Hornby shares surge as group returns to profit

Hornby shares (LON: HRN) were up 30% on Thursday after the group posted a 33% increase in revenue.

The model railway company returned to a profit of £200,000 for the first time in almost ten years of losses.

“Hornby has moved into profitability, the growing sales and margins built on the back of the introduction of some fantastic new products, new technology and the changing environment,” said Lyndon Davies, the group’s chief executive.

“We are heading into our key Christmas trading period and right now it is hard to tell what the outcome will be for the full year results. Our sales continue to be higher than where they were last year, and there is a real energy within the Company for the Christmas season.”

Hornby saw an increase of online sales at the half-year point and had exceeded the sales levels through this channel than it had achieved in the entire 2019-20 financial year thanks to families staying at home and using products.

The group is selling in over 50 markets worldwide, with over 37% of sales in the first six months of 2020 being outside of the UK.

“We are heading into our key Christmas trading period and right now it is hard to tell what the outcome will be for the full year results. Our sales continue to be higher than where they were last year, and there is a real energy within the Company for the Christmas season,” said the group in a statement.

Horby shares (LON: HRN) have surged 30.59% on Thursday to 44,40 (1601GMT).

Twitter reacts to Corbyn being suspended from the Labour Party

Ever since Kier Starmer won the leadership contest, the feeling was that Jeremy Corbyn’s days in the Labour Party were numbered. Not because he’d leave, but because he is the uncompromising left-wing voice that the Starmer cohort see as unelectable.

Without suggesting that today’s EHRC findings were in any way geared towards a coup against the left-wing of the party, that is certainly how its being perceived by many Labour supporters. For now, ex-party leader, Jeremy Corbyn, has been suspended from the Labour Party, based on the both the findings and his response to a report done on the ongoing antisemitism within the party’s ranks.

Antisemitism certainly wasn’t the hot topic on the public agenda when today’s news broke, but will certainly divert some attention from the tired Boris Johnson, who’ll be grateful that Labour have given commentators something else to talk about. Responding to the ruling by the EHRC, and Labour’s decision to suspend him, Corbyn has said he will contest the findings.BREAKING: Jeremy Corbyn suspended from Labour.

“In light of his comments made today and his failure to retract them subsequently, the Labour Party has suspended Jeremy Corbyn pending investigation. He has also had the whip removed from the Parliamentary Labour Party” – spox — Pippa Crerar (@PippaCrerar) October 29, 2020

Twitter users on both sides have also taken to voicing their opinions, with many commenting that Corbyn has spent several decades fighting racism both in and out of Parliament, with a few describing him as ‘the most decent person’ in British politics.I will strongly contest the political intervention to suspend me.

I’ve made absolutely clear those who deny there has been an antisemitism problem in the Labour Party are wrong. I will continue to support a zero tolerance policy towards all forms of racism. — Jeremy Corbyn (@jeremycorbyn) October 29, 2020

Others have called the move out as a direct attempt to subvert the leftists of the party, with one user noting that Corbyn was the first on the list of MPs highlighted to have been suspended. A former Labour MP added:Jeremy Corbyn is not an anti-Semite.

— Gravel Institute (@GravelInstitute) October 29, 2020

In contrast, many are pleased that Starmer’s Labour appears to be expelling the old guard who – guilty or otherwise – have been heavily associated with remarks and behaviours deemed by the EHRC report to be anti-Semitic.It’s appalling that Jeremy Corbyn has been suspended by the Labour Party, but it should surprise no one.

Socialists in the Party must stop deluding themselves: this was always about destroying Jeremy and criminalising criticism of Israel. It had nothing to do with anti-Semitism! — Chris Williamson (@DerbyChrisW) October 29, 2020

Of course, coup or not, Starmer’s team takes a real gamble with this latest move. Certainly, they’d made a vocal commitment to stamping out any reported sources of anti-Semitism within the party. However, many of the party’s left-leaning support core simply do not believe that Corbyn is a racist, and that remarks seen as anti-Semitic were instead critiques of Israeli political policy. Whichever of these reports is true, it is clear that Starmer has a lot of work to do to re-earn the mantle as leader of the ‘party of unity’. Many on the left will now be looking away from Labour – either offering their support to another party, or starting a party of their own. What is on Starmer’s side is time, and with four years until the next, calendared election, he has a lot of time to soothe wounds and flatten out rough edges. We mustn’t forget, though, that Corbyn isn’t gone. For now, he’s merely been distanced, and much to the chagrin of Mr Starmer, he may yet return:Hugely impressed by Starmer’s willingness to confront racism. Suspending Corbyn shows real political courage.

