Wizz Air swings to loss after 70% passenger plunge

Wizz Air (LON: WIZZ) has reported a €243.1m (£219m) for the six months ended 30 September 2020.

The budget airline carrier had a 70% plunge in passengers in the period, down from 22.1 million for the same six months the previous year.

Revenue at the group also fell by 71.8% from €1,670.8m to €471.2.

József Váradi, Wizz Air Chief Executive commented on the results: “Wizz Air distinctly outperformed the industry in the second quarter of the current financial year: we carried 5.8 million passengers at 66% load factor and 72% of our 2019 capacity against an ever-shifting backdrop of travel restrictions across all of our markets.

“Our ancillary revenues continue to increase on a per passenger basis, driven by a resilient performance of our core products. At the same time, our disciplined cost management allowed us to sustain our investment graded balance sheet with a total cash balance of €1.6bn.”

Wizz Air has warned that the upcoming quarter is likely to be a “challenging” one, amid the travel restrictions on top of the seasonal drop in travel.

“Notwithstanding the challenges that lie ahead of us during the remainder of this fiscal year, we have laid the foundation for a swift recovery: in addition to expanding into new markets, we intend to retain all our current staff base and thereby generate a head start for when demand returns,” said Váradi.

“We are confident we will emerge as a structural winner, enabling Wizz Air to grow profitably in the years to come.”

Over the past six months, the airline achieved significant expansion and added 13 new bases as well as 29 aircrafts.

Wizz Air shares (LON: WIZZ) have fallen 10% from a year high in February of 4,526.00p. They have since largely recovered and are currently trading at 3,498.00p (0815GMT).

Uber shares motor ahead 14% with drivers to be classed as contractors in California

Shares of ride hailing apps Uber (NYSE:UBER) and Lyft (NASDAQ:LYFT) shot up well over 10% on Wednesday, as the companies won bids to continue classifying their drivers as independent contractors in the state of California.

The development marks the overturn of what the BBC described as a ‘landmark labour law’, which was passed in 2019 and ruled that gig economy workers should have employee status and the requisite protections and rights that accompany that status.

Opposing that statement, a coalition of gig workers opposing the motion said that: “Billionaire [corporations] just hijacked the ballot measure system in CA by spending millions to mislead voters,”

“Uber, Lyft, & the other gig [companies] took a ballot measure system meant to give voice to ordinary Californians and made it benefit the richest [corporations] on the planet.”

Today’s measure – named Proposition 22 – was backed by ride-hailing apps, and cost companies some $205 million, the most expensive in state history. And, while some drivers backed the motion, labour groups stood in opposition, saying that employee status would guarantee rights such as minimum wage; overtime; expenses; paid sick days and leave; healthcare; and unemployment insurance.

Owing to its stance, the California Labour Federation accused Proposition 22 supporters of “attempting to buy their own law through the ballot measure process”. Having raised around $20 million to oppose the motion, labour groups were crushed by Uber, Lyft, DoorDash and Instacart, who purchased TV adverts and featured in-app ads in their services.

The ride hailing apps had also threatened to withdraw their services from California, had they been forced to start treating their drivers as fully-fledged employees.

In support of the move, the Yes on 22 campaign stated that: “California has spoken and millions of voters joined their voices with the hundreds of thousands of drivers who want independence plus benefits,”

“Prop 22 will protect drivers’ preference to be independent contractors with the flexibility to work when, where, and how long they want.”

Similarly, Terri Gerstein of the Harvard Labor and Worklife Program and Economic Policy Institute said in an email to CNN Business that the result will: “leave thousands of California workers in a precarious and perilous position, without basic rights like workers’ compensation, unemployment insurance, or the right to a safe workplace.”

Regardless, following the news, Lyft shares bounced over 11% to almost $29.2, while Uber shares soared between 14% and 15%, to almost $40.99.

US Big Tech stocks surge with election balance in Biden’s favour

On Wednesday, investors responded to election result uncertainty by heavily backing proven winners and market leaders, and this saw an enormous uptick in US big tech stocks.

After making upwards movements of around 3% in futures, the tech-laden Nasdaq Composite then saw additional growth, up around 4% – at 11,605 points.

