Rishi Sunak – Boris Johnson’s crown jewel or dagger in the back?

Rishi Sunak, a young and charismatic Chancellor, and one of the few members of the government to see their stock rise during the Coronavirus crisis. But why should we be interested in Mr Sunak, and more importantly, should we get used to seeing him on our TV screens?

After six years in politics, he moved into 11 Downing Street and within a few high-profile appearances, cemented himself as a formidable figure on the political mainstage.

Why Asia has yet to embrace sustainable investment, and why it should

Sustainable Investment, defined by the Forum for Sustainable and Responsible Investment as “an investment discipline that considers environmental, social and corporate governance (ESG) criteria to generate long-term competitive financial returns and positive societal impact”, is a rapidly growing industry.

A Financial Times article published earlier this year revealed that “$17.5tn out of the $79tn of total assets under management globally are invested in funds applying environmental, social and governance criteria”. An encouraging figure, perhaps, but one which distorts a canyon of regional disparity in the commitment to environmentally and socially sustainable investment.

The same article reported that a mere 5% of East Asian management assets are currently invested in sustainable projects, compared with almost 30% in the USA and Canada.

While the breadth of the discrepancy may come as a shock, it is in keeping with a decades-long trend within the Asian economy: to put the quest towards economic development first, even at the expense of glaring environmental and social consequences. The result is the staggering rate of pollution and worsening inequality across the Asian continent.

A continent of extremes

A 2019 Greenpeace report concluded that, out of the 100 most polluted cities in the world, 99 were in Asia. In particular, India and China were found to be the worst perpetrators, with the air in the city of Gurgaon – Southwest of New Delhi – containing more than 13 times the World Health Organisation’s (WHO) air quality guideline. Beyond the immediate environmental concerns, Asia is facing a worsening income inequality crisis. A 2017 Oxfam report demonstrated how the continent has become a magnet for economic extremes, with 4 of the world’s 5 most expensive cities residing in Asia, despite a widening wealth gap – aggravated by wage disparity and inconsistent access to education. Yet, Southeast Asia remains a huge market for sustainable investing opportunities. According to the Global Impact Investing Network, nearly a third of all sustainable investment ventures are based in the region, with 44% of companies intending to expand their projects in Asia over the next few years. And that is chiefly because Asia represents a monumental opportunity for companies interested in sustainable investment enterprise; not only is there a growing demand for practical solutions to worsening socio-economic crises – not least including the dire need to tackle pollution and income inequality – but there is a shifting emphasis towards self-sufficiency, both from a political and environmental perspective. The impact of climate change means that many natural resources are already, or will soon, become increasingly scarce and exponentially more expensive. The incentive to prioritise investment in projects which produce a positive socio-environmental impact grows ever greater, not just from an ethical standpoint, but as a practical necessity in a world on the brink of a climate crisis.Appetite for sustainable projects

Politically speaking, the trend towards self-sustainability is one which has slowly come to the forefront of global affairs in recent years, most notably in China. In 2017, the economic superpower announced a $300 billion plan to become self-sufficient by 2025, citing a desire to reduce dependence on foreign imports in the wake of a dramatic rise in domestic demand and a typically volatile international market. Moving forwards, we can perhaps expect to see more Asian businesses following the example of large cap players such as Morgan Stanley and Citigroup, seeking out investment ventures not just on an ethical basis, but as an increasingly attractive move to capitalise on the growing demand for practical solutions to social and environmental issues. That being said, sustainable investment has taken some time to gain traction in Asia, and in its very nature appears to go against the characteristically short-term approach that Asian investors have historically taken. As Curtis Chin wrote in the Financial Times, “the perception of ESG as a gospel preached by well-meaning but interfering non-government organisations has a strong hold in a region where many countries have understandably been focused on rapid economic development”. This dizzying climb towards economic growth has benefitted from the more laissez-faire approach taken by a number of Asian countries – most notably in the region of Hong Kong, which was rated top of the list of the most economically free countries in the world in a 2019 Investopedia report – but the integration of ESG legislation from various non-governmental organisations has been relatively coldly received in some parts of Asia, being frankly low on the “list of priorities”.A new beginning?

