Justin Urquhart-Stewart – Investing through COVID-19, US/China tensions and the demands of ESG

Protesters tell Bank of England to back up its Green Recovery promises

Protesters amassed on Threatneedle Street as the Bank of England announced its decision on QE and interest rates, as well as its Financial Stability Report. Many were seen holding Andrew Bailey masks and speech bubbles with the Governor’s statements about the need to decarbonise and seize the opportunity for a green economic recovery. While others called on Bailey to, “put your money where your mouth is”, with others reminding the bank of its environmental report, which stated that economic stability could not exist without climate and environmental stability.

However, despite the protests, the latest Bank of England FSR made no reference to climate risks, other than to say that it would be delaying its climate stress tests until 2021.

What has been done wrong?

Despite pledging to support the ‘Build Back Better‘ initiative, research posted by Positive Money indicates that the majority of the bank’s financial support is currently going towards high-pollution sectors, who also feature some of the biggest companies laying off high numbers of staff.

Research from the New Economics Foundation also noted that £11.4 billion of the Bank of England’s QE programme had gone towards high-carbon companies, while research form Positive Money indicated that more than 56% of the bank’s Covid Corporate Financing Facility had gone towards bailouts for airlines, and oil, gas and chemical companies.

Rachel Oliver, head of campaigns and organising at Positive Money, said:

“Andrew Bailey understands that environmental breakdown poses an existential threat to economic and financial stability, but he is failing to put his money where his mouth is. It is hugely disappointing that the Bank of England is putting climate on the backburner when it has such a huge opportunity to do something about it.”

“Not only is the Bank of England failing to protect people and planet, it’s also putting corporate elites ahead of the rest of us, giving billions of pounds of no-strings-attached bailouts to firms which have splashed out on dividends while slashing tens of thousands of jobs.”

“If the government truly wants to ‘build back better’, it needs to make sure all of the powerful tools at our central bank’s disposal are geared towards supporting a fairer and greener recovery. Doing so is the only way to make sure the coronavirus crisis isn’t followed by an even bigger climate crisis.”

What can the Bank of England do better?

Campaigners are calling for the bank to attach social and environmental conditions to its corporate bailouts, in order to combat both unemployment and environmental degradation.

According to a YouGov survey commissioned by Positive Money in July, some two thirds of the public supported socially and environmentally conditional financial bailouts.

Perhaps what could have been done is, alongside pledges to retain jobs, companies could have incentivised via a ‘negative’ payback initiative. Whereby, they would pay back more or less money to the Bank of England, on the basis of how much of their operations become decarbonised in the next five years – for instance, the relative scale and commitment BP puts into its renewables push – with the worst performers paying back what is owed, plus interest, and potentially even an additional levy.

In addition, there needs to be a greater push to increase company’s financial responsibility and self-reliance. While maximising profit is an understandable goal, there needs to be greater consideration for posterity. Much as individuals have had to supplement government support with their own savings, the far more able multinational companies ought to be to carry their own weight during an economic downturn, and this is certainly achievable if they assign a portion of their earnings every year into an internal crisis fund for rainy days. Such policies, I believe, should be mandatory, and another conditionality for receiving government support. Alas, the Bank of England reneging on its promises, and today’s protests, are a reminder of what can only be seen as a – thus far – missed opportunity, and the bank needs to do better if and when another round of financial support is called for.

ITV cancels its dividend as earnings half and ad revenue takes ‘severe’ hit

These drops were led by the company pausing the majority of its production activities in mid-March, which resulted in a 17% decline in ITV Studios revenues during the first half, down to £630 million.

Similarly, total Broadcast revenue was down 17% to £824 million, while total external revenue dropped 17% to £1.22 billion during the half year.

The real kicker for the company, however, was what it described as its ‘most severe’ decline in demand for advertising across its categories, with total advertising revenues plummeting 43% in Q1 and 21% in Q2. The situation was equally bleak for ITV shareholders, with the company stating that in light of economic uncertainty, the Board of the company had decided to cancel its interim dividend to conserve cash. Further, and with another hit to shareholders’ dividend cover, adjusted and statutory EPS dropped by 53% and 90%, to 2.9p and 0.5p respectively.With a glimmer of positivity, teh company reported that total viewing had increased by 4%, with ITV Family light viewing up 8% and online streaming up 13%.

