No-deal fears cause UK equity fund exodus

Mounting fears of a no-deal Brexit scenario have caused UK equity funds to shed more than $2bn in the past two months, as investors opt to put their money elsewhere amid doubts over a sustained FTSE recovery.

Data from financial intelligence agency EPFR Global revealed that $2.4bn has been withdrawn from funds exposed to the UK stock market since the beginning of October, taking the net total of equity fund outflows since the Brexit referendum to $42bn – almost 17% of the assets recorded in June 2016.

Continued uncertainty about the outcome of UK-EU negotiations has also dealt a blow to the appeal of UK stocks, with portfolio managers opting to invest their funds in sturdier markets. The average level of UK exposure in global equity funds slid to an all-time low of 5.8% in 2020, compared to almost 9% at the start of 2016, according to fund performance analyst Copley Fund Research.

Chief executive at Copley, Steven Holden, attributed the decline in appeal to “the uncertainty surrounding a post-Brexit trade deal and ongoing Covid-19 concerns”.

Ongoing talks between the European Union and the UK government have so far failed to produce a post-Brexit trade deal, with the UK set to leave the EU on the 31 December – regardless of whether a plan has been put in place or not. Both sides have warned that a no-deal scenario has become increasingly likely in recent weeks.

Ahead of meetings on Sunday, Prime Minister Boris Johnson warned of a “strong possibility” of a no-deal Brexit.

This weekend was initially proposed as the “final deadline” to reach an agreement, but the PM and European Commission President Ursula von der Leyen released a joint statement on Sunday evening confirming that talks will continue as both leaders butt heads over “major unresolved topics”.

A fatal combination of Brexit uncertainty and Covid-19 anxiety has seen the FTSE All-share index down 12% since the beginning of 2020, and although some hedge fund managers – including Marshall Wace – have begun betting on an imminent rebound, global equity managers have still noticeably cut back their exposure to the UK stock market across a number of sectors.

Just 28% of the funds recorded by Copley’s survey currently have exposure to UK energy companies, down from 46% at the start of 2019. Similarly, 51% of funds are invested in UK financial stocks, compared to 64% in 2018.

Portfolio managers are increasingly turning to tech and consumer goods stocks, such as Chinese e-commerce tycoon Alibaba and JD Sports.

Despite the overarching anxiety surrounding Brexit negotiations, the EPFR recorded a slight surge in investments at the start of the week, with about $100m pumped into UK equity funds in the lead up to Wednesday.

Brexit Deal blocked by ‘dynamic’ standards issue

Likely not much of a surprise to many readers, but the Brexit posturing continued from both sides this week – meaning any possible Deal will now be struck at the ‘eleventh hour’. With the prospect of a blockbuster end to the year, a lot of discussion is being had about fishing rights and state aid, but not enough is being said about the ‘dynamic’ standards impasse.

Alan Farkas, Partner at Dorsey & Whitney – a law firm specialised in advising companies on the Brexit transition – spoke to the UK Investor Magazine about the sense of “deep gloom” that now presides over the issue of standards alignment, despite potential for compromise on the fishing and state aid issues.

Fishing rights and ‘value of catch’ proposition

Speaking back in October, a French source told the Express that President Macron occupies an unenviable position, with fisherman in Northern France likely to blame him for a loss of business incurred either by concessions being made or a No-Deal scenario. The source said that: “If there is no deal, he will be made responsible – and it’s even worse for French fishermen.”

European affairs minister, Clement Beaune, added that: “Our fishermen will not be a bargaining chip for Brexit, they will not have to pay the price for Britain’s choices.”

“A bad deal would be the worst outcome. And so we are ready for a no-deal scenario, and we will not accept a bad compromise.” He continued.

The seeming intractability of the fishing rights stalemate seems to have been reinforced by a lack of progress during this week’s talks, and the UK’s decision to send four naval vessels out to defend its fishing waters. However, Mr Farkas notes that the situation is ‘potentially soluble’ with a 5-7-year transition period, and quotas based on ‘value of catch’ and allocated between individual fish stocks.

