N Brown Group shares surge on 108.7% pre-tax profit spike

N Brown Group shares surged 28.6% to 33.9p on the back of the fashion group’s pre-tax profit spike of 108.7% to £19.2 million in its 2022 results, against £9.2 million the previous year.

N Brown Group highlighted an adjusted EBITDA growth of 11.9% to £95 million compared to 84.9 million, alongside an adjusted EBITDA margin increase of 1.7% to 13.3% against 11.6%.

The company reported a revenue slip of 1.8% to £715 million from £728.8 million, as a result of its 0.6% decline in product revenue and a 4% reduction in Financial Services revenue due to a smaller debtor book at the start of the financial year.

The firm also noted an operating costs decline as a percentage of revenue to 36% against 39.8% at pre-pandemic levels in 2020 in light of increased efficiencies and retained cost flexibility.

N Brown Group confirmed a strong balance sheet with unsecured net cash of £43.1 million, alongside an additional £60.1 million in accessible cash voluntarily undrawn on the securitisation funding facility at the year end.

The group added that it expected a 7% revenue growth with a 13% EBITDA margin in the medium-term, and remained confident in its outlook despite inflationary pressures and shifts in consumer behaviour.

“In what has been another volatile period in the consumer environment, I would like to thank all of my colleagues for their continued commitment to serving customers, and their role in delivering a strong performance in the year,” said N Brown Group CEO Steve Johnson.

“The work we have done means we are significantly better placed than we were before the pandemic and, although cautious in the short-term due to inflationary impacts and consumer behaviour, we remain confident that over the medium-term our strategy will support the delivery of 7% product revenue growth with a 13% EBITDA margin.”

The fashion company announced that it would consider the introduction of a dividend payment in FY 2023.

The firm also commented that it would be moving its focus to boost growth in its most promising brands, such as its recent sustainable clothing brand with JD Williams, in a bid to capitalise on its popular offerings as inflationary-related problems kicked off.

“I am pleased with our continued progress in transforming N Brown into a more focused digital business, with a distinct and improving offer across our strategic brands,” said Johnson.

“Our strategic brands returned to growth in the year with growing customer numbers. As we move forward, we are evolving our priorities to concentrate our growth focus on Simply Be, JD Williams and Jacamo, where we see the strongest market potential.”

“We’re executing on our investment plans to unlock these opportunities including through new websites which will be rolled out progressively over the coming months.”

Arrow Exploration RCE-2 well strikes 90 net ft oil

Arrow Exploration shares increased 20.8% to 16.3p in late afternoon trading on Wednesday, after the company reported six hydrocarbons bearing intervals at a total of 90 net feet of oil pay in its Rio Cravo Este-2 (RCE-2) well.

The oil and gas firm commented that its Colombia-based project targeted a large, three-way fault bounded structure with several high-quality reserve objectives on the Tapir Block in the Llanos Basin, which was drilled to a total measured depth of 9,600 feet.

The RCE-2 well was spud on 2 April 2022, and all operational costs reportedly came in line with the project’s budget.

“We’re encouraged by the material results of RCE-2, the second well on the Tapir block. RCE-2 identified new zones for further exploitation with flowing results returning better than expected,” said Arrow Exploration CEO Marshall Abbott.

“We’re currently completing the C7 zone, targeting to be on stream early next week. This effectively doubles Arrow’s production. The Company’s procedures will be to bring RCE-2 on slowly and increase production to best manage the oil reservoir.”

Arrow Exploration confirmed that strong production rates from existing tied-in wells, alongside encouraging results from new drills in Colombia, collectively supported the group’s aim to hit a production rate of 3,000 barrels of oil per dau (boe) within 18 months of its AIM listing in October 2021.

“We are now moving the rig to our next well location, the RCS-1 well, which is expected to spud before the end of May. Arrow’s current production exceeds 1,000 boe/d, producing positive cashflow for the Company during a high commodity price environment. This is an exciting time for Arrow, and we look forward to providing further updates on our progress,” said Abbott.

Power Metal Resources report promising Ditau core sample

Power Metal Resources reported the extraction of a core sample from the DIDD004 hole in its Botswana Ditau drill programme, which provided promising magnetic susceptibility readings.

