Before the impact of the £2.1bn provision, Barclays £3bn profit represents a strong increase on last year and will stoke investor optimism Barclays were in good shape going into the crisis.

“An event like the COVID-19 pandemic makes everyone focus on what’s really important right now. For us, that means running the bank safely and soundly, helping our customers and clients through the difficulties they face, supporting the UK economy and the communities where we live and work, and taking care of our colleagues around the world,” said Jess Staley in a statement included in the update.

Jess Staley continued to outline the impact government schemes such as CBILs had on Barclay’s ability to make loans to UK businesses.

“We welcome the government and Bank of England’s business support programmes and have introduced additional measures to back UK companies ourselves. They are now having a real impact. As at 24 April 2020 we have facilitated significant commercial paper issuance though the Covid Corporate Financing Facility, lent £737m in Coronavirus Business Interruption Loans, approved over 238,000 mortgage and loan payment holidays, and over 6 million customers and clients are currently paying no personal overdraft or business banking charges. We have launched a community aid package; through which we are donating £100m to support those who are being hardest hit by COVID-19. We expect that all of these measures will help to limit the economic and social impact of the pandemic.”

The Barclays CEO highlighted the impact of COVID-19 on the bank’s earning which would have been £3bn if they were not to set aside £2.1bn in provisions for bad loans due to the COVID-19 crisis.

“The impact of COVID-19 came late in what was until that point a good quarter. Statutory profit before tax was £0.9bn and profit before tax excluding credit impairment charges was £3.0bn. We have taken a £2.1bn credit impairment charge which reflects our initial estimates of the impact of the COVID-19 pandemic.”

“The strength of Barclays lies in our diversification by business, geography and currency, which allows us to remain resilient through the developing economic downturn.”

Touching on the letter from the Bank of England which instructed banks to cut their dividends, Staley provided a rough timeline on when the Barclay’s board would start to consider paying dividends.

“In response to a request from the Prudential Regulation Authority (PRA), we cancelled the full year 2019 dividend payment of 6 pence per ordinary share, and the Board will decide on future dividends and its capital returns policy at year-end 2020.”

“Despite all the challenges we face as a consequence of COVID-19, I am confident Barclays will emerge from this pandemic, well placed to continue to serve our customers and clients, the communities and economies in which we operate, and our shareholders.”

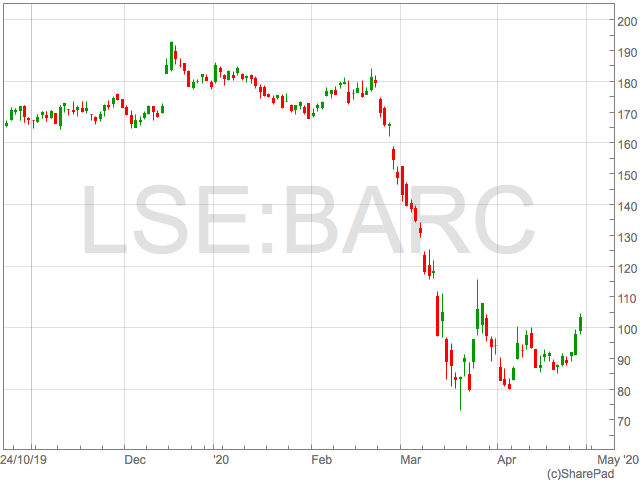

The Barclays share price was up 5.68% at 103.3p in the first hour of trading on Wednesday.

Before the impact of the £2.1bn provision, Barclays £3bn profit represents a strong increase on last year and will stoke investor optimism Barclays were in good shape going into the crisis.

“An event like the COVID-19 pandemic makes everyone focus on what’s really important right now. For us, that means running the bank safely and soundly, helping our customers and clients through the difficulties they face, supporting the UK economy and the communities where we live and work, and taking care of our colleagues around the world,” said Jess Staley in a statement included in the update.

Jess Staley continued to outline the impact government schemes such as CBILs had on Barclay’s ability to make loans to UK businesses.

“We welcome the government and Bank of England’s business support programmes and have introduced additional measures to back UK companies ourselves. They are now having a real impact. As at 24 April 2020 we have facilitated significant commercial paper issuance though the Covid Corporate Financing Facility, lent £737m in Coronavirus Business Interruption Loans, approved over 238,000 mortgage and loan payment holidays, and over 6 million customers and clients are currently paying no personal overdraft or business banking charges. We have launched a community aid package; through which we are donating £100m to support those who are being hardest hit by COVID-19. We expect that all of these measures will help to limit the economic and social impact of the pandemic.”

The Barclays CEO highlighted the impact of COVID-19 on the bank’s earning which would have been £3bn if they were not to set aside £2.1bn in provisions for bad loans due to the COVID-19 crisis.

“The impact of COVID-19 came late in what was until that point a good quarter. Statutory profit before tax was £0.9bn and profit before tax excluding credit impairment charges was £3.0bn. We have taken a £2.1bn credit impairment charge which reflects our initial estimates of the impact of the COVID-19 pandemic.”

“The strength of Barclays lies in our diversification by business, geography and currency, which allows us to remain resilient through the developing economic downturn.”

Touching on the letter from the Bank of England which instructed banks to cut their dividends, Staley provided a rough timeline on when the Barclay’s board would start to consider paying dividends.

“In response to a request from the Prudential Regulation Authority (PRA), we cancelled the full year 2019 dividend payment of 6 pence per ordinary share, and the Board will decide on future dividends and its capital returns policy at year-end 2020.”

