The FTSE 100 was up over 1% in early afternoon trading on Tuesday as markets were pulled up by mining companies on hopes of growing future demand for raw materials.

The G7 $600 billion plan to fund infrastructure in developing countries over the next five years served to send commodities groups surging as investors leapt to the sector.

“Periods when the FTSE 100 rises in the region of 1% in a day should be celebrated given how this year has been so gloomy for investors. Today, the fireworks are most definitely lighting up the sky and the UK market is regaining its mojo,” said AJ Bell investment director Russ Mould.

“Miners revved their engines yesterday following the G7 $600 billion infrastructure plan and were striking more gold today as investors continue to flock to the sector.”

Anglo American shares gained 1.8% to 3,191.7p, Antofagasta rose 0.3% to 1,227.2p, Croda saw an uptick of 0.4% to 6,409p, Endeavor increased 1.4% to 1,770.5p, Glencore soared 2.7% to 465.1p and Rio Tinto climbed 3% to 5,202.5p.

The price of oil increased to $117 per barrel for benchmark Brent Crude, sending Shell and BP shares up 3.2% to 2,181p and 3% to 403.3p, respectively.

China eases Covid-19 restrictions

Meanwhile, China-focused stocks saw an uptick as the Chinese government eased Covid-19 quarantines to ten days rather than three weeks for visitors entering the country.

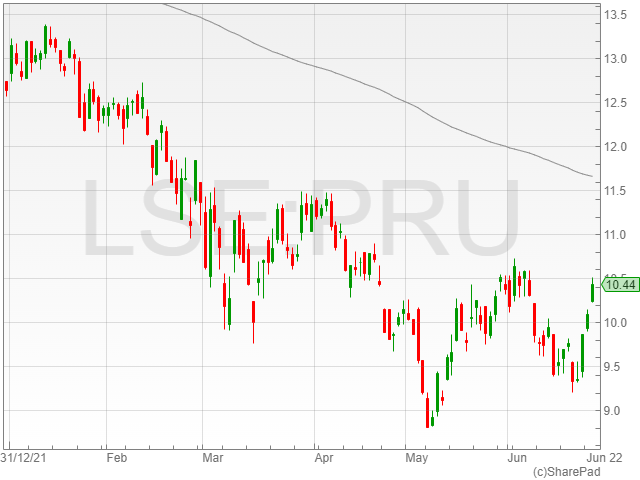

Asia-focused insurance company Prudential gained 3.4% to 1,044.2p and the Hang Seng increased 0.8% to 22,418.9.

The prospect of fewer disruptions to global production also served to boost US markets, with NASDAQ pre-market trading up 0.5% to 12,099.7 and the Dow Jones up 0.5% to 31,604.

“Perhaps helping the cause was news that China would reduce the Covid quarantine period for visitors from overseas, perhaps a sign that the Asian superpower’s extra tough pandemic measures might be relaxed going forward,” said Mould.

“That would help to alleviate fears that commodities demand would be weaker from China if it shut up shop every time a new Covid wave came.”

Utilities fall

Utilities dropped as JP Morgan downgraded Severn Trent, with the group’s shares falling 4.9% to 2,711.5p. The move triggered a dip in United Utilities shares, which dipped 1.2% to 1,021.7p.

“Utilities were out of fashion following a broker downgrade on Severn Trent,” said Mould.

“JPMorgan moved to an ‘underweight’ position on the stock, triggering a 4.2% decline in the share price. United Utilities fell in sympathy.”