The core displayed visible siliceous and haematitic zones, alongside local pervasive pyrite presented as disseminations and in veins.

Power Metal Resources also said extensive fracturing was observed throughout the core and elsewhere in the drilled hole.

The sample was extracted following a drill hole depth of 389 metres reached in the DITDD004 hole, the second operation at the Ditau project.

The Ditau project is currently held as a 50/50 joint-venture listed as Kanye Resources with Kavango Resources, who also operate the project, which has been identified as a potential source of carbonatite hosted rare-earth element, base-metal and possible precious-metal mineralisation.

The core was sourced from the group’s i10 target, which is a discrete 2.2 kilometre in diameter magnetic anomaly which the venture had previously modelled as a possible carbonatite.

Power Metal Resources confirmed that preliminary magnetic susceptibility readings were recorded on the core between 293-321 metres on the “zone of interest”, representing a combined 28 metres of core length.

The readings reportedly coincided with a visibly altered section that Kanye Resources is set to immediately cut half-core samples from to send to the assay laboratory for multi-element analysis.

“The core extracted from hole DITDD004’s Zone of interest, spanning a combined 28m, is fascinating from a geological perspective and we are eager to see the results from further analysis thereon – including laboratory multi-element assays,” said Power Metal Resources CEO Paul Johnson.

“The magnetic modelling undertaken to develop this target appears to be reliable, which is also particularly encouraging for DITDD004 and future drill holes within Ditau.”

“I look forward to reporting further plans and progress over the coming weeks.”

Future Steps

Power Metal Resources mentioned that a one kilometre Audio-Magnetotelluric (AMT) survey would be performed over the i10 target over the coming weeks, in a move to record data to additionally define the shape and form of the zone of interest.

The company added that Mindea Exploration and Drilling Services was in the process of mobilising the diamond core drill rig to target i1 at Ditau, which is the largest of three geophysical targets which Kanye Resources intends to drill in its current campaign, including i10, i1 and i8.

Power Metal Resources confirmed that a future update on the condition of the project would be released shortly regarding the drill hole.

The joint-venture added that its plan moving forward was to collect high-frequency AMT profiles over potential near-surface carbonite targets in order to resolve the location of breccia zones and intrusive sills/dykes intersected in drill hole DITDD003.

Kanye Resources said it had identified 12 geophysical targets at the Ditau Project, i1 to i12, which were believed to be caused by potential carbonatites or intrusive complexes that might host carbonatites, which account for the primary source of mined rare-earth minerals, and are valuable across a selection of high-tech industries.

Spin-Out Companies

Power Metal Resources also commented in its recent quarterly results that the company had made progress in its plans to spin out Golden Metal Resources, which is currently targeting listings on the London capital markets in Q2 2022, alongside First Class Metals.

The company added that First Development Resources and New Ballarat Gold Corporation were targeting listings in the London and Australian markets in early Q3 2022.

Power Metal Resources shares were down 1.7% to 1.4p in early afternoon trading on Wednesday, following the mining firm’s report.

FTSE 100 remains flat as investors seem unshaken by 9% inflation

The FTSE 100 was down 0.1% to 7,507.6 at midday on Wednesday, as record-high rates of 9% inflation seemed to surprise few people, with investors having accounted for the estimated spike in advance and little panic spotted on the market.

“Investing is an expectations game so it’s not really a surprise that the market has shrugged off the highest levels of inflation in the UK in 40 years given the number was actually slightly behind forecasts,” said AJ Bell investment director Russ Mould.

A selection of positive results also boosted the FTSE 100 higher, as the market brushed the gloomy economic outlook off its collective shoulder.

British Land Co shares climbed 3.9% to 526.7p as the company swung to a pre-tax profit of £958 million compared to a £1 billion loss the previous year.

The property development and investment group further announced a 12% growth in net assets.

“Operationally, our leasing volumes across Campuses and Retail & Fulfilment were the highest in ten years and were ahead of estimated rental value,” said British Land Co CEO Simon Carter.

“In London, demand continues to gravitate towards the best, most sustainable space where our Campuses are at a distinct advantage.”

Mould commented: “British Land is seeing demand for the ‘right’ kind of offices as it returned to profit for the first time since 2018 and eye-catchingly revealed it is leasing space at the fastest pace in a decade.”