“Despite all the challenges we face as a consequence of COVID-19, I am confident Barclays will emerge from this pandemic, well placed to continue to serve our customers and clients, the communities and economies in which we operate, and our shareholders.”

The Barclays share price was up 5.68% at 103.3p in the first hour of trading on Wednesday. Barclays shares rally as the bank prepares for COVID-19 fallout

Barclays shares (LON:BARC) rallied on Wednesday after the UK bank posted a reduction in profit for the first quarter as it set aside $2.1bn for bad debt dues to COVID-19.

Shares in Barclays rose significantly above 100p for the first time since late March as Barclays share price rallied over 5% to 103p in early trade on Wednesday.

The UK bank reported statutory profit before tax of £0.9bn, down from £1.5bn in the same period a year ago. Profit before tax would have been £3bn should the bank not have had to set aside £2.1bn in provisions for bad loans.

Before the impact of the £2.1bn provision, Barclays £3bn profit represents a strong increase on last year and will stoke investor optimism Barclays were in good shape going into the crisis.

“An event like the COVID-19 pandemic makes everyone focus on what’s really important right now. For us, that means running the bank safely and soundly, helping our customers and clients through the difficulties they face, supporting the UK economy and the communities where we live and work, and taking care of our colleagues around the world,” said Jess Staley in a statement included in the update.

Jess Staley continued to outline the impact government schemes such as CBILs had on Barclay’s ability to make loans to UK businesses.

“We welcome the government and Bank of England’s business support programmes and have introduced additional measures to back UK companies ourselves. They are now having a real impact. As at 24 April 2020 we have facilitated significant commercial paper issuance though the Covid Corporate Financing Facility, lent £737m in Coronavirus Business Interruption Loans, approved over 238,000 mortgage and loan payment holidays, and over 6 million customers and clients are currently paying no personal overdraft or business banking charges. We have launched a community aid package; through which we are donating £100m to support those who are being hardest hit by COVID-19. We expect that all of these measures will help to limit the economic and social impact of the pandemic.”

The Barclays CEO highlighted the impact of COVID-19 on the bank’s earning which would have been £3bn if they were not to set aside £2.1bn in provisions for bad loans due to the COVID-19 crisis.

“The impact of COVID-19 came late in what was until that point a good quarter. Statutory profit before tax was £0.9bn and profit before tax excluding credit impairment charges was £3.0bn. We have taken a £2.1bn credit impairment charge which reflects our initial estimates of the impact of the COVID-19 pandemic.”

“The strength of Barclays lies in our diversification by business, geography and currency, which allows us to remain resilient through the developing economic downturn.”

Touching on the letter from the Bank of England which instructed banks to cut their dividends, Staley provided a rough timeline on when the Barclay’s board would start to consider paying dividends.

“In response to a request from the Prudential Regulation Authority (PRA), we cancelled the full year 2019 dividend payment of 6 pence per ordinary share, and the Board will decide on future dividends and its capital returns policy at year-end 2020.”

“Despite all the challenges we face as a consequence of COVID-19, I am confident Barclays will emerge from this pandemic, well placed to continue to serve our customers and clients, the communities and economies in which we operate, and our shareholders.”

The Barclays share price was up 5.68% at 103.3p in the first hour of trading on Wednesday.

Before the impact of the £2.1bn provision, Barclays £3bn profit represents a strong increase on last year and will stoke investor optimism Barclays were in good shape going into the crisis.

“An event like the COVID-19 pandemic makes everyone focus on what’s really important right now. For us, that means running the bank safely and soundly, helping our customers and clients through the difficulties they face, supporting the UK economy and the communities where we live and work, and taking care of our colleagues around the world,” said Jess Staley in a statement included in the update.

Jess Staley continued to outline the impact government schemes such as CBILs had on Barclay’s ability to make loans to UK businesses.

“We welcome the government and Bank of England’s business support programmes and have introduced additional measures to back UK companies ourselves. They are now having a real impact. As at 24 April 2020 we have facilitated significant commercial paper issuance though the Covid Corporate Financing Facility, lent £737m in Coronavirus Business Interruption Loans, approved over 238,000 mortgage and loan payment holidays, and over 6 million customers and clients are currently paying no personal overdraft or business banking charges. We have launched a community aid package; through which we are donating £100m to support those who are being hardest hit by COVID-19. We expect that all of these measures will help to limit the economic and social impact of the pandemic.”

The Barclays CEO highlighted the impact of COVID-19 on the bank’s earning which would have been £3bn if they were not to set aside £2.1bn in provisions for bad loans due to the COVID-19 crisis.

“The impact of COVID-19 came late in what was until that point a good quarter. Statutory profit before tax was £0.9bn and profit before tax excluding credit impairment charges was £3.0bn. We have taken a £2.1bn credit impairment charge which reflects our initial estimates of the impact of the COVID-19 pandemic.”

“The strength of Barclays lies in our diversification by business, geography and currency, which allows us to remain resilient through the developing economic downturn.”

Touching on the letter from the Bank of England which instructed banks to cut their dividends, Staley provided a rough timeline on when the Barclay’s board would start to consider paying dividends.

“In response to a request from the Prudential Regulation Authority (PRA), we cancelled the full year 2019 dividend payment of 6 pence per ordinary share, and the Board will decide on future dividends and its capital returns policy at year-end 2020.”

