Hobbyist shares may benefit from lockdown

As large proportion of the developed world’s population become confined to their homes, people will naturally seek ways to entertain themselves. Video games will be the go-to choice for most of the younger generations but there will be a huge demand from hobbyists for the models offered by Hornby and Games’ Workshop.

At the time of writing, a large number of products on Games’ Workshop’s Warhammer website were sold out, suggesting a surge in demand.

Warhammer is commonly known among enthusiasts as ‘plastic crack’ due to the addictive nature of collecting and painting the models, and evidence points to people stocking up for long days inside.

The creation of an almost cult-like Warhammer following has been reflected in consistently strong growth for Games’ Workshop in recent years.

In the half year to 31st December 2019, Games’ Workshop revenue grew by 19% to £148m from £125m the year prior, and profit before tax grew by 43% to £58.6m.

Shareholders have reaped the rewards of Games Workshop’s popularity and increasing profits with share rising from lows of 2,200p in 2018 to 2020 highs of 7,350p.

Shares have since fallen to 4,230p which presents an interesting entry point given the biggest problem the Games Workshop will now have is ensuring their website and order processes can meet demand.

Consider these three exciting energy shares

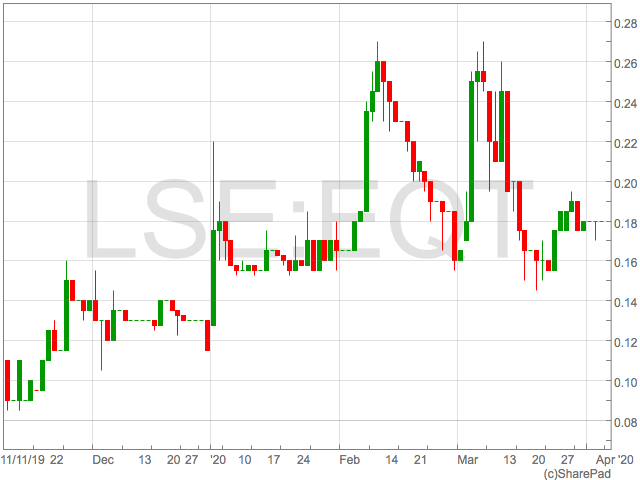

EQTEC

We kick things off with a company driving forward the circular economy with waste-to-energy technology. London-listed EQTEC operates a multi-channel revenue model that sees them earn revenue from technology licensing, engineering support and output sales. EQTEC’s waste-to-energy technology uses inputs such as refuse and farming waste to create energy in the form of gas. Driven by an experienced management team, the company has announced a number of strategic partnerships in recent months which has seen their operations expand into North America and numerous locations across Europe. The company’s technology is providing a positive environmental impact by keeping waste out of landfill and increasing the use of greener fuels. Hurricane Energy

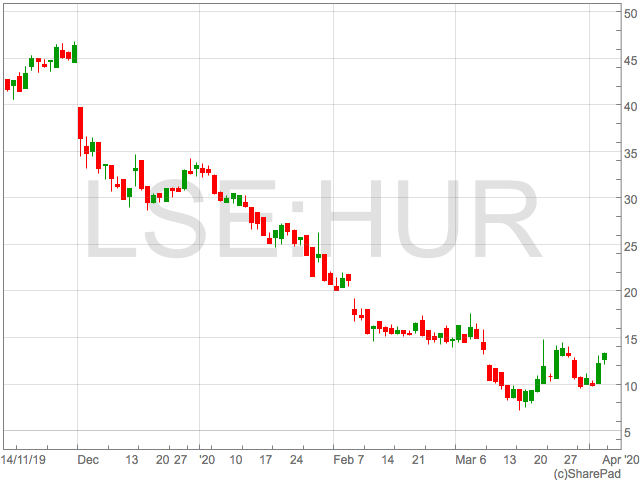

Hurricane Energy

Despite the oil sector being the subject of pressure from a shift in investment trends away from fossil fuels towards greener forms of fuels, the drop in oil prices has heavily hit the oil sector and there are a plethora of companies offering great value.

With a market cap of just £258 million, Hurricane Energy does just that.

Hurricane Energy is operating fields just west of the Shetland Islands and has had much success with their exploration programme, which still ongoing offers potential for further discoveries.

