Deliveroo has appointed Lord Simon Wolfson to its board as a non-executive director.

Lord Wolfson is the Next chief executive and started on the board this week ahead of the delivery service’s stock market floatation.

Will Shu, founder and chief executive, said: “We are looking forward to working with him as we continue to innovate, developing new tech tools to support restaurants, to provide riders with more work and to extend choice for customers, bringing them the food they love from more restaurants than ever before.”

Wolfson said the company was an “exciting, innovative and fast-growing company that, like Next, relies on advanced technology to deliver a market-leading proposition”.

Shu commented on Deliveroo’s performance over the past year: “We’ve demonstrated our model is profitable. We also saw our existing customers looking to order more often, also ordering for the family more frequently, we saw average basket sizes increase, and also ordering a wider range of products.”

Last year, Amazon bought a 16% stake in the company. The money is being spent on “new tech tools to support restaurants, provide riders with more work and extend choice for customers.”

“We are really pleased our shareholders see the opportunity and growth potential ahead of us,” added Shu.

Superdry shares fell 11% on Tuesday after the group warned over its future amid the pandemic.

In the 11 weeks to 9 January, revenues fell 52% as stores closed amid new restrictions. In the six months to 24 October, the company posted a pre-tax loss of £18.9m, compared to the £4.2m loss a year previously.

Superdry co-founder said: “Covid-19 has brought substantial challenges to Superdry as with many other brands, and this has continued through the first half and into the second with renewed lockdowns in our key markets.

“While revenue and underlying profit have been impacted by the external conditions, the brand has continued to focus on the reset, however, with over 70% of stores currently closed and having to shut a significant number over peak, it will take time to see the benefits of all our hard work flow through to the results.”

In a statement, the retailer said: “The group directors noted that the risks set out … indicate that a material uncertainty exists and may cast significant doubt on the group’s ability to continue as a going concern and, therefore, that it may be unable to realise its assets and discharge its liabilities in the normal course of business.”

Net cash reserves remained strong over the year and stood at £54.8m as of 9 January.

“We continue to have a total of over £130m of available liquidity at hand. Our £70m asset-backed lending facility remains available, having not been used in the year to date, and is currently still undrawn,” said the retailer.

Centamin shares rose on Tuesday morning after the group posted a strong 2020 performance and a rise in revenue.

Group revenue for the year rose 25% from $658.1m to $829m. Gold sales for the quarter dropped 42% as the group mined lower grade material.

Martin Horgan, CEO of Centamin, said: “Today’s quarterly and subsequent full year 2020 results were delivered in-line with the revised guidance we issued in October.

“This follows the capital markets event we hosted in December, where we presented the conclusions of the Phase One Life of Asset review and three-year outlook, detailing clear cost-saving, exploration and productivity initiatives, forming part of our plans to unlock Sukari’s potential.”

“We remain convinced about the strategic rationale of combining Endeavour and Centamin to create a diversified gold producer with a high-quality portfolio of assets,” said Endeavour Chief Executive Sebastien de Montessus.

“The quality of information received during the accelerated due diligence process has been insufficient to allow us to be confident that proceeding with a firm offer would have been in the best interests of Endeavour shareholders.”

AO World reported a 67.2% surge in revenue after the group saw a strong demand in electrical sales over the Christmas period.

The online electrical retailer saw revenue in the third quarter jump to £457.3m. Sales in Germany alone surged by 77% to €73.6m.

AO World will invest in new staff and infrastructure to meet demand. The group hired 1,500 employees in 2020 and staff in warehouses, vehicles and drivers.

Founder and chief executive John Roberts said: “I believe we’ve seen ten years of change in ten months, and experienced our strongest ever peak trading period… We look forward to the last quarter and the next financial year with confidence as the structural shift to online is cemented in consumers’ minds.”

“Now that customers have experienced a better, digital-first way to shop for electricals, I believe the majority will never look back.”

Despite the positive trading update, shares were down 7% in early trading.

Analysts at Shore Capital commented: “This is an upbeat trading update, which shows the continued momentum given both the structural shift online and the benefit as other brands physical electrical stores remain closed, as they are not deemed essential retailers during lockdown 2.0 and now lockdown 3.0.”

