MPower operates a B2B business model and has established a distribution network which have taken advantage of MPower’s turn-key solutions.

Whilst MPower is making a positive environmental impact, it has combined this with a positive financial impact through a ‘lease-to-financing’ model that empowers bossinesses and individuals.

MPower operates a B2B business model and has established a distribution network which have taken advantage of MPower’s turn-key solutions.

Whilst MPower is making a positive environmental impact, it has combined this with a positive financial impact through a ‘lease-to-financing’ model that empowers bossinesses and individuals.

Clean Energy startup MPower reaches overfunding on Crowdcube

Clean energy start MPower has reached overfunding on Crowdcube after securing more than £300,000 to expand its Africa focused fintech and clean energy business.

The company is focused on solar powered products that are backed by their software, data solutions and a financing model that supports a distribution network.

MPower provides plug & play solar powered products such as refrigerators and water pumps to rural communities in Africa and have already reached over 2000 end-users in Africa with operations in Togo, Cameroon and Zambia.

MPower operates a B2B business model and has established a distribution network which have taken advantage of MPower’s turn-key solutions.

Whilst MPower is making a positive environmental impact, it has combined this with a positive financial impact through a ‘lease-to-financing’ model that empowers bossinesses and individuals.

MPower operates a B2B business model and has established a distribution network which have taken advantage of MPower’s turn-key solutions.

Whilst MPower is making a positive environmental impact, it has combined this with a positive financial impact through a ‘lease-to-financing’ model that empowers bossinesses and individuals.

MPower operates a B2B business model and has established a distribution network which have taken advantage of MPower’s turn-key solutions.

Whilst MPower is making a positive environmental impact, it has combined this with a positive financial impact through a ‘lease-to-financing’ model that empowers bossinesses and individuals.

The Royal Mint to produce medical visors for the NHS

The Royal Mint is set to start producing medical visors for the NHS to help fill the gap in protective equipment for frontline medical staff in the UK.

The Royal Mint will produce the visor in their state of the art manufacturing plant in Llantrisant.

Usually associated with the production of coins, engineers at the Royal Mint were keen to support the NHS and set about production after finding prototype designs on the internet.

The initial batch of orders will be provided to the Cwm Taf Morgannwg University Health Board Wales but say the have capacity to provide thousands of visors. To facilitate the ramp up in production, the Royal Mint have put out requests for rate materials.

Leighton John, Director of Operations for The Royal Mint commented: “My sister works for the NHS and it really focuses your mind on the challenges they are facing, and the opportunity we have to support them.

“On Wednesday at 9am we knew nothing about medical visors, but we set our engineers the task of developing essential medical equipment which could be easily made on site – within seven hours they’d created a medical visor, and within 48 hours it was approved for mass manufacture. We’ll shortly post the specifications on our website to enable other firms to make them too.

“We are now developing the production line, and urgently calling for help to source 1.0mm PET clear plastic which is in low supply across the UK. We believe firms will have this in stock, and we’d urge them to get in touch with us so we can continue to support our NHS.”

The Royal Mint joins a wave of companies shifting their manufacturing abilities to help fight coronavirus; LVMH have started producing hand sanitiser, F1 teams are making ventilators and Amazon is helping with distribution.

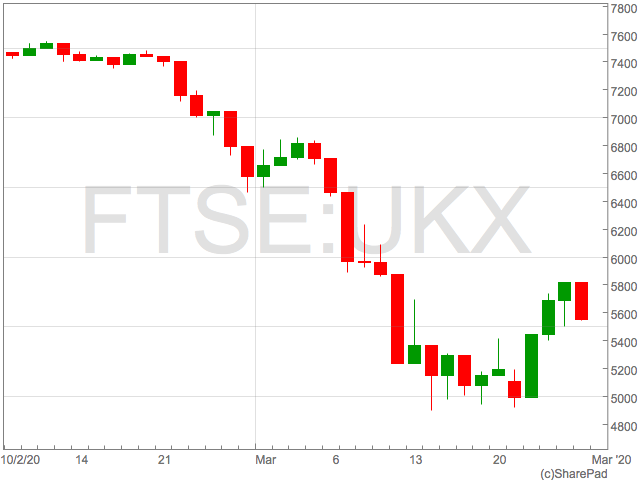

The case for investing in FTSE 100 shares now

After the recent selloff in FTSE 100 shares there is an abundance of companies trading at their lowest levels for decades and could present excellent value for the long-term investor.

Indeed, many shares were offering very good value on an earnings basis before the coronavirus selloff, and it would appear that they only offer better value now.

