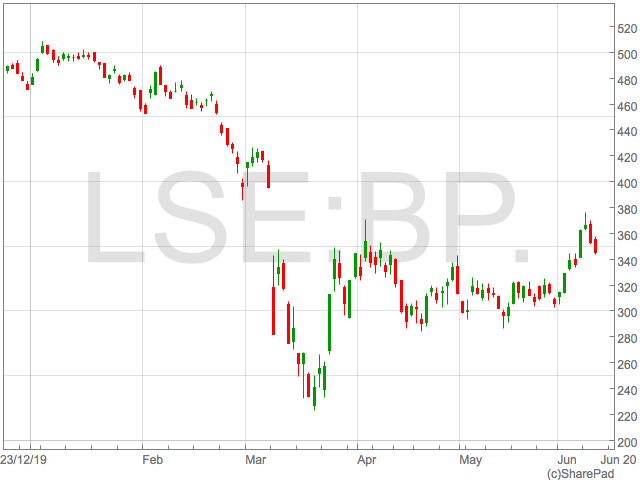

The price of oil will be inextricably effected over the long term and if BP are not able to convert their business model, shareholder returns will deteriorate.

The impact on BP of a lower oil price has already been highlighted by the company in an email from the BP CEO to employees when he said:

“The oil price has plunged well below the level we need to turn a profit. We are spending much, much more than we make – I am talking millions of dollars, every day.”

The email was sent as BP announced 10,000 job cut and said the reduction in head count was needed to make BP a “leaner, faster-moving and lower carbon company.”

The price of oil will be inextricably effected over the long term and if BP are not able to convert their business model, shareholder returns will deteriorate.

The impact on BP of a lower oil price has already been highlighted by the company in an email from the BP CEO to employees when he said:

“The oil price has plunged well below the level we need to turn a profit. We are spending much, much more than we make – I am talking millions of dollars, every day.”

The email was sent as BP announced 10,000 job cut and said the reduction in head count was needed to make BP a “leaner, faster-moving and lower carbon company.”

BP share price: the transition to clean energy will drive long-term returns

The future of the BP share price (LON:BP) will be dictated by how efficiently the company transitions towards cleaner renewable forms of fuel.

BP has set a target to become net-zero by 2050 and the achievement of this goal is not only important for the environment, but the returns of the BP share price.

It has already be demonstrated by countries such as Costa Rica that entire nations can power themselves without the need for fossil fuels.

Costa Rica powered has itself for an entire year solely by renewable energy. As more countries increase the percentage of energy produced from renewable sources, fossil fuel demand will fall.

Whilst renewable power will hit thermal coal, the wider adoption of electric vehicles significantly threatens demand for oil through gasoline and fuel, which is the largest end use of oil.

The price of oil will be inextricably effected over the long term and if BP are not able to convert their business model, shareholder returns will deteriorate.

The impact on BP of a lower oil price has already been highlighted by the company in an email from the BP CEO to employees when he said:

“The oil price has plunged well below the level we need to turn a profit. We are spending much, much more than we make – I am talking millions of dollars, every day.”

The email was sent as BP announced 10,000 job cut and said the reduction in head count was needed to make BP a “leaner, faster-moving and lower carbon company.”

The price of oil will be inextricably effected over the long term and if BP are not able to convert their business model, shareholder returns will deteriorate.

The impact on BP of a lower oil price has already been highlighted by the company in an email from the BP CEO to employees when he said:

“The oil price has plunged well below the level we need to turn a profit. We are spending much, much more than we make – I am talking millions of dollars, every day.”

The email was sent as BP announced 10,000 job cut and said the reduction in head count was needed to make BP a “leaner, faster-moving and lower carbon company.”

The price of oil will be inextricably effected over the long term and if BP are not able to convert their business model, shareholder returns will deteriorate.

The impact on BP of a lower oil price has already been highlighted by the company in an email from the BP CEO to employees when he said:

“The oil price has plunged well below the level we need to turn a profit. We are spending much, much more than we make – I am talking millions of dollars, every day.”

The email was sent as BP announced 10,000 job cut and said the reduction in head count was needed to make BP a “leaner, faster-moving and lower carbon company.”

Shaftesbury posts £287m loss

Shaftesbury posted a £287m first-half loss on Wednesday after being impacted by the Coronavirus pandemic.