“This is AO World’s moment to shine given that the online market has seen a structural shift that could be permanent by consumers… The big challenge will be whether the revenue momentum can continue during the first quarter in financial year 2022 given the tough comparatives that the business will start cycling.”

Sales across the European Union fell 23.7%. Just 9.9m new vehicles were registered, which is down from the 13m new cars that were registered in 2019.

The biggest fall was in Spain, where sales dropped by 32.3%. In Italy, sales fell ‐27.9% whilst in France they were down by 25%.

Sales remained weak over the whole pandemic, however, were lowest in March and April amid the initial lockdowns.

“Containment measures – including full‐ scale lockdowns and other restrictions throughout the year – had an unprecedented impact on car sales across the European Union. 2020 saw the biggest yearly drop in car demand, said industry body ACEA.

Mike Hawes, the chief executive of SMMT, said: “2020 will be seen as a ‘lost year’ for Automotive, with the sector under pandemic-enforced shutdown for much of the year and uncertainty over future trading conditions taking their toll.

“However, with the rollout of vaccines and clarity over our new relationship with the EU, we must make 2021 a year of recovery. With manufacturers bringing record numbers of electrified vehicles to market over the coming months, we will work with government to encourage drivers to make the switch, while promoting investment in our globally-renowned manufacturing base – recharging the market, industry and economy.”

Sales in electric cars almost trebled this year whilst sales of petrol and diesel cars have plunged.

The SMMT commented on the continuing demand for battery and hybrid vehicles: “Market share for battery electric vehicles (BEVs) and plug-in hybrid vehicles (PHEVs) continued to grow significantly, up 122.4% and 76.9% respectively.

“BEVs recorded their third highest ever monthly share of registrations at 9.1%, while PHEV share increased to 6.8% – a combined total of more than 18,000 new zero-emission capable cars joining Britain’s roads.”

Global equities were hushed on Monday as the US enjoyed its first national holiday of the year, leaving the rest of the markets to stroll through their quietest trading session of 2021. It was a sign – if one was even needed – that Europe lacks direction without the US at the helm to direct proceedings.

Lacking a US intervention, and seemingly unimpressed with data from China showing GDP grew 2.3% in 2020, European indices had a muted day all-round. It seems any pent-up momentum might be reserved for Wednesday, when President-elect Joe Biden is finally inaugurated in Washington after months of vitriol and vilification from outgoing President Donald Trump and his administration.

Global equities had a similarly subdued response to Biden’s $1.2tn economic relief plan announced last week.

With Brent Crude slipping to the wrong side of $55 – leaving BP (LON:BP) and Shell (LON:RDSA) to mull over falling shares – the FTSE lost -0.22%, down to 6,720.65 points, by the end of trading on Monday afternoon.

Meanwhile, Eurozone indices spent the day on the positive side of the spectrum, if only by a little. The DAX gained to 13,848.35 with a +0.44% increase, while the CAC clung to 5,617.27 after a meagre +0.099% climb.

As Spreadex financial analyst Connor Campbell put it: “that’s about it”.

Monday marked one of, if not the most, quiet sessions since the year began. While tomorrow is likely to be something of a write-off as well, Wednesday brings with it all the buzz and excitement of a new President, whose “blitz” of presidential decrees to undo Trump-era policies are reportedly ready to go from the moment he steps foot in the White House.

It comes as no surprise then that this week’s “star of the show”, Campbell says, is Wednesday’s inauguration.

However, as soon as Wednesday’s initial excitement is over, attention will turn to whether or not the Democrats will actually be able to implement Biden’s campaign pledges – one of which being the Covid-19 stimulus package he announced last week. It still needs to pass Congress before it can be carried out, and will be the first test of the new administration’s ability to strong-arm new policies through a “precariously balanced, if blue-tinged, Senate”.

How the Democrats perform in the coming days and weeks will set the tone for how investors feel about the Biden presidency as a whole, and will determine which direction global equities head in too.

On top of the high-stakes politics happening in D.C., there is scheduled to be a webinar appearance from Bank of England governor Andrew Bailey on Wednesday – which always has the potential to shift the UK market, for better or worse – followed by the first European Central Bank meeting of 2021 on Thursday.

Thursday also marks the next addition to a slew of increasingly alarming US jobless claims reading – in danger of hitting 1 million if it again overshoots estimates as it did last week – with Friday then rounding up the figures of January’s economic performance with the latest round of flash PMIs.