However, the tide is beginning to turn. The model which Asian businesses are only really just beginning to consider is one which places sustainability at its core, investing in projects that revolve around a positive ESG impact. In 2019, Japan announced that one of its largest banks would be reversing its commitment to coal-fired power generating schemes, and the number of Chinese companies signed up to the United Nation’s Principles for Responsible Investment tripled between 2017 and 2018. So, evidently, Asia has already started to consider sustainable investment, but it has only just dipped its toes into a vast lake of fiscal opportunity. There is still much work to be done in shifting a long-held suspicion, as well as a considerable degree of apathy, towards sustainability projects. The GIIN cited, in particular, “regulators’ unfamiliarity with impact investing” as an obstacle to the growth of the market in Asia, resulting in “complex, inefficient, and restrictive policies or the absence of enabling policies”. Certainly, there is a lack of regulatory framework for sustainable investment projects on the continent, but this is largely because sustainability is a relatively novel concept in business terms, and the legislation simply hasn’t had a chance to catch up. There is some improvement being made in terms of regulations, however, with Hong Kong’s Securities and Futures Commission making it mandatory for all its listed companies to disclose their sustainability credentials – and, from the start of 2020, mainland China has also committed to implementing a similar strategy.A pivotal opportunity

At the turn of the decade, Asia is faced with a pivotal opportunity to change its approach to sustainability, and to put environmentally and socially beneficial projects at the core of its rapidly evolving economy. There is a visible appetite for it too, with a vast population struggling with stark income inequality and the reality of the ever-encroaching dangers posed by climate change. On a continent ravaged by “the worst health crisis of a generation”, the demand for investments that focus on people as well as on money has never been greater. All that remains is for the Asian economy to shift its focus from short-term, high-yield rewards, to a more durable model based on sustainable investment and putting the future before the present. By removing the hindrance of the widespread lack of familiarity and understanding of sustainable investment, and by challenging the deeply-embedded tendency towards short-term profit at the expense of long-term demand, Asia could well blossom into a leading example of how an economy can be recalibrated to give, and not just take.Global equities recovery ran out of steam before the final bell

If you ever wished to see an underwhelming arc, you need only look as far as the performance of global equities on Friday. After a horrific Thursday session, indices had an excited start on Friday, before running out of steam in the afternoon and settling fractionally above where they began.

Speaking on the optimistic opening, Spreadex Financial Analyst Connor Campbell commented,

“There was little reason behind Friday’s gains, beyond investors deciding that the severe losses of the last few days provide a handy entry point to a market that had gone on a hell of a run at the start of the month.”

The FTSE, for instance, rose 1.1% to over 6,150 points, despite the news that the UK economy had contracted by 20.4% in April. Similarly, the DAX added 75 points and the CAC bounced by 1.7%, both in spite of industrial production falling by 17.1% in April.As UK trading entered the final knocking of the week, however, the FTSE was down to a 0.048% rally, to under 6,080 points. Similarly in other equities, the CAC revised its gains down to 0.60%, while the DAX ended up dipping by 13 points. Finally, after recovering to over 25,900 points, the DOW Jones sits at 25,350 points (up from its 25,100 point nadir) as UK traders go home for the weekend.

This evening could offer some consolation, though, with some pundits predicting a 600 point bounce when the bell rings on Wall Street.Similarly, “In terms of data, US import prices are set to rise from -2.6% to 0.6% month-on-month, while the preliminary consumer sentiment reading from the University of Michigan is expected to jump from 72.3 to 75.0.” adds Connor Campbell. So there are some glimmers of positivity for global equities, as we wrap up for the week.

Government considers ending support for overseas fossil fuel projects

The UK government is reportedly assessing its ongoing commitment to financially support overseas fossil fuels after it emerged that £3.5 billion of public funds has been spent on polluting operations since the Paris climate agreement came into effect in 2016.

