The Pound fell to its lowest level against the dollar since 1985 today on the back of the US currency’s rising strength and the UK’s gloomy economic outlook.

The Sterling plummeted to $1.1407 and is currently at 1.1448.

The dollar has been growing in strength over recent days, hitting a 24-year high against the Japanese yen earlier on Wednesday.

Meanwhile, the dollar has also strengthened to a near 20-year high against the Euro.

The US Federal Reserve’s hawkish stance on interest rates, alongside the country’s quantitative tightening, have served to send the dollar’s value higher at a time of market uncertainty.

“While UK-based investors will be well aware of how weak the pound is against the US dollar, … sterling is not the only currency whose decline against the greenback is gathering pace,” said AJ Bell investment director Russ Mould.

“The DXY index, which measures the value of the dollar against six major currencies, stands at its highest level since 2002. Investors need to keep a close eye on this, because periods of marked dollar strength in the past have seen chaos in emerging markets, but also weakness in developed market stocks and commodity prices for good measure.”

“The US Federal Reserve’s interest rate increases and acceleration this month of its quantitative tightening programme are, respectively, increasing the returns available on dollars relative to other currencies and at the same time draining dollars from the global economy, to almost create a shortage of bucks.”

Venture capital is in high demand across the Middle East and North Africa region, according to a recent report by the Global Private Capital Association (GPCA).

The sector has a strong appetite for fintech and e-commerce products, with fintech representing 23% and e-commerce accounting for 20% of all MENA venture capital investment since 2020.

GCPA highlighted consumer demand for crypto, digital payments and BNPL as the driving factors behind the thriving market in the area.

Countries with the highest demand levels included Egypt, United Arab Emirates, Pakistan and Saudi Arabia.

The report mentioned the impact of government subsidies on the tech revolution emerging from the MENA sector, diversifying the region’s economies away from oil and gas.

GCPA noted the largest private equity deal in the MENA area was the tech acquisition by Blackstone Group of UAE technology and visa outsourcing services company VFS Global for $1.1 billion in May 2022.

Private Equity activity was also led by Silver Lake’s $800 million investment into Abu Dhabi’s AI and cloud computing firm Group 42 in 2021.

The price of oil fell below $90 on Wednesday, dropping to $89.93 per barrel for Brent crude as demand fears sparked market volatility, fanning the flames of recession fears.

Prices dropped to levels not seen since before Russia’s invasion of Ukraine, with the swing below $90 marking a far plunge from the commodity’s heights of almost $130 per barrel in March.

Lockdowns in the world’s largest consumer China sent demand fears surging across the market, after the country shut down its 21 million population in Sichuan Province capital Chengdu and introduced a tiered restrictions system in tech hub Shenzhen.

China’s growth and production levels have declined over recent months, and the latest lockdowns sent investment bank Noruma’s expectations of the nation’s GDP to 2.7%, representing a drop from its already bleak estimate of 2.8% from its August estimate.

“Back [on Aug. 17], when we cut our Q3 and Q4 GDP growth forecasts, we did not expect growth to worsen at such a pace,” said Nomura chief China economist Ting Lu.

“What is becoming increasingly concerning is that Covid hotspots are continuing to shift away from several remote regions and cities – with seemingly less economic significance to the country – to provinces that matter much more to China’s national economy,” said Nomura analysts.

Experts are warning of a recession coming down the line in winter, exacerbating fears of lowered demand and sending oil prices down lower.

The closure of the Nord Stream 1 pipeline to Germany also served to add fuel to recession projections, according to credit rating agency Fitch on Tuesday.

Meanwhile, the US Federal Reserve is widely expected to hike interest rates following chair Jerome Powell’s hawkish stance at the Jackson Hole convention last month, and the ECB is anticipated to raise its rates aggressively at its next meeting.

GTCR LLC revealed it was considering a bid for GB Group (LON: GBG) after the market closed on Tuesday. The identification services provider says that it will evaluate any proposals it receives. There is no indication of possible terms or valuation. GTCR says that it is acting on behalf of certain affiliated funds. There is no guarantee that there will be a firm offer.

