the horizon.

Spot gold dipped 1.68% to $1,839.73 per ounce, after slipping to its lowest since July 21 at $1,834.95, while U.S. gold futures shed 2% to $1,835.50.

Stock markets bounced on the news that U.S. business activity increased at its fastest rate in 5 years during November, topping even the most rosy forecasts from Reuters, and spurred investors to inch away from gold after a year which saw the precious metal revel in its all-time high during the peak of the pandemic.

Meanwhile, across the pond in the UK, the joint AstraZeneca-Oxford University coronavirus vaccine programme published its first results, showing that their jab can provide upwards of 70% immunity against Covid-19. Investors hoping for it to outdo competitors’ immunity rates were initially disappointed, but news of another victory in the fight against the pandemic continued to buoy markets higher.

Edward Moya, senior market analyst at OANDA, commented on how today’s updates have affected gold prices:

“Gold broke below the key $1,850 level after an unbelievably strong U.S. PMI release just dampened the need for stimulus. No one was expecting such strong readings in both services and manufacturing”.

Weighing in on what this all means for gold in the coming weeks, Axi chief global market strategist, Stephen Innes, explained to Investing.com:

“Despite all the dovish FED waxing, gold is still trying to form a base after the $100 drop two weeks ago on the back of Pfizer vaccine news. Given it has bounced off $1,850 about three times, there should be a fair amount of speculative interest around that level, and it might be safe to assume a sharp move lower should it break.

“There is still a lot of wood to be chopped to take out strategic longs. Those investors hold gold on a more medium-term basis, given considerable fiscal and monetary spending across G10 economies.

“The only short-term potential trigger for a move higher might be the announcement of a new Treasury Secretary by US President-elect Joe Biden, with former Fed chair Janet Yellen being favored at the moment and the restart of discussions regarding a second US stimulus package”.

SMEs with stock offerings that trade under $5 per share are regarded as penny stocks by the SEC (Securities and Exchange Commission) in the US. In the United Kingdom, penny stocks trade at less than £1. These ‘penny stocks’ companies are characterized by low market capitalizations, and their share offerings are usually associated with low trading volumes. Given that they are usually in their infancy stage of development, they don’t have mass market exposure, and they typically fly under the radar.

Penny stocks are often traded over-the-counter (OTC), or as Pink Sheets. This has important ramifications in terms of credibility. Securities and Exchange Commission (SEC) guidelines, and Financial Conduct Authority (FCA) guidelines have strict rules in place vis-a-vis reporting requirements for listed companies. In the absence of listings on the NASDAQ, S&P 500, NYSE, or LSE, traders have to be careful when picking penny stocks. Fortunately, there are 4 different tiers of penny stocks to choose from, most significantly Tier 1 Stocks and Tier 2 Stocks.

An in-depth education is needed to successfully trade penny stocks online. This guide presents several penny stocks to watch for November 2020.

FindIt Inc (OTCPK: FDIT)

The above chart reflects the current demand/supply, and attendant pricing for Findit Inc (FDIT). The stock is currently regarded as neutral, but recent performance has been strongly bullish heading towards the end of November. The company has a low market cap, as indicated by its $13.581 million figure. The stock is currently trading at $0.1150, almost 4 times higher than it started the year ($0.0318) on January 1, 2020. Tremendous volatility was evident heading into October, and again heading into November. Traders ran up the price of the stock to over $0.20 per share, before taking profit.

The charts and patterns reflect this bullish trading activity, and attendant profit-taking. When traders sold off en masse, the price dropped, allowing for additional price action to buy the dip. That caused the price to rally again. The current pricing for FindIt– an app that has been approved for the Google Play Store – as indicated by the Bollinger Bands is neutral. The stock has a 50-day moving average of $0.11, and a longer term 200-day moving average of $0.06. The current Bollinger Bands have a high band of $0.18, a median band of $0.13, and a low band of $0.09. The price is currently a sliver beneath the median band, indicating that it is possibly slightly oversold and ripe for a reversal.