The West-End landlord, which owns pubs, shops, workspaces, and restaurants in central London said a “collapse” of footfall from February and the closure of shops in March has affected tenant’s ability to pay rent.

The £287m loss is compared to the £38.7m profit made in the same period a year earlier.

“Although our business performed well during the first four months of the period, the growing impact of the measures to address the pandemic are having a material impact on normal patterns of life and commerce, both for our occupiers and on the near-term prospects for our business and financial performance,” said Brian Bickell, the group’s chief executive.

“The economies of London and the West End have a long history of structural resilience, having weathered many episodes of near-term challenges and uncertainties. Their unique features come from a culture of constant evolution across a broad-based economy, attracting talent, creativity, innovation and investment from across the world and reinforcing their enduring appeal to businesses, visitors and as great places to live.”

“In the post-pandemic recovery, these fundamental advantages will underpin their return to prosperity and growth,” he added.

The group has said that it aims to collect 50% rent from tenants that is owed between April-October.

Shares in Shaftesbury (LON: SHB) are trading down 4.94% at 616.00 (1031GMT).

Ebiquity offers exposure to the recovery in marketing services

The transition into an independent global media marketing consultancy took its final shape in the finals to December 2019, which were reported last month. Now, under the new CEO, Ebiquity (LON:EBQ) sold its commoditised Advertising Intelligence business (Adintel) to Nielsen for around £20m in January 2019.

The outlook contained Covid adjusted caution and the proposed dividend of 0.85p was postponed. Results were broadly in line, with revenue down 1% to £68.7m and the underlying PBT was up slightly to £5.3m with EPS of 3.6p. This would give a P/E of 8x and a 2.8% yield, however the accounts are mudded by eight kitchen sink items the largest is the £6.8m Goodwill impairment from closing a US subsidiary.

The ongoing higher margin consultancy practice covers; Media Management, Performance and Contract Compliance. The new CEO reported that business operations and service delivery are being maintained at a normal level during Covid. Revenue, however, was impacted as some clients and sectors hibernated and forward guidance was withdrawn.

The media market continues to undergo significant changes as it shifts from traditional media into the increasingly complexity of the digital media value chain.

This provides the Consultancy business with opportunities to address advertisers’ requirements and to map into the key stages of client’s media cycles using their global media expertise. It’s clients are 70 of the world’s 100 leading advertisers including Sony, L Oreal and Subway. Few can doubt these companies demand as marketing strategies are reappraised.

Initially the CEO’s focus is on improving the profitability by increasing efficiency and expanding the range and value generated by the consultancy. The acquisition of complementary Digital Decisions helps the measurement and advisory services and further deals can be anticipated. Profits to the year-end December 2020 were forecast a £6.5m for a P/E of 6x and a 3% yield and cost reductions have been made. The shares are tightly held with over 60% with institutions; Artemis holding 19%, Canaccord on 13% and JO Hambro with 12%. After the finals Directors brought share at up 30p.

Financials

There is strong cash conversion and net debt is down to £5m in an agreed Banking facility.

Trading Strategy

EBQ are comparatively cheap and set to be re-rated, which could be helped by the AGM statement at the end of this month. Buy

Ebiquity (LSE: EBQ)

29.5p (29-30p)

Mkt Cap: £24m

Next Announcement AGM Friday June 26th – then Interims in September

This tip is from the OGM Newsletter by Jon Levinson and Andrew Hore

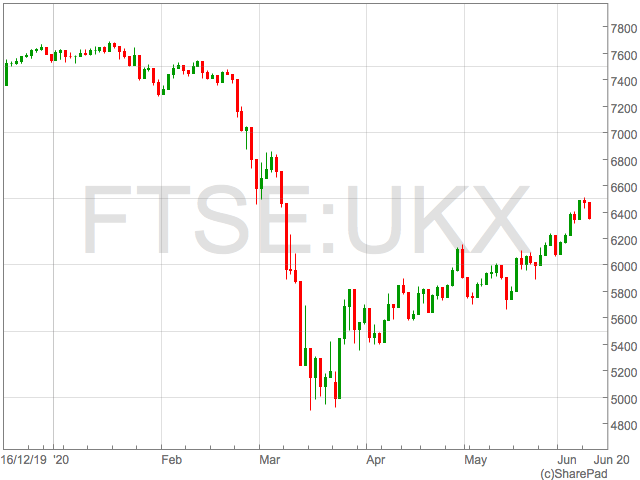

FTSE 100 retreats ahead of Fed meeting

The FTSE 100 paused on Tuesday following a strong session on Monday that saw the index touch the highest levels for three months.