Yacht services provider GYG (LON: GYG) has risen for the second day even though the AIM quotation will be cancelled on Thursday 8 September. JP Jenkins is expected to provide a matched bargain facility before the end of September. The share price is 40% ahead at 35p, having been 21p at the start of the week. The GB Group share price has risen by 22.3% to 638.5p.

Full year results and Cenkos initiating research has helped the Coral Products (LON: CRU) share price to rise 10% to 14.85p. In the year to April 2022, revenues generated by the plastic products manufacturer increased from £10.7m to £14.4m, while pre-tax profit nearly doubled from £760,000 to £1.49m. Earnings enhancing acquisitions have helped to improve the profit and two more have been made since the year end. The total dividend is 1.1p a share. The prospective 2022-23 multiple is less than eight.

Better than expected test results from the East Pepper well in Alberta have pushed up the Arrow Exploration (LON: AXL) share price by 7.25% to 18.5p. Natural gas production peaked at 21,206 mcf/day and averaged 10,921 mcf/day. The ongoing production rate is likely to end up around 7,000 mcf/day. This well should be in production by the end of October. Arrow Exploration expects its total production rate to reach its target of 3,000 barrels of oil equivalent/day by next April.

Synairgen (LON: SNG) says a phase II study trialling SGN001 in patients with chronic pulmonary disease with a confirmed viral infection suggests that human rhinovirus, which 50% of patients had, was cleared more rapidly than in patients treated with a placebo. It also showed that in exacerbating patients there were indications of lower levels of bacterial infection in the second week of treatment. The share price has lost some of its initial gains but is still 3.64% higher at 22.8p.

Panthera Resources (LON: PAT) says that it has made a significant new gold zone discovery at Labola in West Africa. The shares are 7.3% ahead at 7.35p.

Zinnwald Lithium (LON: ZNWD) has published a preliminary economic study on the Zinnwald lithium project in Germany. Post-tax NPV at an 8% discount is $1bn with a 3.3 years payback period following the commencement of production. The project will supply battery grade lithium hydroxide to European battery manufacturers. The initial capital cost is $336.5m. The project could generate an average annual EBITDA of more than $190m. The life of the mine is more than 35 years. The share price is 4.57% higher at 9.15p.

Bluejay Mining (LON: JAY) and Rio Tinto have completed the drilling programme at the Enonkoski nickel copper cobalt project in eastern Finland. This has helped to define new targets. There is a joint venture and earn-in agreement with Rio Tinto. Bluejay Mining has decided to stop exploration at the Muhelampi site at the project, although other areas show promise. There was a negative share price reaction and it fell 9% to 5.75p.

The Verici DX (LON: VRCI) share price has fallen back following the interim figures. The 5.4% fall to 17.5p means that it is back to the level at the start of the week prior to the positive initial results from its validation study for pre-transplant prognostic test Clarava, which was shown to be effective in identifying patients that are likely to reject a transplant. There is net cash of $15.3m, which should last well into next year.

Advertising agency M&C Saatchi (LON: SAA), which remains the subject of two bids, published its interim figures today. Revenues were 10% ahead at £129m, while underlying pre-tax profit was 52% ahead at £16m, thanks to growth in higher margin specialities. However, the reported profit is much lower due to bid-related costs of £9.25m. Net cash was £39.5m at the end of June. Assuming the bids do not succeed a final dividend is expected this year. Forecast earnings are 12.5p a share. Even so, the share price fell 4.5% to 154.9p.

Markets moved into the red as the UK awaited confirmation of the details for Liz Truss’ £130 billion energy relief plan, which would reportedly see the energy price cap frozen or reduced instead of its scheduled 80% rise to £3,548 in October.

The FTSE 100 dropped 0.4% to 7,266.3 in lunchtime trading on Wednesday.

“Action on energy bills continues to be widely trailed as new prime minister, Liz Truss, prepares for an official announcement on her policy,” said AJ Bell investment director Russ Mould.

