Boohoo shares spike over 5% after annual guidance is lifted

Boohoo (LON: BOO) have once again pulled out an impressive set of results in their update on Tuesday morning.

The firm updated the market this morning saying that it has raised its annual guidance following strong revenue growth.

Also in the update, the firm said that it had appointed former JD Sports (LON:JD) chief financial officer as its new deputy chair.

Brian Small, will take up this position with immediate effect having held executive positions at Mothercare (LON:MTC) and Pendragon (LON:PDG).

For the four month period, which ended on December 31, the firm said that its revenue had jumped 44% to £473.7 million from the £328.2 a year ago.

Boohoo said that it expects revenue growth for its financial year, which ends on February 29 to be between 40% and 42% ahead of their previous guided range of 33% to 38%.

The firm added that t expects adjusted earnings before interest, taxes, depreciation and amortisation margin to be 10% to 10.2%, beating its previous guidance of around 10%.

John Lyttle, CEO, commented:

“I am delighted to report the group has enjoyed record trading in the last four months of 2019. All of our brands have performed exceptionally well and delivered strong market share gains. We have continued to see operating leverage in our more established brands, and will continue to invest into them and our newly-acquired brands. The newly-acquired brands, MissPap, Karen Millen and Coast, are showing great promise and open different target markets for the group, in line with our strategy to build our multi-brand platform.”

Analysts have praised BooHoo for their performance in a market which seems to be slumping.

John Woolfitt, Director of Trading at Atlantic Capital Markets:

“Its not all doom and gloom for retail, well at least not if you are operating online. The fast fashion king Boohoo has today hiked guidance after a record quarter and investors will be pleased with the progress the group has made in 2019.”

“The integration of new acquisitions such as Miss Pap, Karen Millen and Coast will add to earnings potential over the coming year to build on what has been a very successful festive trading period.”

“Investors will take results from Boohoo as additional confirmation that if you are investing in the UK retail sector, you have to focus on the online retailers.”

Markets unphased by US-China trade deal progress

Markets dipped slightly on Tuesday morning, despite what appeared to be a warming up of good sentiments between the US and China, and the expected passing of the first phase of a trade deal. Progress was largely priced in by markets, and thus the news didn’t have quite the impact it would have done a few months ago.

The good news stories this morning came from the FTSE, which was able to outperform its counterparts following a disheartening GDP reading on Monday, which pushed Sterling down.

Elsewhere, Boohoo (LON: BOO) saw its revenues bounce 44% during the final four months of 2019, which saw the online fashion retailer buck the cheerless trend set by its peers.

Elsewhere in retail and the highstreet, Christmas proved costly; Marks and Spencer (LON:MKS) issued an underwhelming update, Tesco (LON: TSCO) suffered in Europe though it reported a potential sale of its Asian business, and Sainsbury’s (LON:SBRY) saw a drop in quarterly sales.

Speaking on trade deal progress and the morning’s updates, Spreadex Financial Analyst Connor Campbell stated,

“The markets didn’t really get anything from the newly revealed details of the US-China trade deal, instead drifting lower after the bell.”

“With the agreement all ready to be signed tomorrow, Washington removed the ‘currency manipulator’ label from China – a symbolic gesture rather than tangible one, but nevertheless another example of thawing relationships between the two superpowers.”

“This helped send the yuan to a 5-month high, but did little for the Western indices. Instead the DAX and CAC fell 0.5% apiece, with the Dow Jones set to drop 0.4% later this afternoon. The FTSE avoided the same kind of losses, though was still down a handful of points.”

“The trouble is, the positive aspects of the trade deal are pretty thoroughly priced in. In contrast, any rogue comments from Donald Trump in the coming days – especially those related to ‘phase two’, if the US and China ever get to that point – may then have a disproportionate impact on the markets, good or bad.”

“The reason the FTSE was able to outperform its peers was the continued weakening of sterling. The pound lost another 0.2% against dollar and euro alike, the ongoing speculation of an incoming interest rate cut, heightened by Monday’s dreadful GDP reading, weighing on the currency.”

