Boohoo (LON: BOO) saw profits soar 53% in the six months to 31 August.

Despite the pandemic and factory scandal, the retailer’s revenue grew to 45% to £816.5m from £564.9m in the same period a year earlier.

The boost in profits and sales around the world for Boohoo comes at an interesting time. The allegations of the factory warehouse in Leicester led to a backlash among MPs, the general public, and the industry.

The fashion retailer published an independent report on its suppliers in Leicester, accepting supply chain criticisms and causing the share price to recover.

Despite the scandal, Boohoo has reaped the benefits of the shift to online shopping during the pandemic.

“Our business, along with many others, has faced some of its most challenging times in recent months: the onset of the pandemic meant we had to adapt our operations with nearly all office-based colleagues working from home; we introduced new ways of working safely in our distribution centres; and we have comprehensively investigated reports on concerning and unacceptable working practices in our Leicester supply chain,” said John Lyttle, the chief executive.

“There are many challenges still ahead due to uncertainties posed by the COVID-19 pandemic, but despite these challenges there are many positives from our activities in the first half. The resilience of our business model and the commitment and flexibility of our colleagues and partners has enabled us to continue to operate our business successfully.

“We are grateful to all and pleased to be able to report a strong performance with continued high growth rates in revenue and strong profitability. We also acquired two new well-known women’s brands, Oasis and Warehouse, and we acquired the remaining minority interest in PrettyLittleThing, all of which will support our continued growth and profitability.”

Boohoo has upgraded its revenue growth targets from 25% to 28%-32% for the full year. Shares (LON: BOO) jumped 3% in early trading.

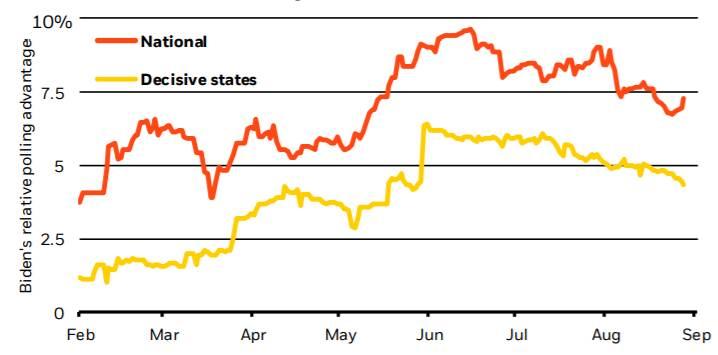

With BlackRock (NYSE:BLK) having stated that Joe Biden remains ahead in national polling, data from marginal electoral states suggests that the gap has been closing ever since June – when concerns over the Trump administration’s handling of Covid-19 were at their peak. With some of that momentum having died off in recent weeks, however, two key revelations within the last couple of days might see the tide once again swing in the Democrats’ favour, just days out from the election.

BlackRock Investment Institute, with data from FiveThirtyEight.

Trump taxes, or lack thereof

The first of these revelations was the publication of President Trump’s income taxes by the New York Times on Monday. The reveal, while hardly surprising, puts the incumbent POTUS in something of a logical bind. Either, he accepts that he is a terrible businessman – which his $421 million in loans and debt might corroborate – and therefore not fit to run the largest economy in the world. Or, more likely, his $750 in income tax reveals, much like his famous draft-dodging, that his patriotism is entirely empty rhetoric.

While he might blow the horn of US nationalism, and tout ‘America First’, the reality is that the US as a society comes fairly far down on Trump’s priority list – perhaps somewhere behind his $70,000 on hairstyle expenses. The bottom line is this: he relies on the support of Americans who are proud of their country, without having much regard for it himself. And, while public services remain underfunded, and trust in public institutions remains fraught, we must all conclude that Trump himself embodies the very worst part of the elite he so often castigates.

Decades of tax information that President Trump has tried to hide from the public provides a detailed view of his business career, revealing huge losses, looming financial threats and a large, contested refund from the IRS. https://t.co/9dMTyjE15cpic.twitter.com/sDkQR56swu

Cambridge Analytica scandal – no man of the people, just a man who thinks little of the people

The second, and perhaps more damning revelation, though, was the recent breakthrough on Cambridge Analytica data – and the fact that the 2016 Trump campaign had relied on Cambridge Analytica’s psychographics to shape voter behaviour. While news that the Vote Leave campaign had used Cambridge Analytica’s data services to manipulate voters in a similar way, might have had little impact in the UK, this latest breakthrough might have greater significance in the US for a few reasons.