This positive news is somewhat offset, however, when we consider that the latter figure refers to a wider trend in online viewing, which is by-and-large a threat to ITV’s long-term viewership. Further, the company noted that Family share of viewing was down 4% during the first half, to 22.6%, due to the BBC’s high news output helping it to gain viewership during the period of uncertainty.

ITV response

Commenting on what she described as ‘one of the most challenging times in the history of ITV’, Chief Executive, Carolyn McCall, said:

“While our two main sources of revenue – production and advertising – were down significantly in the first half of the year and the outlook remains uncertain, today we are seeing an upward trajectory with productions restarting and advertisers returning to take advantage of our highly effective mass reach and addressable advertising platform, in a brand safe environment.”

“We have made good progress in our digital transformation. The majority of our colleagues are working seamlessly at home thanks to the investment we have made in technology and systems and this has helped us continue to deliver on our strategic objectives. The success of the Hub investment plan contributed to driving online viewing up 13% and monthly active users up 15% in H1. We continue to successfully roll out Planet V with around 35% of our VOD inventory now delivered through this platform, which is on track to be live with most of the major agencies by the end of the year. BritBox is ahead of target on subscribers in the UK and we have announced plans to roll out BritBox internationally.”

“The future is still uncertain due to the pandemic but the action we have taken to manage and mitigate the impact of COVID-19 puts us in a good position to continue to invest in our strategy of transforming ITV into a digitally led media and entertainment company.”

Investor note

After dropping following today’s update, ITV shares have since recovered, now up 0.67% or 0.41p, to 61.31p per share 06/08/20 13:10 BST. This is far below its median 12 month target of 92.50p set by 16 analysts, and represents a 42.76% year-on-year drop.Mondi shares rally on ‘resilient’ performance amid COVID challenges

Mondi response

Commenting on the results, and taking note of both the group’s resilience during COVID trading, as well as its ability to reinstate its dividend, CEO Andrew King said: “Sustainable packaging continues to be a long-term priority for our customers and wider society. As a leading producer of both paper and flexible plastic-based packaging, we are in a unique position to support our customers’ environmental goals with packaging that is sustainable by design adhering to our principle of paper where possible, plastic when useful.” […] “Going into the second half of 2020, heightened macro-economic uncertainties remain. Pricing across our key pulp and paper grades is below or in line with the average of the first half. Demand for packaging daily essentials remains robust while we continue to see weakness in certain industrial end-uses. Uncoated fine paper order books have picked up from the lows seen in the second quarter, albeit we do not expect a near-term recovery to pre-pandemic levels. We have rescheduled planned mill maintenance shuts which will have an impact on the second half of the year.” “We are confident that the Group will continue to demonstrate its resilience in the event of a prolonged macro-economic downturn, while remaining well-positioned when the recovery takes place. This is underpinned by the Group’s integrated high-quality, cost-advantaged asset base, culture of continuous improvement, portfolio of sustainable packaging solutions and the strategic flexibility offered by our strong cash generation and financial position.”Investor insights

Following the news, the Mondi shares rallied 1.65% or 23.50p, to 1,448.50p per share 06/08/20 12:28 BST. This is comfortably below its consensus 12-month target price of 1657.10, set by 13 analysts, with today’s price also representing a 6.66% year-on-year dip. The company’s p/e ratio is 9.21, its dividend yield currently stands at 1.71%.Virgin Atlantic files for bankruptcy protection, warns it is running out of money

WH Smith prepares to cut 1,500 jobs as sales dive due to pandemic

Gold price hits $2,000 but might still be worth investing in

Gold price risk factors

A key pressure with either downward or upward pressure is the US NFP data release, which, if it confirms another reading, could strengthen the dollar and put downward pressure on gold. However, despite seemingly manageable initial unemployment data, US jobless claims indicate that the country are sauntering off of the recovery track, and without swift action by the Fed, this could strengthen gold-buying activity. Also, any Fed assistance would likely come in the form of lowering its interest rates or extending its asset-buying programme, both of which would likely stimulate gold prices. Further, and despite some initial signs of recovery, we can always rely on the political newsreel to rock the boat. As stated by Chief Currency Analyst at HYCM, Giles Coghlan: “Stock markets may be making modest daily gains but the chance of a second outbreak of cases, which seems to be increasingly likely, could result in these gains being lost. What’s more, we shouldn’t forget that there are some big-ticket events on the table for the rest of 2020, including the US Presidential election, Brexit and the ongoing US-China trade war. These will all have significant implications on the financial markets depending on how they play out. As a result, investors are taking a conservative approach by reducing their risk exposure.”How should we approach gold?