This tech stock storm was led by gains posted by the big FANMAG members; with Apple (NASDAQ:AAPL) bouncing over 4%; Amazon (NASDAQ:AMZN) surging over 5%; Netflix (NASDAQ:NFLX) up 4%; Alphabet (NASDAQ:GOOGL) storming over 6%; Microsoft (NASDAQ:MSFT) up more than 4%; and Facebook (NASDAQ:FB) hiking more than 7%.

Also worth noting is that despite running out of steam – having rallied around 10% since Monday morning – Tesla mustered the energy to make modest gains. Meanwhile, having won a California bid to classify drivers as contractors, Uber added a notable 14% rally on Wednesday.

These big tech gains weren’t quite matched by other sectors, but their positive trajectory did incentivise US equities to climb more broadly. Indeed, the S&P 500 rose by over 2.7%, to 3,462 points.

Similarly, the Dow Jones rallied by around 2%, or more than 500 points. Significantly, this saw the index break the 28k benchmark for the first time in almost two weeks – reflecting some positive sentiment being injected back into equities, as investors come to terms with the election uncertainty. Perhaps, as seen with today’s big tech boom – the indecisive election hasn’t been quite as bad as many had feared.

For now, and coming towards the latter stages of trading in Europe, it appears that Biden has edged slightly ahead, with leads being eked out in Wisconsin and Michigan. As stated by Spreadex Financial Analyst, Connor Campbell, investors may also be buying back into the idea of a Biden win:

“It appears that once again investors are buying into a Joe Biden presidency, despite the race – which could still have days left in it yet – being on a knife-edge.”

“[…] Investors seem to be taking a kind of win-win attitude to the election. Yesterday’s growth was based on the hopes of a blue wave-led stimulus package. Now that the race is much tighter, and the Democrats have little chance of taking the Senate, the markets are celebrating the likelihood of preserved tax cuts and no healthcare reform.”

Morgan Sindall upgrades profit expectations, shares rise

Morgan Sindall shares (LON: MGNS) surged on Wednesday as the firm told investors it was expected to beat profit ranges for this year.

In the latest trading update, the group said that revenue and margin are both “well ahead” of last year.

Morgan Sindall is in the process of repaying the government for the furlough scheme. It has repaid £7.7m of the £9.5m that it borrowed during the scheme.

The group has declared an interim dividend of 21.0p per share, which is in line with 2019’s interim dividend.

John Morgan, Chief Executive, said: “Following the disruption earlier in the year, all of the Group’s activities are now fully operational again and delivering high levels of productivity. We welcome the Prime Minister’s clear statement that construction activity should continue through the new lockdown restrictions in England for November and we anticipate operating safely throughout with minimal impact.

“Our high-quality secured workload gives us good visibility for the rest of the year and as such, we now expect to deliver a full year performance slightly above the top end of our previous expectations.

“Our strong cash generation, position and balance sheet remain key differentiators. These, together with the improved outlook for the year, have enabled us to repay furlough monies and resume dividend payments as declared today.

“Despite the uncertainty that the pandemic brings, we have a sound platform for future growth with the Group geared towards future demand for affordable housing, urban regeneration and infrastructure and construction investment.”

Morgan Sindall’s cash position expects the average daily net cash for the full year to be in excess of £150m, again ahead of previous expectations.

Morgan Sindall shares (LON: MGNS) are +6.19% at 1.236,00 (1518GMT).

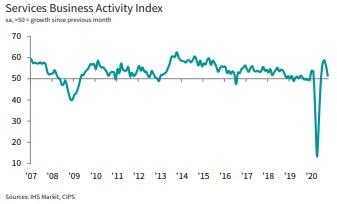

UK service sector PMI ‘slows sharply’ in October due to lockdown restrictions

IHS Markit‘s PMI data illustrated that business activity in the service sector had demonstrated a ‘much weaker rise’ in October, with the rate of expansion at its slowest rate for four months.

The research group also noted that the rate of new work fell for the first time since June, while hospitality, transport and leisure sectors ‘widely commented’ on the adverse impact from tightening restrictions on trade due to the COVID pandemic.

Adjusted for seasonal influences, the IHS UK service sector PMI in October stood at 51.4. Still growing – with 50 being the cut-off for growth and loss – October’s level was a notable drop from 56.1 in September, and below the 52.3 October flash PMI reading.

Between a recovery in business operations and consumer activity, all probable causes of the summer spike pointed to the move out of national lockdown after the second quarter, and the policies designed to reinvigorate demand.