— Nick Cohen (@NickCohen4) October 29, 2020

It reminds me of a (somewhat butchered) Machiavelli proverb: if you are to harm your enemy, kill them. If you merely injure them, they shall remember, and seek vengeance upon you. If Corbyn finds his way back to Westminster, Starmer may have booked himself an uncomfortable time as leader.Worth remembering that it’s *suspends* not *expels*. There has to be due process: that, after all, is partly what the EHRC was so concerned about in its report. Labour may have to ‘welcome’ him back in due course. So, while it’s quite something, it’s not the end – not yet anyway https://t.co/sa4sEjtPSp

— Tim Bale (@ProfTimBale) October 29, 2020

AB InBev scraps dividend despite growth in revenue

AB InBev has reported a 4% increase in revenue, which is against analyst expectations of a 4% loss.

The world’s largest brewer said on Thursday that it had experienced a jump in sales over the third quarter, however, profits had dipped.

Costs of packaging, cans and bottles, as opposed to the cheaper costs of kegs delivered to pubs, has driven up costs for the brewer.

Beer and soft drink volumes grew by 1.9% in the third quarter, following a 17% drop in the previous quarter. Combined revenues of the group’s global brands, Budweiser, Stella Artois and Corona, increased by 6.8% globally and by 8.1% outside of their respective home markets.

“Our third-quarter results reflect our fundamental strengths as the world’s leading brewer and the resilience of the global beer category. We delivered a strong and balanced top-line performance by quickly adapting to meet the evolving needs of our customers and our consumers. In an ongoing volatile and uncertain environment, we remain focused on being part of the solution by prioritizing the health and well-being of our people, communities and customers,” said Carlos Brito, chief executive of the group.

AB InBev has scrapped its interim dividend due to the “uncertainty and volatility” amid the pandemic.

Foxtons revenue down 10%, shares fall

Foxtons shares (LON: FOXT) are down 5% on Thursday morning after the group reported a dip in revenue.

The London estate agent chain said in its latest trading update for the third quarter ended 30 September 2020 that group revenue was £28.5m, down 10% on the previous year.

A significant reduction in the number of overseas student tenants and corporate relocations led to an 8% decrease in lettings revenues.

Revenue generated from lettings totaled £19.5m, down from £21.3m a year previously.

Revenue from sales in the quarter also fell by 18% to £6.9m due to “depressed levels of exchanges, a hangover from the spring lockdown.”

Sales have since picked up, thanks to pent-up demand post lockdown and Stamp Duty relief. Revenue in September picked up by 9% on the previous year.

Mortgage revenue was £2.2m, up 4%, which reflects increased levels of re-mortgage activity.

The Bank of England said on Thursday that mortgage approvals in the UK have hit a 13-year high.

“The number of mortgage approvals for house purchase continued increasing sharply in September, to 91,500 from 85,500 in August. This was the highest number of approvals since September 2007, and is 24% higher than approvals in February 2020,” said the Bank of England.

Commenting on Foxton’s update, chief executive Nic Budden, said: “Foxtons has made good progress in the third quarter, during which we were able to capitalise on increased levels of market activity, driven by the decision to build back capacity soon after the lockdown ended. We have successfully re-built the sales commission pipeline to its highest level in 3 years, delivered a resilient lettings performance and progressed our lettings book acquisition strategy.

“Although the London residential market has gained momentum, we remain cautious as economic uncertainty causes more sales transactions to fall through and is putting downward pressure on rents. During these uncertain conditions, the energy and commitment of our people to go the extra mile enables us to deliver exceptional customer service whilst keeping our customers and employees safe.”

Foxtons shares (LON: FOXT) were down 5% this morning. Shares in the group have fallen over this past year from a high of 98.00p.

Housing boom continues as mortgage approvals hit 13-year high

Mortgage approvals have hit a 13-year high according to new figures from the Bank of England.

In September, banks approved 91,500 mortgages – the highest figure since September 2007.

Demand has been fuelled by the demand for more space since lockdown as well as the stamp duty holiday.

“The number of mortgage approvals for house purchase continued increasing sharply in September, to 91,500 from 85,500 in August. This was the highest number of approvals since September 2007, and is 24% higher than approvals in February 2020,” said the Bank of England.

“Approvals in September were around 10 times higher than the trough of 9,300 approvals in May.”