“The easing of restrictions may not have led to an immediate return to the office en masse but there’s little doubt that employers are looking to tempt workers back for some of the working week and that means having attractive spaces for them to work in.”

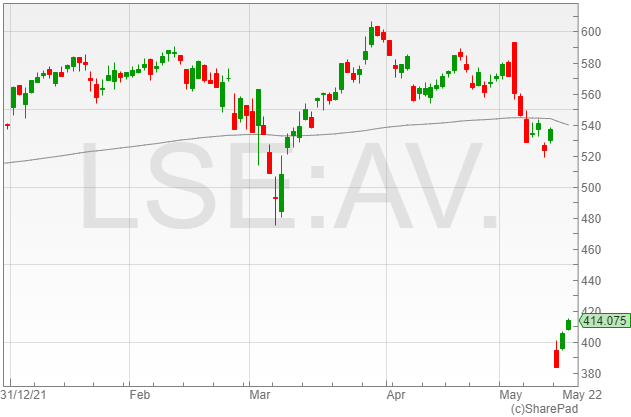

Aviva shares enjoyed a boost of 2% to 414p as a result of record-high Q1 general gross insurance premiums of £2.1 billion, which the firm attributed to strong growth across commercial lines in the UK and Canada.

“Insurer Aviva, which has been busily slimming down under chief executive Amanda Blanc, helped demonstrate its credentials as a honed corporate animal with strong first quarter trading including the best first quarter general insurance sales in a decade,” said Mould.

“For Blanc, who has made an impressive start to her leadership of the business, the low hanging fruit has now been picked and the underperforming operations sold off. She needs to work out how to maintain the momentum behind the business.”

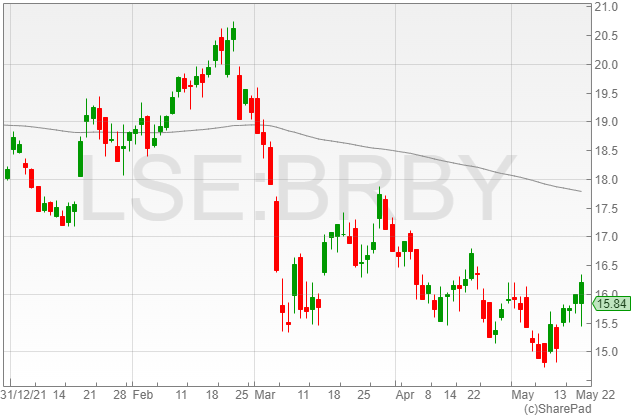

Burberry shares increased 1% to 1,600p, after the luxury brand announced an operating profit of £543 million in its full-year results, reflecting a 4.2% rise compared to its £521 million last year, reportedly in line with management expectations.

The brand has undoubtedly benefited from its wealthy clientele remaining predominantly unaffected by the snapping jaws of rising food and energy costs, with the company’s target consumer probably hardly realising the added expense to their weekly grocery shop.

“Burberry’s post-Covid recovery still has more to go, given it should see greater business once Asian tourists start travelling the world again,” said Mould.

“They have historically been keen buyers of Burberry products on their travels. China’s Covid resurgence is a headwind for now, but one might presume this is only a short-term issue.”

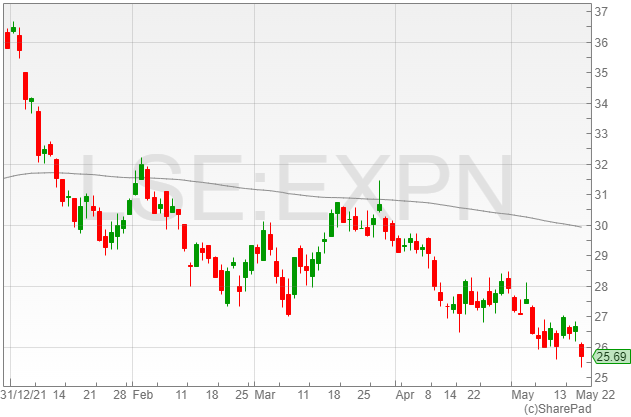

Experian shares fell 4% to 2,561p despite the credit-focused firm’s reported 17% revenue growth to $6.2 billion in FY2022 against $5.3 billion year-on-year as a result of high consumer-focused demand.