It is understood that senior civil servants are considering a new climate strategy with the aim of “phasing out” financial support for oil and gas infrastructure in developing nations. The news comes amid the announcement that the COP26 climate summit – originally scheduled to be held in Glasgow this November – is set to be postponed until 2021 due to the coronavirus pandemic.

Global Witness, a prominent NGO campaigning to end fossil fuel operations, has accused the UK government of “rank hypocrisy” in a complaint to the Organisation for Economic Cooperation and Development (OECD).

Despite the government’s commitment to the climate pact, credit agency UK Export Finance (UKEF) has allegedly offered loans, guarantees and insurance totalling £3 billion to British companies involved in fossil fuel projects, according to a report by Global Justice Now.

The report also outlines that the total value of fossil fuel shares on the London Stock Exchange stands at a whopping £900 billion – higher than the GDP of the whole of Sub-Saharan Africa.

Climate activist for Global Justice Now, Daniel Willis, called for the government to reassess its commitment to overseas fossil fuel operations:

“For the government to show real climate leadership ahead of COP26 and support a global green recovery from Covid-19, it needs to end these highly damaging investments”.

A spokesperson for the UKEF commented on the matter, stating the company is “proactively developing the breadth of [its] support for renewable sectors” and added that it has already allocated £2 billion towards clean growth and renewable energy projects.

In a piece for The Guardian earlier this year, Labour leader Keir Starmer urged “let’s fight for a green new deal now” and explained how the UK government should be shifting its priorities:

“Rather than funding fossil fuel projects abroad, we should use our development budget and technical expertise to help other countries skip our bad habits and grow their own low-carbon economies on renewables instead”.

A spokesperson for the Department of International Development said the UK government has agreed that “all future aid spend will be aligned with the Paris agreement” and will continue its commitment to helping developing nations tackle climate change.

Drax Group extends its £125 million ESG facility to 2025

British power company Drax Group (LON:DRX) today announced that it had successfully completed a three-year-long extension to its Environmental, Social and Governance facility, with the contractual final maturity now pushed back to 2025.

Drax is known for championing ethical alternatives, having become the first coal-run power station company to invest in flue gas desulphurization technology back in 1988. Today, the company – between its subsidiaries – runs the largest biomass-fuelled power station in Europe, the UK’s largest decarbonisation project, and supplies between 7-8% of the country’s electricity supply.

The ESG facility that was extended on Friday will extend the profile of Drax’s existing facilities, and includes maturities to 2029. The facility adjusts the rate of interest Drax pays on its carbon emissions against an annual benchmark, which the company says reflects its commitment to reducing its emissions and becoming carbon negative by 2030.

It finished by saying that its all-in interest rate during the first year of the extended facility would be less than 2%, and that its overall cost of debt would be lower than 4% p/a.

Following the update, Drax shares rallied modestly by 0.75% or 1.60p, to 215.40p per share 12/06/20 15:52 BST. The company has a p/e ratio of 7.15 and a very generous dividend yield of 7.24%. JP Morgan analysts reiterated their ‘Overweight’ stance in May, stating that the company’s shares were under-priced and oversold due to the adverse effects of Coronavirus on energy prices.

Bakkavor sales steadily increase after Coronavirus challenges

UK fresh food provider Bakkavor plc (LON:BAKK) issued a tentative update at the end of the week, stating that its sales were stable, and were even beginning to improve.

The company said that its Chinese business had been ‘severely’ impacted by Coronavirus in January, while a positive start to the year in its UK and US operations was blighted by a sharp dip in sales volumes between March and April.

Since then, Bakkavor said that it had seen early signs of recovery, with sales having stabilised in all three regions. Despite this, the company’s like-for-like revenue was down by 5% year-on-year, for the five months to the end of May.