Net mortgage borrowing rose to £4.8bn in September, up from £3bn in August.

Lloyds Bank returned to profit for the third quarter thanks to the boom in the housing market. After posting a loss in the first half of the year, the lender has returned to profitability after a surge in demand for home loans.

Andrew Montlake, managing director of mortgage broker Coreco, commented on the figures and said that the boom is likely to lose steam.

“The post-lockdown bull run is already over. Lenders have been pulling down the shutters due to ongoing struggles with capacity and concerns over rising unemployment levels, specifically the impact on house price growth,” he said.

UK on-demand digital pharmacy Phlo surpasses £1.65m funding target on Crowdcube

Sponsored by Phlo

Phlo, the UK’s first real-time, on-demand Digital Pharmacy service hit its £1.65m crowdfunding target on Crowdcube in less than 24 hours and is now overfunding. The funding round has already attracted over 600 investors and has raised over £1.8m to date.

Phlo Digital Pharmacy, launched in November 2019, now plans to extend their crowdfunding campaign due to the high level of demand.

Phlo is the UK’s first same-day, on-demand digital pharmacy service, and is a is a fully authorised NHS pharmacy, underpinned by a state-of-the-art technology platform which combines their pharmacy operations, logistics and patient communications.

Founded by former banker Nadeem Sarwar, the firm has established a strong foothold in London, where it delivers medication to patients in under four hours.

This real-time, on-demand service is not currently offered by any other online pharmacy service in the UK and Phlo aims to expand their service to other major cities across England, including Birmingham and Manchester.

Phlo’s laser focus and commitment to patient care is reflected in their five star Trust Pilot reviews. They have also recently secured a contract with Babylon, the UK’s leading telemedicine provider.

Scaling Up

Mr Sarwar, who had the idea for the business five years ago when he visited Babson College near Boston with Adam Hunter, now Phlo Chief Commercial Officer, said the plan is to scale up “city by city”.

He commented:

“There are 36 million patients on prescription in England. About 1% have gone online. My firm belief is the next five million patients will go online in the next two years – it is our job to go and grab a nice slice of that market share.”

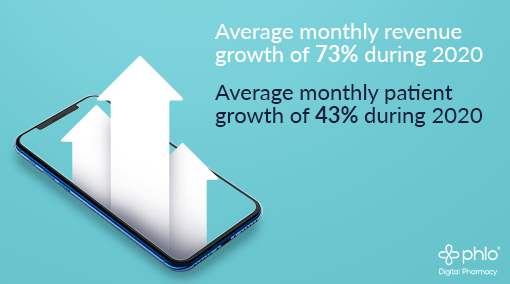

From launch last year, demand and patient numbers have been growing consistently, but in the period since COVID-19 became a significant public health issue, growth has exceeded all expectations.

Since the start of the year, Phlo has seen an impressive average 73% growth in MOM revenue, 43% average growth in MOM patient numbers and a 93% uplift in staff numbers. Phlo has serviced over 5000 patients to date from Jersey to Orkney.

Phlo is headquartered in Glasgow and currently employs 32 members of staff across high-value pharmacy and technology roles. The Pharmacy operations team is situated in central London.

First Digital Pharmacy Crowdfund in UK

This is the first UK Digital pharmacy crowdfund and interest has been high. The initial target of £1.65m was hit in the first 24 hours and the campaign is set to continue until 11thNovember 2020.

Mr Sarwar commented: “I’ve been blown away by the level of support we have received both from our patients and the public. The funds raised from this crowdfunding round will help us to expand our operations in major cities in England and allow us to continue on our path to building the most technology advanced digital pharmacy platform in the UK”

Phlo has also received investment from the UK Government Future Fund in the form of a convertible loan note. Investments will pay 8% interest until they are converted to shares at the completion of a follow – up investment round. Longer term, the company is eyeing up venture capital funding.

To find out more about Phlo’s crowdfunding opportunity, please visit www.crowdcube.com/phlo.

Scaling Up

Mr Sarwar, who had the idea for the business five years ago when he visited Babson College near Boston with Adam Hunter, now Phlo Chief Commercial Officer, said the plan is to scale up “city by city”.

He commented:

“There are 36 million patients on prescription in England. About 1% have gone online. My firm belief is the next five million patients will go online in the next two years – it is our job to go and grab a nice slice of that market share.”

From launch last year, demand and patient numbers have been growing consistently, but in the period since COVID-19 became a significant public health issue, growth has exceeded all expectations.