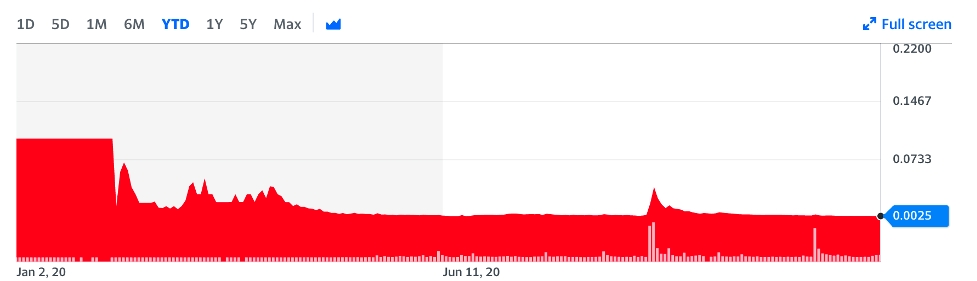

Bantec Inc (OTCPK: BANT)

Bantec Inc is another penny stock that trades OTC. This products & services company manufactures hand sanitizers, and disinfectants. The stock is currently priced at $0.0025 with negligible overall price movement for the year-to-date. There were several periods of volatility over the past month where the stock rallied tremendously. For example, in the final days of October, Bantec stock hit a price of $0.066, which is 2.5 times its current trading price. While miniscule in nominal terms, this huge price percentage appreciation represents a dramatic opportunity for penny stocks traders.

Source: Yahoo Finance

This underscores the importance of percentage appreciation, versus price appreciation. Penny stocks traders who invested $1000 in BANT on October 27 at a price of $0.0031 would have seen the valuation of that stock increased to $0.066 by October 28, before the sell-off and take profit orders were exercised. The initial purchase was the equivalent of 322,580 shares which could have been sold for $0.0066, for a price of $2,129, netting a profit of $1,129.

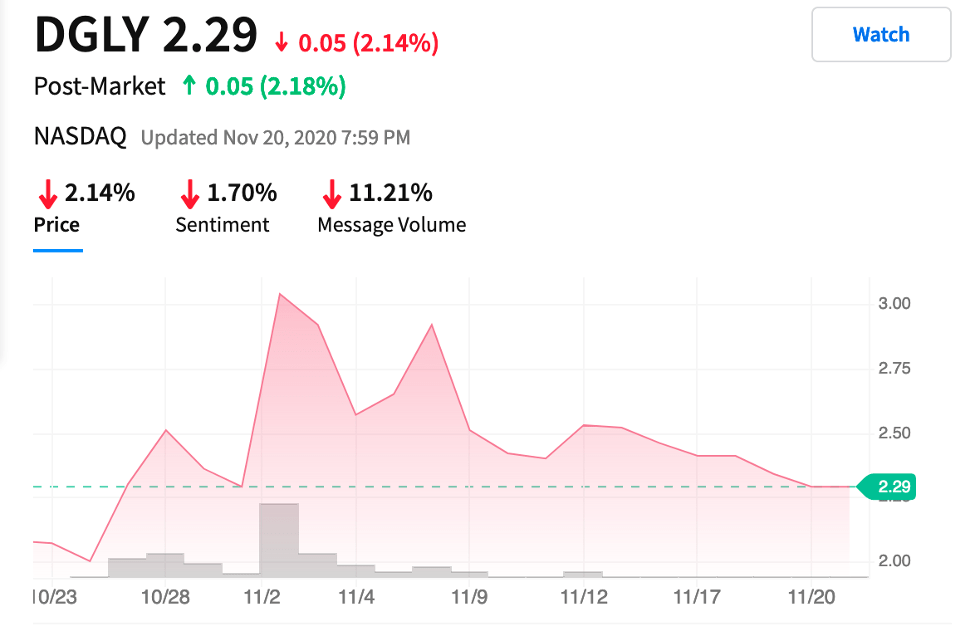

Digital Ally Inc (NASDAQ: DGLY)

Source: StocktwitsDigital AllyIncorporated manufactures body cameras for the police department, among others. The stock is currently trending bearish, as evidenced by the recent downturn since early November. At its current price point ($2.29) it qualifies as a penny stock, and it is listed on the NASDAQ. This automatically places it as a Tier 1 category penny stock since it is subject to stringent reporting requirements. There has been substantial price movement in the stock over the past month, with lows of $1.95 and highs of $3.120. The company’s market capitalization is $61.309M, and the 1-year target estimate is $5.00 per share.