So, a slow start to the week overall, but by all means keep your seatbelts fastened for developments later on in the week.

Deliveroo had already raised $1.5bn from investors with plans to use the funds to innovate, set up for delivery-only kitchen sites, and grow its online grocery business. Its highly-anticipated float, predicted to be on the London market – and touted to be as early as next month – will be the biggest new share issue in three years.

Last week, Jitse Groen – Takeaway.com’s chief executive – said that he would “make life very, very, very complicated for the competitors” in the capital by undercutting them on delivery prices and investing heavily in a new courier network.

Deliveroo currently operates across 12 countries – mostly in western Europe but also in Australia, Hong Kong, Singapore and the United Arab Emirates.

The company was founded by Will Shu — a former investment banker — in 2013. Its heavy investment in technology led to a loss of £319.9m in 2019, which forced the company to take out a short-term £198m loan to mitigate the losses, but enjoyed a surge in sales during the pandemic as online food delivery helped to subsidise the paralysis of the restaurant industry.

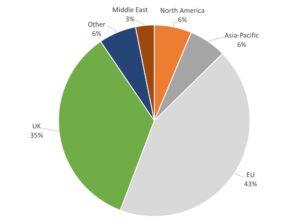

A new report by the London Central Portfolio (LCP) reflecting on lettings trends across 2020 has revealed that almost 50% of new tenants in prime London properties were from the European Union.

The LCP’s data outlined the home regions of new tenants letting London properties in 2020. Travel restrictions during the pandemic resulted in a smaller proportion of tenants arriving from the Middle East and Asia-Pacific, leaving the EU to represent the largest share of new tenancies. The high proportion of UK tenants highlights the increasing affordability of prime London rents and a desire to live in Central London.

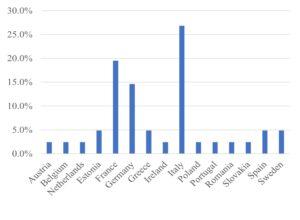

The data was also used to collate new tenancies in 2020 by their home country from the EU 27 nations. Italian and French nationals represented the largest proportion of new EU tenancies in LCP’s portfolio for the year – at 26.8% and 19.5% respectively. Despite the disruption from both Brexit and the pandemic, the appetite to live in London appears to be as strong as ever, as the city continues to flaunt its credentials as an employment and cultural hub.

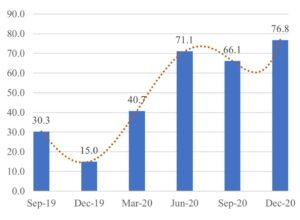

The average vacant period between tenancies in 2020 was varied across the year, reaching a peak of 76.8 days on average in the final month of the year. Stock that was not let out in the “traditionally buoyant” period in September due to the impact of the pandemic remained available in the winter months, increasing vacancy periods in Q4. Longer vacancy periods could also be reflective of increased hygiene efforts on the part of landlords who were advised to deep clean their properties weekly and in between tenants, extending vacancies so that there was enough time to ensure properties were adequately disinfected.

The average length of tenancies increased across 2020 as tenants were less inclined to move during the pandemic. During the spring lockdown, the UK government advised people not to move house, citing the increased risk of spreading Covid-19 as they travel. Average tenancy length also remained “sticky” in 2020 due to the “high quality of LCP’s rental properties and refurbishments encouraging tenants to stay put”.

New tenants in 2020 were overwhelmingly younger people, between the ages of 18 to 29, with 90% of total tenants all under the age of 40. The data confirms the continuing trend of young adults heading to the capital for employment opportunities, but perhaps also reflects the growth in older adults and families opting to move away from city centres to minimise infection risk during the pandemic.

The spring of 2020 saw fewer new tenancies than the historical average due to the impact of the pandemic, although there was a brief recovery once the property market reopened in early summer. This was then followed by a slower September due to the fall in overseas students.

Andrew Weir, CEO of LCP, commented on the 2020 market trends:

“Notwithstanding the pressures of a global pandemic and Brexit negotiations, London remained attractive to EU nationals who made up 43% of new tenancies. Italy and France led the way representing 46.3% of these tenancies. Happy to capitalise on the lack of overseas demand, a large proportion of UK tenants (35%) moved to prime London attracted by widely advertised rent reductions, as landlords competed within a depleted pool of tenants.