Since the start of the year, Phlo has seen an impressive average 73% growth in MOM revenue, 43% average growth in MOM patient numbers and a 93% uplift in staff numbers. Phlo has serviced over 5000 patients to date from Jersey to Orkney.

Phlo is headquartered in Glasgow and currently employs 32 members of staff across high-value pharmacy and technology roles. The Pharmacy operations team is situated in central London.

First Digital Pharmacy Crowdfund in UK

This is the first UK Digital pharmacy crowdfund and interest has been high. The initial target of £1.65m was hit in the first 24 hours and the campaign is set to continue until 11thNovember 2020.

Mr Sarwar commented: “I’ve been blown away by the level of support we have received both from our patients and the public. The funds raised from this crowdfunding round will help us to expand our operations in major cities in England and allow us to continue on our path to building the most technology advanced digital pharmacy platform in the UK”

Phlo has also received investment from the UK Government Future Fund in the form of a convertible loan note. Investments will pay 8% interest until they are converted to shares at the completion of a follow – up investment round. Longer term, the company is eyeing up venture capital funding.

To find out more about Phlo’s crowdfunding opportunity, please visit www.crowdcube.com/phlo.

Scaling Up

Mr Sarwar, who had the idea for the business five years ago when he visited Babson College near Boston with Adam Hunter, now Phlo Chief Commercial Officer, said the plan is to scale up “city by city”.

He commented:

“There are 36 million patients on prescription in England. About 1% have gone online. My firm belief is the next five million patients will go online in the next two years – it is our job to go and grab a nice slice of that market share.”

From launch last year, demand and patient numbers have been growing consistently, but in the period since COVID-19 became a significant public health issue, growth has exceeded all expectations.

Since the start of the year, Phlo has seen an impressive average 73% growth in MOM revenue, 43% average growth in MOM patient numbers and a 93% uplift in staff numbers. Phlo has serviced over 5000 patients to date from Jersey to Orkney.

Phlo is headquartered in Glasgow and currently employs 32 members of staff across high-value pharmacy and technology roles. The Pharmacy operations team is situated in central London.

First Digital Pharmacy Crowdfund in UK

This is the first UK Digital pharmacy crowdfund and interest has been high. The initial target of £1.65m was hit in the first 24 hours and the campaign is set to continue until 11thNovember 2020.

Mr Sarwar commented: “I’ve been blown away by the level of support we have received both from our patients and the public. The funds raised from this crowdfunding round will help us to expand our operations in major cities in England and allow us to continue on our path to building the most technology advanced digital pharmacy platform in the UK”

Phlo has also received investment from the UK Government Future Fund in the form of a convertible loan note. Investments will pay 8% interest until they are converted to shares at the completion of a follow – up investment round. Longer term, the company is eyeing up venture capital funding.

To find out more about Phlo’s crowdfunding opportunity, please visit www.crowdcube.com/phlo.

Scaling Up

Mr Sarwar, who had the idea for the business five years ago when he visited Babson College near Boston with Adam Hunter, now Phlo Chief Commercial Officer, said the plan is to scale up “city by city”.

He commented:

“There are 36 million patients on prescription in England. About 1% have gone online. My firm belief is the next five million patients will go online in the next two years – it is our job to go and grab a nice slice of that market share.”

From launch last year, demand and patient numbers have been growing consistently, but in the period since COVID-19 became a significant public health issue, growth has exceeded all expectations.

Since the start of the year, Phlo has seen an impressive average 73% growth in MOM revenue, 43% average growth in MOM patient numbers and a 93% uplift in staff numbers. Phlo has serviced over 5000 patients to date from Jersey to Orkney.

Phlo is headquartered in Glasgow and currently employs 32 members of staff across high-value pharmacy and technology roles. The Pharmacy operations team is situated in central London.

First Digital Pharmacy Crowdfund in UK

This is the first UK Digital pharmacy crowdfund and interest has been high. The initial target of £1.65m was hit in the first 24 hours and the campaign is set to continue until 11thNovember 2020.

Mr Sarwar commented: “I’ve been blown away by the level of support we have received both from our patients and the public. The funds raised from this crowdfunding round will help us to expand our operations in major cities in England and allow us to continue on our path to building the most technology advanced digital pharmacy platform in the UK”

Phlo has also received investment from the UK Government Future Fund in the form of a convertible loan note. Investments will pay 8% interest until they are converted to shares at the completion of a follow – up investment round. Longer term, the company is eyeing up venture capital funding.