“Given the big package that is expected, anything short could spark renewed selling in consumer-facing stocks.”

The Pound weakened against the dollar after the US currency strengthened, with the dollar index reaching a 20-year high of 110.69 earlier on Wednesday.

“Sterling remains weak and that is leaving UK stocks vulnerable to approaches from overseas predators – cybersecurity GB Group the latest on the block as it is targeted by a US private equity firm,” said Mould.

“An already shrinking UK tech sector on the London market can ill-afford another departure, GB’s peer NCC is also pulled higher by the news.”

Investment bank Noruma cut its Chinese GDP forecast to 2.7% from 2.8% in August, after the country’s recent lockdown in Sichuan Province capital Chengdu and tightened Covid restrictions in tech hub Shenzhen dealt a blow to analyst estimates.

Noruma reported approximately 12% of China’s GDP was impacted by Covid measures at current time, marking a steep growth from 5.3% last week.

“Back [on Aug. 17], when we cut our Q3 and Q4 GDP growth forecasts, we did not expect growth to worsen at such a pace,” said Nomura chief China economist Ting Lu.

“What is becoming increasingly concerning is that Covid hotspots are continuing to shift away from several remote regions and cities – with seemingly less economic significance to the country – to provinces that matter much more to China’s national economy,” said Nomura analysts.

The Hang Seng dropped 0.8% to 19,044.3 and Chinese-facing stocks dipped on the FTSE 100, with Scottish Mortgage Investment Trust sliding 0.4% to 787.2p and Asia-focused insurer Prudential falling 1.1% to 922.1p.

The group announced a £5.2 billion revenue in FY 2022 compared to £4.8 billion the year before, alongside 17,908 properties completed against 17,243 in 2021.

However, the positive results were marred by signs of a housing market slowdown, with the latest report from Halifax signalling a decline in housing demand on the horizon as the cost of living crisis bites.

House prices reached a new record of £294,260 per average UK property in August, however analysts warned of cooler prices for the red-hot market in the coming months.

“Now the cost-of-living crisis has hit home, and while we may not be forced to face the full impact of rises in energy prices, we’re still having to cope with rampant inflation across the board. At a time of rising rates and higher house prices, this is going to push property out of reach for desperate buyers,” said Hargreaves Lansdown finance analyst Sarah Coles.

“However, we won’t see annual house price rises fall in a straight line. This is partly because of the echoes of the stamp duty holiday last year which created really lumpy price changes a year ago.”

“However, it’s also because the property market is driven to a huge extent by sentiment, and right now, that’s a bit of a rollercoaster ride.”

SulNOx announced its new partnership with Rominserv on Wednesday, marking the company’s first large scale agreement with a major petroleum firm.

Rominserv, which currently operates as part of the Romanian crude oil company Rompetrol Group, signed a Memorandum of Understanding (MoU) for SulNOx to initially review and advise on the use of its products within the Rominserv refinery processes.

The collaboration will include the use of Heavy Fuel Oil in burners, tank cleaning and waste oil processes at its refineries, development of new and enhanced “green” Marine Gas Oil products and Green Fuel additives.

Rompetrol currently operates across 12 countries with $4.6 billion in FY 2021 revenues. The firm develops, produces and refines crude oil, alongside operations marketing and distributing refined petroleum products via its chain of over 1,100 gasoline and diesel fuel stations in Romania, Georgia, Bulgaria, Moldova, France and Spain.

“As the first significant petrochemicals company to work with SulNOx, we are genuinely thrilled by this collaboration agreement with Rominserv,” said SulNOx Group CEO Ben Richardson.

“I applaud the Rompetrol management team for looking to SulNOx green technologies to develop solutions to benefit a consumer base which is increasingly demanding greener fuels.”

SulNOx shares were down 0.6% to 12p in late morning trading on Wednesday.

The lockdown of Sichuan Province capital Chengdu last week sent fears for production surging as the 21 million population joined a continued shutdown for tech hub Shenzhen.

Nomura confirmed approximately 12% of China’s GDP was currently impacted by Covid measures, representing a sharp rise from 5.3% last week.