When trading the stock, several important figures need to be assessed, notably the actual earnings versus the consensus earnings. In Q2 2020, and Q3 2020, DGLY beat expectations. This bodes well for bullish trading movements with the stock. The last major ratings upgrade & downgrade by Aegis Capital recommended a buy for this stock. In terms of long-term propositions, with a Biden administration in place, and greater accountability expected of the police force, we can expect demand for DGLY to increase. By the same token, a diminished police presence may act against the stock’s appreciation. It’s too early to tell which way to trade this penny stock, but a buy and hold for the foreseeable future appears to be the consensus.

Note: It is foolhardy to simply accept expert opinions regarding top listings of penny stocks to trade, without conducting your own due diligence. Recommended stocks may be good at the time of writing, but by the time you have read the article, other stocks may be preferred.

Shock, the third Monday in a row where vaccine news push value stocks higher. Though underwhelming, the AstraZeneca (LON:AZN) vaccine trial results shoved long-suffering air travel, financial and commodities stocks higher, once again.

Across the FTSE 100, air travel stocks led the way, with Rolls Royce soaring 7.60%, while IAG bounced around 5.50%. Meanwhile, mining and oil stocks stole the show. While Glencore and BHP rallied 2.37% and 2.25% apiece, BP jumped 3.70% and Shell shares spiked around four-and-a-half percent. Enjoying some progress, too, were financial services equities, with Lloyds rallying 3.87% while Aviva shares increased by 2.08%.

After three weeks of waiting to see where vaccine competitors stand, AstraZeneca’s latest round of results will provide a short boosts ahead of the yet-to-be-published Janssen trial data. For now, IG Senior Market Analyst, Joshua Mahony, goes over the somewhat muted update:

“With AstraZeneca 2% down in early trade, it is evident that markets are somewhat underwhelmed after the largest of the two trials providing just a 70% efficacy.”

“Unfortunately for AstraZeneca, markets have become accustomed to efficacy rates closer to 95% in the wake of the Pfizer and Moderna announcements.”

“While the firm has understandably focused on the 90% efficacy rate seen when a half dose is followed by a full dose a month later, the significantly reduced sample size does provide less confidence in their findings.”

Though a break from lockdown and the reopening of non-essential shops over Christmas has given some a boost, the disappointing AstraZeneca vaccine data has left European equities in a huff as trading came to a close on Tuesday.

Eurozone indexes remained broadly flat, with the DAX down 0.078% while the CAC fell by 0.068%. Meanwhile, the FTSE led the Western losers, falling 0.28% despite positive movements in air travel, financial and commodities equities. Over the pond, the Dow Jones rallied by 0.67%, while the Nasdaq edged lower with a 0.014% loss.

Hit hard during the pandemic, these consumer conglomerates are ideal picks for the old investment adage: buy into what you actually use. And indeed, you’d likely lead a pretty sheltered existence if you hadn’t stumbled across either a Unilever (LON:ULVR) or Diageo (LON:DGE) product.

Using the Warren Buffet philosophy of buying into ‘exceptional companies’ – such as his own Berkshire Hathaway – a doubtful, long-term investor can do little better than tucking money into a company which produces a lot of very popular products. But the question that needs to be asked is – of these, which is best?

Two companies, hundreds of brands

The first area of comparison is their brands, which sectors they operate within, and the forecasts for what these areas look like.

On the one hand, Unilever owns brands across homecare, beauty products and foods and beverages, including: Ben and Jerry’s, Knorr, Dove, Bovril, Carte D’Or, Alberto Balsam, Colman’s, Domestos, Lipton, Cif, Hellman’s, Lynx/Axe, Comfort, Persil, Matey, Magnum, Toni & Guy, Sure, Surf, Pure Leaf, Cornetto, Marmite, Radox, Simple, Solero, TRESemme, VO5, Vaseline, Wall’s, Vienetta, PG Tips, Pot Noodle (etc etc).