“Despite all the challenges we face as a consequence of COVID-19, I am confident Barclays will emerge from this pandemic, well placed to continue to serve our customers and clients, the communities and economies in which we operate, and our shareholders.”

The Barclays share price was up 5.68% at 103.3p in the first hour of trading on Wednesday.

Before the impact of the £2.1bn provision, Barclays £3bn profit represents a strong increase on last year and will stoke investor optimism Barclays were in good shape going into the crisis.

“An event like the COVID-19 pandemic makes everyone focus on what’s really important right now. For us, that means running the bank safely and soundly, helping our customers and clients through the difficulties they face, supporting the UK economy and the communities where we live and work, and taking care of our colleagues around the world,” said Jess Staley in a statement included in the update.

Jess Staley continued to outline the impact government schemes such as CBILs had on Barclay’s ability to make loans to UK businesses.

“We welcome the government and Bank of England’s business support programmes and have introduced additional measures to back UK companies ourselves. They are now having a real impact. As at 24 April 2020 we have facilitated significant commercial paper issuance though the Covid Corporate Financing Facility, lent £737m in Coronavirus Business Interruption Loans, approved over 238,000 mortgage and loan payment holidays, and over 6 million customers and clients are currently paying no personal overdraft or business banking charges. We have launched a community aid package; through which we are donating £100m to support those who are being hardest hit by COVID-19. We expect that all of these measures will help to limit the economic and social impact of the pandemic.”

The Barclays CEO highlighted the impact of COVID-19 on the bank’s earning which would have been £3bn if they were not to set aside £2.1bn in provisions for bad loans due to the COVID-19 crisis.

“The impact of COVID-19 came late in what was until that point a good quarter. Statutory profit before tax was £0.9bn and profit before tax excluding credit impairment charges was £3.0bn. We have taken a £2.1bn credit impairment charge which reflects our initial estimates of the impact of the COVID-19 pandemic.”

“The strength of Barclays lies in our diversification by business, geography and currency, which allows us to remain resilient through the developing economic downturn.”

Touching on the letter from the Bank of England which instructed banks to cut their dividends, Staley provided a rough timeline on when the Barclay’s board would start to consider paying dividends.

“In response to a request from the Prudential Regulation Authority (PRA), we cancelled the full year 2019 dividend payment of 6 pence per ordinary share, and the Board will decide on future dividends and its capital returns policy at year-end 2020.”

“Despite all the challenges we face as a consequence of COVID-19, I am confident Barclays will emerge from this pandemic, well placed to continue to serve our customers and clients, the communities and economies in which we operate, and our shareholders.”

The Barclays share price was up 5.68% at 103.3p in the first hour of trading on Wednesday. ESG, Fintech, eCommerce and Medical Solution online get togethers

Sponsored by Earth Investments

Earth- investments ltd reports here on how It’s not all bad news, it’s just about businesses being flexible, and pulling together more in these uncertain times. Collaboration is key.

Earth Investments online Soirees, are a great example of business that are doing well and making the most of the lock down. They report massive interest in fintec, and ecommerce, and their alternative medical solutions are also booming. Many of their showcased businesses are enjoying huge interest from the current situation.

Their key to success is offering a unique approach to investments, the company focuses on collaborations based on positive impact before profit, as there has never been a better time to invest in certain businesses, for both those elements.

Ideas were brought together, when a group of friends brainstormed how to combine real impact, socially and environmentally with profitability, they then use their profits to do further good.

The Partners have a combination of 300 years of relevant experience, but have Stepped out of their corporate worlds to following their passion, and make a difference,

Vast Experience from the financial industry and real entrepreneurship, coupled with a passion to make a difference is at the heart of what creates this winning team, that energy has brought great results so far.

One partner was the head of loans and investments at Santander, other partners had worked 30 years for HMRC, and The CEO is a well known Relationship Therapist, Meditation teacher and human behaviour specialist, she has headed up raises of over $130 million to date.

All the partners came together with a united mission to help and support impact businesses, and have merged their extensive networks to focus on doing good in the world, offering a real heart felt way of doing business.

Before the lock down the group were running events at the Mayfair Hotel in London.

The Mayfair Hotel Soirees have now gone online!

They now have a strong international group of investors as members.

In keeping with the motto of ” Business should be sophisticated and fun”

The weekly zoom calls are said to be like a night out vibe, friends and fun brought to your home, to enjoy world class entertainers, renowned Ted talk speakers and the wonderful showcasing of a few selected businesses,

Every one who attends raves about these get togethers.

Business is best done when people like, know and trust each other and this creates such a great group, “we have over 50 billion in cumulative wealth on the calls, and business is getting done” the attitude of support and community is growing fast.

Tax advisors are helping people with much needed support too.

Heres a few comments from last week.

“It was a fantastic event, wonderfully hosted”

“Thank you for arranging all the follow up calls, with investors, what a great way to do business”

“The speaker gave me a much needed boost and it was the best piece of wisdom I’ve heard in a long time”

“I think that this is the way forward, I thoroughly enjoyed the entertainment and showcases thank you”

To apply to attend and become part of this wonderfully supportive group of movers and shakers, private investors, venture capitalists, and family offices apply on the link and we will discuss how we can help you, and offer you a free invite.

Click on the link below to vistit our website for more in formation

www.earth-investments.com/index.php/events/mayfair-soiree

Article Sponsored and Issued by Earth Investments

FTSE 100 surges as Trump outlines plan to reopen US economy

The FTSE 100 rallied inline with global equities on Tuesday as the market cheered plans from the US President to increase testing to help reopen the US economy.