“The impact of travel restrictions, on a market predominantly reliant on overseas students and young professionals, has been reduced demand, surplus of stock and longer void periods. Existing tenants have stayed in situ where the property is of a high standard and diligently managed. They have broadly been comfortable with paying passing rents during a time when new tenants have been able to negotiate significant discounts. This highlights the importance of tenant retention during periods of increased competition where prime London in 2020 was labelled as a renter’s market. The strength of covenant for those tenants within LCP’s managed portfolio has resulted in zero defaults in 2020.

“Looking to the future, landlords and buy-to-let investors should take reassurance that once the vaccine has rolled out and travel restrictions are lifted, London will again experience an influx of overseas tenants waiting in the wings to continue their metropolitan life that they have missed over the last year”.

Shares at British-Swedish pharmaceutical firm AstraZeneca (LON:AZN) have climbed nearly 1% after it announced thatUS regulatory bodies have approved the use of its treatment for patients with previously-treated HER2-positive advanced gastric cancer.

In the US, gastric cancer is most frequently diagnosed in the advanced stage, with only around 5% of patients surviving beyond the five year mark. Approximately one in five gastric cancers are HER2 positive.

AstraZeneca and Daiichi Sankyo Company, Limited (Daiichi Sankyo)’s joint effort, Enhertu (trastuzumab deruxtecan), has been approved in the US by the Food and Drug Administration (FDA) for the treatment of adult patients with “locally advanced or metastatic HER2-positive gastric or gastroesophageal junction (GEJ) adenocarcinoma who have received a prior trastuzumab-based regimen”.

In a pre-specified interim analysis from the DESTINY-Gastric01 trial, patients treated with Enhertu had a 41% reduction in the risk of death versus patients treated with chemotherapy, with a median OS (the length of time from the start of treatment that patients are still alive) of 12.5 months versus 8.4 months.

Results from the trial also showed a confirmed ORR (the percentage of people in a study who have a partial or complete response to the treatment) of 40.5% in patients treated with Enhertu, compared to 11.3% in patients treated with chemotherapy. Patients treated with Enhertu had a 7.9% complete response rate and a 32.5% partial response rate, compared to a complete response rate of 0% and a partial response rate of 11.3% for those treated with chemotherapy.

Overall, Enhertudemonstrated a median progression-free survival rate of 5.6 months, compared to 3.5 months with chemotherapy.

Following US approval, an outstanding amount of $115m is due from AstraZeneca to Daiichi Sankyo as a “combined 2nd-line and 3rd-line milestone payment in HER2-positive gastric cancer”. In AstraZeneca, the milestones paid will be on top of the upfront payment made in 2019 and subsequent capitalised milestones, and amortised through the profit and loss.

Ronan Kelly, MD, MBA, Director of the Charles A. Sammons Cancer Center and the W.W. Caruth, Jr. Chair of Immunology at Baylor University Medical Center, Dallas, Texas, US, welcomed the news of Enhertu’s approval:

“Patients with metastatic HER2-positive gastric cancer with progression following 1st-line treatment have historically faced poor outcomes, including low response to treatment and rapid disease progression. This approval represents the first time a HER2-directed medicine has demonstrated a significant improvement in survival compared to chemotherapy following initial treatment in the metastatic setting, and it has the potential to become the new standard of care for this patient population”.

Dave Fredrickson, Executive Vice President, Oncology Business Unit, added: “Today’s approval of Enhertu represents the first HER2-directed medicine approved in a decade for patients with HER2-positive metastatic gastric cancer. We are thrilled to bring this important medicine to more patients and physicians in the US”.

The company has been firmly in the headlines over the past year for its efforts to develop a Covid-19 vaccine, which in conjunction with Oxford University is currently being rolled out across the UK as part of a nationwide vaccination programme. AstraZeneca’s vaccine was among the fastest to be developed in the world. The UK government has already ordered 100m doses.

Shares at AstraZeneca hiked 0.80% to 7,653.00p at GMT 12:54 on Monday afternoon, extending a week-long gain of +1.57%. The stock has received a consensus rating of “hold” on Marketbeat, with an average rating score of 2.35 out of 5, and a P/E ratio of 100.05.