“Britain is believed to be prepared to allow European trawlers to retain up to 47% of the value of certain fish stocks from 1 January,” Farkas says.

State Aid and the COVID bail-out

In short, the EU’s definition of state aid covers all spending which potentially distorts trade between countries, such as tax advantages offered to only a small subset or sector of business. While initially broad-reaching, the practical restrictions on state aid feature a lot of exemptions.

For instance, the General Block Exemption Regulation means that spending on regional aid, training, SME subsidies, R&D, environmental aid and public infrastructure aid are all permissible. Further, the ‘de minimus’ rule means subsidies under €200,000, over three consecutive years and to one company, do not require sign-off by the European Commission.

While these considerations may take some of the initial sting out of the state aid impasse, any worthwhile Brexit deal would shoot down the EU’s current demand. That being: the EU wants the UK to agree to limits on its ability to directly subsidise British industries, while exempting the EC from all state aid provisions. In essence, this framework would allow the EU to subsidise industries at its leisure, while the UK doing the same thing would mean it breaches international law.

This issue is particularly important given our current context, which finds many sectors of the UK economy disproportionately impacted by the COVID-Brexit double-edged sword – and thus in acute need of public support. Issuing a glimmer of hope, Mr Farkas continues: “Possible compromises have been discussed, allowing the UK Government to provide State subsidies of an equivalent proportion to the amount of the [EU Coronavirus] recovery fund.”

Dynamic regulation and intractable Brexit philosophies

The most intractable issue, and one that has not received enough coverage, is the discussion over forward-looking changes to trading, work and goods standards. The debate over the ‘dynamic’ alignment of standards centres around the EU position that any future adjustments to EU regulations ought to be mirrored by UK regulations.

For proponents of the UK sovereignty argument, and those alive long enough to remember the series of Factortame cases, the upshot of ‘dynamic’ standards is rather predictable. Under such as system, the UK would either have to comply with EU policy, or find itself back in a European court, once again scolded by EU lawmakers, and with the possibility of further tariffs being imposed for non-compliance.

Farkas said that: “In an effort to make progress, the UK have conceded that there should be no reduction in existing rules and regulations. These “non-regression clauses” on standards will be part of any trade deal and should there be future disputes between the UK and EU, procedures to adjudicate such disputes will be included in any treaty based on objective measures of actual disruption to trade. This is however as far as the UK Government are prepared to compromise.”

“The latest EU request for dynamic alignment impinges on what the UK Government sees as the fundamental reason for leaving the EU, allowing the UK sovereignty over its own laws.”

He continued by saying that it seems “almost unconscionable” that an agreement reportedly so close to completion, should collapse on disagreements over regulations – on which the UK currently remains a “leading force”. Unfortunately, both sides have deep-seated and valid philosophical justifications for their positions. On one side, we have the Brexit raison d’être – UK sovereignty – and on the other – granting access to the world’s largest, high-standards single market.

Unfortunately, Farkas says that while small compromises might occur between Christmas and New Year, he believes we are now in the “blame game” territory – with neither side wanting to be seen as walking away from what might in hindsight be seen as the basis for a potential deal. Should a No-Deal transpire, the recent exodus from UK equity funds would suggest that the near-term prognosis for FTSE blue chips is not positive, while private investors remain positive about the prospects of domestically-focused SMEs in the New Year.

Brexit No-Deal could upset FTSE value stock rally

Capping off an altogether mixed week, FTSE indexes finished Friday with a slump, having decided to go into the weekend with the prospect of a No-Deal Brexit as the main takeaway.

Down by 0.80%, the FTSE 100 reversed its mid-week gains and finished at 6,546 points, just shy of where it began on Monday. Meanwhile, the FTSE 250 dropped by 0.68%, to 19,622 points – more than 500 points below its Monday open, following a rough week for the index.