Steam ran out the rally caused by a strong jobs report as investors awaited further insight to the thinking of the Federal Reserve who were set to begin their FOMC meeting on Tuesday.

“The rally looks a little tired, as might be expected after the first week of June saw such a strong move higher. The positive impact from the ECB meeting and Friday’s US jobs report has waned, with no fresh bullish news to take their place,” said Chris Beauchamp, Chief Market Analyst at IG.

Analysts also pointed to decoupling of equity markets and the underlying economy in the middle of the coronavirus pandemic which is only just starting to show signs of recovery.

“Those long- and short-term records…may well have inspired Tuesday’s losses. Investors might be questioning the wisdom of such highs in a world still very firmly in the middle of a pandemic,” said Connor Campbell, Analyst at Spreadex.

There was also another instalment of sobering German data that highlighted the impact coronavirus had on the European economy.

“It appears the collapse in German trade – exports plunged 24% in April, while the country’s trade surplus saw a staggering decline, from €12.8 billion to €3.2 billion month-on-month – has sparked Europe’s rather significant wobble,” said Connor Campbell.

Economic V-Shaped Recovery?

Global equity markets have certainly produced a V-Shaped recovery with the S&P 500 erasing all of 2020’s losses when it closed on Monday, despite economic data only just starting to show signs of improvement. “Those long- and short-term records…may well have inspired Tuesday’s losses. Investors might be questioning the wisdom of such highs in a world still very firmly in the middle of a pandemic,” said Connor Campbell, Analyst at Spreadex.

There was also another instalment of sobering German data that highlighted the impact coronavirus had on the European economy.

“It appears the collapse in German trade – exports plunged 24% in April, while the country’s trade surplus saw a staggering decline, from €12.8 billion to €3.2 billion month-on-month – has sparked Europe’s rather significant wobble,” said Connor Campbell.

“Those long- and short-term records…may well have inspired Tuesday’s losses. Investors might be questioning the wisdom of such highs in a world still very firmly in the middle of a pandemic,” said Connor Campbell, Analyst at Spreadex.

There was also another instalment of sobering German data that highlighted the impact coronavirus had on the European economy.

“It appears the collapse in German trade – exports plunged 24% in April, while the country’s trade surplus saw a staggering decline, from €12.8 billion to €3.2 billion month-on-month – has sparked Europe’s rather significant wobble,” said Connor Campbell.

FTSE 100 movers

Most sectors were down in London in a broad selloff that targeted some of the better performing stocks in lasts week’s surging rally. Travel shares and the financials were among the biggest fallers on Tuesday. The FTSE 100’s housebuilders fell Bellway after revealed sales figures for the coronavirus lockdown period declined, but didn’t completely collapse. “The 3% drop in Bellway’s shares might been a bit of an over-reaction to a fairly anodyne statement, but the similar or bigger losses for Taylor Wimpey and Barratt points to a sector-wide malaise this morning,” said Chris Beauchamp.AstraZeneca share price: three reasons I’d buy after the recent pullback

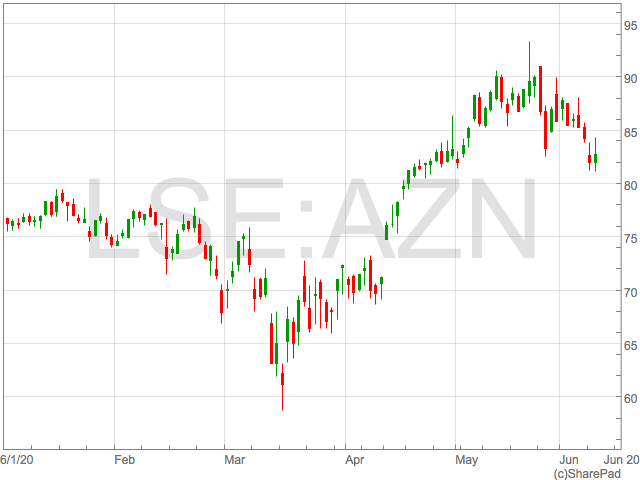

Until recently, AstraZeneca shares (LON:AZN) had been one of the quiet outperformers of the FTSE 100 during the coronavirus volatility.

