Asda has been sold by Walmart (NYSE: WMT) to two billionaire Blackburn-based brothers in a £6.8bn deal.

Mohsin and Zuber Issa are petrol station tycoons and backed by TDR Capital to buy the majority stake in the supermarket.

“We are very proud to be investing in Asda, an iconic British business that we have admired for many years,” said the Issa brothers in a statement.

“Asda’s customer-centric philosophy, focus on operational excellence and commitment to the communities in which it operates are the same values that we have built EG Group on,” they added.

The deal is expected to be completed early next year.

Chief executive Roger Burnley said on the deal: “This new ownership opens an exciting new chapter in Asda’s long heritage of delivering great value for UK shoppers.”

“With our combined investment, expertise and ambition; Asda, Walmart, the Issa brothers and TDR have an incredible opportunity to accelerate our existing strategy and develop an even more exciting offer for our customers as well as strengthen our business for our colleagues,” he added.

The Issa brothers have committed to £1bn investment over the next three years.

Walmart will continue an equity investment in the UK’s third-largest supermarket chain.

Judith McKenna, the chief executive officer of Walmart International, said: “I’m delighted that Walmart will retain a significant financial stake, a board seat and will continue as a strategic partner.”

Cenkos Securities shares (LON: CNKS) were trading +5.55% higher on Friday morning after the group shared interim results.

The securities group reported a pre-tax profit of £753,000 in the six months ending 30 June. This is compared to a £196,000 loss in the same period a year earlier.

Revenue at Cenkos Securities also surged by 21% to £12.9m.

The group has halved its interim dividend by 50% to 1p a share.

“The clear outcome of the 2019 general election made for an encouraging start to 2020 with an increase in asset values and the level of corporate activity. Since then the Coronavirus (“COVID‐19″) and the resulting lock down have had an unprecedented impact on economies around the world,” said chief executive, Jim Durkin in a statement.

“Our ongoing priority is the health and well‐being of our staff and I am grateful for the efforts of our IT team, who ensured an immediate and seamless switch to remote working and our HR and Facilities team for their work to make our office COVID‐secure, ready for our return.

“Swift action and our flexible operating model meant we have been fully operational throughout this time and therefore able to focus on our clients’ needs and assist them through this period. Indeed, the second quarter of 2020 saw a further increase in corporate activity, such that secondary funds raised on AIM were more than double that raised in the first quarter,” he added.

Cenkos Securities shares (LON: CNKS) are now trading +4.44% at 47.00 (1120GMT).

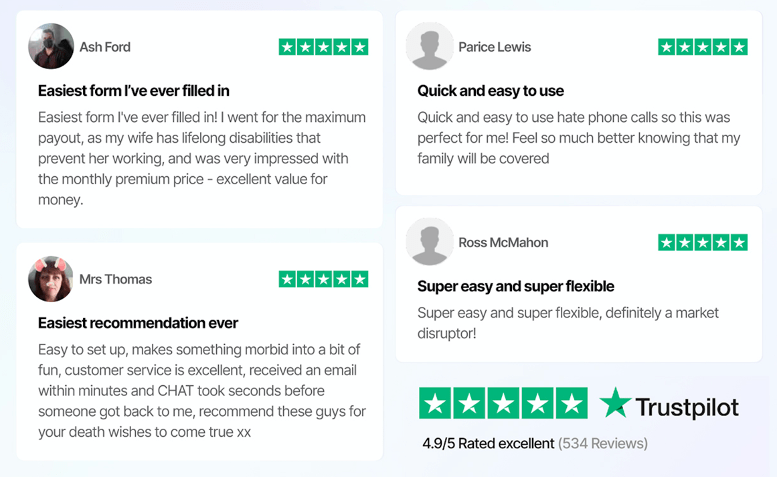

DeadHappy, a digital-first insurance provider, has surged past its £1.5M crowdfunding target on Seedrs and is now overfunding with more than £2.3M raised from over 850 investors.

As the company approaches their stretch target, the crowdfunding campaign will remain open for a limited time only, closing on 9 October 2020: Click here to invest!RIP long boring forms – hello DeadHappy

Recognised as one of the 15 exciting FinTech companies to watch in 2020, DeadHappy is on a mission to disrupt the £3.7bn life market by introducing a unique deathwish-based, pay-as-you-go life insurance product. Adopting a ‘digital-first’ approach, the company has taken a step away from the complex, expensive and boring world of traditional life insurance. Their streamlined online process – optimised for smart phones and tablets – allows customers to answer only four medical questions and obtain life insurance cover in under five minutes. The process is fast, transparent and hassle free.