To find out more about Phlo’s crowdfunding opportunity, please visit www.crowdcube.com/phlo. WPP reveals drop in Q3 revenue

WPP (LON: WPP) has revealed a 9.8% fall in revenue for the third quarter to £2.97m.

Like-for-like sales fell 5.5% to £2.97bn, however, the drop was smaller than the 11.5% fall in the second quarter.

“WPP continues to demonstrate its resilience in a challenging market. We have maintained our new business momentum as clients seek out our creativity and our skills in media, technology, data and ecommerce,” said chief executive Mark Read.

“This month, Uber joined a growing list of major assignment wins that includes Alibaba, Dell, HSBC, Intel, Unilever and Whirlpool, and we continue to lead the new business rankings. We have also renewed and expanded our relationship with Walgreens Boots Alliance to encompass its data- and technology-driven marketing strategy.

“Given the tightening of COVID restrictions around the world and uncertainty in the global economic outlook, we remain cautious about the pace of recovery. It is important that we maintain our strong financial position and we are on track to achieve cost savings towards the upper end of our £700-800 million target.”

WPP said it has seen improvement in North America as clients are returning to spending more on media ads.

Shore Capital analysts said in a note: “Notwithstanding continuing uncertainty over short-term advertising spend, we are encouraged by the momentum flagged in this morning’s update, continue to view WPP as a quality business and like the way in which it is been repositioned.”

WPP shares (LON: WPP) were down 3.25% in Thursday morning trading.

Lloyds returns to profit amid housing boom

Lloyds (LON: LLOY) has reported a pre-tax profit of £1bn, beating expectations for the third quarter.

After posting a loss in the first half of the year, the lender has returned to profitability after a surge in demand for home loans.

This quarter has seen the biggest growth in demand for home loans since 2008, which led to mortgage lending at the bank of £3.5bn.

The temporary stamp-duty holiday has led to a boom in the housing market, also helped by people wanting more space amid the pandemic.

Chief executive Antonio Horto-Osario commented: “Although our performance has clearly been impacted by the pandemic and the associated challenging economic environment, I am pleased that we are now seeing an encouraging business recovery and, with impairments significantly lower, a return to profitability in the third quarter.”

“Our customer-focused strategy and the strength of the group’s business model will allow us to continue to help Britain recover and play our part in helping to return the UK to prosperity.”

Horta-Osorio will be leaving the lender next year after a decade at the helm.

Lloyds shares (LON: LLOY) opened 2.6% at 28.37p. Shares this year have fallen 53% from previous highs of 69.99p.

BT raises profit guidance despite 20% fall in profits

In the latest trading update, BT (LON: BT.A) has reported a 20% fall in half-year profits.

The telecoms giant revealed post-tax profits of £856m – falling from last year’s £1.07bn.

Revenue at the group fell 8% to £10.6bn.

Despite the fall in revenue and profits, BT has raised its full-year guidance to £7.3bn – £7.5bn.

“BT delivered financial results in-line with expectations for the first half of the year, thanks to strong operational performance during exceptional circumstances. Customer demand during the pandemic has shown how critical our networks have become, and our significant network investments have helped us double the number of Openreach’s FTTP orders compared to this time last year and have seen our leading 5G network expand to 112 towns and cities across the UK,” said chief executive, Philip Jansen.

“We continue to invest to make BT more competitive and I’m pleased to see the quality of our products and services improving. At the same time we are firmly on track with the delivery of our modernisation programme and have delivered £352m in cost savings in the first half of the year.

“This performance has given us confidence to raise the lower end of our EBITDA outlook range for this year and publish an EBITDA expectation of at least £7.9bn for 2022/23, with sustainable growth from this level forward. This growth will be driven by the continued recovery from Covid-19, enhanced by sales of our converged and growth products, and by significant savings from our modernisation and cost saving programme. In combination these factors will more than offset legacy product declines.

“The growth in EBITDA underpins the planned reinstatement of our dividend next year whilst ensuring that we can continue to drive value-creating investments in our networks and products.”

BT shares (LON: BT.A) opened +5% at 107,10. Over the past year shares in the group have fallen almost 50%.

Three reasons why New Year’s Eve may be an eventful time for equities

It’s still an election, twenty new COVID policy measures, and a Christmas dinner away, but its worth trying to anticipate what equities will look like as the clock strikes midnight on New Year’s Eve. And, here are three factors to consider.