The company spoke on its UK operations, saying that its like-for-like revenues were down on-year by 19% in April and 13% in May, with its salad and ‘food-to-go’ offering being the hardest hit. It said, however, that it had seen a gradual increase in demand for these products, and that it would work to expand ranges it had simplified at the start of the outbreak.

Regarding its overseas operations, Bakkavor said it had adjusted its US offerings to accommodate lower demand, and that these measures had helped it to mitigate against the worst of the financial fallout. In China, the company said that the lifting of restrictions has allowed restaurants and stores to open, which will allow the Group to resume regular service.

Bakkavor weathers the storm

Speaking on the company’s prudence and flexibility, Chief Executive Agust Gudmundsson commented,“I would once again like to express my thanks to all of my Bakkavor colleagues, who are working tirelessly to help keep supermarket shelves well stocked. I am hugely grateful for their support and extremely proud of their commitment and determination during these difficult times . We continue to make their health, safety and wellbeing our foremost priority, and have been working in close cooperation with the various regulatory bodies, our colleague representatives and the unions to maintain a safe working environment for all our stakeholders.”

“In the UK, consumer behaviours continue to adjust, and while it will take time for sales to return, I have been encouraged by the recent increase in volumes. Current events have also reinforced my confidence in the vital role we play in partnering with our customers to deliver the fresh, healthy and convenient food that consumers look for every day.”

“In the US and China, both businesses have managed incredibly well through the turmoil, and we continue to support our customers as they reopen their stores and restaurants.”

Investor insights

Following a careful but positive Coronavirus trading update, Bakkavor shares rallied 2.28% or 1.80p, to 80.60p per share 15:08 BST 12/06/20. The company’s p/e ratio is 6.20, their dividend yield stands at a generous 5.01%.UK economy shrinks record 20.4% in April

The UK economy nosedived 20.4% in April 2020 in the largest monthly fall since records began, according to the Office for National Statistics (ONS). The report described the impact of the coronavirus pandemic as a “significant shock” to the economy, citing the dramatic fall in GDP and “record broad-based falls in output for production, services and construction”.

Analysis collated from more than 15,000 businesses for the ONS’s Monthly Business Survey showcased the extensive and almost indiscriminate impact that lockdown and social distancing measures have had on the UK economy. With wide-ranging business and factory closures, and a sharp decline in consumer demand, the vast majority of British companies have had to resort to unprecedented action in order to stay afloat.

The April contraction is three times greater than the decline seen during the entirety of the 2008 to 2009 recession. At its peak in between February 2008 and March 2009, GDP contracted by 6.9%. This year’s GDP contraction of 20.4% between March and April represents a fall equivalent to £30 billion in Gross Value Added.

On the bright side, analysts have suggested that April is likely to be the worst month as lockdown measures have been incrementally eased from May onwards to allow economies to open back up.

Alastair George, the leading investment strategist for Edison Group, commented on the significance of the findings,

“This is a truly historic rate of GDP contraction but not a surprise. The risk has been that central banks have almost been too effective in supporting markets, masking the economic cost of lockdowns as well as dimming employment and training prospects for younger people less at risk from COVID-19. These will be important figures to frame the debate on the government’s lockdown policy for the remainder of the year”.

UK Prime Minister Boris Johnson also added his insight, stating he was “not surprised” by the ONS figures:

“We’ve always been in no doubt this was going to be a very serious public health crisis but also have big, big economic knock-on effects. The UK is heavily dependent on services, we’re a dynamic creative economy, we depend so much on human contact. We have been very badly hit by this.”

The news comes in light of reports that the number of Brits claiming unemployment benefit soared to 2.1 million during April, a jump of more than 856,000 on the previous month as the full impact of the lockdown set in.

JP Morgan Brazil Investment Trust provides exposure to economic recovery in Latin America

JP Morgan Brazil Investment Trust stands out as a recovery play to the global coronavirus recession with exposure to Brazil’s domestic market, and companies operating on the global stage.

Brazil has recorded the second highest number of coronavirus cases globally, as well as the third highest number of deaths.