It is also worth noting that overall service sector PMI data masks the worst-hit businesses, namely hoteliers, restaurants and broader catering industries. Of these latter categories, survey respondents ‘overwhelmingly attributed’ lower business activity to COVID restrictions being put in place in October, with the subsequent fall in demand for hospitality and leisure services set to intensify during November’s national lockdown.

Commenting on the Group’s data, Tim Moore, Economics Director at IHS Markit, said:

“October data indicates that the UK service sector was close to stalling even before the announcement of lockdown 2 in England, with tighter restrictions on hospitality, travel and leisure leading to a slump in demand for consumer-facing businesses. This was only partly offset by sustained expansion in areas related to digital services, business-to-business sales and housing market transactions.”

“The service sector as a whole recorded its slowest output

growth since June, while new orders declined for the first

time in four months. A lack of forward bookings in parts of

the economy most affected by lockdown measures led to

widespread reports of redundancies and another sharp fall

in total employment numbers during October.”

“November’s lockdown in England and a worsening COVID-19 situation across the rest of Europe means that the UK economy seems on course for a double-dip recession this winter and a far more challenging path to recovery in 2021.”

Between a recovery in business operations and consumer activity, all probable causes of the summer spike pointed to the move out of national lockdown after the second quarter, and the policies designed to reinvigorate demand.

It is also worth noting that overall service sector PMI data masks the worst-hit businesses, namely hoteliers, restaurants and broader catering industries. Of these latter categories, survey respondents ‘overwhelmingly attributed’ lower business activity to COVID restrictions being put in place in October, with the subsequent fall in demand for hospitality and leisure services set to intensify during November’s national lockdown.

Commenting on the Group’s data, Tim Moore, Economics Director at IHS Markit, said:

“October data indicates that the UK service sector was close to stalling even before the announcement of lockdown 2 in England, with tighter restrictions on hospitality, travel and leisure leading to a slump in demand for consumer-facing businesses. This was only partly offset by sustained expansion in areas related to digital services, business-to-business sales and housing market transactions.”

“The service sector as a whole recorded its slowest output

growth since June, while new orders declined for the first

time in four months. A lack of forward bookings in parts of

the economy most affected by lockdown measures led to

widespread reports of redundancies and another sharp fall

in total employment numbers during October.”

“November’s lockdown in England and a worsening COVID-19 situation across the rest of Europe means that the UK economy seems on course for a double-dip recession this winter and a far more challenging path to recovery in 2021.”

Between a recovery in business operations and consumer activity, all probable causes of the summer spike pointed to the move out of national lockdown after the second quarter, and the policies designed to reinvigorate demand.

It is also worth noting that overall service sector PMI data masks the worst-hit businesses, namely hoteliers, restaurants and broader catering industries. Of these latter categories, survey respondents ‘overwhelmingly attributed’ lower business activity to COVID restrictions being put in place in October, with the subsequent fall in demand for hospitality and leisure services set to intensify during November’s national lockdown.

Commenting on the Group’s data, Tim Moore, Economics Director at IHS Markit, said:

“October data indicates that the UK service sector was close to stalling even before the announcement of lockdown 2 in England, with tighter restrictions on hospitality, travel and leisure leading to a slump in demand for consumer-facing businesses. This was only partly offset by sustained expansion in areas related to digital services, business-to-business sales and housing market transactions.”

“The service sector as a whole recorded its slowest output

growth since June, while new orders declined for the first

time in four months. A lack of forward bookings in parts of

the economy most affected by lockdown measures led to

widespread reports of redundancies and another sharp fall

in total employment numbers during October.”

“November’s lockdown in England and a worsening COVID-19 situation across the rest of Europe means that the UK economy seems on course for a double-dip recession this winter and a far more challenging path to recovery in 2021.”

Between a recovery in business operations and consumer activity, all probable causes of the summer spike pointed to the move out of national lockdown after the second quarter, and the policies designed to reinvigorate demand.

It is also worth noting that overall service sector PMI data masks the worst-hit businesses, namely hoteliers, restaurants and broader catering industries. Of these latter categories, survey respondents ‘overwhelmingly attributed’ lower business activity to COVID restrictions being put in place in October, with the subsequent fall in demand for hospitality and leisure services set to intensify during November’s national lockdown.

