Facebook set to launch cryptocurrency

Facebook (NASDAQ:FB) is set to launch a cryptocurrency in 2020, it was announced on Tuesday.

The currency, which is set to be called Libra, will be available for use on Facebook apps such including WhatsApp and Instagram.

It will be stored in a digital wallet named Calibra, which is set to be available as an App next year.

Facebook said the currency will be aimed at the 1.7 billion individuals without a bank account.

However, concerns have been raised over data privacy and the security of the currency.

Facebook said that Libra will be managed independently by the Libra Association. The group includes MasterCard, PayPal, eBay, Spotify, Uber and Vodafone.

Stefano Parisse, group director of product and services at Vodafone, commented on Libra: “As a Founding Member of the Libra Network, Vodafone will extend its commitment to digital and financial inclusion by supporting the creation of a new global currency and encouraging a wide range of innovative financial services to be developed through its open-source platform.

“This has the potential to be truly transformative and will benefit those who have never used, or are struggling to access, financial services around the world.”

Last week, Facebook announced it was expanding its presence in the UK, with the creation of 500 new tech jobs in the capital.

The social network said it will create new jobs focusing on Artificial Intelligence, as it looks to address personal safety and security across its various apps.

Shares in Facebook are currently up +4.24% as of 10:39AM (GMT).

Castleton revenue jumps on organic growth and key acquisitions

Social housing solution provider Castleton Technology (LON:CTP) released preliminary full year results on Tuesday that revealed a 13% increase in revenue and 24% jump in adjusted EBITDA to £6.3 million.

Revenue growth was driven by a combination of both organic growth and a number of acquisitions. Organic revenue growth represented 7.3% as Castleton successfully cross-sold their suite of products to their some 591 housing association clients.

Castleton reported an increase to 50% from 40% in the number of the clients taking more than one product.

These agreements are typically providing multi-year revenue sources from ongoing service provision.

An example of this is a 4-year contract with Dumfries and Galloway Housing Partnership, worth £1.2m.

Key to revenue growth going forward will be the ability of Castleton to guide existing customers towards the sweet spot of customers taking eight or more of their products. Currently just 7% of clients are taking eight or more products providing significant cross-selling opportunities in 2020FY.

Acquisitions

Castleton are demonstrating a focus on delivering enhanced technology solutions with the acquisition of an Indian service provider who previously supplied the group with additional development capacity. The Indian acquisition was one of three notable acquisitions in the period that included technologies for delivering financial modelling and communication tools. Dean Dickinson, CEO of Castleton, said: “It has been another year of significant progress for Castleton, delivering strong organic growth at both revenue and EBITDA level underpinned by healthy cash generation. This has not only resulted in the continued reduction in net debt, but it has also enabled operational growth through the acquisition of Deeplake, the perpetual licence for our modelling solution, the launch of new digital solutions and expanded development capabilities with Castleton India.” “A number of milestone projects are now fully-live and operational with three early adopter sites for integrated solutions. These combined customer references have been a major contributor to us winning the new integrated solutions contract in January with Connect. The early adopters and this new contract demonstrate the strength of our proposition, our ability to cross-sell and the trust our customers have in our capabilities to deliver on their vision for complete digital transformation.” finnCap issued a note following this morning’s results which forecast revenue of £28.5m for 2020, rising to £30.5m in 2021. finnCap have a 140p price target on Castleton.Kier Group shares sink on strategic review and dividend suspension

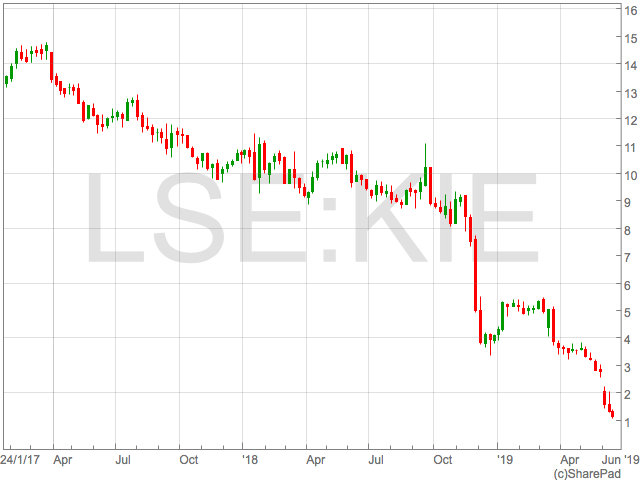

Kier Group (LON:KIE) shares sank on Monday as the group announced a strategic review and the suspension of its dividend.

The group said it would shift focus to regional building, infrastructure, utilities and highways by selling or exiting its non-core businesses such as Kier Living and environmental services.

Shares in Kier Group were down over 14% in Monday afternoon, trading at a little over 110p. Shares in Kier Group have fallen from highs around 1,400p in 2017.