Sadly, as with many other countries, the true number is likely to be a lot higher.

The government of Brazil was one of the administrations that failed to act quickly with lockdown measures as the Brazilian president pointed to the possible deaths associated with economic deteriorated as a result of coronavirus economic shutdown.

“Are people dying? Oh, yeah. And I feel for them. I feel for them. But there will be more people dying, many many more, if the economy is destroyed by these lockdown measures imposed by governors,” said Brazil’s President Jair Bolsonaro.

The Presidents decision to prioritise the economy over coronavirus was met with condemnation and the ratings agency Fitch still predicts the economy will fall 6% in 2020.

However a 6% drop is still significantly better than the 11.5% drop the OECD predicts the UK will shrink in 2020. Brazil has roughly the same number of deaths recorded from coronavirus as the UK.

The Brazilian economy has also been dogged by the disappointment over the failure of the government to deliver on promises of economic growth, despite massive spending and borrowing.

The Brazilian government is proving incredibly unpopular with prior failings and approach to tackling COVID-19, and investors have made there feelings heard.

Despite these hurdles, over time, the virus will be brought under control, and the government will either be replaced or push on with its pro economy agenda.

It would actually be hard for sentiment around Brazil to get much worse.

Coronavirus has caused disruption to Brazils financial assets, but the underlying demographics and natural resources of Brazil remain.

With this in mind, any further weakness in JP Morgan Brazil Investment Trust could provide an attractive opportunity with a long term view that the situation in Brazil improves.

The trust is highly cyclical in it’s composition with the top ten holdings dominated by natural resources, financials and industrials.

Diversified miner Vale accounts for 10% of the trust and is poised to benefit from a global economic recovery and higher demand for commodities.

In addition, the financials will facilitate the economic recovery as well as being beneficiaries of it.

The trust trades at a significant 17% discount to NAV which represents negative sentiment to Brazil in the market and offers the opportunity for appreciation in the price as sentiment approves.

With this in mind, any further weakness in JP Morgan Brazil Investment Trust could provide an attractive opportunity with a long term view that the situation in Brazil improves.

The trust is highly cyclical in it’s composition with the top ten holdings dominated by natural resources, financials and industrials.

Diversified miner Vale accounts for 10% of the trust and is poised to benefit from a global economic recovery and higher demand for commodities.

In addition, the financials will facilitate the economic recovery as well as being beneficiaries of it.

The trust trades at a significant 17% discount to NAV which represents negative sentiment to Brazil in the market and offers the opportunity for appreciation in the price as sentiment approves.

With this in mind, any further weakness in JP Morgan Brazil Investment Trust could provide an attractive opportunity with a long term view that the situation in Brazil improves.

The trust is highly cyclical in it’s composition with the top ten holdings dominated by natural resources, financials and industrials.

Diversified miner Vale accounts for 10% of the trust and is poised to benefit from a global economic recovery and higher demand for commodities.

In addition, the financials will facilitate the economic recovery as well as being beneficiaries of it.

The trust trades at a significant 17% discount to NAV which represents negative sentiment to Brazil in the market and offers the opportunity for appreciation in the price as sentiment approves.

With this in mind, any further weakness in JP Morgan Brazil Investment Trust could provide an attractive opportunity with a long term view that the situation in Brazil improves.

The trust is highly cyclical in it’s composition with the top ten holdings dominated by natural resources, financials and industrials.

Diversified miner Vale accounts for 10% of the trust and is poised to benefit from a global economic recovery and higher demand for commodities.

In addition, the financials will facilitate the economic recovery as well as being beneficiaries of it.

The trust trades at a significant 17% discount to NAV which represents negative sentiment to Brazil in the market and offers the opportunity for appreciation in the price as sentiment approves. Morrisons: 35pc shareholders oppose executive pay policy

Over a third of investors have voted against Morrison’s pay policy at a shareholders meeting on Thursday.