The story on Friday was disappointingly glum, what with the first COVID vaccines being rolled out just a couple of days prior, and a low pound and new trade deals with Singapore and Vietnam, all looking to jack up the sentiment towards UK equities.

Alas, it was the continuing Brexit impasse, and increasing likelihood of a No-Deal scenario that ruled traders’ thoughts at the end of the week. Speaking on the FTSE’s underwhelming performance, and the likelihood of No-Deal, IG Senior market Analyst, Joshua Mahony, said:

“Wednesday’s Brexit dinner appeared to provide little more than clarity that both sides remain as far apart as ever, with a growing consensus that a no-deal Brexit now appears to be the most likely eventuality.”

“Sceptics will see the current impasse as a way to fame any eventual deal as a success on both sides, yet we have just three weeks to both finalise and sign off a deal that needs to pass through all 27 EU nations.”

“From a market standpoint, the value-led recovery seen over the past month is coming into question, with the FTSE 250 outperformance likely to reverse if a no-deal Brexit comes back to hurt domestically-focused firms.”

The situation was hardly peachy for the UK’s largest international financiers, either. Despite the Bank of England lifting the ban on bank dividend payments on Thursday, Lloyds shares fell almost 4.5%, while NatWest shares shed more than 6.60%.

“The prospect of a no-deal Brexit is doing little to bolster optimism for the UK banks, with the likes of Lloyds, NatWest, and Barclays leading the FTSE losses in early trade”, Mr Mahony added.

“The latest BoE financial stability report highlighted that banks are in a very healthy position as they head into what could be a very turbulent few months.”

“However, with the government having staved off a wave of insolvencies and administrations through the pandemic, the next question is just how they can avoid any short-term economic suffering that could come with a disorderly exit from the EU.”

Finishing on a smaller and brighter note – should a No-Deal Brexit materialise, some investors are heartened by the opportunities this could offer UK-focused SMEs and micro-caps, especially given that the potential for tariffs may give them a price advantage in the domestic market.

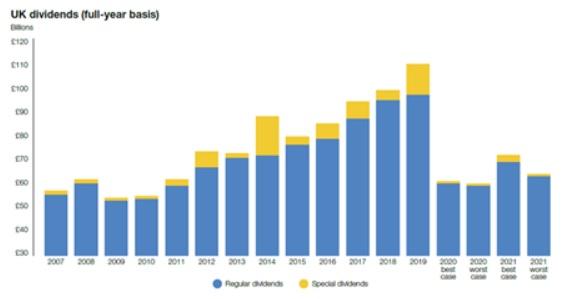

Unfreezing bank dividends: wise or woeful?

With bank pay-outs on ice, Q3 dividends hit their lowest level since the financial crash aftermath in 2010 – down by 49.1% on a headline basis, to £18.0 billion.

Of the estimated £14.7 billion of cuts during the third quarter, some two fifths of this number came from bank dividend reductions, due to Bank of England restrictions. Similarly, chopped oil and mining dividends accounted for one fifth and one eighth of cuts respectively.

While two-thirds of companies cutting or cancelling their dividend sounds drastic, these figures are certainly more modest than the second quarter, where dividends dropped by 57.2% and 75% of companies cut or cancelled their coveted investor income.

According to Link Group, the hardest-hit areas were airline, travel, leisure, general retail, media and housebuilding. Within travel and retail in particular, pay-outs fell year-on-year by 96%, while dropping by approximately two-thirds in the remaining sectors. Meanwhile, food and basic consumer goods retailers increased their pay-outs, and BAE and IMI caught up on all the dividends they missed during the year-to-date.

The question is: following the Bank of England’s recent decision, was it right to remove the ban on banking sector dividends?