Since launch, the company has insured over £1bn of cover and has had overwhelmingly positive customer feedback, with an NPS of 86 and a Trustpilot score of 4.9, from more than 500 reviews.

Life insurance to die for

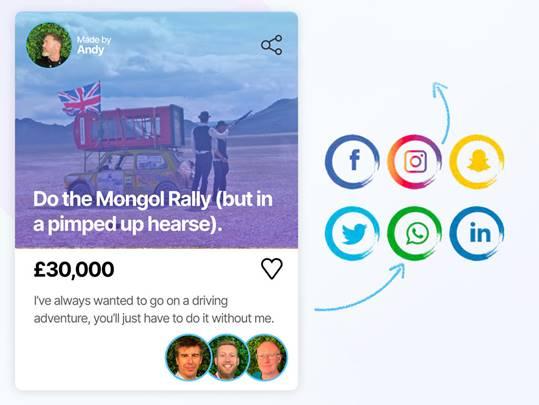

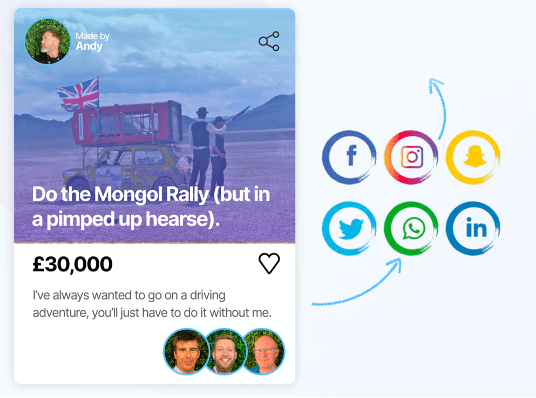

Equipped with the idea of helping people think, talk and plan for what they want to happen when they die, DeadHappy offers a life insurance product based on deathwishes. Deathwishes help customers identify their life insurance needs and gives their life insurance plan some real, tangible meaning.

“Our Deathwish platform helps customers specify how they want their insurance payout to be used, such as pay off your mortgage or send your family on holiday,” says Phil Zeidler, Co-founder of DeadHappy. “Crucially, it acts as a catalyst to thinking about what you’d like to happen when you die and helps to open up those conversations with your loved ones.”

Launched in February 2019, the company’s ‘Deathwish Platform’ has seen over 120k deathwishes created to date.

The crowdfunding round

DeadHappy’s current crowdfund follows £5.5m investment to date from notable VCs Octopus and eVentures, both of whom are reinvesting in this round.

“As we look forward to the next stage of development for this company, we’re really excited to support them on their mission to change people’s attitudes to death,” said Malcom Ferguson, partner in Octopus Ventures.“And hopefully go some way to fixing the chronic underinsurance that exists in this sector.”

Why we invested in DeadHappy – Octopus Ventures from DeadHappy on Vimeo.

DeadHappy plans to use the funds raised to continue its rapid growth through marketing investment, launch new products, and accelerate the on-boarding of partners and sponsors.

The company’s round on Seedrs is set to close on the 9thof October 2020.

Click here to invest!

After being a private company for the past nine years, Playboy has revealed plans to list on the stock market.

In a deal that is valued at $415m (£323m), the company will merge with SPAC Mountain Crest Acquisition.

Playboy has transformed its business model and now describes itself as a consumer products company, selling clothing and gaming.

The merger is expected to be completed in 2021, when the group will be listed on the Nasdaq, the US stock market index.

Playboy chief executive Ben Kohn said: “The intention was always to return the company to public markets.”

“Our mission – to create a culture where all people can pursue pleasure – is rooted in our 67-year history and creates a clear focus for our business and role we play in people’s lives, providing them with the products, services and experiences that create a lifestyle of pleasure,” Kohn said in a statement.

“We are taking this step into the public markets because the committed capital will enable us to accelerate our product development and go-to-market strategies and to more rapidly build our direct-to-consumer capabilities,” he added.

On Friday’s opening, the FTSE 100 took a slide as markets prepare for the furlough scheme to end and the US President tested positive for coronavirus.