However, the recent selloff is also a stark reminder that shares present risks to investors due to sudden changes in the macro environment that feed through to underlying company earnings. This is a risk that remains despite shares being at record lows and investors should think hard about what makes shares a good price to buy.

Taking the hypothetical example of company XYZ plc’s shares that were trading at £10 in January and are now trading at £3, it doesn’t necessarily mean they are now ‘good value’ or ‘cheap’.

When assessing the value of FTSE 100 companies, investors should reflect on companies’ earning potential in the future, typically over the next 12 months.

Indeed, measures implemented by central banks and government such as the Federal Reserve’s ‘unlimited’ asset purchase and the UK’s promise to pay workers 80% of their wages will provide short term relief rallies.

These should be treated with caution as they can represent ‘Bull Traps’ that suck investors into thinking stocks will continue back up to recent highs, before dumping again.

Technical analysts will always recommend waiting for markets to retest highs or lows before entering a position around market reversals. This means you avoid being sucked into traps and reaffirms the market will respect lows before they move higher.

In the case of the FTSE 100, the key levels to retest will be 5,000. This is both psychological and very close to the closing low of 4,993.

Earnings

The recent selloff in equities due to the spread of COVID-19 was driven in the most part by uncertainty on what earnings will look like over the next 12 months, and the assumption they will be severely reduced. A reduction in earnings will be reported by a large proportion of the FTSE 100; airlines have completely shutdown, banks are being forced into repayment holidays and utility companies are going to see power usage and prices fall. The key question for investors is now whether, over the next 6-12 months, the earnings outlook is going to change to the extent that the recent decline in equity prices makes current share prices good value compared to future earnings. Whilst monetary and fiscal stimulus will prevent company earnings from completely collapsing, a broad rally in share prices will depend almost entirely on an economic recovery driven by businesses resuming operations and creating jobs, once the peak of coronavirus has passed. In short, a sustained rally back to the FTSE 100 highs around 7,700 is only likely once the health crisis shows signs of ending. However, as investors await a medical response to COVID-19 they will be presented with once in a generation opportunities for long term purchases, but must be prepared to accept short term volatility.Bull Trap

Indeed, measures implemented by central banks and government such as the Federal Reserve’s ‘unlimited’ asset purchase and the UK’s promise to pay workers 80% of their wages will provide short term relief rallies.

These should be treated with caution as they can represent ‘Bull Traps’ that suck investors into thinking stocks will continue back up to recent highs, before dumping again.

Technical analysts will always recommend waiting for markets to retest highs or lows before entering a position around market reversals. This means you avoid being sucked into traps and reaffirms the market will respect lows before they move higher.

In the case of the FTSE 100, the key levels to retest will be 5,000. This is both psychological and very close to the closing low of 4,993.

Investors must consider the Enterprise Investment Scheme (EIS) to support the NHS and economic recovery

to support the NHS and economic recovery")

Enterprise Investment Scheme (EIS) investments are sought by investors around the end of the tax year as they seek mitigate tax with investment in exciting innovative companies.

This year more than ever, investor focus will be on innovative medical opportunities, especially those promising to provide relief in the NHS battle against COVID-19.

There have been a number of high profile products from listed companies helping the coronavirus crisis such as Novacyt’s COVID-19 testing kits, but some of the real innovations may be unlocked in unlisted companies that could benefit from EIS investment.

Andrew Aldridge, Partner at Deepbridge Capital, has highlighted investors can help innovations in the healthcare sector by investing in companies that are directly providing treatments and researching therapies and vaccines for COVID-19, as well as those developing ventilators.

In addition, Andrew Aldridge suggested EIS investors should also consider companies providing relief to the ongoing strains on the NHS such online healthcare delivery platforms, technologies to assist with remote working and devices designed to minimise human contact.

“These companies are quite rightly receiving commercial interest in the acquisition of products but in order for them to be able to scale up research development and manufacturing, they also need venture capital. The EIS is therefore a key Government weapon in this current fight,” said Andrew Aldridge.

“By utilising the EIS, investors can benefit from generous tax reliefs (potentially including income tax relief mitigation, CGT deferral, IHT mitigation and loss relief), whilst also directly assisting the UK’s healthcare and economic battle with Coronavirus. Delaying investments should not be an option. Investors and financial advisers should be speaking with EIS product providers in the life sciences and tech sectors and asking how they can help raise much needed funds.”

“The NHS staff, the supermarket workers, those ensuring the UK continues as best to continue to operate with some vague degree of normality are quite rightly the heroes of the hour. However, investors can have a major impact on this scenario by ensuring that innovators have the resources to expedite their innovations which can make a real distance.”