Hurricane Energy is in the favourable position of having $164 million cash as of 18th March 2019 which will ensure funding for the drill programme in the foreseeable future.

In addition, Hurricane had revenues of $170 million and profit after tax of $58.7m in 2019 almost eradicating the need to raise capital a dilute shareholders in the pursuit of their long term goals.

Despite the lower price of oil, shares look very cheap considering the potential for good news from their ongoing exploration program which could sees further increases to production and revenue.

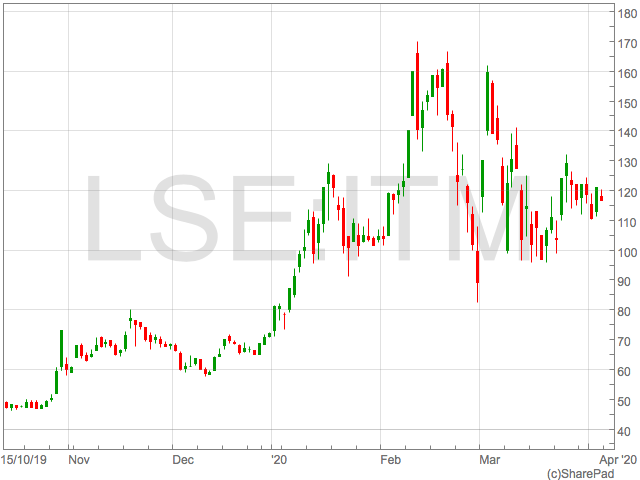

ITM Power

ITM Power provides specialist Hydrogen Power Stations that utilises Proton Exchange Membrane (PEM) technology.

The UK-listed company products includes both power storage and fuels with a wide range of applications ranging from powering buses through to storing and providing hydrogen energy for entire islands.

ITM is receipt of government funding, the most recent tranche was £7.5 million from the Department for Business, Energy and Industrial Strategy to develop the next phase of the Gigastack Hydrogen project.

Gigastack is a renewable hydrogen project that uses wind power and demonstrates the forward thinking nature of ITM and how their business is facilitating the UK’s drive towards becoming net-zero by 2050.

During the development stage of the business ITM has understandably posted losses in recent years. However, the company has a strong balance sheet having recently raised £58.8 from placings and the receipt of strategic investment from their partners. One for the future.

The Lloyds share price is too hard to ignore at current levels

The Lloyds share price (LON:LLOY) has suffered terribly since the onset of the coronavirus crisis, having more than halved since the beginning of 2020.

The writing of a letter by the Bank of England to UK banks effectively instructing them to cease all unnecessary payouts, including ordinary share dividends and buybacks, was the final straw for the market and shares fell beneath 30p.

However, with most of the ‘bad’ news now currently priced into shares, there is the argument that the sellers have been shaken out, leaving plenty of opportunity for a share price recovery.

To make a case for entering Lloyds shares at current levels investors should refer back to the fundamentals of the company in 2019. This will provide a reference to where Lloyds’ underlying business should return to as the UK economic recovery takes place over the next 12-24 months.

One should note that the much touted ‘V-shaped recovery’ to the coronavirus crisis in the early days of the spread is unlikely to happen due to the structural changes to the employment market.

Sharp increases in unemployment across the globe means the recovery will be slightly more protracted. Nonetheless, animal spirits will return and this will untimely drive Lloyds’ operations back up to prior levels.

Lloyds share price

Highlighting the opportunity for investors at current levels is the valuation of Lloyds shares based on historical earnings. Lloyds net profit was £3 billion in 2019 meaning at 28p, Lloyds is trading at a 6.5x earnings multiple. However, it is entirely feasible that Lloyds profit is completely wiped out in 2020 making PE ratios utterly useless to judge Lloyds in 2020. The reduction in interest rates by the Bank of England in an effort to support the economy will have an impact on Lloyd’s net interest income so investors should expect this to reduce earnings while rates remain low. In addition, banks including Lloyds are providing payment holidays while ceasing the provision of mortgages which will also hit revenue. Investors should look past 2020 and to the period when the economy has been resuscitated. This is where the value in Lloyds current share price lies as this is when earnings return and will make 28p look cheap. It is also the period that Lloyd will start paying dividends again. With a PE Ratio of 6.5x historical earnings Lloyds shares are too hard to ignore given the potential for recovery, notwithstanding heightened volatility while we wait. The Lloyds share price was 28p in morning trade 3rd April.Oil jumps as much as 35% lifting FTSE 100 after Saudi/Russia production cut reports

The price of oil soared on Thursday afternoon following reports Russia and Saudi Arabia were to agree on a production cut that could amount to 10 million barrels a day.