The FTSE 100 fell 0.7% to 5,837 points. European and Asian stocks also opened lower, whilst Wall Street is also expected to open lower amid the news of Donald Trump.

Trump tweeted on Friday: “Tonight, @FLOTUS and I tested positive for COVID-19. We will begin our quarantine and recovery process immediately. We will get through this TOGETHER!”

Fiona Cincotta, a market analyst from City Index, said: “The markets are already fretting about an uncertain election and this just adds another layer of uncertainty.”

Despite reassurances from Trump, many have noted that his age could lead to more severe forms of the disease. Polling day is in a month’s time on 3 November.

Shares on London’s blue-chip index are expected to come under pressure as the furlough scheme comes to an end and one in 10 employees in the UK are expected to lose their jobs.

“The Footsie remains fettered by investor insouciance and bleak prospects for the UK economy as a whole, down 23% in the year to date and seemingly unable to break out of its current narrow band,” said Richard Hunter, who is the head of markets at Interactive Investor.

“Further countries being added to the UK quarantine list alongside targeted local lockdowns have done little to lighten the mood, with the moves piling further pressure on several already beleaguered sectors.

“Large fundraisings announced by the likes of British Airways owner International Consolidated Airlines and Rolls-Royce are further indications of travel industry in turmoil,” he added.

Ravaged by more than 8 million Covid-19 cases, and at least 328,000 reported deaths, Latin America’s virus crisis seldom makes the headlines in the UK media, yet it remains the most affected region in the world by the ongoing coronavirus pandemic.

‘The fear for many is that the region has tried to do too much, too soon’

According to the Turkish-run news broadcaster Anadolu Agency, Latin American countries make up some 28% of the 31.8 million confirmed cases globally, and almost a third of total deaths around the world. Out of the 15 countries with the highest death rate, 11 are located in Latin America or the Caribbean.

Recent forecasts from the International Monetary Fund (IMF) and the World Bank have expressed concern that Latin America and the Caribbean will suffer the most out of all the emerging-market economies worldwide in the post-pandemic recovery period.

In June, the IMF reported on the “steep” economic toll of the pandemic on Latin American countries, estimating that their cumulative economies will shrink by a record 9.4% in 2020, with only a mild +3.7% recovery next year.

Reuters reported this week that a recent projection by the Bank of America outlined a potential GDP decline of 8.2% across the region, which is worse than the predictions for the Middle East, Africa and Asia.

The two largest economies, Brazil and Mexico, have weathered their worst economic downturns since the Great Depression during the 1930s. Brazil is now facing a contraction of between 5-7%, while the Bank of Mexico released an estimate of a GDP drop between 8.8-12% for 2020.

Argentina, having been deep in a crippling depression before the pandemic hit after defaulting on its national debt for the ninth time in history, is expected to see a GDP fall of some 11% according to analysts at Citigroup bank.

So how can Latin America tackle the still-emerging economic impact of the pandemic? With widespread reports of the flouting of social distancing rules and pleas to convince the public to adopt masks in crowded places, the fear for many is that the region has tried to do too much, too soon.

Too much, too soon?

A report by the Washington Post earlier this month described the scenes on the ground in Buenos Aires – the capital city of Argentina – where “clusters of people, many without masks, were strolling and chatting” on the city’s crowded boulevards.

The country’s president, Alberto Fernández, began undoing months of strict lockdown measures in July, when he announced a return to “normal life”.

Despite initiating “one of the world’s strictest coronavirus lockdowns” early on in the year – warning citizens that “you can recover from a drop in the GDP, but you can’t recover from death” – the reception from the Argentinian public was, in some cases, worryingly apathetic.

There were frequent reports of lockdown violations, with some stores staying open during the pandemic, stating that online sales were not sufficient to keep businesses afloat.

The initial success in clamping down on Covid-19 cases quickly started to unravel, and infection rates began to soar again in the summer months.

People were reportedly “on edge” as the pandemic took on distinctly political undertones, with the Argentinian government blaming the rise in cases on lockdown breaches and opposition groups claiming that basic freedoms were being jeopardised.

Cooped-up and frustrated citizens flooded back to Buenos Aires’s streets as the lockdown came to an end. In the two months since the country reopened, Argentina has seen new coronavirus cases triple, now breaching an additional 12,000 every day.