Investors choosing to invest through the Enterprise Investment Scheme get numerous tax benefits including 30% tax relief and exemption, capital gains tax and relief on any losses.

Economic recovery

The Enterprise Investment Scheme can not only help with the funding of medical companies fighting coronavirus but will be instrumental in helping the UK economic recovery. SMEs employed 16.6 million people in 2019, representing 60% of the working population and the backbone of the UK economy. While the Enterprise Investment Scheme provides investors with generous tax benefits and the potential of huge returns, it also supports employment in innovative and high growth sectors such as technology, healthcare, food and drink, and sustainability. The importance of the EIS was highlighted by Director General of the Enterprise Investment Scheme Association, Mark Brownridge, who has been lobbying government to increase reliefs given to investors in an effort to further support investment during the coronavirus slowdown. He said: “we believe it is perfectly achievable to implement these recommendations in the short term and that they will facilitate faster and increased deployment of capital to entrepreneurial businesses.” “We estimate that between £100m to £200m of addition private investment could be achieved right now to support the businesses that represent the future, but without this additional support they may well not achieve their full potential, or at worst may fail. We strongly urge the Government to review our recommendations”EIS Opportunity: Help Me Stop – Rehab in The Real World

Help Me Stop (www.helpmestop.org.uk) is a breakthrough non-residential alcohol and drug treatment service launched in recent months in London. The Help Me Stop “Dayhab” service is based on the successful US Intensive Outpatient Programme model, which has been proven to produce the same results as the traditional residential treatment model, but at only one tenth of the cost.

With COVID-19 keeping many of us in our homes, and access to addiction treatment becoming much harder, Help Me Stop has now launched a Digital Dayhab solution to operate alongside the Company’s existing first centre in West London.

The UK is currently failing in the way alcohol and drug addicts can access suitable treatment. Every year in the UK 500,000 people are looking for addiction treatment, but less than 3% are accessing rehab due to the very high cost of residential treatment. Price and disruption to lifeare the two most common reasons for clients not finding suitable Rehab.

A typical residential centre will charge £25,000 for 4 weeks – the Help Me Stop Digital Dayhab service provides 75 hours of intense treatment over 4 weeks for £1,750 – less than 10% of the cost. The service consists of a combination of group and one on one sessions, and there is also a supplementary recovery service and family programme available alongside the core programme.

The first Help Me Stop Dayhab centre was successfully launched in the summer of 2019 and has to date performed to plan. Due to the current epidemic, however, the Company has temporarily paused its branch expansion programme, to focus on the launch of its new online service, which is already signing up clients and showing signs of taking off successfully.

It should be noted that the new online service has the potential to attract clients from all over the UK and is not geographically restricted. Help Me Stop therefore has the ability to bring affordable Dayhab to both the home and the high street.

Help Me Stop is not only generating significant demand and demonstrating its viabilityin the UK market, mirroring the US experience, it is also a totally scalable business with potential to expand quickly across the UK in the next 3-5 years with a combination of online and high street units, in the process disruptingthe marketplace by putting recovery within reach for many thousands of people.

The current offer document for Help Me Stop assumes a branch roll out to up to 12 branches by 2023. The Directors believe that the new Digital Service has the potential to easily replicate and possibly exceed that growth pattern. The business is projecting Ebitda of £3.5m by 2023, which based on an exit multiple of 10 (industry average is 9-13) would produce a value of £35m, equivalent to a return of 8 x cash.

The business qualifies for EIS and will be issuing shares both before and after the tax year end, providing the ability for investors to carry income tax relief back to 2018-2019 tax year, if required.

The Greatland Gold share price offers a buying opportunity

The Greatland Gold share price (LON:GGP) has pulled back from their recent highs and as it finds support, analysts are suggesting now is a good time to buy.

Greatland Gold has outperformed during the period of volatility in stock markets in 2020 due to an exciting series of updates from its gold projects in Australia.

The company is operating six exploration licenses in Western Australia and Tasmania in areas that have not previously been subject to heavy prospecting.

The Gold safe haven?