As cyclical shares were ravaged by concerns over worst recession in recent history, AstraZeneca was among the shares possessing enough defensive qualities to outperform the benchmark as investors sought out quality.

This reversed in the risk-on rally through May and early June when cyclical equities took charge and those companies that were bought into as a safe havens gave up gains as the market rotated into companies perceived to benefit from economic reopenings.

AstraZeneca shares were on the list of ‘lockdown’ shares’ that suffered during the rotation into cyclical shares.

We feel provides the opportunity to buy AstraZeneca given the potential for the pharmaceutical company to lose its ‘defensive’ tag and become a real growth stock.

The dividend seems secure enough for AstraZeneca shares to be classed as an income play, even if the current drug pipeline doesn’t provide a huge boost to revenue in the medium term.

In the full year results the board reaffirmed their progressive dividend policy, and with revenue growing 17% in Q1, the financial position is sufficiently robust to support this.

With a AstraZeneca share price of 8,293p, the current yield is 2.8% and more than respectable given the recent dividend cuts to FTSE 100 companies.

Gilead Merger

It has been reported AstraZeneca approached Gilead about a possible merger which would have been the largest Pharma deal in history. However, such a deal looks unlikely in the short-term as both companies focus on their own pipeline of drugs and shareholder value creation. “We believe such a transaction, which would likely effectively be an equity merger of equals, is unlikely given limited strategic rationale for AstraZeneca at this time and our US biotech team’s view that Gilead is still in the midst of a turnaround,” said Jefferies Analyst Peter Welford. The initial market reaction to a potential merger was for shares to fall reflecting the market’s scepticism over the deal. Should the deal not materialise AstraZeneca’s shareholders will receive a greater proportion of the upside in Astra’s current drug pipeline.Drug Pipeline

AstraZeneca’s pipeline of drugs holds the potential for a number of blockbusters that would be transformational to the company. The foremost trail is that of Lung Cancer drug Tagrisso which has had a series of statistically significant results in the elimination of the disease in early stage cases. José Baselga, Executive Vice President, Oncology R&D at AstraZeneca even said the drug provided hope for a cure. “The momentous results of the Phase III ADAURA trial for Tagrissodemonstrate for the first time in a global trial that an EGFR inhibitor can change the course of early-stage EGFR-mutated lung cancer and provide hope for a cure,” said José Baselga. AstraZeneca are also developing testicular cancer drug Lynparza which has had positive findings from trials. Heart failure drug Farxiga has just received approval from the FDA, providing the potential to treat million of people in the United States. There has also been progress in a number of the other 167 drugs in the AstraZeneca pipeline.Dividend

The dividend seems secure enough for AstraZeneca shares to be classed as an income play, even if the current drug pipeline doesn’t provide a huge boost to revenue in the medium term.

In the full year results the board reaffirmed their progressive dividend policy, and with revenue growing 17% in Q1, the financial position is sufficiently robust to support this.

With a AstraZeneca share price of 8,293p, the current yield is 2.8% and more than respectable given the recent dividend cuts to FTSE 100 companies.

Vaccine Production

The UK-based drug company is preparing for the production and distribution of 2 billion doses of a COVID-19 vaccine that would be monumental for the fight against COVID-19. However, vaccine production is not taken into consideration as a reason to buy shares due to no profit approach being employed by Astra. AstraZeneca is one of hundreds of companies in a race to find a vaccine and although the vaccine is not yet proved having received significant funding from governments. AstraZeneca’s vaccine is using the common cold virus combined with COVID-19 proteins to induce a immune response from the body.UK household debt to reach £6bn amid pandemic

The StepChange debt advice charity has warned that households in the UK are expected to build up £6bn in debt amid the Coronavirus pandemic.

Due to the growth of households falling behind on credit card payments and utility bills, a total of 4.6m households could risk dangerous levels of debt.

In response, the Treasury has said they plan to fund debt advice services by an additional £38m.