“It was, broadly, a terrible Christmas for UK retailers. However, as is often the case, boohoo managed to buck the trends that have afflicted its high street peers, crying tears of joy after a record quarter. For the 4 months to the end of 2019 revenue jumped 44%, causing it to lift its forecast growth for the year to 40-42% against previous estimates of 33-39%. That increase was enough to send the stock to a fresh all-time high, the fashion brand rising 3.3% to strike £3.28.”

Taylor Wimpey expect results to be steady following turbulent 2019

Taylor Wimpey plc (LON:TW) have told the market that they expect their results to be in line with expectations.

The firm had alluded to both political and economic complications across the 2019 trading year, as the property market was hit by external shocks.

The FTSE 100 trader said that the housing market remained stable in the last year, however there were challenges faced in London and the South East.

Taylor Wimpey noted that total house completions in 2019 has increased by 5% to 15,719 which included joint ventures.

“While 2020 will continue to be a year of change for the UK, we welcome the increased political stability following the general election,” the company said.

“We start the year with a strong order book and continue to target a smoother profile of completions throughout the year but expect 2020 to continue to be second half weighted,” the housebuilder said.

2019 ended with a record total order book valued at £2.17 million, which showed a ruse from the £1.78 figure a year ago.

The house builder said that it remains cash generative and intends to return £610 million to shareholders in a dividend form.

Pete Redfern, Chief Executive, commented:

“Our results for the year to 31 December 2019 will be in line with our expectations. Despite an uncertain political and economic backdrop in 2019, we have continued to experience a good level of demand for our homes and trading in the second half of the year was as anticipated. The Group has again delivered a record sales rate and we increased home completions by c.5% in the year.

In 2019, our focus was on strengthening the long term sustainability of the business, further improving our build quality and customer offering, as well as increasing operating capacity and flexibility. In 2020, we will continue with these initiatives and will also prioritise a renewed cost focus and process simplification improvements.”

Operating profit for the period was down 9.4% to £311.9 million, however this was attributed to higher build costs and geographic mix.

Market analysts have been somewhat impressed with the performance of Taylor Wimpey, which will please shareholders.

John Woolfitt, Director of Trading at Atlantic Capital Markets commented

“Today’s figures show, that despite political uncertainty, the sector is still performing well. Record sales rates for Taylor Wimpey and an increase in home completions all bode well for the builder’s shares which are shaking off any concerns over slowing house prices.”

“This, and a positive outcome for the conservatives in the December election, has also led to further upgrades for the whole sector and a positive outlook for the year ahead.”

“Dividends increased significantly to £600m in 2019 and although dividends are not set to jump to the same degree in 2020, investors can look forward to a similar payout of around £610m from Taylor Wimpey in the year ahead.“Wimpey build from November

In November, the firm reported strong demand in their second half update.

Taylor Wimpey did warn homebuilders about potential rising costs in 2020, however in the Wednesday statement, the firm speculated that cost inflation may reduce in 2020 instead.

The FTSE 100 listed home builder, reported a 12.5% rise in its orders, to £2.7 billion as it exploited strong demand coupled with lower interest rates and the governments Help to Buy scheme boosting demand.

Total order book, excluding joint ventures, stood at 10,433 homes as at November 10 from 9,843 homes a year earlier.

The Homebuilding market – Boris Bounce wears off

Just as the election results were hitting news headlines on 13th December, many of the British Home builders saw their shares in green.

Notable rises came from Berkeley Group Holdings PLC (LON:BKG) whose shares spiked 13.06%, whilst Barratt Developments Plc (LON: BDEV) shares rose 12.52% to 755p.

MJ Gleeson (LON:GLE) updated the market last week saying that they remained confident in a home building market that was still facing uncertainty.

The householder said that its Homes unit had sold 811 units during the half year period to end 2019, which saw a 17% climb year on year from the 691 figure.

Additionally, Gleeson said that the demand for its low cost homes remains strong and is on track to deliver full-year unit completions in line with expectations.