Gold has been long though of as a safe-haven and the perfect place to allocate capital during periods of uncertainty and Greatland Gold could be seen as a proxy for the underlying price of gold. However, the safe haven gold thesis has tested and somewhat disproved during the recent the selloff. As coronavirus started to negatively affect global stock markets, true to form there was a move higher in gold as investors flocked to safe havens such as gold and bonds. Though gold initially rose, as market volatility picked up in stock markets it feed through to the gold market with market participants being forced to liquidate positions in the gold futures and options markets to cover requirements elsewhere. Gold prices sank $250 and have not yet again tested to the upside. With such moves causing volatility in gold, it suggests Greatland Gold should not be seen as a safe haven proxy investment on the price of gold. This is not where the opportunity lies for Greatland Gold, or where investors will find share price appreciation. In the same vein, it is unlikely volatility in the price of gold will negatively impact Greatland Gold in the short term.Greatland Gold shares

Greatland Gold shares have risen not because of a move higher in the price of gold, but because of progress in it’s exploration program in Australia, which has yielded very encouraging drill results. The most recent of these announcements was an update on the Havieron deposit in the Paterson region of Western Australia. The company said the Havieron project had demonstrated high-grade mineralisation with a 0.5m section yielding 159 grams of gold per tonne and a 3m section yielding 91 grams/tonne. There are currently eight rigs operational in the area and testing continues, providing the opportunity for further positive updates in the near future. Gervaise Heddle, CEO of Greatland Gold plc, commented on the results: “We are delighted by this sixth consecutive set of excellent results from Newcrest’s drilling campaign, which continue to demonstrate the continuity of high-grade mineralisation and expand the mineralised footprint.” “These latest results represent one of the best sets of drilling results at Havieron since Newcrest began its exploration campaign and reinforce the potential to accelerate the timetable for commercial production.” Since the update Greatland Gold has pulled back from the recent high of 5.68p but equity analysts remain positive in the shares. “I would suggest investors use the recent pullback to pick up the shares,” said John Woolfitt, Director of Trading at Atlantic Capital Markets.JLEN reaffirms dividend

JLEN (LON:JLEN), the diversified renewable infrastructure investment trust, has reaffirmed its dividend in the face of uncertainty created by the spread of coronavirus.

The trust said it was committed to paying its quarterly dividend of 1.655p and guided on a full year dividend of 6.66p. With shares trading around 106p, JLEN provides a yield of 6.2%.

The news will increase investor confidence in the JLEN dividend as scores of Bluechip FTSE 100 companies scrap or reduce their dividends in an effort to conserve cash during the decline in economic activity caused by coronavirus.

No material long-term impact

JLEN operate a portfolio of renewable energy assets including wind, solar, hydro and biomass in the UK and is a strong financial position having just completed a placing and is conservatively geared through a revolving credit facility which isn’t due to refinanced until 2022. Although they are conscious of COVID-19, their operations have remained largely unaffected by the spread of the virus. The investment trust said in a release they saw no material long-term impact from COVID-19 on its ability to continue to meet their investment objectives. In the short-term, it is expected JLEN will experience lower power prices as demand drops inline with economic activity, but this isn’t expect to cause significant disruption to operations. JLEN have price floor or fixed price arrangements for summer 2020 and winter 2020/2021 for 49% and 48% of their power generation respectively. The has seen an impact to it’s food waste projects that are reliant on commercial waste food which has seen a reduction in collections. Residential food collections are said to remain stable. The food waste business makes up less than 5% of the JLEN portfolio. The company said it will monitor COVID-19 developments closely but the health and safety of all employees, stakeholders and their staff is of primary importance. JLEN (LON:JLEN) shares traded at 106p in early trade on Thursday.Remote opportunities for cyber security firm ECSC

Cyber security is a growth area and the expansion of remote working due to COVID-19 is likely to highlight its importance. AIM-quoted ECSC (LON: ECSC) is set to benefit. ECSC is still losing money, albeit a reduced amount, but it has started to generate cash.

ECSC provides cyber consulting services to organisations and businesses. Some of these clients then become managed services customers, although some sign up for managed services even though they have not received consultancy.

ECSC is an interesting comparison with Novacyt (LON: NCYT) because the share price soared on the back of high-profile cyber security events and was approaching £6 at one point. The valuation was not sustainable, and the share price has not been near those levels since. Novacyt is selling tests, but the short-term boost is unlikely to be sustained and it will be difficult to justify the valuation even if it is. However, there is underlying growth.

Cyber growth

Cyber security is not something that will go away. The UK market is estimated to be worth £8.3bn and it continues to grow at around 9% a year. In 2019, ECSC revenues grew by 10% to £5.91m. Managed services revenues increased by 48% to £2.61m. Consulting revenues dipped slightly to £2.9m, although they did grow in the second half. The other revenues come from third party products and other services. There are more than 100 reseller partners and these generated 17% of new clients during the year. This partner programme enables ECSC to engage with a broader range of clients. The reported pre-tax loss declined from £1.26m to £750,000. Operating costs were maintained so most of the growth in revenues dropped through to profit. Managed services has additional capacity and as more work is won its margins are set to continue to rise. Gross margins were 68% in 2019, up from 53% the year before. Cash was generated in the second half. This offset the outflow in the first half. There was an inflow from operations of £52,000 with a further boost of £152,000 from a tax credit. There was a £634,000 operating cash outflow in 2018. Capitalised AI software development costs and other capital investment meant that cash did fall from £650,000 to £351,000, although that is an increase on the June 2019 figure. The order book was worth £2.6m at the end of 2019 and since then two three-year managed services contracts that are worth £590,000 have been won from a charity and a high street retailer. There are tax losses of £5.67m, so future profit should be covered for many years.Future