Commenting on the Group’s data, Tim Moore, Economics Director at IHS Markit, said:

“October data indicates that the UK service sector was close to stalling even before the announcement of lockdown 2 in England, with tighter restrictions on hospitality, travel and leisure leading to a slump in demand for consumer-facing businesses. This was only partly offset by sustained expansion in areas related to digital services, business-to-business sales and housing market transactions.”

“The service sector as a whole recorded its slowest output

growth since June, while new orders declined for the first

time in four months. A lack of forward bookings in parts of

the economy most affected by lockdown measures led to

widespread reports of redundancies and another sharp fall

in total employment numbers during October.”

“November’s lockdown in England and a worsening COVID-19 situation across the rest of Europe means that the UK economy seems on course for a double-dip recession this winter and a far more challenging path to recovery in 2021.” John Lewis to axe 1,500 head office jobs

John Lewis has announced plans to axe a further 1,500 head office jobs in an attempt to return to profit.

The retailer said on Wednesday that it plans to cut the additional jobs as part of a target to annually save £300m.

“Our partnership plan sets a course to create a thriving and sustainable business for the future. To achieve this we must be agile and able to adapt quickly to the changing needs of our customers,” said chairman, Sharon White.

“Losing partners is incredibly hard as an employee-owned business. Wherever possible, we will seek to find new roles in the partnership and we’ll provide the best support and retraining opportunities for partners who leave us,” White added.

In other news that the retailer announced today that executive director of finance, Patrick Lewis, will be replaced by Bérangère Michel. Lewis is the only family member still working at the company and will be stepping down after 26-years at the retailer.

White said about Lewis stepping down: “His determined drive to build the financial strength of the business has granted us the opportunity to emerge stronger from the Covid crisis.”

So far this year, John Lewis has permanently closed eight of its 50 department stores and has already announced plans to cut 1,300 jobs.

“Before the virus struck, 40% of John Lewis sales were online. This could now be closer to 60% to 70% of total sales this year and next,” the company said in a statement over summer.

The retailer hopes to create a simpler and more “agile and flexible head office.”

Smurfit Kappa shares soar with ‘particularly pleasing’ Q3 earnings of €390m

FTSE-listed packaging company Smurfit Kappa (LON:SKG) watched its shares bounce to around 5% on Wednesday morning, on news of strong Q3 earnings that put it on track to hit its full-year target.

Having posted EBITDA of €1.13 billion for the year-to-date, the company boasted an EBITDA margin of 17.8% and ‘particularly pleasing’ third quarter EBITDA of €390 million. The company said that from both an operational and financial perspective, this progress demonstrates “the strength and resilience of the Group”.

Smurfit Kappa added that its results reflected the benefits of its capital allocation decisions, cost management, geographic reach and recovery across its US and Americas businesses. It continued, saying the strong data underlines its 65,000 customers’ support for its innovation, supply chain management and sustainability credentials.

The company said that its business is now ‘strongly weighted’ towards FMCG customers, where it feels it is well-positioned to capitalise on e-commerce and innovative packaging demand. It added that it had implemented new ways of working during the pandemic, and would carry out a programme to look at ways to further increase its operational efficiency and effectiveness.

Responding to the company’s progress and full-year targets, the company’s CEO, Tony Smurfit, commented:

“I am pleased to report that the quality of our business and the strength of our people has produced an excellent performance in both the third quarter and the year-to-date. While some uncertainty still exists around the evolution of the effects of COVID-19 in the weeks ahead, absent a dramatic change to working practices, the Group expects to deliver EBITDA in the range of €1,460 million to €1,480 million for the full year 2020.”

“We are increasingly excited by our future prospects and the structural growth drivers of our business including e‑commerce and sustainable packaging as well as our innovative ability to capitalise on these opportunities. Reflecting the Board’s confidence in SKG’s performance and prospects, it is recommending a second interim dividend of 27.9 cent per share. This second interim dividend, following the payment of an interim dividend in September, ensures the Group is aligned with the dividend payment cycles of previous years. It is proposed to pay this dividend on 11 December 2020 to all ordinary shareholders on the share register at the close of business on 20 November 2020.”

Following the update, Smurfit Kappa shares bounced around 5% at lunchtime on Wednesday, up to 3,258.00p a share 04/11/20. This price is ahead of any other price posted during the year-to-date, and ahead of analysts’ target price for the stock, of 3,150p. The company has a ‘Buy’ rating from analysts, a p/e ratio of 17.13 – behind the consumer cyclical average of 31.19 – and a 56.53% “outperform” rating from the Marketbeat community.Kerry Group posts strong recovery in Q3

Kerry Group shares (LON: KYGA) climbed over 3% on Wednesday morning after posting a trading update for the nine months ended 30 September 2020.