The FTSE 100 was 2.1% higher at 5,970 in mid afternoon trading on Tuesday.

Donald Trump said he wanted to ramp up the testing of individuals across America in order allow broader reopening of the economy.

“We are continuing to rapidly expand our capacity and confident that we have enough testing to begin reopening and the reopening process,” said Trump in an address at the White House.

Some states had begun opening businesses last week after the US President passed responsibility to individual states to manage their own economies.

Today’s announcement brings back control of the reopening process to the White House as the administration will be driving forward the push to increase testing.

The White House also touched on plans for contact tracing in individuals who test positive for COVID-19.

Counties such as South Korea who implemented a high level of contact tracing have managed to keep deaths from coronavirus much lower than other major economies.

Broad FTSE 100 rally

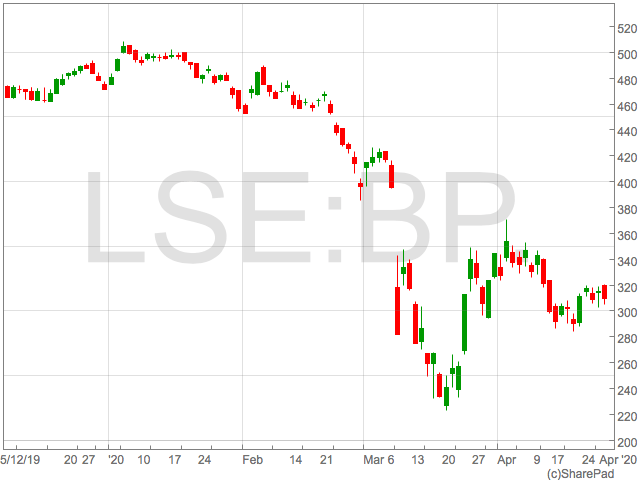

The FTSE 100 built on gains through Tuesday’s session as investors prepared for the economic recovery associated with the reduction in lockdown measures in the world’s largest economy. UK banks were significant gainers with Lloyds, Barclays and RBS all rising in excess of 7%. The move higher in banks also comes a day after the UK government announced ‘Bounce Back Loans’ for small business which will be 100% backed by the government, completely de-risking the banks making the loans. Oil companies BP and Shell were stronger as BP released a trading update and maintained their dividend for the first quarter. The price of oil, on the other hand, had another day of severe volatility as concerns resurfaced over storage capacity.Travis Perkins sees cash outflow slowing as stores reopen

Building material company, Travis Perkins (LON:TPK), has shed light on the impact of COVID-19 in a trading update that highlighted strong sales until lockdown measures were in place.

However, the pandemic shut large parts of Travis Perkins’ business, leading to a 4.8% reduction in sales across the group in the first quarter.

The company, which also owns Wickes and Toolstation, said it saw a £50m cash outflow during the first month of the coronavirus lockdown and has started to reduce cash commitments. Furloughing staff and deferring VAT payments will assist in TPK’s cash conservation. Travis Perkins have furloughed roughly half of their 30,000 staff for three weeks on full pay.

Providing some optimism on the reopening of the UK economy, Travis Perkins said it expected sales resumption to stem the flow in the coming weeks as its outlets begun to reopen.

The company also said it expected to benefit to the tune of £90m from business rates holidays.

House builders such as Taylor Wimpey have recently announced they will reopen sites again in early May, signalling a trend across the industry that will lead to increased demand for Travis Perkins goods.

Nick Roberts, Chief Executive, commented on the update:

“In light of the COVID-19 emergency, we have established a new operating model that has kept colleagues and customers safe, operating within Government guidelines, and enabling branches across all of the Group’s businesses to remain open. Moreover, we have provided essential services and support to keep the nation’s critical infrastructure maintained and operational and the UK’s homes warm, dry and safe during this time of need.

“We continue to adapt our operations, applying stringent social distancing and using technology to enable contactless operations, and we are therefore able to respond to the Government’s call to ensure that the construction industry can continue to deliver on crucial programmes and projects and be an engine for future economic recovery.

“As we move forward we will continue to adjust our operations, with our foremost priority to keep colleagues and customers safe and the industry supplied with the materials it needs.”

Shares in Travis Perkins were 3.2% higher on the day at 1,052p and are down 34% year-to-date.

House builders such as Taylor Wimpey have recently announced they will reopen sites again in early May, signalling a trend across the industry that will lead to increased demand for Travis Perkins goods.

Nick Roberts, Chief Executive, commented on the update:

“In light of the COVID-19 emergency, we have established a new operating model that has kept colleagues and customers safe, operating within Government guidelines, and enabling branches across all of the Group’s businesses to remain open. Moreover, we have provided essential services and support to keep the nation’s critical infrastructure maintained and operational and the UK’s homes warm, dry and safe during this time of need.

“We continue to adapt our operations, applying stringent social distancing and using technology to enable contactless operations, and we are therefore able to respond to the Government’s call to ensure that the construction industry can continue to deliver on crucial programmes and projects and be an engine for future economic recovery.

“As we move forward we will continue to adjust our operations, with our foremost priority to keep colleagues and customers safe and the industry supplied with the materials it needs.”

Shares in Travis Perkins were 3.2% higher on the day at 1,052p and are down 34% year-to-date.

House builders such as Taylor Wimpey have recently announced they will reopen sites again in early May, signalling a trend across the industry that will lead to increased demand for Travis Perkins goods.