“I think every voter has a right to see this. It’s crazy that we don’t have the right to see this.”@profcarroll asked for Cambridge Analytica to release the information they held about him.

First, psychographics are a dossier of a person’s personality and psyche, built on myriad data about online transactions, interactions and opinions. And, while an Orwellian thought for most, what makes this subject particularly sensitive in the US, is that American citizens don’t yet have the right to access their own psychographics dossier. Therefore, data about who they are is being used to manipulate their decision-making at crucial junctures, by whoever has the money to pay for said data, and they are not even aware of what the data says about them.

Secondly, Trump is on record, promising that such tactics had not been used. Not only does such manipulation and control completely contravene – and undermine – much of the rhetoric he has spouted against the Democrats (namely that their policies encroach on people’s freedoms), but perhaps represents one of the most disturbing lies of his presidency. ‘I’m here to protect your freedoms from the clutches of the nasty liberal elite – except I’m even worse’ – or something to that effect.

Third, is the timing of this latest revelation. Not only has this scandal broken onto the (at least UK) news cycle just hours out from the first presidential debate – it is also an election scandal, only days out from election day. With all of Trump’s vitriol against postal votes, the potential for legal challenges and the POTUS even threatening to squat in the Whitehouse in the event that the vote doesn’t go his way, the Cambridge Analytica leak by Channel 4 News really should tell voters that he is the wolf in sheep’s clothing.

Whether or not swing voters accept these damning breakthroughs, or whether they’ll be seduced by the Trump ‘stitch-up’ narrative, has yet to be seen. However, just hours out from the beginning of the main election coverage, these revelations couldn’t have come at a better time for team Biden, and might prove costly for team Trump.

Hotel Chocolat (LON:HOTC) made a slightly better than expected profit last year, but the chocolate maker and retailer is likely to lose money this year. Online demand has increased by 150% so far this year.

In the year to June 2020, Hotel Chocolat made an underlying pre-tax profit of £2.4m, down from £14.1m, on revenues 3% ahead at £136m. Second half revenues fell by 14% - reflecting disruption to Easter trading. There is growth in online sales, and they will remain more important than in the past. This indicates the strength of the brand.

VIP members increased by 50% to 1.3 million. Managemen...

Digital TV technology developer Mirada (LON: MIRA) has provided technology to its first major TV service in Europe. This could help it to build up revenues on the continent.

Spain-based Mirada has provided its Iris technology for Zapi, a new digital pay TV platform launched by Plataforma Multimedia de Operadores (PMO). The Iris technology has been used in the Americas, but this the largest contract in Europe so far.

Iris can be used to provide services across all major TV set top boxes and devices. It can integrate services, such as Netflix.

The majority of group revenues have been coming from Mexico and other South American companies. Asia has also been a greater contributor than Europe. Spain will provide a reference for other potential clients in Europe.

Income

Clients like the choice of paying upfront for technology and licences or spreading the cost with a Software-as-a-Service type deal. By its nature the first type of revenues is likely to be more lumpy than SaaS, but there tends to be some revenues from this source each year. Those deals also generate recurring maintenance income.

The deal with PMO is one with an upfront payment plus income from user licences when customers are signed up. PMO expects subscribers to reach 600,000. That means that there will be licence income over the period that these users are signed up, which will be well past the end of this financial year. Even a few dollars per licence would generate a significant income.

Financials

Mirada increased continuing revenues by 13% to $13m in the year to March 2020 and it generated cash. Work was carried out on deployments that should yield growing licence and managed services revenues in the future.

Capitalised development spending was $4.3m last year and this was partly financed by the cash generated from operations and the £2.12m raised from the sale of a non-core business. Net debt was $5.1m at the end of March 2021 and a loan from the major shareholder has been extended to November 2021.

Lockdown has led to increased consumption and take up of TV services, but there were worries that it could delay the finalisation of contracts. The latest launch in Spain and the previous announcement of a service launch in the US Virgin Islands shows that work has been completed on contracts that were previously won.