Analysts have suggested that Latin American countries face the same challenges that we so often see in the context of right-wing conspiracy theorists in the United States, with “the same divisive individualism that has hampered a unified coronavirus response” to the pandemic across the pond.

Indeed, in Colombia there were reports of large parties attended by thousands in July, almost undoubtedly contributing to the late summer surge in cases there. A Peruvian mayor came under fire for being caught “going out, getting drunk, then playing dead in a failed attempt to avoid detection”.

Most infamous of all, travellers to Brazil have reported on swamped beaches, packed sidewalks and flagrant flouting of mask-wearing rules.

However, the sudden surge in cases is more than just a public health concern – it is also a big red warning sign that the region’s economic recovery is in peril.

Should public health officials convince governments to impose secondary regional – or even national – lockdowns, the inching progress made in recent weeks towards a healthier economy would grind to a halt, or perhaps reverse entirely.

‘There is a general sentiment that further lockdown measures could dash hopes of a return to pre-Covid economic normality in the near future’

What does the data say?

While the data on economic recovery differs across Latin American countries, there is a general sentiment that further lockdown measures could dash hopes of a return to pre-Covid economic normality in the near future.

The latest IHS Market Manufacturing Purchasing Manager’s Index (PMI) data for Brazil confirmed that the country’s manufacturing sector had been making significant strides in recovery into September, with “near-record expansions in new orders and production, alongside a return to growth of export sales”. Companies also widely “stepped up hiring and purchasing activity, with optimism towards future output also strengthening”.

In fact, the PMI rise from 64.7 in August to 64.9 in September represented “the strongest improvement in the health of the sector since data collection started in February 2006”.

Commenting on Brazil’s data, Pollyanna De Lima, Economics Associate Director at IHS Markit, emphasised that the country had been forced to overcome significant demand and supply challenges as a result of the pandemic:

“There were clear signs that operating capacities came under pressure, among manufacturers and in supply chains. For producers, this was evident from a record rise in backlogs of work, while vendors were unable to deliver purchased inputs in a timely manner. Panellists commented on COVID-19 related workforce shortages at suppliers, as well as a lack of available raw materials”.

Should Brazil’s government opt to implement another lockdown, the supply chain issues which threatened the country’s manufacturing sector during the peak of the pandemic may well rear their ugly heads once more.

33,269 new cases were recorded in Brazil this Wednesday, with an estimate of almost half a million active infections. Reuters reported that the country had seen more than 1,000 deaths in just 24 hours. Meanwhile, speculation mounts if further restrictions are imminent after Rio de Janeiro cancelled its annual Carnival parade for the first time in more than 100 years over social distancing concerns.

‘Where growth was anticipated, however, that was contingent on a gradual recovery from the coronavirus pandemic and softer restrictions domestically and externally’

Mexico’s PMI data followed along a similar line to Brazil’s, with “renewed optimism towards future output and softer contractions in new orders, input buying and employment”, and a marked improvement from 41.3 in August to a six-month high of 42.1 in September.

But, as with Brazil’s encouraging healing arc so far, De Lima warned that Mexico’s economic recovery very much hinges on “softer” measures to combat the new surge in Covid-19 cases.

“Following six months of pessimism, companies on average became optimistic that output will increase over the course of the coming 12 months. Where growth was anticipated, however, that was contingent on a gradual recovery from the coronavirus pandemic and softer restrictions domestically and externally”.

4,446 new cases were recorded in Mexico on 30 September, with some 130,000 active cases currently on health officials’ radars.

What does this mean for Latin America’s long-term future?

‘Latin American countries can seize this opportunity to address long-held socio-economic grievances’

A decade ago, the head of the Inter-American Development Bank, Luis Alberto Moreno, predicted that the 2010s would see Latin American countries finally thrive.

Just last week, however, the same man stated that the region had missed this “rare opportunity”, citing comparatively low investment in infrastructure, high prices and the “dismal” quality of public services, as well as the stagnating quality of education available to aspiring young professionals.

The coronavirus pandemic may not be solely responsible for the setback, but it has certainly jeopardised hopes that Latin America might be able to make the incoming 2020s its success story decade.

A number of countries, including even the region’s economically-strongest – Brazil and Mexico – now turn to face the next decade from a disadvantage, having suffered heavily from lockdown measures and with a full recovery not expected for years to come.