The company reported a moderate slowdown in expected growth in the range of 7%-9%, however, alongside a series of legal claims against the group “across all its major geographies.”

Experian confirmed that several claims were in enforcement, including a selection from the Consumer Financial Protection Bureau in North America and the Information Commissioner’s Office in the UK.

Stagflation, Burberry and Open Orphan with Alan Green

The UK Investor Magazine is joined by Alan Green for a rundown of key market themes and Uk equities.

We start by looking at Stagflation at the implications for the UK economy and markets. Stagflation is a period of rising inflation, economic contraction, and rising unemployment.

The UK satisfies the first two of these, however, unemployment remains robust. We look at whether rising inflation will soon hit jobs activity and what it could mean for equities.

We also discuss the relationship between the FTSE 100 and US indices and how this may develop if we see recession in the US.

Burberry has posted a respectable set of results and is proving a possible choice for income investors. Margins have improved with sales as the luxury brand jumps back from COVID.

Open Orphan’s valuation is worth attention. One could argue the current market cap doesn’t pay justice to their revenue growth and forecast profitability.

We update on the latest from Tertiary Minerals and their portfolio of assets including a selection in Nevada and Nambia.

Experian revenue grows to $6.2bn on high consumer-focused demand

Experian shares dropped 3.2% to 2,582.3p in late morning trading on Wednesday, after the company announced a 17% increase in revenue to $6.2 billion compared to $5.3 billion in its FY2022 results.

The credit-focused group said its positive performance was driven by strong demand for consumer-focused services across North America, Latin America and the UK.

The firm reported an operating profit growth of 16% to $1.4 billion from $1.1 billion year-on-year, and included a net gain from associate disposals of $90 million, which was offset by a business disposal loss of $43 million.

The group also incurred impairment charges net of reversals of $25 million, and restructuring and exceptional costs of $26 million.

Experian confirmed a pre-tax profit rise of 34% to $1.4 billion against $1 billion in 2021, boosted by a $186 million reduction in net finance costs from financing fair value remeasurements.

“We had a very good year with total revenue growth of 17% at both actual and constant exchange rates, and organic revenue growth of 12%,” said Experian CEO Brian Cassin.

“Benchmark earnings per share also progressed strongly, up 21%. Cash performance was very strong, with Benchmark EBIT to operating cash flow conversion of 109%, and actual exchange rates growth of 22%.”

“We have made major steps forward in Consumer Services, which is transforming the shape of our business, and we also progressed materially a series of strategic initiatives in Business-to-Business.”

The group announced an EPS uptick of 34% to 127.5c, reflecting the higher pre-tax profit, alongside a $16 million profit from discontinued operation, and a reduction in its effective tax rate and a higher level of shares in issue.

Experian also reported a total dividend increase of 10% to 51.7c against 47c year-on-year.

The group highlighted an estimated organic revenue growth in the slower range of 7%-9%, with modest margin growth at constant currency exchange rates supported by continuing investment in the execution of its strategy.

Experian said it was in a strong position to weather the current volatile macroeconomic disruptions on the back of its positive track record and robust, resilient performance.

Legal Claims

The company furthermore pointed out an “increasing number of pending and threatened claims and regulatory actions involving the group across all its major geographies”, which Experian said were being “vigorously defended.”

Experian confirmed that some claims were in enforcement, including a series from the Consumer Financial Protection Bureau in North America and the Information Commissioner’s Office in the UK.

The firm commented that it did not believe the outcome of any individual enforcement notice would have a material impact on the company’s financial position, however, Experian noted that in the possible case of unfavourable outcomes to the legal proceedings, the group could benefit from applicable insurance recoveries.

Aviva hits record £2.1bn in Q1 general gross insurance premiums

Aviva shares increased 0.7% to 408.5p in early morning trading on Wednesday, following the insurance group’s reported 5% rise to a record £2.1 billion in general gross insurance written premiums in Q1 2022.

The firm attributed its record levels to strong growth across commercial lines in the UK and Canada.

“First quarter trading was positive, and our performance shows the clear benefit of Aviva’s business mix across insurance, wealth and retirement,” said Aviva CEO Amanda Blanc.