Nick Roberts, Chief Executive, commented on the update:

“In light of the COVID-19 emergency, we have established a new operating model that has kept colleagues and customers safe, operating within Government guidelines, and enabling branches across all of the Group’s businesses to remain open. Moreover, we have provided essential services and support to keep the nation’s critical infrastructure maintained and operational and the UK’s homes warm, dry and safe during this time of need.

“We continue to adapt our operations, applying stringent social distancing and using technology to enable contactless operations, and we are therefore able to respond to the Government’s call to ensure that the construction industry can continue to deliver on crucial programmes and projects and be an engine for future economic recovery.

“As we move forward we will continue to adjust our operations, with our foremost priority to keep colleagues and customers safe and the industry supplied with the materials it needs.”

Shares in Travis Perkins were 3.2% higher on the day at 1,052p and are down 34% year-to-date. BP’s first quarter profit hit by lower oil price and demand destruction

FTSE 100 oil major BP (LON:BP) has reported a drop in profits in the first quarter as the lower oil price and a sharp reduction in demand due to coronavirus takes it’s toll.

BP’s Q1 underlying replacement cost profit fell to $0.8bn, down from $2.4bn in the same period a year ago.

The confirmation of such a large drop in profit barely moved the share price as the market has seemingly priced in the recent negative impact of the COVID-19 crisis to BP shares.

BP shares were softer by 1.59% to 309p in mid morning trade on Tuesday and are down 34% year-to-date.

Looking forward to the second quarter, investors should be prepared for a significant impact due to the lower price of oil. In the first quarter, BP recorded an averaage oil price of $47.47 per barrel, down from $55.90 in the fourth quarter of 2019.

With oil trading around $20 for much of the second quarter, which started 1st April, BP are likely to record a much lower oil price in the next trading update.

Despite the sharp reduction in profitability, BP have maintained their dividend of 10.5 cent which is due to be paid 19th June.

The maintenance of the dividend was helped in large part by BP’s strong cash position. BP had $32bn in liquid assets at the end if the quarter.

BP CEO, Bernard Looney commented on the results:

“This extraordinary time for the world demands extraordinary responses. And thankfully we are seeing that just about everywhere we look around the world. Our industry has been hit by supply and demand shocks on a scale never seen before, but that is no excuse to turn inward. BP, like many other companies, is stepping up and extending a helping hand to those in need. We do it not because it is expected of us – but because we want to. That is consistent with our purpose.”

“We are focusing our efforts on protecting our people, supporting our communities and strengthening our finances. I am incredibly proud of the work that our people are doing in all three areas, particularly our colleagues in operations – from rigs to

retail and everywhere in between – who are continuing to deliver energy and provide goods in the most difficult of circumstances.”

“At the same time, we are taking decisive actions to strengthen our finances reinforcing liquidity, rapidly reducing spending and costs, driving our cash balance point lower.”

“We are determined to perform with purpose and remain committed to delivering our net zero ambition.”

Looking forward to the second quarter, investors should be prepared for a significant impact due to the lower price of oil. In the first quarter, BP recorded an averaage oil price of $47.47 per barrel, down from $55.90 in the fourth quarter of 2019.

With oil trading around $20 for much of the second quarter, which started 1st April, BP are likely to record a much lower oil price in the next trading update.

Despite the sharp reduction in profitability, BP have maintained their dividend of 10.5 cent which is due to be paid 19th June.

The maintenance of the dividend was helped in large part by BP’s strong cash position. BP had $32bn in liquid assets at the end if the quarter.

BP CEO, Bernard Looney commented on the results:

“This extraordinary time for the world demands extraordinary responses. And thankfully we are seeing that just about everywhere we look around the world. Our industry has been hit by supply and demand shocks on a scale never seen before, but that is no excuse to turn inward. BP, like many other companies, is stepping up and extending a helping hand to those in need. We do it not because it is expected of us – but because we want to. That is consistent with our purpose.”

“We are focusing our efforts on protecting our people, supporting our communities and strengthening our finances. I am incredibly proud of the work that our people are doing in all three areas, particularly our colleagues in operations – from rigs to

retail and everywhere in between – who are continuing to deliver energy and provide goods in the most difficult of circumstances.”

“At the same time, we are taking decisive actions to strengthen our finances reinforcing liquidity, rapidly reducing spending and costs, driving our cash balance point lower.”

“We are determined to perform with purpose and remain committed to delivering our net zero ambition.”

Looking forward to the second quarter, investors should be prepared for a significant impact due to the lower price of oil. In the first quarter, BP recorded an averaage oil price of $47.47 per barrel, down from $55.90 in the fourth quarter of 2019.

With oil trading around $20 for much of the second quarter, which started 1st April, BP are likely to record a much lower oil price in the next trading update.

Despite the sharp reduction in profitability, BP have maintained their dividend of 10.5 cent which is due to be paid 19th June.

The maintenance of the dividend was helped in large part by BP’s strong cash position. BP had $32bn in liquid assets at the end if the quarter.

BP CEO, Bernard Looney commented on the results:

“This extraordinary time for the world demands extraordinary responses. And thankfully we are seeing that just about everywhere we look around the world. Our industry has been hit by supply and demand shocks on a scale never seen before, but that is no excuse to turn inward. BP, like many other companies, is stepping up and extending a helping hand to those in need. We do it not because it is expected of us – but because we want to. That is consistent with our purpose.”