Of course, the crisis does also offer an opportunity to make some changes to ensure Latin America can indeed thrive in the future.

Reuters draws attention to the pandemic’s brutal force as “exposing deep-seated structural problems that now must be addressed with far-reaching and long-overdue reforms in education, healthcare services and the implementation of the rule of law”.

Perhaps Latin American countries can seize this opportunity to address long-held socio-economic grievances – including high poverty rates, subpar infrastructure and poor education – and help to lay the groundwork for a stronger economic resurgence in the coming years.

As with it seems everything lately, the future is all but guaranteed. That being said, Latin America faces a particularly steep uphill battle towards economic recovery.

While it may be tempting to see this as a burden, there is some merit in the view that the coronavirus pandemic could shake up the status quo to the point that the poverty, inequality, and economic instability which have plagued the region since the end of the colonial era can finally start to be undone, and Latin America’s cumulative economies could get a long-awaited chance to shine.

Thanks to fairly positive PMI data, the Dow Jones broke the 28k point mark for the second time in September and only the third time since the Covid pandemic took full force.

The 28k has been something of a blue-skies benchmark ever since the Dow first hit it last November, but its ability to sustain this level (as it did during the August-September transition) is doubtful.

Already surrendering half of its 1% opening gains, the Dow Jones is now sitting on a 0.42% rally, at 27,897 points.

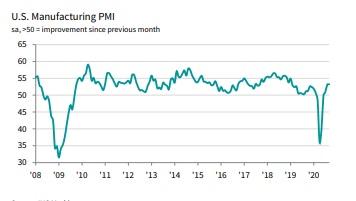

This followed largely positive PMI data, with September manufacturing indicating what IHS Markit (NYSE:INFO) described as “the sharpest improvement in operating conditions across the U.S.

manufacturing sector since early-2019”.

Overall, IHS said growth was supported by production output posting a quick increase at the end of the third quarter, with the rate of growth at its sharpest rate for ten months. A positive upshot of this was the upward pressure on capacity, which forced manufacturers to expand their workforce – leading to the second-sharpest rise in employment since November 2019.

IHS Markit graphic and US PMI data

According to the IHS survey, US manufacturing PMI stood at 53.2 in September, up marginally from 53.1 in August but down on the earlier flash reading of 53.5.

Speaking on some of the risk factors facing US manufacturers, IHS Chief Business Economist, Chris Williamson, stated:

“But it was not all good news. Supply shortages worsened as companies increasingly struggled to source enough inputs to meet production requirements. With demand often exceeding supply, prices rose sharply again across many types of inputs, especially metals.”

“Growth of new orders for consumer goods also waned during the month, hinting at some cooling of demand from households, commonly blamed on Covid-19. Overall order book inflows consequently slowed compared to August.”

“The outlook also darkened, as companies grew more concerned about the sustained economic disruption from the pandemic alongside uncertainty caused by the upcoming presidential election. The sector therefore looks to be entering the fourth quarter on a slower growth trajectory, adding to signs that fourth quarter GDP growth will wane considerably from the third quarter rebound.”

Looking ahead at the future of the Dow Jones, and much like the business confidence indicator within PMI data, a lot will be determined by the outcome of the US presidential election. For now, though, neither the Dow nor business confidence benefit from the uncertainty and political hostility we are currently seeing over the pond.

While a popular, burgeoning sector for tackling carbon emissions, renewable energy has had to continue innovating in order to allay critics’ doubts. First, there was the issue of inconsistent energy supply, which is being tackled by grid-scale storage systems. Second, is the major gripe with electric vehicle engine components. Harmful to produce, and harmful to dispose of, the recent investment by Low Carbon Innovation Fund 2 represents a step towards in these issues becoming a thing of the past.

On Thursday, energy-specialised merchant bank, Turquoise, announced that the Low Carbon Innovation Fund 2 had completed its third deal, investing £350,000 in battery specialists, Connected Energy.

Connected Energy specialises in reusing the batteries of electric vehicles, which typically become redundant after their capacity falls by just 25%. What they do is take these out-of-commission batteries and repurpose them as components of a grid-scale energy storage system, which are needed to smooth fluctuations both in demand by energy users, and in supply by wind and solar farms.

Connected Energy systems currently range from a 300kW behind the meter system, to a 12MW system currently in development, and modular multiples of those.