There are opportunities and challenges for the business during this period of uncertainty. Higher levels of remote working are likely to unearth problems with many organisations’ cyber security and the ECSC rapid response operation could benefit. However, longer-term decisions may be put on hold and delay new contracts, particularly in consultancy. ECSC hopes to breakeven during the COVID-19 outbreak. Forecasts are impossible for any company at the moment. ECSC has made a strong start to 2019 with a 9% increase in revenues, though, and it has cash in the bank and debt facilities of £500,000. That, and £2m of recurring revenues, means that it will be able to withstand a limited slowdown. This year’s figures may not end up as would have been hoped for – a pre-tax profit was expected for 2020 before forecasts were withdrawn. However, the underlying trend in the cyber security market will continue and ECSC will be able to progress towards a pre-tax profit even if it is not this year. Looking at a long-term graph of the share price will not provide an accurate view of the progress made by ECSC. The share price has risen 5p to 82.5p on the back of the results, compared with a low of 62.5p. This is a growing business and the increased remote working due to COVID-19 will make it clear to businesses and organisations just how crucial cyber security is to them.Talks between airlines and government “ongoing”

The British Airline Pilots Association (BALPA) released a statement on Wednesday concerning talks between airlines and the government as the COVID-19 outbreak escalates.

“Talks are ongoing with airlines and the Government to look at how best to support the aviation industry though the current coronavirus crisis,” the BALPA said in a statement.

It continued to add that claims that the government is not going to support the aviation industry are “misleading”.

Instead, the BALPA emphasised that discussions concerning unique measures for individual airlines are “ongoing”.

The aviation industry is one to have been hit particularly hard in recent weeks as many countries have imposed travel restrictions in order to contain the spread of the illness.

Italy, Europe’s worst-affected country, was put on lockdown two weeks ago.

This lead to Ryanair (LON:RYA) lowering its passenger target for 2020 as flights to and from Italy were suspended.

Last week, Ryanair noted that “Italy, Malta, Hungary, Czech Republic, Slovakia, Austria, Greece, Morocco, Spain, Portugal, Denmark, Poland, Norway and Cyprus have imposed flight bans of varying degrees”.

With travel bans of this scale occurring, it is no wonder the aviation industry has been hit particularly hard by the spread of the illness.

Elsewhere in the industry, Flybe (LON:FLYB) collapsed, with the immediate crash of the airline blamed on COVID-19 related impacts.

“I’ve said before that there is no ‘one size fits all’ solution, due to the different structures and needs of each airline,” the BALPA General Secretary, Brian Strutton, said.

“Each airline will need to be reviewed to ensure a good use of taxpayers money. The Government will be looking at areas such as the airline’s financial state, whether it could raise the cash in other ways, or if it’s crucial to the UK transport system. These deliberations still are ongoing so we should await the outcomes,” Brian Strutton added.

UK average house prices grow 1.3% in January

New data on Wednesday from the Office for National Statistics revealed that house prices grew at a slower rate in January.

Average house prices in Britain rose by 1.3% over the year to January 2020, down from the 1.7% growth seen in December 2019.

The data from the Office for National Statistics is before the COVID-19 outbreak began in the UK.

Since then, the outbreak has developed significantly in the UK, with the government accelerating measures to help contain the spread of the illness.

Earlier this week, Boris Johnson addressed the nation and delivered strict social distancing rules to ensure people stay at home.

However, before the situation escalated, average house prices increased in England to £247,000, Wales to £162,000, Scotland to £152,000 and Northern Ireland to £140,000, the Office for National Statistics said.

House prices in London continue to be the most expensive, averaging at £477,000.

“Over the past three years, there has been a general slowdown in UK house price growth, driven mainly by a slowdown in the south and east of England,” the Office for National Statistics said.

Commenting on the COVID-19 outbreak, the Office for National Statistics added: “During the coronavirus (COVID-19) outbreak, we are working to ensure that we continue to publish the UK HPI. The price collection for this publication has been largely unaffected.”

“As this situation evolves, we are developing several solutions to meet potential scenarios depending on the amount of data that is able to be collected by our data suppliers to ensure we are still able to produce the publication over the coming months,” it added.