Interim figures will be published during November. There will be some revenues from the Spanish deal, but there should be a greater contribution in the second half and the following year.

With sustainability becoming an increasingly significant consideration for discerning investors, being able to differentiate between true sustainability and merely a green veneer – or, ‘greenwashing’ – will become increasingly important as time goes on. That is why Tribe Impact Capital wants investors to know the risks of relying on ESG (Environmental, Social and Governance), and how a promising acronym might just be another way of pulling wool over consumers’ eyes.

According to the Tribe analysis, ESG has become a ‘powerful framework’ for businesses to consider their operational risks by using a shared language, and to provide shareholders and lenders with a gauge of the extent to which companies identify and mitigate against these risks.

However, despite encouraging steps in the right direction, and introducing sustainability vocabulary into corporate discourse, a major problem with ESG data sources is that the consumers are led to believe assertions of ‘sustainability’, ‘responsibility’ and ‘impact’ often provided by a singular piece of publicly available information.

According to Tribe, ‘genuine sustainability’ requires engagement with a business’ products, services and history, and needs to be based on data from multiple sources and specialists.

Indeed, if we look at oil and gas blue chip, Shell (although you could pick many), the company posts ESG reports, yet its operations are anything but sustainable or ethical. Indeed, even after undergoing seemingly radical CSR reforms, its operations in Nigeria remain the subject of regular controversy.

Between providing funding for munitions to suppress protestors (as declared in US Embassy cables in 2006); to being complicit in a $1.1 billion bribery arrangement in 2011 (as reported by global witness); tax irregularities valued at $1.67 billion between 2004 and 2012 (ActionAid); and 1,010 official oil spills between 2011 and 2018 (Amnesty), One might think of RDS as a prolific offender.

What makes Shell so interesting, though, is that their CSR initiatives are often touted as some of the best in the oil industry, and that should give us some sense of why using cheery acronyms, such as ESG, is often misleading. According to Tribe’s statement:

“Over the last few years we have seen examples of businesses that would never be recognised as responsible or sustainable, due to certain business practices identified in the impact due diligence process, appearing in active and passively managed funds under an ESG banner across sectors. From the financial sector – a bank getting exemplary scores for governance yet investing billions of dollars into Tar Sands exploration businesses for example, to within the clothing retail sector – where large gaps in data and scrutiny on both the environmental and social impact of production were overlooked.”

“Problems then arise in both hoped-for impact and financial returns. This misrepresentation is misleading to investors and opens them up to the exact risks they were seeking to protect themselves against with a sustainable investment strategy. It is therefore critical investors don’t fall into the trap of taking too much comfort from ESG data’s protective blanket and failing to interrogate a business’ strategy in a more holistic manner.”

The solution Tribe would suggest to this dilemma, would be a greater focus on impact investment. In Tribe’s investments, they focus on businesses working to affect positive change, and they use the UN’s 2015 Sustainable Development Goals as a framework to guide their efforts. Or, as Tickr Co-Founder, Tom McGillicuddy, put it: investing in companies with a business model built around creating a positive impact.

Another solution is put forward by the Temple Bar Investment Trust Director, Dr Lesley Sherratt, who suggests that another way to make companies more sustainable is by institutional investors moving the goalposts of what can be considered Responsible Investment. Using this approach, Sherratt appreciates the majority stake that the likes of pension funds and investment trusts have in buying shares, and states that if they were to apply more limited but demanding criteria, then companies would be obliged to change their business models, in order to be eligible for Responsible Investment portfolios.

With the FTSE 100 dominated by overseas dollar earners, we see exposure to the UK’s smaller companies as the best way to position for a recovery in the UK economy.

The below trusts satisfy the mandate with a range of exciting UK-listed companies, many of whom flourished during the COVID-19 restriction period.

BlackRock Throgmorton Trust

The ‘high-conviction’ BlackRock Throgmorton Trust is managed by Daniel Whitestone who heads up BlackRock’s Emerging Companies team.

The Throgmorton Trust seeks out companies ‘with strong management teams, strong and dominant market positions’ as well as those that be classes as ‘disruptors’.