Nomura used a new model which weights the GDP of affected regions by how tight the Covid measures are.

According to the investment bank’s report, the country’s GDP is now forecast down to 2.7% compared to previous expectations of 2.8% announced in August.

“Back [on Aug. 17], when we cut our Q3 and Q4 GDP growth forecasts, we did not expect growth to worsen at such a pace,” said Nomura chief China economist Ting Lu.

Nomura has often led the pack in cutting estimates for the country before other investment banks, however institutes across the board have been reducing projections for China repeatedly over the last several months.

Nomura currently has the lowest forecast for China among its contemporaries.

The bank said its new model demonstrated China’s GDP was rapidly approaching levels seen over the Shanghai lockdown in April and May, at which time the weighted impact on GDP was slightly above 20%.

“What is becoming increasingly concerning is that Covid hotspots are continuing to shift away from several remote regions and cities – with seemingly less economic significance to the country – to provinces that matter much more to China’s national economy,” said Nomura analysts.

The Pound fell to 1.14922 against the dollar in late morning trading on Wednesday as the dollar strengthened.

The Sterling hit a low of 1.14545 earlier in the morning, marking a fall from its high of 1.1609 on Tuesday after reports emerged regarding new Prime Minister Liz Truss’ £130 billion relief plan to freeze or reduce energy bills for UK households.

The Pound has so far taken a 15% blow against the dollar year-to-date as the Ukraine war continues to rain bad news on the European continent.

Rising energy prices and food cost inflation have triggered a cost of living crisis which has only exacerbated the double hangover of Covid and Brexit, the effects of which are still impacting the UK.

The currency was also weakened as analysts pointed out the uncertain effect of Truss’ energy policy combined with the next Bank of England interest rates move.

“The net impact of support measures may not be too straightforward as they may easily get mixed in with the implications for BoE policy,” said ING analysts.

Meanwhile, the US dollar index reached a 20-year high of 110.69 earlier on Wednesday.

WH Smith shares slid 2.8% to 1,436.6p in early morning trading on Wednesday, after the franchise reported strong FY 2022 travel sector performance, alongside a HY2 impact to its high street business following disruptions to its funkypigeon.com greeting card segment.

WH Smith confirmed its FY 2022 trading was in line with management expectations, with HY1 total group revenue against 2019 levels reaching 84%.

Travel across HY1 hit 82% of 2019 levels, alongside an 86% result across its high street sector.

Meanwhile, WH Smith confirmed HY2 total group revenues hit 112% of 2019 revenues, along with 129% in travel and 80% in its high street business.

“After June’s impressive trading update, expectations were perhaps running too high for WH Smith, with investors today seemingly disappointed it hasn’t raised guidance once again in its latest update,” said AJ Bell investment director Russ Mould.

“Given the fragile nature of the retail sector, the fact it remains on track must be seen as a positive, particularly when you consider that plenty of other companies on the high street or selling goods online have started to show cracks, with profit warnings creeping out.”

The company said its travel sector benefited from continued recovery in passenger numbers across all its key markets. The firm noted strong ATV growth and higher penetration, driven by its strategy to develop and enhance its ranges, including technology, and health and beauty.

“WH Smith’s business model is split into two – one part is to generate as much cash as possible from the high street stores and just keep them ticking over without expecting too much growth. The other, more exciting, part is to use the travel shops as the growth engine for the group,” said Mould.

“The fact travel sales are now above pre-pandemic levels is very encouraging as it shows its strategy of rolling out new stores and reengineering existing ones to include broader categories such as health and beauty is working.”

WH Smith reported strong recovery across the UK and US, with initial slower recovery in the rest of the world. However, Europe displayed the strongest recovery overall in FY 2022, with high growth levels in Australia and Asia.

The franchise noted a focus on cost efficiencies and the return on space in its high street sector, and announced further cost saving opportunities, most notably through rent reductions.