“We know that some people are struggling with their finances during this difficult time, which is why we want to make sure people can access the help and support they need to manage their debts and get their finances back on track,” said John Glen, economic secretary to the Treasury.

Research by YouGov has shown that each affected adult has accumulated an additional £1,076 of arrears and £997 of debt since the start of lockdown.

The chief executive of StepChange, Phil Andrew, said: “We were already dealing with a debt crisis, but COVID has so far added another four million people and counting to the number who are going to need help finding their way back to financial health. With £6bn of additional household debt directly attributable to the effects of the pandemic, this is a problem that isn’t going to solve itself.”

“As a charity, we have our own part to play. Like other debt charities, we are gearing up for a significant increase in demand for our usual services. We are also working on a specific solution to help people whose finances have been hit by the pandemic and who need a short term helping hand to get back on track without jeopardising their credit status.”

“The false calm in which we find ourselves while furlough and forbearance take the strain will not last indefinitely. We will be ready to help as more people find their debt problems crystallising over the coming months.”

FTSE 100 hits 3-month high

The FTSE 100 continued it’s march higher on Monday as London’s large cap index briefly traded above 6,500, the highest levels for three months.

The rise in equities follows a bumper US jobs report that pointed to 2.5 million jobs being added to the US economy in May, as opposed to a loss of 8 million jobs.

The shock jobs data suggests the post-coronavirus lockdown is well ahead of all economist expectations, and has fuelled appetite for risk assets such as equities.

However, not all economic data has been as positive with Eurozone GDP falling 3.2% in the first quarter and German export data showed further economic contraction with exports falling 15% in April.

Nonetheless, analysts see these softer economic readings as being largely priced into equity markets and instead are focusing on the reopening of economies and associated recovery.

“The market continues to view all of these economic reports as rear-view mirror stuff, as optimism over economic re-openings continues to drive sentiment,” said Michael Hewson, chief market analyst at CMC Markets.

Nonetheless, analysts see these softer economic readings as being largely priced into equity markets and instead are focusing on the reopening of economies and associated recovery.

“The market continues to view all of these economic reports as rear-view mirror stuff, as optimism over economic re-openings continues to drive sentiment,” said Michael Hewson, chief market analyst at CMC Markets.

Nonetheless, analysts see these softer economic readings as being largely priced into equity markets and instead are focusing on the reopening of economies and associated recovery.

“The market continues to view all of these economic reports as rear-view mirror stuff, as optimism over economic re-openings continues to drive sentiment,” said Michael Hewson, chief market analyst at CMC Markets.

Global jobs

The US jobs report has caused short term optimism but multinational companies are still navigating lower demand. Government schemes such a the UK’s furlough scheme have provided support to employers thus far but will soon evaporate. Signalling the longer term impact of the coronavirus lockdown, markets assessed further job cuts to major global brands listed on the UK’s exchanges. FTSE 100 oil major BP announced they were to cut 10,000 of their global workforce whilst luxury fashion brand Mulberry said they were going to slash their staff by 25%. The BBC reported BP CEO said in an email to staff: “The oil price has plunged well below the level we need to turn a profit.” “We are spending much, much more than we make – I am talking millions of dollars, every day.” If this proves to be a theme throughout other industries, the US jobs report and subsequent optimism in stock markets could prove premature.Travel and leisure shares

The FTSE 100’s travel shares have flown over the past week and were again among the risers on Monday despite a 14-day quarantine coming into effect. “The surge in travel- and airline-related names comes on the day when the UK implements a quarantine for overseas travel, perhaps the very definition of shutting stable doors after the horse has bolted,” said Chris Beauchamp, Chief Market Analyst at IG. “With lockdowns easing across Europe and no sign of a second infection wave, this move has been staunchly opposed by airlines, and it looks like the market expects the restriction to remain in place for only a limited time,” Beauchamp said.Mulberry to cut 25pc of workforce, shares fall

After a fall in demand amid the Coronavirus pandemic, Mulberry (LON: MUL) has announced plans to cut its global workforce by 25%.

The luxury handbag maker employs 1,500 people globally. The redundancies will affect people across the head office, stores and manufacturing.

Thierry Andretta, the group’s chief executive, said in a statement: “Launching a consultation process has been an incredibly difficult decision for us to make but it is necessary for us to respond to these challenging market conditions, protect the maximum number of jobs possible and safeguard the future of the business.”