“We are focusing our efforts on protecting our people, supporting our communities and strengthening our finances. I am incredibly proud of the work that our people are doing in all three areas, particularly our colleagues in operations – from rigs to

retail and everywhere in between – who are continuing to deliver energy and provide goods in the most difficult of circumstances.”

“At the same time, we are taking decisive actions to strengthen our finances reinforcing liquidity, rapidly reducing spending and costs, driving our cash balance point lower.”

“We are determined to perform with purpose and remain committed to delivering our net zero ambition.” Boris Johnson says the UK is now at maximum risk from COVID-19

In his first speech since falling ill, Boris Johnson has said this is the point the UK is at maximum risk from COVID-19, despite being past or nearly past the peak.

Johnson took the opportunity to highlight “there are real signs now we are passing through the peak” of coronavirus following a sustained plateau in the number of death in the UK and a reduction in the number of new cases.

The speech came just as countries such as Spain and Italy begin to reopen their economies after strict lockdowns. Over the weekend Spain allowed children outside for the first time in five weeks and Italy has said certain businesses will reopen 4th May. There is pressure on the UK government to provide guidelines on current lockdown measures given the raft announcements from other countries. The UK government also has another headache in the target it set itself of 100,000 tests per days by the end of April. With it looking highly doubtful the government will hit this self-imposed target, Boris Johnson is likely to receive criticism in his first week back in the job ass the country grows restless under social distances rules. Johnson did make reference to a possible announcement this week on what the lifting of measures could look like but made no comment on timings.UK Prime Minister Boris Johnson says “there are real signs now we are passing through the peak” of the coronavirus outbreak “thanks to our collective national resolve”https://t.co/5bxxzw13mR pic.twitter.com/whkrC5doVO

— BBC News (UK) (@BBCNews) April 27, 2020

Despite any action taken this week, critics will have hard numbers to target the UK government’s handling of the COVID-19. With deaths surpassing 20,000, the UK now has recorded nearly as many deaths as Italy and Spain whilst other European countries such as Germany and Sweden have kept their death rates remarkably low. Germany has managed to keep deaths from coronavirus to just 5,750 despite having a similar sized population as the UK. Sweden forewent strict lockdown measures yet has only recorded 2,200 deaths. In addition to the tragic human cost of coronavirus, the economic cost will likely be higher than it could of been due to the ineffectiveness of business loans made through banks and time it took to roll out the furlough scheme. The government is being blamed for the poor uptake of Coronavirus Business Interruption Loan Scheme. Just 16,000 loans have been made in the UK as France’s equivalent loan scheme has made 250,000.“We cannot spell out now how fast, or slow or even when those changes will be made” says @BorisJohnson. Though in coming days he promises to share emerging thinking on how to modify lockdown

— Robert Peston (@Peston) April 27, 2020

FTSE 100 gains in broad risk-on rally driven by reopening of economies

The FTSE 100 rose on Monday as stocks rallied in a broad risk-on rally sparked by optimism over the reopening of major economies.

Following weeks of strict lockdowns, Italy and Spain had begun lifting a number of measures which signalled a move back to some form of normality.

The United States has already begun an uncoordinated reopening with some states already allowing the resumption of trade for businesses such as hairdressers and bowling alleys.

President Trump has tabled the idea of a phased reopening but individual states have taken this as an opportunity to implement their own interpretation of an economic reopening.

The prospect of increased economic activity has caused a wave of optimism in markets with the FTSE 100 rising by 1.4% to 5,834 shortly before 12pm on Monday.

However, the reopening of economies has not been adopted in a globally coordinated basis and the UK still has no timeline or guidance on when the UK will start reopening it’s economy.

There is a consensus growing that countries must have a comprehensive testing programme in place to reopen businesses in a meaningful way.

The UK is yet to match other counties’ scale of testing so the UK government is likely to behind other governments in reopening the economy.

“We need to put in place a very dense testing regime so you would detect that rebound going back into exponential growth very quickly and not wait for the ICUs to fill up and there to be a lot of deaths. If you see the hot spot, you kind of understand the activities causing that,” said Bill Gates in an interview with CNN.

Stimulus and corporate results

The Bank of Japan was the latest central banks to release a round of stimulus as it announced it would make unlimited purchases of Japanese Government Bonds. Such a move would be considered extraordinary in normal circumstances but large purchases of assets by central banks has become the go-to response to COVID-19. Deutsche Bank also added to the positive mood on Monday after it made a pre-annoucment of earnings which pointed to profit being towards the higher end of estimates. Plant hire company Ashtead was the FTSE 100’s top riser on Monday as the company said profits would be largely inline with last year and the company’s status as an essential business had helped keep operations open.Ashtead share price builds on stable trading environment

Shares in plant-hire company Ashtead (LON:AHT) rose on Monday after the company said operations were relatively stable during the coronavirus crisis.

Although the US-focused business highlighted disruption due to coronavirus, the business has been classed as an essential business due to the work it does with emergency services. This means most of Ashtead’s locations have remained opened and providing Ashtead with a steady stream of business through the crisis.

The company also provided guidance on profit for 2020FY ending 30th April. Ashtead said it expects profit before tax to be in the region on £1.050m, this would be almost identical to 2019FY profit before tax of 1,059.5m.

Shares in Ashtead (LON:AHT) rose over 7% on Monday morning in reaction to the news.