The news was first unveiled by President Trump who put out a tweet following a telephone conversation with ‘his friend’ the Crown Prince of Saudi Arabia.

Russia and Saudi Arabia have been locked in a price war following the decision by Russia to increase production which has rocked global oil markets.

Oil prices ripped higher with both Brent and WTI up over 25% and Brent Crude rose over $30. Following Trump’s tweet, reports emerged of Saudi Arabia requesting an emergency OPEC meeting. In an interview with Bloomberg, Ryan Sitton, Texas Railroad Commissioner , said before the US lockdown the global oil market was 18 million barrels a day oversupplied which he thought was now at around 22 million barrels a day. This would mean cutting 10 million barrels would still leave an oversupply in the oil market and could pressure oil prices as storage facilities continue to become full. Nonetheless, equities surged on the back on the news with oil heavy weights BP and Royal Dutch Shell adding to gain in the immediate reaction. Shell was up over 10% on Thursday afternoon adding a significant number of points to the FTSE 100. Shares had been trading towards their lows before the announcement following the largest rise in US unemployment figures in history. Initial jobless claims rose by 6.6 million, doubling last week’s 3 million. This is the sharpest increase in unemployment figures in US history. During the financial crisis it took 19 weeks for 10 million to register unemployed in the US and the same amount have been recorded in just two. The FTSE 100 had rallied to highs of 5,547 before the rally faded into the close.Just spoke to my friend MBS (Crown Prince) of Saudi Arabia, who spoke with President Putin of Russia, & I expect & hope that they will be cutting back approximately 10 Million Barrels, and maybe substantially more which, if it happens, will be GREAT for the oil & gas industry!

— Donald J. Trump (@realDonaldTrump) April 2, 2020

Equity Funds to buy to navigate the coronavirus crisis

Equities have sunk during the coronavirus-indiced selloff and now offer a range of opportunities that haven’t been seen since the financial crisis.

Those choosing to use the services of fund managers are being presented with a plethora of options to take advantage of the low prices in equities.

ETFs that follow the price of indices offer low-cost exposure to indices such as the FTSE 100 for investors who want to passively track any broad recovery in stocks.

iShares Core FTSE 100 UCITS ETF does just that with an ongoing cost of just 0.07% and a 5.8% distribution yield at the end of March 2020 when the FTSE 100 was around 5,500.

The passive versus active approach to money management rages on and actively managed funds in the UK are as still as popular ever, despite the growth of ETFs. This has, however, created benefits for investors in the form of lower costs for OEICs, Unit Trusts and Investment Trusts.

In the actively managed space, we would point to high income funds in Shroders Core UK Equity and the Aberdeen Standard Equity Income Trust that yield 6% and 10% respectively.

Expect these yields to change as we learn of more dividend cuts but both funds are dominated by high-quality FTSE 100 companies such as Shell, BP, GSK, AstraZenec and British American Tobacco, so we wouldn’t expect the adjustments to the fund yields are overly dramatic.

A theme we feel that will be as important beyond the coronavirus crisis as it was before is sustainability and making investments that provide a positive impact.

With this in mind we continue to be impressed by JLEN Environment Assets that reaffirmed its dividend as many FTSE 100 companies scrapped them all together. At 109p JLEN yields in excess 5.8%.

The JLEN Investment Trust invests in a portfolio of renewable energy assets including hydro, biomass, solar and wind. Demonstrating the forward-thinking nature of management, JLEN announced the acquisition of a biomass plant as the UK moved towards the peak of coronavirus, a decison investors should take confidence in.

YourGene to assist with COVID-19 testing

Formally Premaitha Health, in 2018 the name changed to YourGene (LON:YGEN) and the focus shifted to on being an international molecular diagnostic group, which is successfully commercialising genetic products and services.