Naturally, gold is a game of volatility. If sentiment indicates uneasiness and uncertainty, then gold tends to flourish. The key takeaway about how markets are affected by pandemics – more so than by orthodox economic downturns – is that they’re entirely shaken by the fact that they can’t control a virus. Not only are pandemic responses largely at the behest (or mercy) of political figureheads and the services they commission, but the potential -as we’ve seen – for illnesses to resurge and take a second pass at societies and markets, gives them both long-lasting potential, and the ability to truly spook investors. If you’re feeling unsure about the exact nature of market sentiment, or sentiment in the US market, it might be worth looking towards the Chicago Board Options Exchange’s CBOE Volatility Index, which offers real-time market expectations of volatility based on S&P 500 options.Does the BP share price offer better value than Shell?

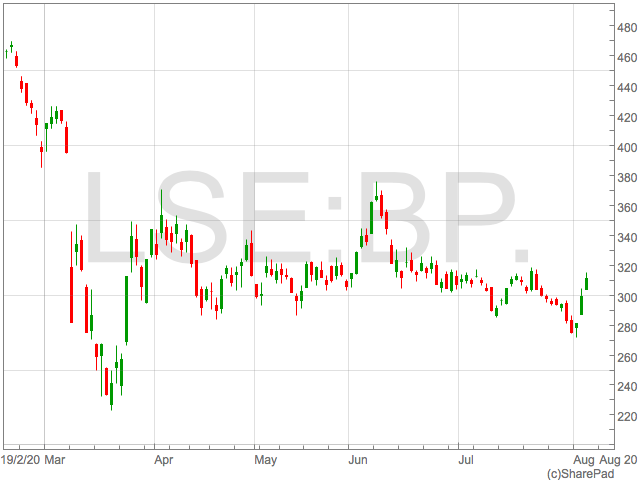

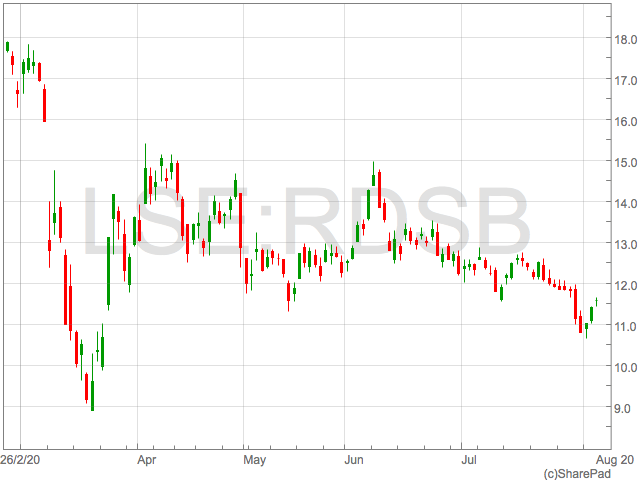

BP share price

By first looking at the the BP share price in absolute terms, it is evident that BP has outperformed Shell in 2020 with BP shares down 34% year-to-date and Shell losing 46% of it’s value. Having trading mostly inline with each other, a deviation in the two companies became pronounced as the two companies announced their second quarter earnings. This deviation was largely noticeable in the performance of the shares on the respective days of their announcements, providing a gauge of investor sentiment to the underlying performance of the businesses. BP shares rallied some 4%, whilst Shell sank around 6% on the day of their announcements. The rally in BP shares took place despite a cut in their dividend, suggesting the market had largely priced in a reduction in payouts and were more concerned with the underlying profitability and management of the companies.