For financial 2019, the firm reported pretax profit of £41.2 million, which showed growth by 11% from the £37 million a year ago.

The results today posted by Taylor Wimpey are impressive, and shareholders will be keen to see how 2020 unfolds as the Brexit negotiations take their turn and hopefully many political uncertainties are cleared.

Shares of Taylor Wimpey trade at 205p (+1.88%). 14/1/20 10:34BST.

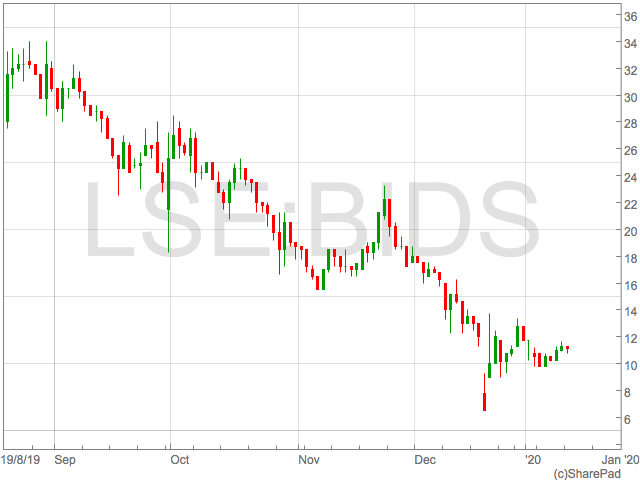

Will Bidstack shares overcome this hurdle in their business model?

Bidstack (LON:BIDS) are expanding into the very exciting gaming industry and have recently announced agreements with a major agency, a key step to future success.

However, Bidstack are attempting to enter an extremely competitive programmatic advertising network market and will be taking on some of the world’s largest technology companies.

Although Bidstack are providing innovations through the context of in-game displays such as football hoardings, they lack a significant function other digital advertising in direct engagement.

The Beauty of advertising networks run by Google, Amazon and Facebook at is the ability to drive and track engagement with adverts.

Whether it be display banner adverts run by Google or an advert to download an App through Instagram, advertisers are able to measure the effectiveness of their adverts by tracking clicks, downloads or sign ups and analysing the cost per engagement.

This removes a lot of the potential value from Bidstack’s business model when compared to the traditional digital advertising networks.

However, it doesn’t render it completely worthless. The attention of gamers carries significant value. Twitch is an example of this.

The challenge for Bidstack is their inventory merely replicates an out-of-home advertising model but places it in a digital environment, without the interaction enjoyed by other forms of digital advertising. This may raise questions among the major agencies when creating plans for the world’s leading advertisers.

This removes a lot of the potential value from Bidstack’s business model when compared to the traditional digital advertising networks.

However, it doesn’t render it completely worthless. The attention of gamers carries significant value. Twitch is an example of this.

The challenge for Bidstack is their inventory merely replicates an out-of-home advertising model but places it in a digital environment, without the interaction enjoyed by other forms of digital advertising. This may raise questions among the major agencies when creating plans for the world’s leading advertisers.

Bidstack Business Model

Here lies the fundamental flaw in Bidstack’s model. Adverts run through Bidstack’s inventory is void of opportunity for engagement. Bidstack have said they don’t want to ruin the immersive experience of gaming. This is attractive to the game developer, but not so much to potential advertisers. Can you imagine a gamer playing Fifa online and pausing their match mid flow to interact with an advert and buy a product? It seems unlikely. Firstly because the functionality isn’t there and it is very doubtful to ever be there at a meaningful scale. Secondly, and most importantly, gamers are going to have little propensity to stop their game and make third part purchases, even if they could. This removes a lot of the potential value from Bidstack’s business model when compared to the traditional digital advertising networks.

However, it doesn’t render it completely worthless. The attention of gamers carries significant value. Twitch is an example of this.

The challenge for Bidstack is their inventory merely replicates an out-of-home advertising model but places it in a digital environment, without the interaction enjoyed by other forms of digital advertising. This may raise questions among the major agencies when creating plans for the world’s leading advertisers.