In effect, they produce most of the products on your corner shop’s shelves. While sales have been ahead of target during 2020, uncertainty has continued to weigh on the company’s share price. Though, while tight purses might affect the extent of purchases in non-essential consumables, a lot of Unilever products in beauty and homecare will be viewed as shopping basket staples, and therefore would likely not be hampered too greatly, even in a COVID risk worst-case-scenario.

On the other hand, we have the alcoholic beverages-specialised Diageo, which owns brands such as: Black & White, Johnnie Walker, J&B, Lagavulin, Singleton, Talisker, and Crown Royal whiskies; Ciroc, Ketel One, and Smirnoff vodkas; Bundaberg, Captain Morgan, and Ron Zacapa rums; Gordon’s and Tanqueray gins; as well as prolific names such as Don Julio tequila, Baileys liqueur and Guinness beer.

With the international closure of hospitality outlets across the world, out-and-about alcoholic beverage sales have been absolutely hammered during 2020. With this painful fall, there are two avenues to consider going forwards. Following its recent share price dip, we might conclude that COVID risk factors will likely prevail until a vaccine is rolled out effectively – and will continue to weigh on sales. On the other hand, shares rallied in early November, and we might imagine that between being among the worst-affected sectors by the virus, and the pent-up demand for socialising and holidaying, the outlook for Diageo could be promising. Indeed, hopes of normality returning aside – Christmas is coming, and we have to consider how much holiday booze demand has already been priced in by the market.

Which one offers better value?

The second comparison should be on each company’s price, value and income potential.

In terms of share price, both companies have been broadly moving upwards since the start of the first COVID lockdown, with both falling slightly on Monday, with Unilever down 1.68% and Diageo falling 0.91%, to 4,381p and 2,920p respectively.

Analysts have a consensus ‘Hold’ stance on Unilever stock, with 6 Buy, 2 Hold, and 3 Sell stances. Similarly, the company has a consensus target price of 4,819.55p (around a 10% potential increase), with highs of 5,411p from Goldman Sachs analysts and lows of 3,814p courtesy of HSBC – both quoted in October.

Meanwhile, analysts also have a ‘Hold’ stance on Diageo stock, with 10 Buy, 6 Hold and 2 Sell stances. Its consensus target price is 2,969p, some 1.7% up from its current level and contrasting Goldman Sachs’ November target projection of 3,200p, and UBS’ September projection of 2,800p.

In terms of which is better, Diageo received a 56.64% ‘outperform’ prediction from the Marketbeat community, versus Unilever’s 52.27% ‘underperform’ vote share. However, each company has appeared in seven research reports over the last three months – which suggests high interest in both – while Unilever insiders have sold none of the company’s stock in the last ninety days, whereas Diageo insiders sold 1,153% more of the company’s stock than they bought.

This follows Diageo’s recent share price uptick, where it bounced around 530p. And, while selling off stock to capitalise on a boom isn’t inherently negative, it does suggest that insiders found short term maximisation more worthy than the company’s price prospects in the short-to-medium-term. Meanwhile, at its lowest since the start of the month, Unilever stock has been described by many on forums as a bargain.

In terms of value, Unilever also outperforms Diageo. Its p/e ratio of 17.44 is still above the consumer defensive average of 11.49, but far far below Diageo’s 48.99 score.

The story is much the same in terms of income. Unilever boasts a 3.42% dividend yield and a pay-out ratio of 59.27%. Being below 75% or so, this rate stands at a healthy and sustainable level. In contrast, Diageo has a dividend yield of 2.40%. Not shabby, but its pay-out ratio of 116.86% isn’t ideal, as it may be too high to be sustainable – and relied upon.

A mind towards posterity

Our final consideration, which is natural when thinking of a long-term holding, is future strategy and product considerations. In reality, both companies excel in innovation, with both featuring highly trendy brands who capitalise on consumer whims and cultural events.