Second Quarter Losses

Both companies reported historic drops in profitability. BP reported a $6.7 billion adjusted loss in the second quarter compared with a $2.8 billion profit in the same period a year prior. Shell, on the other hand, produced an adjusted profit of $600 million, down from $3.5 billion a year ago With BP swinging to huge loss but still able to stage a rally, the reaction in the share prices following the releases should be attributed to analyst estimates going into results. The reaction in BP’s share price reflects the significant beat of a loss of $8.45 billion, predicted by analysts polled by Bloomberg whilst Shell beat by a much smaller margin.Dividends

As BP released the dramatic loss, they took the historic decision to slash their dividend in half by cutting it from 10.5 cents to 5.25 cents. With GBP/USD exchange rates currently at 1.309, this equates to 4.01p meaning if this level of dividend is maintained, investors can expect an annual yield of 5% from a BP share price of 314p. Shell took the decision to cut their dividend in the prior quarter, slashing the dividend by two thirds to 16 cent. This was maintained in the second quarter and with Shell trading at 1,158p, investors in Shell will be receiving a yield of 4.2%. Based purely the income from the two shares, BP would seem more attractive to income seekers with their higher yield, but this approach is too simplistic to fully evaluate the relative value of each company’s equity. It must be noted the earnings coverage of these dividend is non existent in the case of BP and negligible in the case of Shell so attention must be paid to the cash position of each company.Cash

BP’s cash position has actually improved based from the end of 2019 as the company tapped the bond market for cash to the tune of $11 billion. The bond issue, coupled with $25 billion of impairments and writes offs, helped offset BP’s whopping $20 billion pretax loss meaning BP’s cash rose to $34.6 billion from $18 billion in the first quarter. With dividend payments reducing, this amount of cash would seem sufficient to support dividends and provide resources for their shift strategy towards a low carbon energy producer. However, the $20 billion pretax loss should be a concern for investors as a similar drain in the coming quarters would put the cash position under pressure. This is highlighted by BP’s lack of Free Cash Flow. Measured by deducting investing cash from operational cash flow, BP’s Free Cash Flow amounts to a $272 million deficit. Shell, conversely, produced Free Cash Flow of $12 billion, suggesting Shell has greater scope to invest in the next chapter of their shift towards greener fuels and the next big growth area for energy companies. Shift To Renewables

Shift To Renewables

With the destruction of oil demand and associated fall in oil prices, the focus on renewables has increased for both BP and Shell.

Both companies have strategies to increase the proportion of clean power they produce, and when assessing the relative value of each over the long term, this must be central to any valuation thesis.

However, with revenue from renewables limited in both companies, the judgement of their low carbon activities falls to natural gas.

In this respect, Shell has a far larger exposure to natural gas and would be judged to be ahead of BP in becoming a greener energy producer.

Summary

With the absence of any meaningful multiples based on earnings in the first half of 2020, the assessment of value falls to cash and ability to shift towards the demands of government targets on emissions. In both of these respects we would feel Shell has the edge over BP, despite BP providing investors with a higher yield.Segro boosts its dividend by 10% despite profit plunge

It added that it could see potential rent of £22 million from development completions, 64% of which have been leased by 30 June. It continued, saying that rents agreed in reviews and renewals were on average 10.4% higher than previous passing rents, while vacancy rates had increased but ‘remains low’ at 5.2%, and customer retention ‘remains high’ at 88%.

Segro response

After speaking on the company’s resilient performance during lockdown, company Chief Executive, David Sleath, discussed the consumer shift to e-commerce, and how this has fortified demand for efficient logistical spaces and supply chains:“The impacts of the pandemic are accelerating the adoption of technology, particularly e-commerce, across society and have resulted in a renewed focus by many occupiers on the critical importance of efficient, resilient logistics supply chains. These factors play to the quality of our portfolio and should continue to support and enhance occupier and investor demand for our prime warehouses, both in the UK and, increasingly, on the Continent.”

“Our existing portfolio has performed well and our development programme has expanded, with a pipeline of additional near-term pre-let projects which is approximately twice the size of a year ago. This, combined with our well-located land bank, means we are in a strong position to make further progress in the second half of the year and beyond.”