This removes a lot of the potential value from Bidstack’s business model when compared to the traditional digital advertising networks.

However, it doesn’t render it completely worthless. The attention of gamers carries significant value. Twitch is an example of this.

The challenge for Bidstack is their inventory merely replicates an out-of-home advertising model but places it in a digital environment, without the interaction enjoyed by other forms of digital advertising. This may raise questions among the major agencies when creating plans for the world’s leading advertisers.

Demographics

Despite engagement presenting a potential hurdle, Bidstack does provide value to advertisers in the form context and the ability to gain the attention of a specific demographic. Harnessing this effectively is where long term shareholder value should be created given the recent decline in social media users. The recent slow down could signal a top in advertising growth through Facebook, Instagram and Twitter. This is of course a high risk assumption given the resources of the social media giants, but it may play into Bidstack’s hands. “Bidstack is a very interesting proposition and appeals to me as a more speculative aim stock. They look to have coupled up two sectors in a partnership that will see advertising delivered to a huge demographic in a new, unique and very passive way,’ said John Woolfitt of Atlantic Capital Markets. Summarising the potential risk of Bidstack’s model John Woolfitt continued “with any company like this you must see it for what it is, this is no defensive income share and it will need potential investors to understand the concept. Shares like this should occupy the smaller more speculative section of your overall portfolio.” “That all being said the company is well positioned to take advantage of the evolving technology, and as a lot of gamers globally are now in their 30’s and have disposable income they are well positioned to catch the opportunity at a time that has now seen the consumers become a valid audience for advertising.” Bidstack (LON:BIDS) listed in 2018 at 6p per share and currently trade at 11p, having reached highs of 42p in June.City Pub Group fall 8% following festive slow down

City Pub Group PLC (LON:CPC) have said to shareholders on Monday that they will miss market expectations, leaving shares in red.

The firm said that they experienced “subdued” trading across the festive period, which dampened expectations.

In its financial year, which ended on December 29 the firm said that it had performed relatively well. The firm saw its revenue rise 31% to £59.8 million, as like for like sales jumped 1.7%.

Following the slower Christmas period, the firm said that adjusted earnings before interest, tax, depreciation, and amortisation for the year is now expected to be slightly below market expectations, between £9.1 million and £9.2 million.

Notably this would see a 15% rise year-on-year, which is something for shareholders to be pleased about.

The pub chain also said that the 2018 festive period was a busy one compared to this year, where business slowed.

However, a number of one-off factors in the last quarter of its year held back fourth-quarter performance.

“The Rugby World Cup did not have the impact that we expected. Political uncertainty culminating in the December election held back sales until the result was known and unhelpful weather during November and December dampened trading further,” said the company.

“There were also disruptions on South West trains throughout December due to industrial action, which had an impact on our London estate.”

“The group has a strong business model that is quick to respond to the more normal trading conditions now prevailing,” it continued.

“Efforts too refocus on operating margins are already underway and this year’s performance should see the benefits of this. In addition, there are two underperforming sites that have been earmarked and actively marketed for disposal.”

Looking to its new financial year, City Pub Group noted it will benefit from some recently opened pubs.

It also has three large developments which will open later in the year.

Generally successful year for City Pub

In September, the firm saw its profit rise as it posted impressive financial results for the first half of FY19. In spite of their trading performance following the announcement, the Company performed well during the first half, with like-for-like sales increasing by 2.6% and revenues spiking 36% on a year-on-year basis, to £27.1 million. This led the Group’s 20% EBITDA surge, to £3.6 million, and a 19% hike in adjusted profit before tax, to £1.9 million. City Pub Group said they had opened four new pubs during the period, with their in development becoming their main focus, in lieu of further acquisitions. The Company added that it had reaped the rewards of its new regional management structure and Weekly Employee Bonus Scheme, both of which the Group said would bolster growth and incentivise staff.Competitors – JD Wetherspoon still leads the market