For instance, Unilever’s Ben & Jerry’s creates new flavours to tap into contemporary tropes (such as Netflix and Chill’d), and performs vocal advocacy on issues such as climate change, BLM and the migrant/refugee crisis (not interchangeable, just depends on the viewer). Meanwhile, Diageo is hardly slacking, having launched the Johnnie Walker ‘White Walker’ to mark the Game of Thrones finale, along with new gin flavours, no-ice-needed Baileys, and a fruit-based Ketel One variety, to adapt with changing consumer taste trends.

In terms of their commitments to sustainability, both companies have set clear targets, with Diageo pledging to be carbon neutral by 2030, while Unilever has for some time reported on its sustainability initiatives, and now targets $1.2 billion in plant-based sales by 2025.

Likely the more ambitious in terms of sustainability goals, Unilever’s push for greener mass production is positive overall – with sustainability being an increasingly factored-in part of the investment process. However, it will alienate some who view this kind of overt messaging to be contrary to their own views – or, ‘virtue signalling’.

Out of the two companies, I’d favour Unilever. Its recovery may not be as dramatic as the one Diageo saw a couple of weeks ago (and may yet see), but its current entry point is comfortable versus where it is expected to move over the coming years. Similarly, it’s less overvalued, pays a bigger dividend and seems to be more decisive in its green transition.

For full disclosure, the author has a holding in Unilever, but this was only after beginning to carry out his research into different consumer defence equities.

Connells has confirmed a £82m takeover bid for Countrywide.

The estate agent chain said on Monday morning that it would offer 250p per share in cash.

David Livesey, Connells group chief executive, said: “Countrywide shareholders have repeatedly been promised jam tomorrow and it has never been delivered.

“There is no quick and easy fix. Turning the business around, especially in unpredictable market conditions, will be a difficult, expensive and lengthy process.

“Countrywide needs new ownership, not yet another speculative scheme that is based on hope rather than experience.

“Our proposal gives Countrywide shareholders significant immediate upside in cash, at a 72 per cent premium to the undisturbed price, with none of the downside risks of remaining independent.”

Connells has also said that without this offer, Countrywide is likely to “enter administration without a significant capital injection.”

The firm offer is now subject to the approval of the board and shareholder support.

Shares in the estate agent group (LON: CWD) rocketed almost 8% on the news and are currently trading at 233,20 (1443GMT).

With the UK suffering more than most at the hand of the COVID pandemic – and watching its GDP shed 19.8% during the second quarter – it appears only natural that investors are chomping at the bit, and trying to climb aboard the British economic recovery train. Having displayed some optimism following Pfizer and Moderna vaccine news, global equities ended last week in something of a consolidation phase. With that in mind, here are three fund picks to help you capitalise on any prolonged UK recovery – if and when vaccines are successfully rolled out.

BlackRock’s UK Trust remains hungry for growth

Our first offering is the BlackRock Throgmorton Investment Trust (LON:THRG), which offers less on the value-for-money and income side but offers plenty in the way of growth potential.

Delivering less on the cost-effectiveness side, BlackRock Throgmorton’s price versus NAV trades at a 2.7% premium, while its yield is the most modest of our picks at 1.49% and its ongoing charges figure middles at a rate of 0.59%.

What this fund really does deliver on, though, is aggressive and highly active equities trading. Indeed, as the company states in its bio:

“The BlackRock Throgmorton Trust looks to back the UK’s strongest emerging companies. An unusual feature of the Trust is its ability to ‘short’ companies that we find unattractive, enabling us to profit if the share price falls. This gives the Trust’s manager the opportunity to back investment ideas with real conviction, within a strong risk framework.”

Trading 212 describes the investment trust as having around 30% of its assets held in CFDs or comparable equities derivatives at any one time, allowing it to both enjoy the rallies of its constituent stocks, and profit by hedging against their dips.

With this tactic, the fund has enjoyed consistent and impressive over every timeframe. Over the last year, its stock has posted a 11.6% jump; following a 55.3% bounce over the past three years; and a 128% hike over a five-year period.

At present, the company looks to be among the more attractive candidates in the IT UK Smaller Companies sector. Their shares are trading for 688.00p apiece, and their top holdings are Gamma Comms (2.8%), YouGov (2.6%), Games Workshop (2.6%), Avon Rubber (2.5%), Watches of Switzerland (2.5%).