Top holdings include companies such Serco Group, YouGov, Dechra Pharmaceuticals, Games Workshop and Gamma Communications.

Games Workshop is a particular stand out after the model and games company announced a significant shift to online sales during the COVID-19 lockdown which is likely to help margins on the other side.

Gamma Communications is a holding that certainly satisfies the ‘disruptor’ element of the portfolio with its multi channel communications offering. Gamma enjoyed a 12% increase in revenue in the first half.

The fund interestingly notes that it uses CFDs to profit from falls in the share prices of companies. This typically higher risk activity can utilise leverage and provide protection against volatility in equity markets.

As at 30th June the trust had 3.9% of the portfolio allocated to various short positions.

This strategy appears to have paid off with BlackRock Throgmorton Trust up 95.9% over the past 5 years making it one of the best performing UK Small Companies Trusts.

JPMorgan Smaller Companies Investment Trust

The attraction to the JPMorgan Smaller Companies Investment Trust stems largely from the trusts focus on the UK consumer. However, with a backdrop of COVID-19 causing concerns about consumer confidence in the short-term, we see strength in the trusts exposure to specialist consumables.

The trust again holds Games Workshop whose inelastic demand from enthusiasts is unlikely to see any major problems in the near term.

It also holds Future plc, the specialist media company who commands loyal communities of users and readers with titles such as FourFourTwo, Horse & Hound and the official magazines for Xbox and Playstation. Specialist titles such as these provide contextual opportunities for advertisers meaning Future can see step much of the reduction in advertising spend associated with newspapers and more general publications.

Other consumer companies such as Dunelm and Pets at Home also fall into the specialist sector but retail exposure may mean the market asks questions of the shares going forward.

With a 14% discount to NAV, JPMorgan Smaller Companies Investment Trust provides an attractive exposure to growing UK companies that have taken COVID-19 in their stride.

FTSE 100 listed heating and plumbing distributor, Ferguson plc (LON:FERG), saw its shares rally almost 7% on Tuesday, on news that it had reinstated its dividend.

The news came as part of its otherwise understated full-year results for the period ended July 31. Revenues were down by 0.9% year-on-year, falling from US$22.01 million to US$21.82 million. Meanwhile, its profits took a more notable hit, down by 4.8%, from US$1.32, to US$1.26 million.

This subdued trend looked to be reflected in its shareholder’s situation, with basic earnings per share falling 11.2%, to 427.5c. However, the company announced it would be reinstating its dividend at 208.2c a share – the same level as in 2019 and 2018.

The Ferguson statement noted that the decision to reinstate the dividend had been made due to the Group’s prospects and ‘strong’ financial position.

The company added that prior to its activity being paused in March, it invested $351 million in six acquisitions.

Ferguson response

Speaking on the update, company Chief Executive, Kevin Murphy, commented:

“We have delivered a strong performance in 2020, which given the global pandemic has highlighted the resilience of our business model. Early in the crisis we moved decisively to protect the health and wellbeing of our associates while continuing to serve our customers supporting critical infrastructure. We have rapidly adjusted our ways of working to adapt to this new operating reality while taking action to lower the cost base. We have also managed working capital and capital expenditure which alongside the strong profit delivery has led to an excellent cash performance.”

And looking towards the future, he added:

“[…] It is impossible to predict the future progress of the virus, or its economic impact and we expect the current levels of uncertainty to continue for the foreseeable future. However, the fundamental aspects of our business model remain attractive and since the start of the new financial year Ferguson has generated low single digit revenue growth in the US in flat markets overall. While we remain cautious on the outlook for the year as a whole, the business is in good shape and well prepared to address any further market related disruption.”

Investor notes

Following the update, Ferguson shares rallied 6.85% or 508.00p, to 7,924.00p apiece 29/09/20 12:00 GMT. Analysts have a majority ‘Hold’ stance on the company, alongside a 6,541.00p consensus target price, and the Marketbeat community offering a 52.97% ‘Outperform’ rating on the stock.

The company has a p/e ratio of 18.45, ahead of the industrials sector average of 11.35.

Luxembourg-based general goods store B&M European Value Retail S.A. (LON:BME) saw its shares rally on Tuesday as it published results from its impressive first-half period.