“We delivered healthy sales numbers across all our major business lines, with UK customer numbers up by over 100,000 in the last year to 15.4m, increasing our confidence that we can transform Aviva’s performance and grow.”

The company confirmed a 2% growth in UK and Ireland Life sales to £8.4 billion, with a rise in Annuities and Equity Release, alongside Protection and Health, slightly offset by Wealth.

Aviva commented that its total BPA sales increased 29% to £843 million in the term, with a healthy pipeline weighted towards HY2 2022.

The insurance firm added that its UK and Ireland Life value of new business rose 31% to £144 million, with a VNB margin of 1.7% which was driven by Annuities and Equity Release VNB of £31 million.

Meanwhile, Aviva further noted a GI combined ratio of 96.4%, reflecting a £70 million cost for February storms in UK GI and more general motor claims frequency.

“We remain very well positioned to benefit from the long term growth trends in our markets, and to meet our upgraded financial targets,” said Blanc.

“This is underpinned by our strong capital position which benefits from rising interest rates.”

“Our financial strength and market leadership give us confidence that we can successfully navigate the current uncertain economic conditions.”

Aviva commented that it remained on track to meet its cash remittance, own funds generation and cost reduction targets announced at its FY 2021 results presentation.

The insurance group further assured investors that it was well-placed to navigate the volatile macro-economic environment, alongside its on-schedule acquisition, announced in March this year, of Succession Wealth to close in HY2 2022.

Aviva reiterated a dividend guidance of £870 million for 2022 and £915 million for 2023 following its capital return and share consolidation, which would amount to 31p and 32.5p per share, respectively.

Inflation hits 40-year high of 9% as food and energy costs surge

The Consumer Price Index (CPI) rose to 9% in April compared to 7% in March, according to figures reported by the Office of National Statistics (ONS) today.

The rise represents the highest 12-month growth since records began in 1997, and is also the highest rate on record for the constructed historical series, which kicked off in 1989.

The ONS commented that the last time inflation hit its current high was 40 years ago in 1982, with projections in the range of 6.5% in December to almost 11% in January.

Meanwhile, the CPI including owner occupiers’ housing costs (CPIH) gained by 7.8% year-on-year, marking an increase from 6.2% in March, the highest rate since records began in 2006.

The increase of 1.6% also marked the largest annual rate growth in the National Statistics series, along with the constructed series, which began in 1989.

CPIH rose approximately 2.1% in April 2022 on a monthly basis, against an uptick of 0.7% in April the last year.

Pain at the Pumps

The surge in inflation was attributed to housing and household services, which represented 2.7% of the annual rise, with the bulk of the rise due to climbing electricity, gas, fuel and other housing costs, while transport accounted for 1.4% of the growth.

The ONS confirmed the largest upward contributors to the CPIH increase were related to housing and household services at 1.2%, with restaurants and hotels contributing 0.1% and recreation and culture accounted for a 0.1% rise.

The most significant downward contribution was reportedly due to clothing and footwear, which contributed 0.09% to the figures.

“The surge in energy prices is draining us dry, after gas prices almost doubled in a year. In April, the huge hike in the energy price cap pushed inflation to a 40-year high of 9%,” said Hargreaves Lansdown senior personal finance analyst Sarah Coles.

“Unfortunately, this doesn’t come as a massive surprise to anyone. After-all we have been living through this horrible period, so we know all-too well how expensive life is getting.”

The energy price cap rose 54% in April, sending household energy budgets skyrocketing with an additional £700 per year in energy costs.

The war in Ukraine sent the cost of gas up by almost 100% year-on-year, and petrol surged to 161.8p per litre compared to 125.5p month-on-month, setting the price of filling a 55-litre car at £19.97 higher than in April 2021.

Analysts revealed that 40% of people had cut back on non-essential car travel to save on fuel costs.

The energy price cap is scheduled for a further rise between 30% to 50% in October this year, which is set to pile even more pain onto struggling consumers.

“What makes things even worse, is that we know that this is just the first blow, and we’re set for a follow-up in October that could send us reeling,” said Coles.

“Energy price hikes would be bad enough on their own, but we’re also having to deal with record fuel costs, eye-watering rises in supermarket prices and the soaring cost of home repairs and improvements.”