“There are still some levers it can pull to enhance the financials from the high street shops such as find more places to cut costs including deals with landlords to cut rent. The travel business is all about being clever with the floor space and planting as many new flags as possible around the world,” said Mould.

“For a business that most people associate with selling the Radio Times and a big packet of felt tip pens, there’s no getting over the fact that it has managed to move with the times and turn a seemingly tired brand into an ever-expanding retail group.”

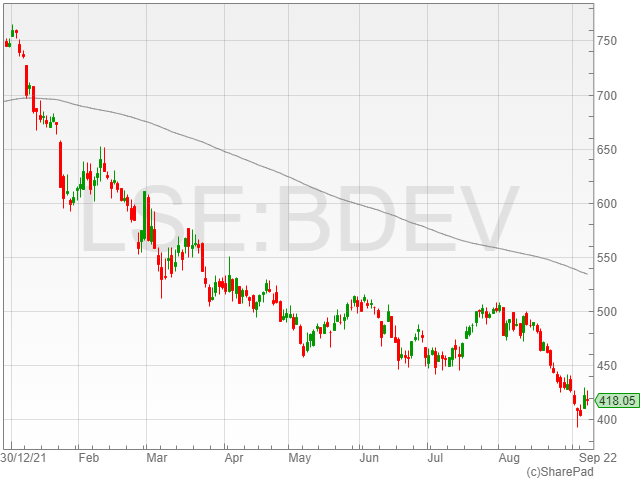

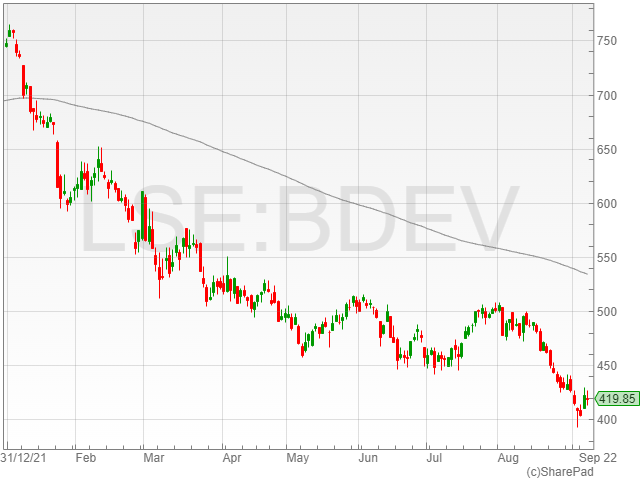

Barratt Developments shares dipped 0.8% to 418.6p in early morning trading on Wednesday, after announcing a statutory pre-tax profit of £642 million in FY 2022 against £812 million the last year.

The company highlighted revenues of £5.2 billion in FY 2022 against £4.8 billion the last year.

Barratt Developments reported total home completions of 17,908 compared to 17,243, marking a recovery to pre-pandemic levels. The group confirmed a targeted 3% to 5% growth in total home completions in FY 2023, representing between 18,400 and 18,800 houses.

The firm mentioned a statutory profit from operations decline to £646 million from £811 million, along with an operating margin slide to 12.3% compared to 16.9%.

Barratt Developments announced an adjusted profit from operations rise to £1 billion from £919 million, alongside an adjusted operating profit margin of 20% compared to 19.1%.

The group noted a basic EPS fall to 50.6p against 64.9p year-on-year, and an adjusted EPS of 83p compared to 73.5p.

The company also highlighted a ROCE of 30% against 27.8% in FY 2022.

Barratt Developments confirmed net cash of £1.1 billion from £1.3 billion the year before.

“This has been a year of fantastic progress, with completions recovering to pre-pandemic levels and excellent productivity across our sites,” said Barratt Developments CEO David Thomas.

“Our financial strength and operational excellence position us well to navigate the macro-economic uncertainties ahead.”

“I’d like to thank our employees, sub-contractors and supply chain partners for helping us to continue to deliver the industry-leading, sustainable homes and developments our customers want and the UK needs.”

Barratt Developments hiked its dividend 25.5% to 36.9p against 29.4p in the previous year.