Almost 35% of the votes cast were against the current pension deals for the chief executive, David Potts, and the chief operating officer, Trevor Strain.

Whilst the UK corporate governance code suggests that pension contributions should be in line across an entire company, shop floor staff at the supermarket receive 5% whilst Potts and Strain’s bank payments are worth 24% of their basic salaries.

“Although the policy vote passed, and we received considerable positive feedback during consultation, the board acknowledges a number of shareholders decided to vote against the policy,” said a spokesperson from Morrisons.

“Kevin Havelock (chair of the remuneration committee), on behalf of the board, will therefore continue to engage with shareholders and will report in due course on the outcome of those discussions.”

The AGM took place virtually to adhere to social distancing rules.

Earlier this week, Potts celebrated his supermarket staff and their efforts during the pandemic.

“All our colleagues have been putting their bodies on the line every day going to meet members of the public. One purpose has galvanised over 100,000 people – to serve people of Britain. We provide the most important thing outside of public health,” he told the Guardian.

Shares in the supermarket (LON: MRW) are trading at 184.45 (1222GMT).

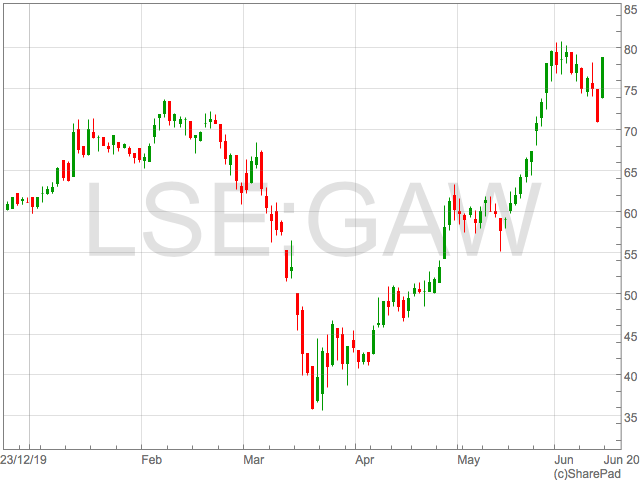

Games Workshop bounces back with better than expected sales during COVID-19

Games Workshop shares (LON:GAW) surged on Friday after the group unveiled robust activity during the coronavirus lockdown.

The UK Investor Magazine previously highlighted Games Workshop as one of the hobbyist companies that would benefit from the coronavirus lockdown as model makers took advantage of spending more time indoors.

On Friday, this was confirmed when the Games Workshop made a sharp revision to their pretax profit for the year to 31st May 2020.

Games Workshop shares were over 10% higher to 7,855p on Friday and are 28% stronger year-to-date.

In April, Games Workshop released a trading statement guiding for pre-tax profit of £70 million. Today’s announcement said pretax profit would be no less than £85 million, signalling elevated sales during the coronavirus lockdown.

Revenue for the year to 31st May 2020 will be circa £270 million, substantially ahead of 2019’s £256m.

Games Workshop said they had opened 306 of their 532 stores across 20 countries whilst adhering to local social distancing.

“Following our announcement on 28 April 2020 we have continued to re-open our operations globally, in line with local guidance, whilst ensuring our priority is the health, safety and wellbeing of our staff and customers,” Games Workshop said in a statement.

“Our warehouses are now operational and our factory is working in a limited capacity, at all times complying with the social distancing and hygiene requirements in each country. Trade and online sales orders are also being processed as these staff currently work from home.”

Games Workshop produces ‘Warhammer’ models that can be used in war games and are commonly referred to as ‘plastic crack’ due to the pull the products have on enthusiasts as they seek to expand their collection and compete in competitions.

Many of the products on the Games Workshop were out of stock for a period at the start of the lockdown, and although there were initial concerns over Games Workshop being able keep production facilities open to fulfil demand, this seems to have been navigated with some success.

Game Workshop also has a strong digital product that represented roughly 20% of sales in 2019, which is likely to have seen greater activity through lockdown.