US lockdown

The propensity of some states in America to begin reopening their businesses means the lockdown will become generally more liberal in the United States supporting construction work in the short-term. The Sunbelt brand is Ashtead’s most significant contributor to revenue with Sunbelt US accounting for 84% of group revenue in 2019FY. The gradual reopening of the US economy and Sunbelt’s status as an essential service is likely to provide support for Ashtead’s business for the remanding of 2020. Brendan Horgan, Group Chief Executive, commented on the update: “We are grateful for and extraordinarily proud of our team members who continue to respond as essential service providers during a time when our communities are in need. All levels of the organisation have quickly adapted our operations to continue servicing our customers while keeping our leading value of safety at the forefront of all we do.” :Looking forward, I am certain the swift actions we took during these unprecedented times and the strength of our balance sheet will serve the Group well. These factors, when combined with the diversity of our products and end markets, contribute to the strength of our long-term business model and put the Board in a position of confidence to look to the coming financial year as one of strong cash generation and strengthening our market position.”The emerging new sector of FTSE 100 ‘lockdown’ shares

There is an emerging new sector of FTSE 100 shares whose products and services have become inextricably linked to the coronavirus lockdown.

The economy has changed beyond recognition due to the spread of coronavirus and the subsequent lockdown and social distancing measures.

The initial market reaction was of course a devastating selloff that saw major global equity indices lose around a third of their value.

Equity indices, including the FTSE 100, have since stabilised and even started to move higher, helped by a recovery in beaten down cyclical shares, but also by an emerging new sector of those shares that benefit from the lockdown.

There are two factors behind the link to the lockdown; firstly those shares that enjoy increased revenue from the lockdown and those shares that benefit from increased buying by investors seeking a safe haven through the volatility.

These shares have outperformed during the coronavirus lockdown and will likely continue to do so whilst measures remain in place, until such a point they are lifted, when these stocks could very well underperform the wider FTSE 100 benchmark.

Ocado

Ocado has probably earned the crown as the ultimate lockdown share after consistently breaking record highs and posting gains of 25% in 2020. Consumers have flocked to Ocado’s website to avoid going to the supermarket to the extent the site crashed and others were unable to get a delivery slot for weeks. However the problems are now subsiding and Ocado is likely to have gained thousands of new customers that will continue to use their service after lockdown measures lift.

Sainsbury

Supermarkets are likely to be a beneficiary of the lockdown due to lack of alternatives for consumers who don’t buy items online. While demand for food remains relative steady after the spike higher due to panic buying, supermarkets will benefit from consumers purchasing goods they would have bought elsewhere during their trip to the supermarket. Sainsbury is particularly well placed to benefits from this with their in-store Argos offering, something that makes in stand out among the FTSE 100’s supermarket, although the likes of Morrisons and Tesco could well be be included as lockdown shares. In addition to the sales associated to Argos, with consumers unable to take holidays or eat out, it is likely they will spend more on higher quality items from Sainsbury as well as increasing the number of meals consumed as a result of shopping in Sainsbury’s stores.Polymetal & Fresnillio

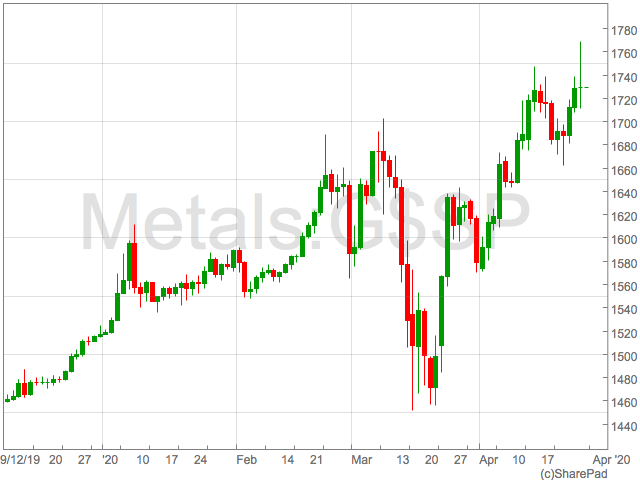

Gold and other precious metals provide investors with a safe have during times of volatility, as well as providing a hedge against inflation. The spread of coronavirus has provided plenty of market volatility and gold has reacted accordingly; the yellow metal is up 16% year-to-date. In addition, to market volatility lifting gold, the prospect of higher inflation will provide support for the gold price going forward. For the time being, an increase in the price of everyday goods will be largely offset by the drop in the price of oil but the unprecedented levels of monetary stimulus from central banks and fiscal cash injections will lead to higher level of inflations as economies begin to open up. FTSE 100 Polymental & Fresnillo have been on a tear since the beginning of lockdown measures and are set to remain elevated during the period of uncertainty.

Reckitt Benckiser

The FTSE 100 owner of Dettol, Cillit Bang and Air Wick will have experienced an uptick in demand during lockdown panic buying, and the home-oriented products are expected to experience steady demand throughout the lockdown. RB is also one of the traditionally defensive ‘bond-proxy shares’ which will become increasingly attractive to investors whilst government bond yields remain depressed.AstraZeneca

The entire world is attempting to move heaven and earth in order lift the coronavirus lockdown. The key to lifting the lockdown are effective measures prevent the spread of COVID-19 and reduce the death rate in those infected by the virus. A vaccine is many months away so effective treatment of severely ill patients will be the most immediate method of fighting COVID-19. AstraZeneca is currently trialing two drugs in Calquence and Farxiga. The drugs have already been approved for the treatment of leukaemia and diabetes so it is deemed safe to conduct broad trials. We await the early results for signs of efficacy in treating COVID-19IG Group sees a jump in new clients and higher trading revenue