The company now has a market capitalisation of just £183m, the lowest in the FTSE 350.

The strategic review is the result of debt levels the group today said were ‘too high’ and low levels of cash generation accentuating the companies debts.

Andrew Davies, Chief Executive of Kier, commented:

“Since becoming Chief Executive on 15 April, I have visited many of our key locations and spent time with all of our businesses, meeting the leadership teams and many of our dedicated people in the process. I have also met with many of our clients. Kier has a number of high-quality, market-leading businesses, in particular Regional Building, Infrastructure, Utilities and Highways. I believe that these businesses will deliver long-term, sustainable revenues and margins and are inherently cash generative.”

“As previously announced, I have been leading a strategic review which has resulted in the actions being announced today. These actions are focused on resetting the operational structure of Kier, simplifying the portfolio, and emphasising cash generation in order to structurally reduce debt. By making these changes, we will reinforce the foundations from which our core activities can flourish in the future, to the benefit of all of our stakeholders.”

The problems that led to the collapse of Carillion will be fresh in the minds of investors and there are significant similarities with the problems Kier Group are facing.

Kier Group will be aware of this and have taken drastic steps to reduce head count by 1,200 – whether this provides a base to rebuild is to some extent out of Kier’s hands and will ultimately depend on government contracts.

The strategic review is the result of debt levels the group today said were ‘too high’ and low levels of cash generation accentuating the companies debts.

Andrew Davies, Chief Executive of Kier, commented:

“Since becoming Chief Executive on 15 April, I have visited many of our key locations and spent time with all of our businesses, meeting the leadership teams and many of our dedicated people in the process. I have also met with many of our clients. Kier has a number of high-quality, market-leading businesses, in particular Regional Building, Infrastructure, Utilities and Highways. I believe that these businesses will deliver long-term, sustainable revenues and margins and are inherently cash generative.”

“As previously announced, I have been leading a strategic review which has resulted in the actions being announced today. These actions are focused on resetting the operational structure of Kier, simplifying the portfolio, and emphasising cash generation in order to structurally reduce debt. By making these changes, we will reinforce the foundations from which our core activities can flourish in the future, to the benefit of all of our stakeholders.”

The problems that led to the collapse of Carillion will be fresh in the minds of investors and there are significant similarities with the problems Kier Group are facing.

Kier Group will be aware of this and have taken drastic steps to reduce head count by 1,200 – whether this provides a base to rebuild is to some extent out of Kier’s hands and will ultimately depend on government contracts.

The strategic review is the result of debt levels the group today said were ‘too high’ and low levels of cash generation accentuating the companies debts.

Andrew Davies, Chief Executive of Kier, commented:

“Since becoming Chief Executive on 15 April, I have visited many of our key locations and spent time with all of our businesses, meeting the leadership teams and many of our dedicated people in the process. I have also met with many of our clients. Kier has a number of high-quality, market-leading businesses, in particular Regional Building, Infrastructure, Utilities and Highways. I believe that these businesses will deliver long-term, sustainable revenues and margins and are inherently cash generative.”

“As previously announced, I have been leading a strategic review which has resulted in the actions being announced today. These actions are focused on resetting the operational structure of Kier, simplifying the portfolio, and emphasising cash generation in order to structurally reduce debt. By making these changes, we will reinforce the foundations from which our core activities can flourish in the future, to the benefit of all of our stakeholders.”

The problems that led to the collapse of Carillion will be fresh in the minds of investors and there are significant similarities with the problems Kier Group are facing.

Kier Group will be aware of this and have taken drastic steps to reduce head count by 1,200 – whether this provides a base to rebuild is to some extent out of Kier’s hands and will ultimately depend on government contracts.

The strategic review is the result of debt levels the group today said were ‘too high’ and low levels of cash generation accentuating the companies debts.

Andrew Davies, Chief Executive of Kier, commented:

“Since becoming Chief Executive on 15 April, I have visited many of our key locations and spent time with all of our businesses, meeting the leadership teams and many of our dedicated people in the process. I have also met with many of our clients. Kier has a number of high-quality, market-leading businesses, in particular Regional Building, Infrastructure, Utilities and Highways. I believe that these businesses will deliver long-term, sustainable revenues and margins and are inherently cash generative.”

“As previously announced, I have been leading a strategic review which has resulted in the actions being announced today. These actions are focused on resetting the operational structure of Kier, simplifying the portfolio, and emphasising cash generation in order to structurally reduce debt. By making these changes, we will reinforce the foundations from which our core activities can flourish in the future, to the benefit of all of our stakeholders.”

The problems that led to the collapse of Carillion will be fresh in the minds of investors and there are significant similarities with the problems Kier Group are facing.