In November, J D Wetherspoon plc (LON:JDW) saw their shares spike following a bullish update. The British pub chain boasted strong sales figures, which increased across the quarter as customers spent more its nearly 900 pubs across Britain and Ireland. The company reported higher demand for coffee, pink gin, real ale and breakfast. Additionally beer sales rose significantly as British consumer trends changed by the quarter. J D Wetherspoon’s like-for-like sales rose 5.3%, which exceeded both market and analyst expectations. Additionally, the firm pledged to create 10,000 new jobs over the next four years in December. Wetherspoon updated the market by saying that they plan to open between 50-60 new pubs and hotels. These new branches will be located within in small and medium-sized British towns and cities but also in London, Edinburgh, Glasgow, Birmingham and Leeds as well as the Irish cities of Dublin and Galway. “Wetherspoon will not be entering into any deal like everyone else,” a company spokesman said.Fuller, Smith & Turner experience turbulence

Another name in the industry, in Fuller, Smith and Turner (LON:FSTA) saw their shares crash a few weeks back. In January, pub operator Fuller’s agreed to sell its historic brewing operations to Japanese brewer Asahi Group Holdings Ltd (TYO:2502) for £250 million. Fuller’s expects the higher overhead levels to remain in place until the services agreement ends in May. Following this, the now pure-play pubs and hotels operator will be able to transition its costs structure to this new focused business. The statement provided updated shareholders saying that annual profit was set to be unchanged.The firm alluded to costs with the separation of its brewing business came in significantly higher than expected. Certainly, City Pub have performed well across their financial year. The firm still has lots of growth and development to undertake, but shareholders can remain confident that 2020 will be a productive year for the firm. Shares in City Pub Group trade at 198p (-8.97%). 13/1/20 14:28BST.British economy sees weakest period of Economic Growth since 2012 in November

The British Economy has seen its weakest period of economic growth since 2012 in November.

Figures released on Monday morning showed the British people that the economy in November had grown a modest 0.6%, which was the weakest figure since June 2012.

This figure also represented a slowdown from the 1% annual growth figure in October, which has been hampered by both political and economic stresses.

Output in November fell by 0.3% which was the biggest drop since April, and certainly the pre-election caution had hit both consumers and investors.

In November, notable slumps came from British supermarkets and the Big Four saw their profits slump.

Sainsbury’s (LON:SBRY) saw their profits fall across the Christmas period.

n the 15 weeks to January 4, total retail sales, excluding fuel, were down 0.7% from last year. Including fuel, sales were down 0.9%, which has seemed to edge shareholders.

In the three months to November, the economy grew 0.1% which was a positive note to take however the future of British retail and the British high street has never looked so glum

On a more positive note, grocery sales rose 0.4% from a year ago with online grocery sales up 7.3% an area which the firm has looked to expand over the last few years.

Additionally, Morrisons (LON:MRW) have reported that their sales have fallen in their update dating to January 5.

The firm said that challenging trading conditions coupled with consumer uncertainty were the largest contributors to the slump in sales.

Morrison’s said that said like-for-like sales, excluding fuel, were down 1.7% year-on-year.

Additionally the decline was further

accelerated by a fall in retail sales, as a like for like performance in the wholesale unit remained flat.

Notably, fuel sales declined 2.8% year on year across the 22 weeks period, and total sales dipped 2.9% but the figure totaled 1.8% without fuel sale considerations.

The weak data, reflected the uncertainty of last autumn about Brexit and the election, said John Hawksworth, chief economist for accountants PwC.

“It is too early to say for sure if economic momentum will pick up in the new year now the political situation is clearer, but our latest survey of the financial services sector with the CBI does suggest some boost to optimism since the election,” he said.

The British public are still in a stalemate and do not know which direct Brexit negotiations are heading towards.

Indeed, the victory by the Conservatives has given British politics some clarity however the Boris Bounce has seemed to fade.

PM Johnson is planning to take his deal to the EU this week, and the deadline set at January 31 still could be pushed further back if the EU stipulate against terms of the exit deal.