JP Morgan-advised veteran offers good value

At the other end of the spectrum, the JP Morgan-advised Mercantile Investment Trust (LON:MRC) offers decent price growth and earnings and value potential.

Launched back in 1884, the veteran investment trust offers a price to NAV discount rate of -2.10%, a yield of 2.86% and an ongoing charges figure of 0.44%. All of these fundamentals are the best for income and value out of our three picks – and while not the best you’ll find on the IT UK market as a whole, they’re respectable among funds that rank within the upper echelons of most factors taken into consideration.

With the income and cost potential in mind, you’d almost consider riding out some rough equities valuations in the near-term, as Mercantile Investment Trust says in its commentary:

“Geopolitical concerns are likely to drive continued market volatility as the closely contested US election draws to a protracted conclusion and as Brexit negotiations intensify.”

“From a valuation viewpoint, the case for equities remains compelling. Short-term hits to profitability need to be balanced against the potential for medium-term recoveries.”

With that being said, the fund hardly boasts weak growth. With its price up by 3.2% over the last twelve months, Mercantile has also seen its share price rise 20.9% in the last three years, and a healthy 53.2% in the last five years.

At present, the trust’s shares are trading for 229.00p. Its holdings are topped off by pandemic victors Games Workshop (3.4%), alongside Computacenter (3.3%), Bellway (3.1%), Softcat (2.8%), Intermediate Capital (2.6%).

The fund with the inviting equities picks

Receiving a five-star rating from trustnet and a risk score of 95 (meaning it has a lower risk profile than the UK’s top 100 shares), the FTSE 250-listed Finsbury Growth and Income Trust (LON:FGT) boasts decent income alongside an impressive roster of investments.

Though costly with a 0.66% ongoing charges figure, the fund boasts a -0.70% discount rate, a 1.93% yield and 65.7% growth over the last five years.

More impressively, though, Finsbury may be perfectly positioned to capitalise on the recoveries of some of the hottest UK companies. For instance, its top holding is in the London Stock Exchange (11.70%), followed closely by Unilever (10.80%), which is currently trading at a bargain price, while being described by The Motley Fool and Yahoo Finance as a ‘world class company’. Similarly, 6.40% of its holdings are in The Sage Group, which suffered a 13% hammer-blow at the end of last week.

Further, as the UK exit lockdown in the new year, the hope is that housebuilding and hospitality (as well as industrial activities) will have scope for a resurgence. Should the former two sectors manage to expand on their current activity levels, this would benefit the company’s holdings in property developers, Schroders (6.80%), and alcoholic beverage conglomerates, Diageo (9.50%) and Remy Cointreau (5.40%), respectively.

Starting the week at a ten-day low and down by 0.8% during the last twelve months, the Finsbury Growth and Income Trust could position investors well to capitalise on the hopeful (if gradual) UK recovery, and return to normality.

Shares at the world’s second-largest cinema chain, Cineworld (LON:CINE), have rocketed more than 22% on the back of the news that the firm has secured waivers for its debt deadlines until June 2022 and £336 million in new loans to help see it through the remainder of the pandemic.

Last week, Cineworld shares took a tumble amid rumours that the chain was seeking a CVA to take the pressure off its mounting debt crisis – with more than £6 billion owed to creditors and a half-year loss of £1.3 billion due to a fatal combination of global lockdown measures and a near-paralysis of new blockbuster releases.

The chain temporarily closed all of its UK and US sites back in October, but has said that today’s move will provide Cineworld with “financial and operational flexibility until lockdown restrictions in key jurisdictions are eased and studios are able to bring their enhanced pipeline of major releases back to the big screen”.

Among the new terms are equity warrants worth around 11% of its share capital, debt measures set to give the company over £233 million of extra liquidity, and reduced monthly cash spend to around £45 million.

Cineworld also extended its £83 million incremental revolving credit facility from December 2020 to May 2024, as well as pulling forward an expected tax refund of more than £150 million to early 2021.

Mooky Greidinger, chief executive at Cineworld, welcomed the chain’s news:

“Over the long term, the operational improvements we have put in place since the start of the pandemic will further enhance Cineworld’s profitability and resilience.