Kier Group will be aware of this and have taken drastic steps to reduce head count by 1,200 – whether this provides a base to rebuild is to some extent out of Kier’s hands and will ultimately depend on government contracts. Sativa Investments appoints Cenkos as new corporate broker and advisor

Sativa Investments (LON:SATI) has appointed Cenkos as their new corporate broker and advisor.

Sativa Investments thanked their prior broker Peterhouse in the release who oversaw the listing of Sativa on the NEX Exchange 15 months ago.

Geremy Thomas, founder and Chief Executive Officer of Sativa Investments commented:

“Cenkos is a top-ranking financial adviser and broker and has demonstrated its knowledge of the medicinal cannabis and CBD wellness industry by recently publishing a world-class and highly detailed industry note.

“Cenkos’ appointment is in line with Sativa’s progression from, in only 15 months, being the UK’s first listed medicinal cannabis investment vehicle to its transition to a fully operational seed-to-consumer trading business.

“The UK medicinal cannabis industry has significant growth opportunities and we look forward to working with Cenkos on the Company’s next phase of development, which will include engaging with major institutional investors who are now showing an interest for medicinal cannabis and CBD wellness equities.”

Name change to Sativa Group

The change in broker comes hot on the heels of a proposed change in the name to Sativa Group at the recent Annual General Meeting. The cannabis group has secured a number of deals in the past few months including a supply agreement with a Swiss firm as the group establishes a model thats places Sativa as a purchaser of raw materials as opposed to a producer in what the company calls a ‘smart-sourcing strategy’. The company is set to open its first Goodbody & Blunt CBD and wellness outlet in Bath later in June.UK cannabis listings

Sativa Investments was the first cannabis companies to list in London some 15 months ago and is one of a handful of early stage cannabis companies listed in the UK. While Sativa Investments joined the market as a cannabis company through an IPO, others have shifted their operations to cannabis from other sectors. Highlands Natural Resources, for example, was operating shale exploration in Colorado before raising funds to launch a vertically integrated cannabis business.

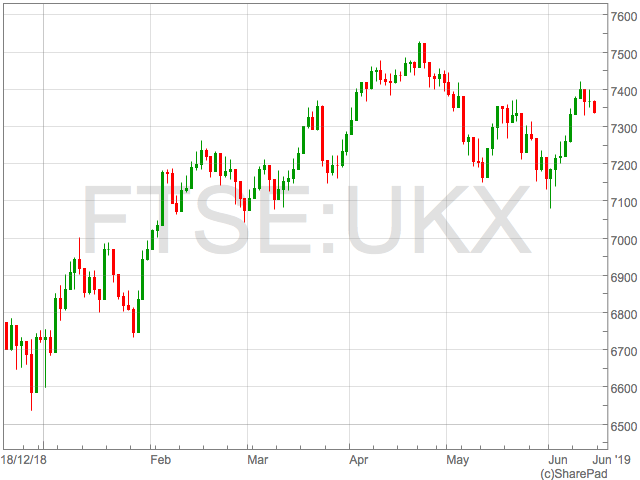

FTSE 100 falls on Iran worries and poor Chinese data

The FTSE 100 has retreated further from 6 -week highs made earlier this week as tensions in the Gulf of Oman and poor Chinese data hits UK stocks.

The FTSE 100 was down as much as 0.57% in early trade on Friday to 7327 as investors pondered the consequences of explosion on a number of oil tankers in recent weeks and whether it could lead to military confrontation between Iran and the United States.

Iran has strenuously denied suggestions from the United States that they were involved in the explosions and have said they felt were being framed. There has so far been no solid evidence as to the parties involved in the explosions or the cause.

Sentiment was further soured by a raft of Chinese data that suggested the US/Sino trade war was having a negative impact on the world’s second largest economy.

“The Chinese data overnight was not good, the country clearly feeling the trade war pinch. Fixed asset investment fell from 6.1% to 5.6%, its worst level in 7 months, while industrial production dropped to 5.0% for the first time in 17 years. Only the retail sales reading avoided a precipitous decline, instead unexpectedly jumping from 7.2% to 8.6%,” said Connor Campbell, Financial Analyst at Spreadex.

Chinese GDP growth has fallen to 6.4% and the measures imposed by the Trump administration are being blamed on slowdown which could have far reaching implications for the global economy and the globally focussed FTSE 100.

In individual stock news, Autotrader fell 2.6% as it broke key technical levels following a strong 2019 which has seen shares rally from 429p to highs of 605p. The group recently report final results which revealed an 8% increase in revenue to £355.1 million. Profit before tax rose 15% in a strong year that has seen Autotrader enter the FTSE 100 index.

The top riser was precious metals miner Fresnillo whose perceived safe haven characteristics has won favour of traders seeking an outlet in the face of geo-political tensions.