Caledonia Mining shares bounce over 5% following record production figures

Caledonia Mining (LON:CMCL) have seen their shares bounce on Monday afternoon following record production figures from its Blanket Mine.

The firm said that it is considering to revise future dividends, and following the update today these could rise.

At the start of the month, Caledonia said it would be paying $0.075 quarterly dividend, which was 9.1% higher than the previous figure.

The firm said that it had delivered strong performance from the Blanket Gold Mine in Zimbabwe.

The mine produced 16,875 ounces of gold in the last quarter of 2019, a record for the firm. The figure was 24% higher than the quarter before and 13% higher year-on-year

The firms total production in 2019 was 55,182 beating internal guidance which was pitched between 50,000 and 53,000 ounces.

Caledonia remain optimistic in future outlook

Looking to 2020, the Jersey-based company sees gold production between 53,000 ounces and 56,000 ounces. Chief Executive Steve Curtis said: “I am delighted to report a production record at Blanket of 16,867 ounces in the fourth quarter. An improvement in the electricity supply and vigilant focus on grade control and production tonnage have resulted in an excellent production result for the final quarter of which our entire operational staff can be justifiably proud. “The impressive operational turnaround was achieved without any compromises on safety. This is a commendable achievement given the distractions posed by the challenging conditions experienced by our workers due to the economic environment in Zimbabwe.” “I am also pleased to see we have not lost this momentum as we start 2020 with the mine continuing to perform very well into the new year. With the improved operational performance and the current buoyant gold prices leading to healthy operating margins we expect Caledonia to continue its track record of strong cash generation,” Curtis continued. “I expect 2020 to be a landmark year for our business: we look forward to commissioning the central shaft later in 2020 which we anticipate will then deliver increased operating cash flows and reduced capital expenditure will follow.”Shareholders remain impressed after beating annual guidance

In July, the firm said that it planned to retain its full year guidance as it updated shareholders on its Q2 activity. The Company stated that 12,712 ounces of gold were produced during Q2, which represented a 6.4% rise on the 11,948 ounces for Q1. Caledonia Mining retained its full year guidance of 53,000 – 56,000 ounces despite H1 output standing at just 24,660 ounces; this was 3.4% lower than last year’s volume of 25,582 ounces. The Company currently holds a 49% in Blanket Mine, but has penned a conditional agreement to expand this to 64%. It said it remained on target to reach its 80,000 ounces per annum target for 2022. “As at March 31, 2019, Caledonia had cash of approximately US$9.7 million. The Company plans for Blanket to increase gold production from 54,511 ounces in 2018 to approximately 75,000 ounces in 2021 and approximately 80,000 ounces by 2022,” the Company said.Zimbabwe Operators

Firms that hold operations in Zimbabwe have also given the market solid updates over the last few months. Notably, Botswana Diamonds PLC (LON:BOD) and Vast Resources PLC (LON:VAST) have announced a deal to replace the Heritage concession agreement between the two firms. The new agreement outlines the formation of a new company which holds the interest of Vast Resources,the Chiadzwa Community joint venture and Katanga Mining (TSE:KAT). Additionally, the agreement expresses the intent to issue new shares representing 2.5% of the newly formed company to Botswana Diamonds once the detailed agreement between Katanga and Zimbabwe Consolidated Diamond Co becomes effective. Shareholders of Caledonia Mining will be pleased with the update today, as 2020 could be a year of growth and expansion for the London listed miner. Shares in Caledonia Mining trade at 668p (+5.20%). 13/1/20 13:49BST.Feedback agree deal with Imagine Engineering for fluoroscopic medical equipment

Feedback Plc (LON:FDBK) have told the market about signing a new deal with a US based technology firm.

Feedback said that it had agreed a commercial partnership agreement with Imagine Engineering LLC to support the installation and refitting of a modernized fluoroscopic medical equipment across the US.

Imaging Engineering is the manufacturer of an X-ray fluoroscopy product, “Insight Essentials” which enables the capture of fluoroscopy and X-ray images using low-cost hardware.