Speaking on Low Carbon Innovation Fund 2‘s investment in the electric vehicle battery repurposing company, Turquoise Managing Director, Ali Naini, commented:

“Connected Energy helps reduce emissions in a number of innovative ways, such as reducing the cost of electric vehicles by increasing the value of their used batteries, reusing valuable materials in those batteries, and creating energy storage systems that help with the wider adoption of renewable energy. They also have many of the attributes necessary for creating strong investor returns. This makes the company a perfect fit to the remit of LCIF2.”

Given that the Low Carbon Innovation Fund 2 has the UK Ministry of Housing, Communities and Local Government as its Managing Authority, Connected Energy CEO, Matthew Lumsden, says he is excited to strengthen his company’s links with local and national government.

Renewi shares (LON: RWI) soared 18% on Thursday afternoon.

According to the Buckinghamshire-based company, trading between 1 April to 30 September was “materially ahead” of expectations.

“Given the resilience of the group’s trading in the first half, which included a period of extensive lockdown measures in the first quarter, the board now anticipates a performance for the year ending 31 March 2021 which is materially ahead of its previous Covid-19 adjusted expectations,” said the group in a statement released on Thursday.

Whilst the share price surged by 18% on Thursday to 22,90, the price of shares has fallen by 37% this year to date.

“The Board remains suitably cautious about the macroeconomic outlook, including any potential future slowdown in the later-cycle Dutch construction market and potential further measures to contain Covid-19,” said the group on future trading.

“However, given the resilience of the Group’s trading in the first half, which included a period of extensive lockdown measures in the first quarter, the Board now anticipates a performance for the year ending 31 March 2021, which is materially ahead of its previous Covid-19 adjusted expectations.”

“Longer term, whilst the speed and extent of economic recovery will influence our performance, waste volumes have historically been resilient through cycles and the transition to increased recycling will continue to support our business model. The sustainability agenda and the potential for a “green recovery” supported by the EU and national governments are expected to present attractive opportunities for Renewi to convert waste into a wider range of high-quality secondary materials. We remain confident our three strategic growth initiatives will deliver significant additional earnings over the next three years and beyond.”

Renewi shares (LON: RWI) are currently trading +19.72% at 23,25 (1545GMT).

Likely to be a crucial day of results and potentially influential on global equities, the Australian, European, and Asian economies posted their manufacturing PMI data on Thursday, and September’s results displayed various degrees of success across some of Asia fastest-growing economies

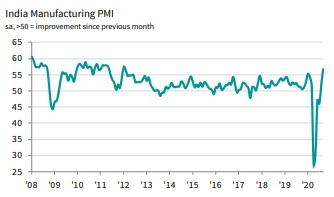

India manufacturing moves up a gear

Continuing the boom it began in August, India’s manufacturing sector enjoyed an orders and production renaissance, pushing its PMI to its highest mark since January 2012.

With renewed expansions in export sales and input stocks, and improved business confidence, output rose for the first time in six months, reflecting an uptick in input costs.

IHS Markit (NYSE:INFO) stated that India’s PMI increased from an already-positive levl of 52.0 in August, to 56.8 in September, signalling not just back-to-back growth but its highest reading for more than eight-and-a-half years.

IHS Markit graphic and India PMI data

With reports of loosened Covid restrictions and recovery in demand, Indian manufacturers lifted output by around 30 points in a matter of months – the third quickest recovery in the history of IHS’ surveys.

Speaking on the data, IHS Markit Economics Associate Director, Pollyanna De Lima, added:

“Exports also bounced back, following six successive months of contraction, while inputs were purchased at a sharper rate and business confidence strengthened.”

“One area that lagged behind, however, was employment. Some companies reported difficulties in hiring workers, while others suggested that staff numbers had been kept to a minimum amid efforts to observe social distancing guidelines.”

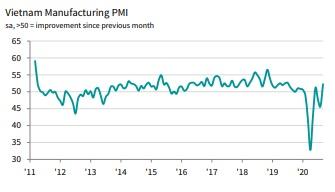

Vietnam PMI bounces back to green

On a more modest but similar trajectory is Vietnam, whose manufacturing PMI returned to growth in September as Covid concerns somewhat eased. With this, output and new orders regained their footing, while business confidence grew and the rate of job cuts slowed down.

This saw the manufacturing PMI of Asia’s fifth-fastest-growing economy recover from the negative level (sub-50) of 45.7 points in August, and back into the green, at 52.2 points for September.