On the one hand, reinstating payments will likely provide lenders and savers with additional cash. On the lender side (banks), dividends returning will likely encourage investors to look towards the biggest financial stocks on the FTSE for reliable, long-term investment. This may in turn drive up banks’ share prices, and give banks the capital flexibility to be more generous with products such as mortgages or business loans (whether this comes to fruition is another story).

On the saver side, those with financial equities in their pension pots will benefit from the extra income which will be compounded and used to build up their retirement funds.

Now, on the other hand, while encouraging investors capital to flow into banks, reinstating dividends also – inevitably – come at a cash cost. As stated by Positive Money Executive Director, Fran Boait: “It is deeply concerning that the Bank of England is pandering to commercial banks and allowing them to prioritise shareholder payouts instead of supporting the Covid-19 recovery.”

“The Bank rightly suspended dividend payouts in March to make sure lenders were preserving capital to support struggling households and businesses across the economy. Private banks have been lobbying to overturn this intervention ever since, proving once again that they cannot be trusted to work in the public interest, even during a global pandemic.”

“The Bank is now also considering watering down its guidance on limiting executive bonuses. With considerable economic uncertainty and unemployment set to rise sharply, this would be premature and irresponsible.”

Rolls-Royce shares slide ahead of tough recovery

FTSE 100 listed engineering firm, Rolls-Royce Holdings plc (LON:RR), watched its shares drop around 9% on Friday, as the company laid bare the challenging year its had, and the harsh realities of restructuring.

During the 11-month period to the end of November, the company reported that large engine LTSA invoiced flying hours fell to approximately 42% of what they were the year before. Rolls-Royce said that although flying hours had picked up since April, the pace of recovery has since dropped, as a result of a second wave of infections in some geographies.

During Q3, large engine flight hours were around 29% of what they were the previous year, though this was a marked improvement from Q2, where traffic was just 24% of what it was in 2019. As a result of the slowing recovery, the company said its guidance remains unchanged, though it has reduced the pace of it large-engine production.

Speaking on its other business segments, Rolls-Royce said that business aviation has been less impacted than commercial flights, in spite of border restrictions coming into force in many regions. Similarly, it said that its defence business has remained ‘resilient’, with a strong order book – including 56 EJ200 jet engines bought by the German Air Force – and an encouraging 2021 forecast (partially led by the UK’s bolstered MoD budget).

Its Power Systems business saw a ‘significant fall in demand’ in non-governmental sectors during 2020, with some signs of recovery during the second half, spearheaded by the Chinese market. On a brighter note, its Small Modular Reactor consortium benefitted from the increasing favour for nuclear power, securing strategic agreements with Exelon Generation and CEZ, and the UK Government signing a £215 million four-year development deal.

Speaking on the company’s performance and the long road to recovery, Rolls-Royce CEO, Warren East, said: “We have made rapid progress on our restructuring programme and the consolidation and reorganisation of our Civil Aerospace footprint is well underway. Our £5 billion recapitalisation package in November was well supported and has increased our resilience and strengthened our balance sheet. The outlook remains challenging and the pace and timing of the recovery is uncertain. However, our actions have given us a strong foundation to deliver better returns as our end markets improve and we continue to drive our ambition of delivering more sustainable power to support the creation of a net zero carbon economy.”

With its credit facilities in mind, and excluding lease liabilities of around £2.1 million, and liquidity of up to £9.0 billion, the company expects to end the year with net debt of between £1.5 billion and £2.0 billion.

Rolls-Royce added that on the whole, “The pandemic is causing a reduction in demand for our Civil Aerospace products and services that we expect will take several years to recover”.

The upshot of this view has been the company’s ‘major reorganisation’ programme, announced on May 20. Having made progress towards its £1.3 billion cost saving target, the company says it will have to cut 9,000 jobs by 2022, with the 5,500 job losses expected by year-end being 500 more severe than the previous estimate of 5,000 redundancies.