Investor insights

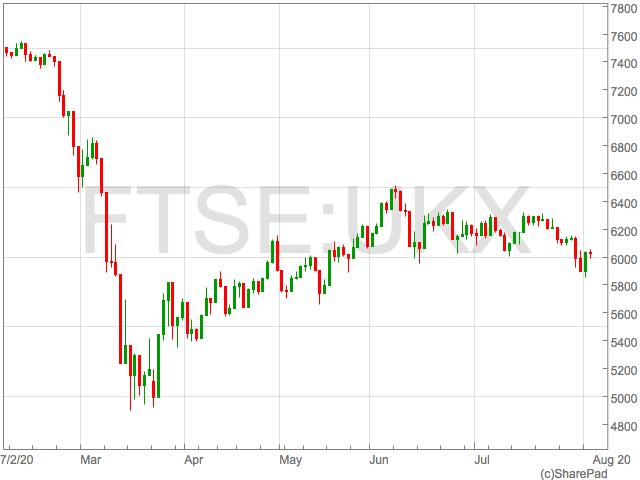

Following the news and a relatively bright outlook, Segro shares rallied 3.22% or 31.00p during trading on Wednesday, up to 994.20p per share 12:50 GMT. This is above the company’s 12-month median target price provided by 19 analysts, which stands at 910.00p a share, and represents a 35.35% jump year-on-year for the same day. The company’s p/e ratio is 12.15, its dividend yield stands at 2.08%.FTSE 100 held steady by BP and travel optimism

BP shares were up in excess of 6% in mid afternoon trade on Tuesday.

Diageo was the FTSE 100’s biggest faller as the drinks giant counted the costs of coronavirus and the impact on sales. Diageo’s full year sales were down 8.7% as coronavirus offset strength in the first half.

“Fiscal 20 was a year of two halves: after good, consistent performance in the first half of fiscal 20, the outbreak of Covid-19 presented significant challenges for our business, impacting the full year performance,” said Ivan Menezes, Chief Executive of Diageo.

Diageo shares were 5.5% weaker in the wake of the news.

IAG was higher amid optimism surrounding demand for travel on the back of an upbeat update from easyJet.

“European airlines are on the rise after easyJet saw better-than-expected summer demand,” said Joshua Mahony, Senior Market Analyst at IG.

“Airlines are soaring in early trade today, with easyJet bringing a rare bit of good news after seeing stronger-than-expected demand despite the pandemic.”

Shares in easyJet were up over 9% whilst IAG was 4% higher. easyJet are no longer in the FTSE 100 having slipped to the mid cap index in the last reshuffle.

“With the airline expecting to run flights at 40% of capacity, we are seeing a clear sign that many people are confident enough to travel despite the Covid risks that have held some back,” Mahony continued.

“With the airlines likely to see better-than-expected revenues after improved demand, the subsequent alleviation of pressure on their finances should lessen the need for further funding going forward.”

IAG have recently announced plans for a €2.75 billion rights issue to help them through the COVID-19 crisis.

BP shares were up in excess of 6% in mid afternoon trade on Tuesday.

Diageo was the FTSE 100’s biggest faller as the drinks giant counted the costs of coronavirus and the impact on sales. Diageo’s full year sales were down 8.7% as coronavirus offset strength in the first half.

“Fiscal 20 was a year of two halves: after good, consistent performance in the first half of fiscal 20, the outbreak of Covid-19 presented significant challenges for our business, impacting the full year performance,” said Ivan Menezes, Chief Executive of Diageo.

Diageo shares were 5.5% weaker in the wake of the news.

IAG was higher amid optimism surrounding demand for travel on the back of an upbeat update from easyJet.

“European airlines are on the rise after easyJet saw better-than-expected summer demand,” said Joshua Mahony, Senior Market Analyst at IG.

“Airlines are soaring in early trade today, with easyJet bringing a rare bit of good news after seeing stronger-than-expected demand despite the pandemic.”

Shares in easyJet were up over 9% whilst IAG was 4% higher. easyJet are no longer in the FTSE 100 having slipped to the mid cap index in the last reshuffle.

“With the airline expecting to run flights at 40% of capacity, we are seeing a clear sign that many people are confident enough to travel despite the Covid risks that have held some back,” Mahony continued.

“With the airlines likely to see better-than-expected revenues after improved demand, the subsequent alleviation of pressure on their finances should lessen the need for further funding going forward.”

IAG have recently announced plans for a €2.75 billion rights issue to help them through the COVID-19 crisis.