These molecular tests are less time and labour intensive than traditional culture methods and can provide rapid diagnosis. Interestingly, the company is apply its services to COVID-19 testing.

Its interims to September reported its first EBITDA profit which was £0.3m after a 97% increase in revenue to £7.8m. The reorientation of the business on four strategic growth priorities has produced 56% organic growth with a gross profit margin of 60% for a 141% increased Gross Profit to £4.7m.

What’s exciting us is the agreement for contract manufacturing services for ‘part’ of a COVID-19 Test. The agreement is with a subsidiary of Novacyt (LON:NCYT) which recently recorded a £131m Mkt Cap as the shares doubled on announcements it’s diagnostic tests kits went into production.

Initially, Ygen are contracted to produce critical components but the agreement could soon be expanded.

In November 2019, Ygen opened its state-of-the-art facility at Citylabs, in the centre Manchester’s £95m genomics campus. This GMP (Good Manufacturing Practice) facility has un-used capacity, which would have been slowly filled by Ygen’s own growing requirements, but it is well prepared to scale-up as it anticipates ramping-up production.

The Citylabs facility is a key part of the ongoing integration of the £8.9m Elucigene acquisition which was completed in April 2019. The consolidation into a single management structure and manufacturing facility is already generating efficiencies. The four strategic priorities are product penetration, geographic and product expansion and acquisitive growth with earning enhancing deals.

One of the factors in the accelerated organic growth at the Interims was the increased product penetration for the flagship non-invasive prenatal tests (NIPT) for Down’s syndrome and other genetic disorders, and an expansion of its oncology and research services activity. The sales footprint has been expanded as it now sells products into over 60 countries worldwide, compared to 30 countries.

The US is a target for expansion and corporate activity can be anticipated. The COVID -19 tests will accelerate utilization of the new capacity and the company’s profitability.

Financials

In April 2019, an over-subscribed fund raising at 10.25p a share raised nearly £12m. After the acquisition and investment in the new facility the net cash is around £3.6m.Trading Strategy

At a near £100m market cap a moderate upgrade seems anticipated, the risk from here however seems to be missing the Covid -19 assisted upside. BuyAverage Cash ISA savers will earn just £12 in interest with UK’s 10 biggest banks

Cash ISAs continue to provide savers with disappointing savings rates as interest rates remain at record lows.

With an average amount of £5,114 saved in Cash ISAs it means the average interest from the UK’s top banks would provide interest of just £12.77, research from RateSetter found.

Data compiled by Rate Setter

*0.05% from 1 May 2020. 0.5% used in calculations.

**0.1% from 1 July 2020. 0.24% used in calculations.

Rhydian Lewis, CEO at RateSetter, said:

“Cash ISAs provide certainty on the returns they deliver – but with interest rates closing in on zero, this essentially guarantees your money will fall in value once inflation is factored in.

“However, people should not give up on the prospect of growing their money in the coming year. There are still inflation-beating ISA investment options out there which offer shelter from the turbulence of the stock market, such as the Innovative Finance ISA.”

The Innovative Finance ISA provides exposure to a range of underlying assets such as property or small business loans and typically provides much higher returns than Cash ISAs. The higher yields do of course come with a higher level of risk and aren’t suitable for all savers.

Stocks & Shares ISAs may also prove a popular alternative to Cash ISAs in 2020 as shares trades at some of the lowest levels for years, providing savers and investors with a number of bargains.

| Instant access Cash ISA rate | 1 year ISA rate | 2 year Isa rate | |

| Barclays | 0.40% | 1.00% | N/A |

| Lloyds Bank | 0.05% | N/A | 0.65% |

| Santander | 0.20% | N/A | 0.75% |

| HSBC | 0.50%* | N/A | N/A |

| Halifax | 0.05%** | N/A | 0.55% |

| TSB Bank | 0.24% | N/A | 1.05% |

| Natwest | 0.20% | 0.30% | 0.35% |

| Nationwide | 0.30% | 0.50% | 0.60% |

| RBS | 0.35% | 0.30% | 0.35% |

| Yorkshire Bank & Virgin Money | 0.50% | 1.36% | N/A |

| AVERAGE | 0.24% | 0.69% | 0.61% |

Lloyds share price sinks after it cuts dividend on advice from Bank of England

The Lloyds share price (LON:LLOY) sank on Wednesday after the UK banks announced it would be cutting its dividends with immediate effect.