“In spite of the good performance of our sector-leading digital and omni-channel platform, and our global network of digital concessions, the shutting of all our physical stores has had, and will continue to have, a marked effect on our business.”

“We remain confident in the strength of the Mulberry brand and our strategy over the long-term,” he added.

Stores in the UK are set to re-open from 15 June, however, revenue will continue to be affected by the social distancing measures.

“Even once stores reopen, social distancing measures, reduced tourist and footfall levels will continue to impact our revenue,” said Andretta.

The group has already opened stores in South Korea, China, Europe, and Canada.

Shares in Mulberry have fallen 30% over the course of the year. This morning, shares in the group are trading down 5.61% at 185.00 (1210GMT).

AstraZeneca approaches Gilead over possible merger

It has been reported AstraZeneca (LON:AZN) approached US-based Gilead about a possible merger that would create one of the globe’s largest pharmaceutical companies.

If the merger were to go ahead, the new company would be the world’s foremost organisation in the fight against COVID-19 given the development of vaccines and treatments at the respective companies.

Despite an initial buzz around the merger, it was later reported by the Times that AstraZeneca dropped their interest in the deal.

It is common for companies to decline media comment during merger talks and sources provide information under on the understanding anonymity, making it hard to verify progress of any talks.

A spokesman for AstraZeneca said they do not comment on “rumors or speculation’ whilst Gilead declined to comment.

COVID-19 treatment

AstraZeneca has recently announced they are working on the provision of 2 billion vaccine doses should it receive approval from ongoing trials. Whilst AstraZeneca is working on a potential vaccine, Gilead is the only treatment that is approved in the US to treat COVID-19. Gilead’s anti-viral drug, Remdesivir, received emergency approval from the FDA after a number of trials found positive effects in patients with severe COVID-19. Despite the positive results, other studies found little or no positive effects and there is some scepticism around the long term impact of the drug. Notwithstanding the development of COVID-19 treatments and vaccines, the new organisation would have a significant pipeline of potential drugs for cancer and other life-threatening diseases. AstraZeneca has recently released updates on cancer drug Tagrisso which has the potential to be a blockbuster for the UK-based company. These pipelines may also be a stumbling block for a merger because Gilead’s pipeline could provide investors with significant value without the interference of AstraZeneca. In addition, the sheer size of the two companies would make it a difficultly slow process to push through and have approved during lockdown and social distancing. Shares in AstraZeneca (LON:AZN) were 2.5% softer at 972p at lunchtime in London trade.Ryanair to continue flights despite new quarantine rules

The Ryanair boss has insisted the airline will continue all flights throughout summer, despite new quarantine rules for travelers.

From Monday all passengers arriving in the UK must self-isolate for 14 days. However, for airline boss, Michael O’Leary, these rules are “rubbish”.

Speaking to the BBC on Monday, he said “British people are ignoring this quarantine. They know it’s rubbish”.

His comments come after Ryanair, easyJet (LON: EZJ) and British Airways owner, IAG, (LON: IAG) started legal action against the government to try and overturn the new rules that require travelers to self-isolate for two weeks.

Following a letter from the three airlines, a Ryanair spokesperson said: “These measures are disproportionate and unfair on British citizens as well as international visitors arriving in the UK. We urge the government to remove this ineffective visitor quarantine which will have a devastating effect on UK’s tourism industry and will destroy even more thousands of jobs in this unprecedented crisis.”

The new rules are designed to prevent a second wave of the Coronavirus and will be reviewed every three weeks.

The chief executive of Heathrow Airport has also criticized the government measures, saying that up to 25,000 jobs could be lost if these restrictions weren’t relaxed soon.

“We cannot go on like this as a country,” said John Holland-Kaye.

“We need to start planning to reopen our borders. If we don’t get aviation moving again quickly, in a very safe way, then we are going to lose hundreds of thousands if not millions of jobs in the UK just at the time when we need to be rebuilding our economy, he added.

“76,000 people are employed at Heathrow. That represents one in four households in the local community, so if we start cutting jobs en masse it will have a devastating impact on local communities.”

Shares in Ryanair (LON: RYA) are trading at 12.98 (1126GMT).