IHS Markit graphic and Vietnam PMI data

This latest reading marks the first upturn in business conditions for three months, and the most notable improvement since July 2019, according to IHS.

Anecdotal evidence also suggests that control over the pandemic has been a key factor in supporting a recovery in operating conditions, as increasing case numbers had been seen in the previous survey period.

With the recent reduction in cases, client demand increased, leading to a ‘solid’ increase in new orders. Alongside this growth, production expansion was also registered, along with new business from abroad increasing for the first time since January.

Speaking on the positive impact of controlling the virus, IHS Economics Director, Andrew Harker, commented:

“After a rise in COVID-19 cases in late-July and early August briefly threw the sector’s recovery off track in August, the September PMI results were much more positive.”

“With control of the pandemic regained, firms saw an influx of new orders, ramped up production and were at their most optimistic for over a year. As ever though, sustaining these positive trends is dependent on virus cases not picking up again.”

Philippines regains stability

On a more tentative note, Filipino data indicated that operating conditions for manufacturers had returned to something broadly resembling stability.

While at a marginal pace, new orders rose for the first time since February – led by improving customer demand as more part s of the country’s economy reopened due to the easing of Covid restrictions. Similarly, business sentiment improved to its highest point since February, with upbeat forecasts attributed to hopes of rising demand and Covid becoming a thing of the past in the not-too-distant future.

Meanwhile, output fell to its weakest level in three months, though this, also, was only a marginal change. However, unemployment continues to expand at a notable rate, which manufacturers often link to non-replacement of voluntary leavers and sufficient capacity. Further, cost burdens rose as shortages led to higher prices, and respondents only partially passing on higher costs to clients, due to market pressures forcing them to keep prices competitive.

Following a downturn, with 47.3 points in August, September saw a very slight return to positivity, with Philippines manufacturing PMI rising to 50.1. This latest reading represents extremely modest expansion, and its the highest since conditions were last stable in the goods producing sector, back in February.

IHS Markit graphic and Philippines PMI data

Talking on potential improvements in operating conditions, IHS Economist, Shreeya Patel, commented:

“According to firms, the ongoing restrictions related to the COVID-19 pandemic continued to limit the performance of the sector, with some businesses forced to pare back operations.”

“On a more hopeful note, stronger business sentiment and efforts to rebuild stocks suggest panellists are preparing for an improvement in demand over the coming months, although optimism continues to rest on the development of the pandemic.”

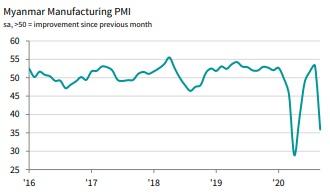

Myanmar hampered by a surge in Covid cases

Unfortunately unable to gain traction away from Covid was Asia’s sixth-fastest-growing economy, Myanmar, whose manufacturing PMI suffered as performance indicators were scuppered by a resurgence in new cases.

With factories temporarily closing to combat the spread of the virus in September, both output and new orders ‘declined rapidly’ according to IHS Markit. Alongside these considerations, a deterioration in business conditions, and contraction in workforce numbers, both saw the July-August recovery stopped in its tracks.

As stated by IHS, Myanmar manufacturing PMI fell from a 15-month-high in August, at 53.2 points, to 35.9 in September – representing a notable contraction.

IHS Markit graphic and Myanmar PMI data

This new figure is the second-lowest recorded in the country since the IHS survey began in December 2015, and only above April’s score of 29.0, when the virus was at its peak. Further, the month-on-month decrease of 17.3 points is actually the largest on record, and even more severe than the previous record of 16.3, witnessed between March and April.

According to IHS, four out of five of the PMI indicators had negative trajectories in September, with the exception being suppliers’ delivery times. Output and orders declined at their second fastest rate since the group’s surveying commenced, with these indices both recording month-on-month declines of over 28 points.

Speaking on a bleak month for Myanmar manufacturing, IHS Economics Director, Trevor Balchin, stated:

“The impact has so far been less severe than the record deterioration in business conditions seen in April. But the month-on-month decline in the PMI was the largest on record as it collapsed by over 17 points from August’s 15-month high of 53.2 to 35.9.”