“The group continues to monitor developments in the relevant markets in which we operate and our entire team is focused on managing our cost base.

“We look forward to resuming our operations and welcoming movie fans around the world back to the big screen for an exciting and full slate of films in 2021″.

News of Cineworld’s debt waiver sent shares at the company soaring 22.37% at lunchtime on Monday 23/11/20, up to 56.40p, following on from an extremely turbulent year which saw prices crash to an annual low of 15.64p in March.

Recent weeks have seen its share price edge higher, up 42.45% in the last month, as combined vaccine development efforts fuel the cinema industry with hope that a post-pandemic world may be on the horizon.

Analysts at Investec (LON:INVP) commented on Cineworld’s news, stating:

“With vaccine development progressing, this should give investors significantly greater confidence in Cineworld emerging from the crisis, allowing the company to capture demand as it returns with a robust slate of postponed films.

“Although recent changes to the theatrical window by peers have captured industry headlines, we continue to believe those will have limited impact on industry box office revenues overall”.

Shares at Cambridge-based pharmaceuticals firm AstraZeneca (LON:AZN) have slid over 1% on Monday morning despite the news that their coronavirus vaccine, in collaboration with Oxford University, has proven to be up to 90% effective in interim trial data.

Initial results showed the first half dose is able to provide 70% protection against the virus, but a secondary full dose of the vaccine saw immunity rise to 90% – suggesting that the dosage of the first jab primed the immune system significantly from just half of the full dose.

Additional data also indicated that the AstraZeneca-Oxford vaccine helps to prevent the spread of coronavirus in asymptomatic patients, after researchers reported a drop in transmission amongst those with no symptoms.

Clinical trials so far show the vaccine to be safe, with only minor complaints of sore arms and fever among patients – not unusual after immunisation of any kind. A database of more than 24,000 volunteers across the UK, Brazil and South Africa found no major concerns.

While the 70% effectiveness results may have left investors feeling disappointed, following last week’s news of the Pfizer and Moderna jabs providing up to 95% protection, the AstraZeneca-Oxford vaccine is far cheaper to produce and to store than its trans-Atlantic counterparts – needing only normal refrigerator temperatures.

The UK government has already pre-ordered 100 million doses in preparation for a mass rollout as soon as the vaccine is widely available, while AstraZeneca has pledged to provide 3 billion doses for global use over the course of next year.

“The announcement today takes us another step closer to the time when we can use vaccines to bring an end to the devastation caused by [the virus],” said Oxford’s Professor of Immunology, Sarah Gilbert.

UK Prime Minister Boris Johnson has also welcomed the “incredibly exciting news”, and despite the additional safety checks before the vaccine can hit the market, he has hailed the “fantastic results” as an early victory against the pandemic.

Nevertheless, shareholders appear to have taken news of the 70% efficacy at face value, with AstraZeneca shares slipping 1.76% to 8,171.00p at midday, following on from a week-long downward trajectory of 3.96% – likely a reaction to competitors’ vaccines speeding ahead.

The company has a P/E ratio standing at 22.4, with a prospective dividend yield over the next 12 months of 2.6%.

The above chart reflects the current demand/supply, and attendant pricing for Findit Inc (FDIT). The stock is currently regarded as neutral, but recent performance has been strongly bullish heading towards the end of November. The company has a low market cap, as indicated by its $13.581 million figure. The stock is currently trading at $0.1150, almost 4 times higher than it started the year ($0.0318) on January 1, 2020. Tremendous volatility was evident heading into October, and again heading into November. Traders ran up the price of the stock to over $0.20 per share, before taking profit.

The charts and patterns reflect this bullish trading activity, and attendant profit-taking. When traders sold off en masse, the price dropped, allowing for additional price action to buy the dip. That caused the price to rally again. The current pricing for FindIt– an app that has been approved for the Google Play Store – as indicated by the Bollinger Bands is neutral. The stock has a 50-day moving average of $0.11, and a longer term 200-day moving average of $0.06. The current Bollinger Bands have a high band of $0.18, a median band of $0.13, and a low band of $0.09. The price is currently a sliver beneath the median band, indicating that it is possibly slightly oversold and ripe for a reversal.

