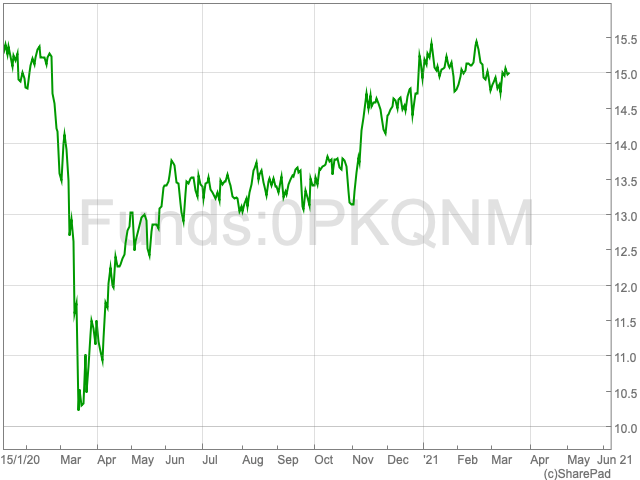

Rio Tinto Share Price

At one point, Rio Tinto (LON:RIO) doubled its valuation over the past year, from 3,212p per share in March 2020 to 6,352p per share in February 2021, as a result of a sharp rise in commodity prices.

During March 2020 the Rio Tinto share price has seen a dip, to 5,496.82p per share, which was caused by iron ore prices dropping from recent highs.

Results

Rio Tinto announced in February a 22% rise in annual net profit of $9.77bn for 2020 , up from $8.01bn the year before. The world’s leading producer of iron ore also reported a 20% increase in underlying earnings to $12.45bn, above analyst forecasts of $11.75bn. While its revenue in 2020 grew by 3.3% year-on-year to $44.6bn.

In addition to a positive cash flow in each of the past five years, Rio Tinto’s free cash flow was $9.4bn in the 2020.

Rio Tinto revealed a record $6.5bn final dividend, or $3.09 a share, plus a one-time payout of 93 cents per share. In addition to the company’s half-year dividend, Rio Tinto’s payout for the financial year amounted to $9bn.

Production

Rio Tinto maintained expenditure of $625 million on exploration and evaluation, as the company progressed its greenfield programmes and other evaluation projects, in particular Resolution Copper in Arizona, Jadar lithium-borates in Serbia and Winu copper-gold in Western Australia.

The FTSE 100 mining company also is due to start negotiations with the government of Mongolia as it seeks to complete the $6.75bn expansion of a large-scale copper project in the Gobi dessert.

Commodities

Iron ore’s price thrived throughout 2020, and Rio Tinto’s outlook will depend on whether or not the commodity can continue its rise into 2021, as it makes up 63% of the mining company’s revenue.

However, a recent pollution crackdown by China began to suppress the price of iron ore. There are now question marks over the future prospects of the commodity, which could in turn lead to concerns over the FTSE 100 company’s future prospects.

Having risen from $80 per tonne in March 2020 to nearly $180 per tonne a year later, the commodity has retreated following China’s new policies.

Nicholas Snowdon, analyst at Goldman Sachs, predicts the Chinese government will increasingly look to limit emissions which will cap the production of iron ore, causing downward pressure on the price of the commodity.

“We now see iron ore prices turning lower in the coming months,” said Snowdon, who has set a 12-month price target of $100 a tonne. “This reflects mounting evidence that supply is shifting toward a sustained recovery and also that China’s environmental policies will reinforce a peak in iron ore imports.”