Fluoroscopy is a form of dynamic X-ray capture which enables real time, moving patient imaging and is commonly used for a number of imaging investigations within gastroenterology, orthopaedics and interventional radiology.

Under the terms of agreement, Feedback Medical, Feedback’s wholly owned subsidiary, will receive a license fee for each installation performed by Imaging Engineering and will have no commitment beyond maintaining and providing the software.

The firm also added that all intellectual property relating to the software will remain with Feedback.

Feedback will provide the core software to manage the entire system for the “Insight Essentials” product, from image capture through data management to DICOM (Digital Imaging and Communications in Medicine) networking

Feedback Medical will receive a licence fee for or each installation performed by Imaging Engineering.

Tom Oakley, CEO of Feedback plc, said:

“This partnership will allow US healthcare providers to modernise their fluoroscopic equipment to meet the needs of the next decade, with considerable savings for the provider and a reduction in equipment disposal. For Feedback, the licence fee provides us with a new stream of revenue reflecting our strategic focus on the Cadran product portfolio which includes our flagship product, Bleepa, and its commercial roll-out in 2020. We look forward to continuing to work with Imaging Engineering as it rolls out the Insight Essentials system throughout the United States.”

Feedback grow following Bleepa trial

In November, the firm updated shareholders about a new trial with Pennine Acute Hospitals NHS for its new medical communication platform, Bleepa.

Bleepa is a platform which enables clinicians to access medical grade images through smartphones, tablets and desktop computers.

Dr Georges Ng Man Kwong, Consultant Chest Physician and CCIO of Pennine Acute Hospitals NHS Trust, commented:

“Bleepa is addressing a direct clinical challenge to better support our busy respiratory clinicians (at the Royal Oldham Hospital) by improving referral process and patient care. Each referral requires rapid and reliable access to radiology images and clinical handover information, and a means of messaging referring teams and documenting outcome. Bleepa has the potential to bring this together for our clinicians and therefore for our patients. We are delighted to be involved with this innovation solution.”

The medical technology sector remains volatile

Consort Medical plc (LON: CSRT) are a noteworthy name in this sector. The firm said that interim profit was bruised due to an incident at its Aesica Cramlington manufacturing facility.

Consort’s pretax profit for the six months ended October 31 was £1.2 million, far less than the £9.6 million profit posted the year before as revenue fell 4.3% to £146.0 million from £152.5 million.

This was primarily caused by the Cramlington incident, in which a small area of the Northumberland-based operating plant was damaged in what was described by Consort at the time as “the rapid thermal degradation of a chemical resulting in the expulsion of material and contamination of the facility”.

Additionally, AorTech International plc (LON: AOR) have seen shares become volatile following research and development investments.

AorTech is focused on the commercialization of its world leading biomedical polymer technology, components and medical devices.

AorTech has, through a licence and supply agreement, all of its materials manufactured by Biomerics, a leading contract manufacturer and innovative polymer solutions provider in the USA.

The firm said in an update to shareholders said that it had widened its interim loss on costs. However, shareholders did get some consolidation with the fact that revenues had rose.

It seems that shareholders have been more focused on the revenue gains rather than the widened loss, as share price moved positively this morning.

For the six months to the end of September, the biomaterials and medical devices firm said its pretax loss widened to £239,000 from £225,000 the year before.

This was due to administrative expenses rising by 29% to £451,000 from £350,000, as a result of research & development activities.

However revenue, which comes from the licensing of AorTech’s polymer technology, grew by 27% to £299,000 from £236,000 the prior year.

Shareholders of Feedback should remain confident with the firm, as the new deal will allow them to expand into the US medical technology market which may see longer term benefits.

Shares in Feedback plc trade at 0.95p (-6.40%). 13/1/20 13:14BST.

Victrex announce deal with Yingkou Xingfu to expand into China

VIctrex PLC (LON:VCT) have told shareholders that they will be partnering with a Chinese firm to build a manufacturing unit in China.

Shares in Victrex trade at 2,471p (-0.099%). 13/1/20 12:50BST.