The above chart reflects the current demand/supply, and attendant pricing for Findit Inc (FDIT). The stock is currently regarded as neutral, but recent performance has been strongly bullish heading towards the end of November. The company has a low market cap, as indicated by its $13.581 million figure. The stock is currently trading at $0.1150, almost 4 times higher than it started the year ($0.0318) on January 1, 2020. Tremendous volatility was evident heading into October, and again heading into November. Traders ran up the price of the stock to over $0.20 per share, before taking profit.

The charts and patterns reflect this bullish trading activity, and attendant profit-taking. When traders sold off en masse, the price dropped, allowing for additional price action to buy the dip. That caused the price to rally again. The current pricing for FindIt– an app that has been approved for the Google Play Store – as indicated by the Bollinger Bands is neutral. The stock has a 50-day moving average of $0.11, and a longer term 200-day moving average of $0.06. The current Bollinger Bands have a high band of $0.18, a median band of $0.13, and a low band of $0.09. The price is currently a sliver beneath the median band, indicating that it is possibly slightly oversold and ripe for a reversal.

The above chart reflects the current demand/supply, and attendant pricing for Findit Inc (FDIT). The stock is currently regarded as neutral, but recent performance has been strongly bullish heading towards the end of November. The company has a low market cap, as indicated by its $13.581 million figure. The stock is currently trading at $0.1150, almost 4 times higher than it started the year ($0.0318) on January 1, 2020. Tremendous volatility was evident heading into October, and again heading into November. Traders ran up the price of the stock to over $0.20 per share, before taking profit.

The charts and patterns reflect this bullish trading activity, and attendant profit-taking. When traders sold off en masse, the price dropped, allowing for additional price action to buy the dip. That caused the price to rally again. The current pricing for FindIt– an app that has been approved for the Google Play Store – as indicated by the Bollinger Bands is neutral. The stock has a 50-day moving average of $0.11, and a longer term 200-day moving average of $0.06. The current Bollinger Bands have a high band of $0.18, a median band of $0.13, and a low band of $0.09. The price is currently a sliver beneath the median band, indicating that it is possibly slightly oversold and ripe for a reversal.

The above chart reflects the current demand/supply, and attendant pricing for Findit Inc (FDIT). The stock is currently regarded as neutral, but recent performance has been strongly bullish heading towards the end of November. The company has a low market cap, as indicated by its $13.581 million figure. The stock is currently trading at $0.1150, almost 4 times higher than it started the year ($0.0318) on January 1, 2020. Tremendous volatility was evident heading into October, and again heading into November. Traders ran up the price of the stock to over $0.20 per share, before taking profit.

The charts and patterns reflect this bullish trading activity, and attendant profit-taking. When traders sold off en masse, the price dropped, allowing for additional price action to buy the dip. That caused the price to rally again. The current pricing for FindIt– an app that has been approved for the Google Play Store – as indicated by the Bollinger Bands is neutral. The stock has a 50-day moving average of $0.11, and a longer term 200-day moving average of $0.06. The current Bollinger Bands have a high band of $0.18, a median band of $0.13, and a low band of $0.09. The price is currently a sliver beneath the median band, indicating that it is possibly slightly oversold and ripe for a reversal.

Bantec Inc is another penny stock that trades OTC. This products & services company manufactures hand sanitizers, and disinfectants. The stock is currently priced at $0.0025 with negligible overall price movement for the year-to-date. There were several periods of volatility over the past month where the stock rallied tremendously. For example, in the final days of October, Bantec stock hit a price of $0.066, which is 2.5 times its current trading price. While miniscule in nominal terms, this huge price percentage appreciation represents a dramatic opportunity for penny stocks traders.

Bantec Inc is another penny stock that trades OTC. This products & services company manufactures hand sanitizers, and disinfectants. The stock is currently priced at $0.0025 with negligible overall price movement for the year-to-date. There were several periods of volatility over the past month where the stock rallied tremendously. For example, in the final days of October, Bantec stock hit a price of $0.066, which is 2.5 times its current trading price. While miniscule in nominal terms, this huge price percentage appreciation represents a dramatic opportunity for penny stocks traders.