The company boasted 25.3% revenue growth, led by 29.5% revenue growth in its UK stores and like-for-like growth of 23.0%. The company attributed this to elevated average spend per visit, and its variety and value of products on offer.

The company added that it expects first half EBITDA to be above the guidance range of £250 million to £270 million, at £285 million.

Other positive news included the opening of nine new B&M UK stores, which after closures brings the number up by one. Similarly, the company said it expects to open 40 to 45 new stores in the UK, most of which will be in the fourth quarter.

B&M European continued, stating that its Heron Foods convenience store chain, had enjoyed like-for-like sales growth, alongside six net new store openings.

It added that its Babou stores in France reopened on 11 May 2020, with H1 revenue standing at €156.8 million and a ‘small positive’ EBITDA outturn. Overall, it said 37 stores were trading under the B&M brand at the end of H1.

B&M response

Speaking on the results, Chief Executive, Simon Arora, comments:

“Our Group has performed well in the first half. Our business model is proving well-attuned to the evolving needs of customers, given our combination of everyday value across a broad range of product categories being sold at convenient out-of-town locations.

Our people have risen to the many challenges posed by the COVID-19 crisis, not least in serving our customers through a period of high demand, keeping our shelves filled, providing a clean and safe shopping environment, as well as sourcing higher volumes than we had planned. I thank them all for their commitment, hard work and resilience.”

Investor notes

Following the update, the company’s shares rallied 4.76% or 23.32p, to 513.72p apiece 29/09/20 11:30 BST. Analysts also have a majority ‘Buy’ rating on B&M European stock, a consensus target price of 452.62p, and with Marketbeat‘s community offering a majority ‘Outperform’ stance on the company. The Group also has a p/e ratio of 25.15.

UK mortgage approvals have hit a 13-year high.

August saw mortgage approvals hit 84,700, which is the highest rate since October 2007. Demand has boosted thanks to the record low-interest rates and suspension of stamp duty.

New figures from the Bank of England revealed the post-lockdown demand reach new highs, however, consumer borrowing and repayments remains much lower than pre-pandemic levels.

“The mortgage market continued to show more signs of recovery in August,” it said in the report.

“On net, households borrowed an additional £3.1 billion secured on their homes, following borrowing of £2.9 billion in July. Mortgage borrowing troughed at £0.5 billion in April, and is still a little below the average of £4.2 billion in the six months to February 2020. The increase on the month reflected slightly higher gross borrowing of £18.8 billion, although it is still below the pre-Covid February level of £23.7 billion.”

“The number of mortgage approvals for house purchase continued increasing sharply in August, to 84,700 from 66,300 in July. This was the highest number of approvals since October 2007 but it only partially offsets weakness seen between March and June. In total, there have been 418,000 approvals in 2020, compared with 524,000 in the same period in 2019,” added the Bank of England’s report.

Thomas Pugh from Capital Economics said: “Despite the resurgence in the housing market, consumer credit barely rose in August.”

“And the darkening clouds on the economic horizon may tempt some households to start to rein in spending in the months ahead. Those restrictions and rising unemployment will put a further dampener on consumers’ ability to spend.”

“And the prospect of a no deal Brexit is having a chilling effect on business investment. Overall, we doubt that the economy will grow by much, if anything, over the next few months,” he added.

Cairn Energy (LON: CNE) has posted a $324m (£251.8m) loss for the first six months of the financial year.

After being hit with $240m worth of fines, the Edinburgh-based company swung into a loss despite producing the top-end of its full-year guidance.

“We have successfully managed the business through a challenging external environment, always ensuring that the safety of our people is paramount,” said Simon Thomson, the group’s chief executive.

“We took early action with significant reductions and deferrals to the capital programme. Alongside the sale of interests in both Norway and Senegal, we have realigned the portfolio and demonstrated Cairn’s continued commitment to shareholder returns.

“With a strong net cash position and limited capital commitments, Cairn is well-positioned to deliver further value for shareholders,” he added.

The FTSE 250 company posted revenues of $172m (£133.64m) for the six months ended 30 June. Average oil prices fell from $67.84 a year earlier to $40.21 per barrel.

Cairn Energy shares (LON: CNE) are trading -2.04% at 137,63 (1003GMT).