Though undergoing a process of consolidating the manufacture of its aero-engine structures into ITP Aero, the company is actually considering of disposing of ITP Aero altogether, having just confirmed the £2 billion disposal of its nuclear instrumentation and control business.

Commenting on challenging road ahead for Rolls-Royce, Third Bridge Senior Analyst, Ben Nuttall, said: “Rolls Royce’s cash receipts will recover as the world starts to fly again.”

“Recent vaccine news creates an interesting upside case for Rolls Royce, which could see a quicker end to this period of high cash burn without them having to raise further liquidity.”

“Rolls Royce is experienced at restructuring. The company undertook major restructuring after the financial crisis in 2010, then again in 2013 and 2016. They know how to make significant savings, but the aerospace giant will still have to navigate a bumpy period of operational challenges.”

Following the rather sombre update, Rolls-Royce shares dropped by 8.98%, down to 115.60p a share 11/12/20 12:30 GMT. The Marketbeat community issues a 70.54% ‘Underperform’ rating on the stock, while analysts give the stock a consensus target price of 393.17p a share, and a Hold stance.

Airbnb achieves biggest US flotation of 2020

Airbnb shares more than doubled on Thursday on the company’s Wall Street debut, valuing the group at $100bn.

Shares opened at $146, well ahead the initial public offering (IPO) price of $68. The stock soon after hit a high of $165 and marked the biggest US floatation of 2020.

Brian Chesky, Airbnb’s chief executive officer, commented on the surge in share price: “I don’t know what else to say. I’m very humbled by it.”

Based on Thursday’s share price, Airbnb’s three co-founders will become multi-billionaires.

Chesky founded the company in 2008 in his San Francisco apartment. The company now has over seven million short-term listings worldwide.

Commenting on Airbnb’s IPO, Jay Ritter, a finance professor at the University of Florida, said: “20 years ago in the internet bubble as similar things were going on. [Airbnb’s] valuation numbers being talked about a month ago, a week ago, were nowhere close to the numbers today. It’s a great company, but that high a valuation is pretty remarkable.”

In November, the group posted a $697m (£527m) loss for the nine months to the end of September. The loss has widened from the $323m loss that was posted for the same period a year earlier.

Whilst proving to be wildly successful, Airbnb has come under fire and has not gone without its controversy. Residents and local governments in many cities are cracking down on the group due to its impact on the local residents.

This week also saw Amnesty International call on the group to remove the 200 rental listings in the illegal Israeli-occupied Palestinian Territories.

Saleh Higazi, Amnesty International’s Middle East deputy director, said: “No company should be party to human rights abuse and until Airbnb ends its business relationship with the Israeli settlements it will be deeply compromised.”

Sterling tumbles on no-deal Brexit risk

Following the news that the likelihood of a no-deal Brexit is a “strong possibility”, the pound was down almost 0.4% against the euro to 1.091.

European Commission president Ursula von der Leyen told EU leaders on Friday: “The probability of a no deal is higher than of a deal…To be seen by Sunday whether a deal is possible.”

Susannah Streeter, a senior investment and markets analyst at Hargreaves Lansdown, said:

“With the UK now looking like its hurtling towards a no-deal Brexit, investors should adopt the brace position for swings in sterling and shares in domestic focused companies. This morning the pound is struggling to rise above 1.09 against the euro with a distinct lack of direction before the fresh deadline of Sunday looms.

“Warnings from Prime Minister Boris Johnson, that companies should prepare for a no-deal scenario, will not have added to confidence, given that there are just three weeks until January 1, when WTO rules would come into force.”

As well as the pound, European stocks were also down on Friday’s opening. The FTSE 100 is down 0.4%, Germany’s DAX is 0.3% lower, France’s CAC 40 is down 0.27%, and Spain’s IBEX opened 0.4% lower.

Michael Hewson, CMC Markets UK’s chief market analyst, remains confident that a deal could still be struck and said:

“Overall, there still seems to be some optimism that pragmatism will prevail as the 31st December deadline gets closer, and the realisation slowly dawns of the potential economic damage that could ensue in the days after a no-deal outcome.