“With a two-week lockdown introduced in Yangon towards the end of September, the trajectory in cases over the coming weeks will be crucial as authorities judge when to ease the new restrictions and enable the manufacturing sector to resume its recovery. The October PMI will provide the first signs of any rebound in activity, or indeed further retrenchment.”

Life insurance to die for

Equipped with the idea of helping people think, talk and plan for what they want to happen when they die, DeadHappy offers a life insurance product based on deathwishes. Deathwishes help customers identify their life insurance needs and gives their life insurance plan some real, tangible meaning.

“Our Deathwish platform helps customers specify how they want their insurance payout to be used, such as pay off your mortgage or send your family on holiday,” says Phil Zeidler, Co-founder of DeadHappy. “Crucially, it acts as a catalyst to thinking about what you’d like to happen when you die and helps to open up those conversations with your loved ones.”

Launched in February 2019, the company’s ‘Deathwish Platform’ has seen over 120k deathwishes created to date.

Life insurance to die for

Equipped with the idea of helping people think, talk and plan for what they want to happen when they die, DeadHappy offers a life insurance product based on deathwishes. Deathwishes help customers identify their life insurance needs and gives their life insurance plan some real, tangible meaning.

“Our Deathwish platform helps customers specify how they want their insurance payout to be used, such as pay off your mortgage or send your family on holiday,” says Phil Zeidler, Co-founder of DeadHappy. “Crucially, it acts as a catalyst to thinking about what you’d like to happen when you die and helps to open up those conversations with your loved ones.”

Launched in February 2019, the company’s ‘Deathwish Platform’ has seen over 120k deathwishes created to date.

Life insurance to die for

Equipped with the idea of helping people think, talk and plan for what they want to happen when they die, DeadHappy offers a life insurance product based on deathwishes. Deathwishes help customers identify their life insurance needs and gives their life insurance plan some real, tangible meaning.

“Our Deathwish platform helps customers specify how they want their insurance payout to be used, such as pay off your mortgage or send your family on holiday,” says Phil Zeidler, Co-founder of DeadHappy. “Crucially, it acts as a catalyst to thinking about what you’d like to happen when you die and helps to open up those conversations with your loved ones.”

Launched in February 2019, the company’s ‘Deathwish Platform’ has seen over 120k deathwishes created to date.

Life insurance to die for

Equipped with the idea of helping people think, talk and plan for what they want to happen when they die, DeadHappy offers a life insurance product based on deathwishes. Deathwishes help customers identify their life insurance needs and gives their life insurance plan some real, tangible meaning.

“Our Deathwish platform helps customers specify how they want their insurance payout to be used, such as pay off your mortgage or send your family on holiday,” says Phil Zeidler, Co-founder of DeadHappy. “Crucially, it acts as a catalyst to thinking about what you’d like to happen when you die and helps to open up those conversations with your loved ones.”

Launched in February 2019, the company’s ‘Deathwish Platform’ has seen over 120k deathwishes created to date.

The crowdfunding round

DeadHappy’s current crowdfund follows £5.5m investment to date from notable VCs Octopus and eVentures, both of whom are reinvesting in this round.

“As we look forward to the next stage of development for this company, we’re really excited to support them on their mission to change people’s attitudes to death,” said Malcom Ferguson, partner in Octopus Ventures.“And hopefully go some way to fixing the chronic underinsurance that exists in this sector.”

Why we invested in DeadHappy – Octopus Ventures from DeadHappy on Vimeo.

DeadHappy plans to use the funds raised to continue its rapid growth through marketing investment, launch new products, and accelerate the on-boarding of partners and sponsors.

The company’s round on Seedrs is set to close on the 9thof October 2020.

Click here to invest!

The crowdfunding round

DeadHappy’s current crowdfund follows £5.5m investment to date from notable VCs Octopus and eVentures, both of whom are reinvesting in this round.

“As we look forward to the next stage of development for this company, we’re really excited to support them on their mission to change people’s attitudes to death,” said Malcom Ferguson, partner in Octopus Ventures.“And hopefully go some way to fixing the chronic underinsurance that exists in this sector.”

Why we invested in DeadHappy – Octopus Ventures from DeadHappy on Vimeo.

DeadHappy plans to use the funds raised to continue its rapid growth through marketing investment, launch new products, and accelerate the on-boarding of partners and sponsors.

The company’s round on Seedrs is set to close on the 9thof October 2020.

Click here to invest!

{kind=link}