Lloyds will not pay any dividends from 2019 and will cancel future payments in 2020 to conserve cash during the coronavirus crisis.

Lloyds share price

The news sent the Lloyds share price down as much as 6% in an immediate market reaction. Such news will be a body blow to Lloyd’s investors who have enjoyed a progressive dividend policy that has made Lloyds one of the most popular shares for income among retail investors. The Lloyds dividend cut came after UK banks received letters from the Bank of England’s Prudential Regulation Authority outlining advice to cut dividends as well as stopping cash bonuses for senior staff. Lloyds released the news to investors with a statement on their dividend: “In order to help us to serve the needs of businesses and households through the extraordinary challenges presented by Covid-19, the board has decided that until the end of 2020 we will undertake no quarterly or interim dividend payments, accrual of dividends, or share buybacks on ordinary shares. “In addition, in response to a request from the PRA and to preserve additional capital for use in serving our clients, the board has agreed to cancel payment of the final 2019 dividend in relation to ordinary shares. Accordingly, resolution 17 in relation to the declaration of that dividend will be withdrawn from the AGM, scheduled to take place on 21 May 2020. Our board will decide on any dividend policy and amounts at year-end 2020.” While the cut in dividends will be a blow to investors in the short-term, once the coronavirus induced economic slowdown subsides it is likely the bank will resume paying dividends. Lloyds and other UK banks are in a strong financial positions following the adoption of stringent capital ratio so whilst the economic slowdown may hinder profitability it won’t have the devastating impact the financial crisis did.UK Banks cut dividends after advice from the Bank of England’s PRA

UK Banks including Lloyds, RBS, Barclays, HSBC and Standard Chartered have cut their cut dividends after advice from the Prudential Regulation Authority (PRA).

The PRA advised banks to scrap all outstanding dividends from 2019 and suspend all further pay outs in 2020 to maintain high levels of cash through the coronavirus health crisis.

In a letter to Barclays CEO Jes Staley the Bank of England’s PRA said the “The PRA welcomes the consideration given by you and your firm to suspending dividends and buybacks on ordinary shares until the end of 2020.”

The letter also detailed instructions on how Barclays should release the news to the market which saw UK banks make an almost coordinated series of releases.

Barclays were due to pay investors £1 billion in dividends on Friday, which will now be cancelled.

In addition to cutting dividends, banks were advised not pay cash dividends to senior staff. Lloyds said in a statement: “In order to help us to serve the needs of businesses and households through the extraordinary challenges presented by Covid-19, the board has decided that until the end of 2020 we will undertake no quarterly or interim dividend payments, accrual of dividends, or share buybacks on ordinary shares. “In addition, in response to a request from the PRA and to preserve additional capital for use in serving our clients, the board has agreed to cancel payment of the final 2019 dividend in relation to ordinary shares. Accordingly, resolution 17 in relation to the declaration of that dividend will be withdrawn from the AGM, scheduled to take place on 21 May 2020. Our board will decide on any dividend policy and amounts at year-end 2020.” Shares in the UK banks were all down over 6% in early trade on Wednesday with HSBC the most heavily hit, down over 8%. HSBC managed to avoid many of the worst effects of the financial crisis and today’s cut in dividend will be a big shock to investors. Banks are set to report updates to the market at the end of April.This letter from regulator to Barclays boss, saying cancel all dividends and bonuses, would have been utterly unthinkable before 2008 banking crisis. Banks now treated precisely as they should always have been, namely as agents of state policy when the going gets tough https://t.co/5OeUDeQwTZ

— Robert Peston (@Peston) March 31, 2020

Synairgen shares surge on commencement of Coronavirus treatment trial

Shares in Synairgen (LON:SNG) jumped on Tuesday after the UK-based biotech company announced it had commenced trails for a COVID-19 treatment.

The AIM listed company had begun trials for SNG001 which is an inhaled formulation of interferon-beta-1a, a protein impacted by COVID-19.

Interferon beta is a naturally occurring protein which drives the body’s natural antiviral responses.

The trial will initially involve 100 patients in a double blind test using a placebo.

Following the announcement, shares in Synairgen rose by 11% to 69p, valuing the company at £83 million.