The company saw a strong recovery in Q3 for the foodservice channel, which was boosted since April.

Group reported revenue decreased by 4.5% and at the end of September, net debt stood at €1.8bn.

Kerry Group has resumed providing full-year earnings guidance and expects a strong recovery for the final quarter of this year.

Developing market volumes has declined by 2.9% for the year to date, with continued recovery in Q3, which was led by good growth in China.

The Americas region also saw business volumes continuing to recover, with the third quarter declining by 2.8%.

Edmond Scanlon, the chief executive, said: “This year has seen unprecedented variability and complexity across our industry. The agility and ingenuity of Kerry’s teams in adapting to these changing conditions has contributed to Kerry’s strong recovery in the third quarter, which was in line with previous guidance.

“In the foodservice channel, we have seen a strong recovery since April, as restaurants reopened and adapted their operations and menus to cater for increased consumer demand for takeaway, online and delivery. Performance in the retail channel remained strong, primarily through growth in authentic cooking, plant-based offerings and health and wellness products.

“We continued to make good progress on a number of strategic fronts. During the third quarter we reached agreement to acquire Bio-K Plus International probiotics in Canada and Jining Nature Group, a leading savoury taste business in China. We also recently launched our 2030 sustainability strategy – Beyond the Horizon. This details Kerry’s sustainability targets and will be central to Kerry’s growth strategy, as we continue to innovate with our customers and expand our reach of sustainable nutrition solutions globally.”

Kerry Group shares (LON: KYGA) are trading +3.44% at 108,10. The high this year to date was 125,50.

Is Hovis on the brink of a takeover deal?

Sky News has learned that following a bidding war, Endless is in advanced talks to buy the bread-maker Hovis.

Wednesday morning saw the other bidder, Newlat Food, issue a statement saying they had pulled out from talks and would only continue if they were the only interested party.

A deal could be confirmed as early as this week.

Owned by Premier Foods (LON: PFD) and US investment firm, Gores Group, Hovis is a 134-year old firm that employs 2,800 people across the UK. Sales at the brand surged over lockdown as consumers stockpiled.

Although not confirmed, it is estimated that shareholders are expecting a £100m deal for the brand.

Newlat joined the bidding process for Hovis a month ago and said on their website: “Newlat Food is awaiting feedback from Hovis shareholders and, therefore, any other details regarding the transaction will be communicated with the evolution of the negotiations.”

In a statement released on Wednesday afternoon Hovis owner, Premier Foods, said that they can “confirm that a sale process for a potential transaction in respect of Hovis is ongoing. However there can be no certainty that any transaction will conclude. The Group will provide an update in due course as appropriate.”

M&S shares rise despite first-ever loss

Marks & Spencer (LON: MKS) posted its first loss in the 94-years as a listed company on Tuesday as sales were dented by the pandemic.

The high street retailer posted a £87m pre-tax loss for the six months to September 26, which is down from the £158.8m profit it made in the same period a year ago.

Revenue at the group was down 15.8% from £4.9bn to £4.1bn.

During the lockdown, the food hall remained open, however, the clothing division was closed until mid-June, and clothing sales slumped 40% in the period.

Chief executive Steve Rowe said: “In a year when it has become impossible to forecast with any degree of accuracy, our performance has been much more robust than at first seemed possible.”

“But out of adversity comes opportunity and, through our Never the Same Again programme, we have brought forward three years change in one to become a leaner, faster and more digital business. From launching M&S Food online with Ocado to establishing an integrated online business division ‘MS2’ to step-change growth, we are taking the right actions to come through the crisis stronger and set up to win in the new world.”

Despite the loss, shares in the group rose 4.3% on this morning’s opening.

Richard Hunter, head of markets at Interactive Investor, said: “There is little doubt that a reorganisation of the company and, to some extent the brand, is long overdue. Whether the speed of this transformation is too little, too late remains to be seen, but M&S is making every effort to stem what has been a slow decline over recent years.”

Earlier this year, M&S revealed plans to axe 7,000 jobs by the end of the year.

M&S shares (LON: MKS) are currently trading +6.05% at 97,56 (0932GMT).