Food Prices

The cost of living is also starting to strain household food budgets, with a reported 41% of consumer making the concerning decision to purchase less from grocery stores, demonstrating that the crushing rate of inflation has already gone far beyond impacting frivolous purchases such as high-end fashion and specialty goods.

The price of food and non-alcohol drink rose 6.7% since last year, with pasta increasing 10.4%, milk rising 16.1% and margarine spiking 22.7% across supermarket offerings.

“Unfortunately, these price rises aren’t over yet. The conflict in Ukraine has pushed up the price of food globally, but it has also accelerated the rising cost of animal feed and fertiliser, which are feeding through into farm costs,” said Coles.

“When you add in the cost of fuel for manufacturing and distribution, it will keep pushing prices up at the supermarket in the coming months.”

Interest Rates to Rise

The Bank of England have been urged by the government and by consumers to tackle the issue of surging inflation, which has run far beyond its target rate of 2%. However, Bank governor Andrew Bailey told cabinet ministers this week that he was powerless to stop the crushing tide of inflation, despite the institution’s efforts to stamp out spiking costs by hiking interest rates 0.25% to 1% earlier this month.

The Bank is set to raise interest rates to 1.25% in its next meeting in June, however experts have warned that this will not stop inflation in its tracks, and it will add a fresh burden to households already struggling to cut down on the essentials to survive.

The UK economy has been through an awful month of inflation; unfortunately, with inflation set to hit 10% in October, the worst is yet to come on the horizon.

Burberry maintains outlook for 2022

Burberry reported a jump of 32% in adjusted operating profits followed by reaffirming its outlook for the year in the luxury fashion company’s preliminary results on Wednesday. Burberry’s results were in line with market and management expectations.

Burberry noted a 21% rise in revenue from £2.34bn to £2.83bn in 2022 with retail comparable store sales contributing through an 18% rise and full-price comparable-store sales seeing a 24% rise.

The group’s revenue jump was driven by the recovery from the pandemic whereas, the 18% rise in retail comparable stores was due to full-price sales which were slightly counteracted by the exit of markdowns in mainline and digital stores.

Burberry’s wholesale revenue generated £512m to the the total group revenue due to strong orders in Americas and recovery in Asia from travel retail, and licensing added £41m in 2022.

Total comparable store sales increased 6% as the pandemic caused disruptions in operations particularly in the fourth quarter of FY22.

However, Asia Pacific noted a 13% rise in comparable store sales with full-price sales noting an increase of 29%.

In Asia, Mainland China’s comparable store sales increased 37% and full-price comparable store sales was up 54%.

EMEIA comparable store sales dropped by 18% with full-price seeing an 11% decline owing to a slowdown in tourist shopping which generally contributes 50% of the total comparable store sales in the region.

Due to larger investments and “cost normalisation”, Burberry reported an 18% increase in operating expenses.

The group reported a 4% increase in operating profit to £543m and adjusted operating profit surged 32% to £523m which matched management expectations said the luxury fashion company. Burberry’s reported operating margin was 18.5%.

Pretax profit for Burberry recorded a 4% rise from £490m to £511m in 2022 out of which £396 was attributable to shareholders.

In 2022, the group generated £340m in free cash flow which was £9m lower than 2021 and noted a cash conversion of 106%.

Burberry declared an 11% rise in the annual dividend to 47p from 42.5p in 2021.

The cash generated from operating activities rose due to higher profits and strict management of working capital.

Burberry has confirmed its guidance of high single-digit revenue growth for 2022.

Gemma Boothroyd, Freetrade analyst, said,”New CEO Jonathan Akeroyd will be hoping that by winding up markdowns, the retailer will re-establish its exclusivity. But the only way that strategy pays off is if countries with high spending power play ball.”

“Akeroyd’s ability to hit the ground running heavily depends on demand from the Chinese market. Today’s results show the demand is there, the problem is, China’s Covid policies are out of his control.”

“China’s a long-term investment. Current Covid restrictions are short-term hurdles, but Burberry’s eyes are on the longer-term horizon. And it’s sensible. Akeroyd’s overarching goal is to reposition the brand, redefining its reputation.”

“That transformation won’t happen overnight. So investors still twiddling their thumbs on Burberry’s pre-pandemic share price recovery will be waiting a while still.”