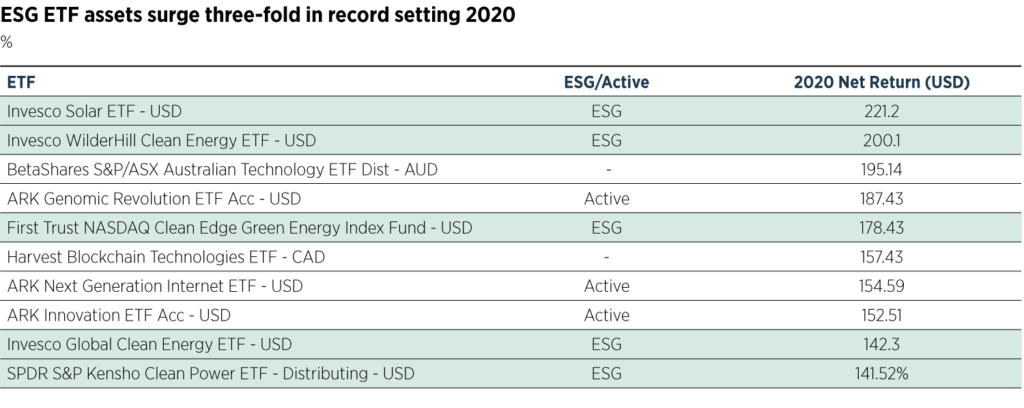

While the Covid-19 pandemic stranded global markets in the eye of the storm, many investors switched their usual holdings for ESG stocks as the merits of investing responsibly became more apparent.

Data from TrackInsight (the world’s first ETF analysis platform) revealed that, while wider stockmarkets were falling 20% in the spring of last year when the impact of the pandemic truly unfolded, ESG portfolios outperformed due to their higher exposure to the healthcare and technology sectors.

As well as this, investors have begun to realise that business models which support and capitalise on a sustainable future will no doubt become “more robust” as the implications of climate change materialise.

According to ESG Clarity, investors also increasingly want to put their funds behind companies supporting all stakeholders – employees, clients, supply chains and shareholders – at a time when societies are “united in the face of the pandemic” (the ‘social’ element of ESG).

Anaelle Ubaldino, head of ETF research and investment advisory at TrackInsight, commented:

“It’s clear that 2020 was a long-awaited turning point for ESG ETFs with huge growth in this sector. As competition for potentially trillions of dollars of new ESG assets heating up, we expect to see more issuers enter the ESG ETF market over 2021″.

On Monday, TrackInsight announced the launch of ESG Observatory, an online hub that provides tools, data and analysis on the global market for ESG ETFs, for investors “looking to build sustainability into their ETF portfolios”.

The project has been formed of a “unique triumvirate with unsurpassed knowledge of the ETF and Sustainable Investment industries; combining the ETF expertise of TrackInsight, the independent ESG Consensus® methodology of Conser and guidance on mapping ETFs against the Sustainable Development Goals provided by the SDG Investors Partnership of UNCTAD – the United Nations Conference on Trade and Development”.

ESG Observatory is supported and sponsored by Amundi Asset Management.

The aim is to provide transparency for users who seek to “invest with purpose” by helping them to monitor and analyse key ESG investment trends, compare the different ESG strategies offered by ETF issuers, and measure which products are contributing most towards meeting the United Nations Sustainable Development Goals (SDGs).

James Zhan, Senior Director of Investment and Enterprise at UNCTAD, commented on ESG Observatory’s launch:

“In view of the material risks posed by issues such as climate change and the global pandemic, investors are paying increasing attention to sustainability in their investment decisions. By looking into the impact of ESG ETFs from the SDG angle, we believe TrackInsight’s ESG Observatory can help align financial products with sustainable outcomes, and ultimately contribute to channelling finance to key SDG sectors”.

And TrackInsight’s founding CEO, Jean-Rene Giraud, added:

“The astonishing pace of adoption for ESG ETFs is being driven by demand from institutional and retail investors who realise that their investment decisions have consequences and who want to invest with purpose. With the market for ESG ETFs exploding worldwide, ESG Observatory provides a valuable resource for those investors who want independent data and information on the market, knowledge of the investment choices they have and metrics to gauge which ETFs are contributing most to a sustainable future”.