In individual stock news, Autotrader fell 2.6% as it broke key technical levels following a strong 2019 which has seen shares rally from 429p to highs of 605p. The group recently report final results which revealed an 8% increase in revenue to £355.1 million. Profit before tax rose 15% in a strong year that has seen Autotrader enter the FTSE 100 index.

The top riser was precious metals miner Fresnillo whose perceived safe haven characteristics has won favour of traders seeking an outlet in the face of geo-political tensions.

In individual stock news, Autotrader fell 2.6% as it broke key technical levels following a strong 2019 which has seen shares rally from 429p to highs of 605p. The group recently report final results which revealed an 8% increase in revenue to £355.1 million. Profit before tax rose 15% in a strong year that has seen Autotrader enter the FTSE 100 index.

The top riser was precious metals miner Fresnillo whose perceived safe haven characteristics has won favour of traders seeking an outlet in the face of geo-political tensions.

Iofina receives approval to develop CBD oil in Kentucky

Iofina announced it is set to explore producing and developing CBD oil and other hemp-based products on Thursday.

The company said it had received conditional approval for its Hemp Processor/Handler License Application from the Kentucky Department of Agriculture.

The will allow the company to explore the production of cannabidiol based products as part of its newly created IofinaEX subsidiary.

Explaining the decision to move into the cannabis market, Iofina cited The 2018 Agriculture Improvement Act, which legalised the cultivation of hemp at a federal level.

President and CEO Dr. Tom Becker commented: ‘‘The Directors are determined to explore the isolation of CBD oil and other valuable products from hemp, a market which is currently under developed but rapidly growing. Iofina’s expertise in speciality chemicals makes the new venture a suitable addition to the Iofina Group.

“The conditional approval for our Handler/Processor License in Kentucky is an important step forward as we plan to execute the project at IofinaEX, and we look forward to updating the market as we develop this subsidiary further.”

Iofina specialises in the exploration and development of Iodine.

Its operations are in the US, specifically in Kentucky, Montana, and Oklahoma.

However, the company is London-listed on the junior AIM market.

Shares in Iofina (LON:IOF) are currently +9.06% as of 13:43PM (GMT), on the back of the announcement.

PwC fined £4.55m over Redcentric audit

PwC has been fined £4.55 million over the conduct of its audit of Redcentric.

PwC was dealt the fine by The Financial Reporting Council (FRC), the UK’s audit regulator.

The FRC had initially fined the auditor £6.5 million, however it was reduced after PwC publicly apologised for its mistakes.

The council also imposed sanctions against two partners, Jaskamal Sarai and Arif Ahmad, in relation to an audit conducted between March 2015 and March 2016.

Both individuals were fined £140,000 pounds each.

Claudia Mortimore, Deputy Executive Counsel to the FRC, said in a statement:

“The sanctions reflect the seriousness and extent of the breaches. Professional scepticism was lacking in this audit. Had it been applied, it is likely that certain material misstatements would have been detected. As this is the second Final Decision Notice involving PwC Leeds’ office in recent years, we have mandated that the firm supplements its ongoing monitoring and support for that office, to further improve the quality of audit work in the future.”

A PwC spokesperson added: ‘We are sorry that our work fell below the professional standards expected of us. Since the work in question was completed, we have taken numerous steps to strengthen processes. In addition, this month we announced an additional £30m investment annually as part of a new wide-ranging action plan to provide greater focus on the quality and public interest responsibilities of PwC’s statutory audit services.

Accountancy firms such Deloitte, KPMG, EY and PwC are under pressure amid calls for reform in the industry.

MPs have called for the so-called ‘Big Four’ to be broken up to lessen their “stranglehold” on the industry.

Tesco sales growth slows in Q1

Tesco (LON:TSCO) reported a slowdown in sales growth in the first quarter in a trading update on Thursday.

The UK’s largest supermarket said that like-for-like sales increased 0.4% year-on-year in three month period until 25 May.

This marked a slowdown from 1.7% reported for the previous quarter.

Meanwhile, total sales slipped by 0.4%, impacted by the closure Tesco Direct last year.

Nevertheless, the supermarket said that this proved ahead of the UK market.

Chief Executive Dave Lewis, commented on the results: “We have had a strong start to the year, growing ahead of the UK market on both a volume and value basis. Our customer offer is more competitive than ever, with a wider choice of our ‘Exclusively at Tesco’ products now available in more stores, helping to drive more than 10% sales growth across the range.”

In recent years Tesco has faced intensified competition from rivals such as Lidl and Aldi, both of whom have continued to grow market share.

On Wednesday, Lidl announced plans to further expand into London, opening a further 40 stores.

The move could prove a blow to the various Tesco Express locations in the capital.

Last year, Tesco unveiled a new discount store, Jack’s, with the aim of taking on the growing popularity of Lidl and Aldi.

Shares in the supermarket are currently down -0.53% as of 12:24PM (GMT).