VIctrex have said that they will tie up a deal with Yingkou Xingfu Chemical Co Ltd to build a manufacturing plant in Liaoning, in the north east of China.

Victrex said they “already has an established relationship with its joint-venture partner through its monomer supply chain, with Yingkou Xingfu having significant experience of developing and operating chemical facilities in China which meet international quality, process and environmental standards.”

Through its Hong Kong subsidiary, Victrex will own three quarters of the joint-venture, and will aim to build a polyether ether ketone, or PEEK, polymer manufacturing facility.

The company said it will invest £32 million in the partnership, and the facility will be capable of producing 1,500 tonnes of polymers per year.

This comes at a good time for Victrex, as it follows the China 2025 initiative, unveiled by the country in 2015, which aims to increase China’s presence as a competitive global player in the manufacturing industry by 2025.

Jakob Sigurdsson, Chief Executive of Victrex, said: “This investment is in line with our record of not only investing ahead of demand, but in complementing and further differentiating our range of PEEK and PAEK grades, as well as setting the stage for specific geographic growth, whereby we can capitalise on the significant opportunities in China and the Asia Pacific region by having a competitive manufacturing presence there.

“Alongside the Made in China 2025 initiative, some of our increasingly diverse application areas mean our customers require a quality and differentiated PEEK offering. Whilst we already manufacture a range of PEEK and PAEK grades, this will enhance our portfolio, making us even better positioned in a region where we have seen strong growth in recent years and continue to see attractive opportunities, aligned to our know-how and strong technical and application development capabilities.

“Overall, we believe this is a good entry point to a China manufacturing operation, working with an established partner and offering an attractive returns profile.”

Victrex build following slow update

At the start of December, the firm saw its shares dip following a modest update.

In the twelve months to September 30, Victrex recorded pretax profit of £104.7 million, down 18% on the £127.5 million reported the year before. Additonally, Revenue fell 9.8% year on year to £294.0 million from £326.0 million.

The company lowered its total dividend per year to 59.56 pence, down 58% on the 142.24p distributed the year before.

Victrex saw a 15% drop in group sales to 3,751 tonnes from 4,407 tonnes the year before.

The company explained: “This reflects the cyclicality in Automotive and the associated impact on our Value Added Resellers segment, together with some de-stocking, with supply chain inventories running very low.”

The company also noted the “weaker” Electronics market, with both the semiconductor and smartphone markets down.

Victrex said a further headwind was the “tough” year on year comparative in its Consumer Electronics business, where it signed a large contract in the prior year. Excluding that contract, total group sales are down 12%.

Automotive Industry slumps – one of Victrex’s biggest customers

The automotive industry is one of Victrex’s biggest customers, however 2019 was a very slow year for car manufacturers and retailers.

Notable updates came from Nissan (TYO:7201) who saw their shares slide on November 13, as the firm cut its full year forecast.

Nissan’s demand was hit by a strong yen and falling sales. Its poor performance highlights stagnation in the progression of the global automotive industry.

Nissan outlined a new executive team appointment, who are set to takeover on December 1st following a string of poor performances.

The scale of the recovery that is needed is evident as Nissan reported their second worst quarter performance in 15 years.

After the appointment of Chairman Ghosn, business has gone both after facing falling profits, uncertainty over management and tensions with shareholders.

Additionally, Renault (EPA:RNO) saw its shares in red after the firm cut its 2019 guidance as a result of “less favourable” economic environment.

The firm said it now expects its group revenue to decline between 3% to 4%, “due to an economic environment less favourable than expected and in a regulatory context requiring ever-increasing costs”.

Renault added that its revenue for the third quarter amounted to €11.3 billion, down by 1.6% from the €11.5 billion figure recorded in the third quarter of 2018.

The car manufacturer continued to add that “the Automotive operating free cash flow should be positive in H2 while not guaranteed for the full year”.

Moreover, Renault said that is management will review the “Drive the Future” mid-term plan targets introduced in 2017.

The announcement that Victrex have made today will certainly please shareholders, and gives an opportunity of growth in a young Chinese market.