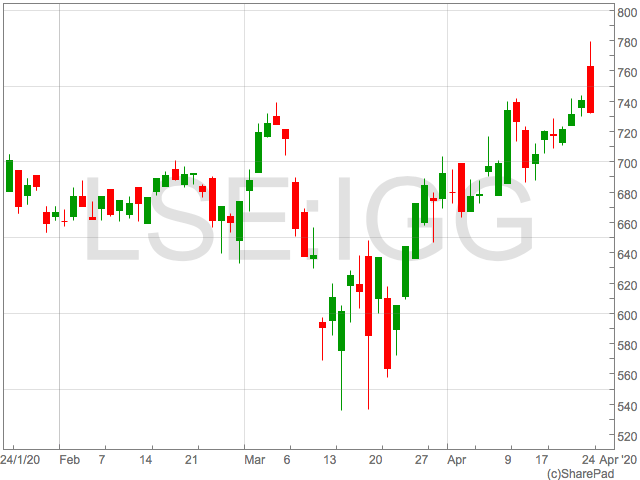

Spread betting and online trading company IG Group (LON:IGG) has enjoyed a sharp rise in the number of new clients and a jump in trading activity due to the coronavirus crisis.

The company said they had generated £173 million in the first 36 trading days of their Q4 trading period. When taking consideration revenue for the rest of the year it means IG have earnt £562.7 million in revenue so far in 2020FY, already well ahead of 2019FY’s £488m.

With the country under lockdown, traders have jumped at the opportunity to harness the volatility in financial markets by trading IG’s products.

The increase in activity means IG are set to return to revenue levels not seen since new ESMA regulations were implemented to help protect inexperienced retail clients from the high leverage of many of IG’s products.

However, the higher levels of activity meant remuneration levels would increase accordingly and costs were expected to rise by £40m.

The strength in the underlying business means IG Group are one of the few companies confident enough to maintain dividend payments and the company is to maintain their 43.2p dividend.

“During such a prolonged period of volatility, we’ve seen high volumes of clients choosing to trade markets with IG, reflecting our business resilience, our robust systems and our commitment to delivering the best possible trading experience,” said IG CEO, June Felix.

Cynics may argue the IG CEO attempts to distract from the fact IG have profited from the coronavirus crisis by drawing attention to the IG Brighter Future Fund in a large part of the comment on the results.

June Felix continued; “we are encouraged with the resilience and performance of our employees in such challenging times for everyone. The IG Brighter Future Fund builds on our culture of supporting the local communities in which we operate, helping disadvantaged young people gain access to improved educational opportunities. We are thrilled to be able to build on our partnership with Teach First and forge ties with other new international partners to support the long‐term education needs of children living through such an unsettling period.”

Shares in IG Group (LON:IGG) were down 0.6% in mid-afternoon trade having reverse early gains.

The increase in activity means IG are set to return to revenue levels not seen since new ESMA regulations were implemented to help protect inexperienced retail clients from the high leverage of many of IG’s products.

However, the higher levels of activity meant remuneration levels would increase accordingly and costs were expected to rise by £40m.

The strength in the underlying business means IG Group are one of the few companies confident enough to maintain dividend payments and the company is to maintain their 43.2p dividend.

“During such a prolonged period of volatility, we’ve seen high volumes of clients choosing to trade markets with IG, reflecting our business resilience, our robust systems and our commitment to delivering the best possible trading experience,” said IG CEO, June Felix.

Cynics may argue the IG CEO attempts to distract from the fact IG have profited from the coronavirus crisis by drawing attention to the IG Brighter Future Fund in a large part of the comment on the results.

June Felix continued; “we are encouraged with the resilience and performance of our employees in such challenging times for everyone. The IG Brighter Future Fund builds on our culture of supporting the local communities in which we operate, helping disadvantaged young people gain access to improved educational opportunities. We are thrilled to be able to build on our partnership with Teach First and forge ties with other new international partners to support the long‐term education needs of children living through such an unsettling period.”

Shares in IG Group (LON:IGG) were down 0.6% in mid-afternoon trade having reverse early gains.

The increase in activity means IG are set to return to revenue levels not seen since new ESMA regulations were implemented to help protect inexperienced retail clients from the high leverage of many of IG’s products.

However, the higher levels of activity meant remuneration levels would increase accordingly and costs were expected to rise by £40m.

The strength in the underlying business means IG Group are one of the few companies confident enough to maintain dividend payments and the company is to maintain their 43.2p dividend.

“During such a prolonged period of volatility, we’ve seen high volumes of clients choosing to trade markets with IG, reflecting our business resilience, our robust systems and our commitment to delivering the best possible trading experience,” said IG CEO, June Felix.

Cynics may argue the IG CEO attempts to distract from the fact IG have profited from the coronavirus crisis by drawing attention to the IG Brighter Future Fund in a large part of the comment on the results.

June Felix continued; “we are encouraged with the resilience and performance of our employees in such challenging times for everyone. The IG Brighter Future Fund builds on our culture of supporting the local communities in which we operate, helping disadvantaged young people gain access to improved educational opportunities. We are thrilled to be able to build on our partnership with Teach First and forge ties with other new international partners to support the long‐term education needs of children living through such an unsettling period.”

Shares in IG Group (LON:IGG) were down 0.6% in mid-afternoon trade having reverse early gains.