“An outcome that in the current circumstances would simply heap economic pain on top of economic pain.”

This week, the UK has signed free trade deals with Singapore, Vietnam, Norway, Iceland, and Canada. The deals have come just weeks before the end of the Brexit transition period.

The Vietnam embassy said in a statement: “Today, UK International Trade Secretary Liz Truss and Vietnam Minister of Industry and Trade Tran Tuan Anh concluded the UK-Vietnam Free Trade Agreement. This will be a further boost to UK-Vietnam bilateral trade, which has tripled between 2010 and 2019 to £5.7bn ($7.58bn)”.

UK signs free trade deals with Singapore & Vietnam

The UK has signed free trade deals with Singapore and Vietnam.

The deal with Singapore was announced on Thursday and covers a trade relationship worth over $22bn (£17bn) and is similar to the trade relationship the country currently has with the EU.

The deal between the UK and Vietnam was concluded on Friday, just weeks before the UK’s transition period ends.

The embassy said in a statement: “Today, UK International Trade Secretary Liz Truss and Vietnam Minister of Industry and Trade Tran Tuan Anh concluded the UK-Vietnam Free Trade Agreement. This will be a further boost to UK-Vietnam bilateral trade, which has tripled between 2010 and 2019 to £5.7bn ($7.58bn)”.

Earlier this week the UK announced trade deals with Norway, Iceland, and Canada.

For the UK’s deal with Singapore, the agreement means the removal of tariffs and will enable both countries with access to each other’s markets in services. In addition, the deal will cut non-tariff barriers for pharmaceutical products, medical devices, renewable energy generation, and electronics, cars and vehicle parts.

The news of the various trade deals comes as Boris Johnson has said that the likelihood of a no-deal Brexit is a “strong possibility”.

Following talks with the European commission chief, Ursula von der Leyen, Boris Johnson said the EU’s current offer was unacceptable.

“It was put to me that this was kind of a bit like twins, and the UK is one twin the EU is another, and if the EU decides to have a haircut then the UK is going to have a haircut or else face punishment. Or if the EU decides to buy an expensive handbag then the UK has to buy an expensive handbag too or else face tariffs.”

“Clearly that is not the sensible way to proceed and it’s unlike any other free trade deal. It’s a way of keeping the UK kind of locked in the EU’s … regulatory orbit.”

Adding the likelihood of a no-deal Brexit, Boris Johnson said:”There’s a strong possibility that we will have a solution much more like Australian relationship with the EU than a Canadian relationship with the EU.”

RWS shares fall on full-year results

RWS Holdings shares opened 4.47% lower on Thursday after the group posted results for the year ended 30 September 2020.

The provider of language services and language technology shared a 5.5% fall in adjusted profit before tax to £70.2m.

The RWS Life Sciences division saw increased revenues of 6% to £69.5m, which was a record high thanks to growth in all key areas and particularly linguistic validation services.

Andrew Brode, Chairman of RWS, commented: “The Group has delivered a resilient performance, reflecting its diversified revenue streams across its three specialized divisions, with stronger levels of activity in Life Sciences and Moravia mitigating headwinds in IP Services.

“The Group’s focus on Life Sciences and technology customers, who are thought to be likely beneficiaries in a post Covid-19 world, and the importance to our customers of managing their research and development investments through a strong global patent strategy, puts RWS in a strong position.

“The merger with SDL offers an unrivalled opportunity to consolidate the Group’s world-leading language services offering and provide our extensive blue-chip client base with best in class solutions for all of their language requirements.

“The new financial year has begun positively, slightly ahead of our expectations. We have no net debt and whilst our focus is on integrating SDL, our strong balance sheet places us in pole position to compete for the most attractive acquisition opportunities,” he added.

RWS has proposed 7.25p, which is a 3.6% increase on last year.