Goldentree Asset, Avenue Capital and Goldman Sachs (LON:GS) owned hotel chain Travelodge, has, like many, been near the eye of the storm during the Coronavirus lockdown, with regular trading all but flat-lining. What sets it apart from its hotel counterparts, though, is that its future may be equally problematic.

The staycation renaissance may not be enough

With outlets dotted all across the UK, you’d think Travelodge would be in a prime position to capture a lot of the demand for impromptu weekend getaways, and in some ways that’s true.

With sites dotted along key tourist destinations such as the South Coast, the Lake District and Loch Lomond and the Trossachs, Travelodge are well-placed to meet the needs of a lot of Brits looking to claw back some semblance of a summer holiday, as restrictions continue to be lifted at a gradual pace.

What isn’t so good is the density of Travelodge sites in inner city areas. As stated by Premier Inn owners Whitbread (LON:WTB) in their announcement earlier in July:

“It is still very early days and therefore too early to draw any conclusions from our booking trajectory, especially as there has been volatility in hotel performance in other countries that relaxed controls before the UK. However, in traditional regional tourist destinations, we are seeing good demand for the summer months, whilst the rest of the regions and metropolitan areas, including London, remain subdued.”

The issue here is that alongside their hotels across a wide range of popular tourist destinations, Travelodge has large clusters of hotels in cities such as London, Manchester, Leicester and Liverpool. These sites, while they may see activity gradually increase in the next couple of months, will under-perform because their core customer base has not gotten back to normal.

These hotels, we might assume, rely primarily on a mixture of tourists and business people. The former group will be diminished, as domestic tourists are still conscious of going to crowded metropolitan areas, and international tourists are only starting to benefit from loosening restrictions. The latter group – business people – are acting in a diminished capacity, with many companies not yet bringing their employees back to the office, with fewer still asking their employees to travel long-distance.

Goodnight Travelodge

The second, and far bigger reason for concern, though, is the news reported by the Telegraph that the company are to lose ‘dozens’ of its landlords, who intend to launch a rival hotel chain named ‘Goodnight’.

The Goodnight chain is expected to be formally announced later on Friday, with its official launch being the 1 January 2021. The news follows rows between hotel landlords and Travelodge’s hedge fund owners over steep rent cuts, the likes of which also occurred in 2012 under a company restructuring.

Friday’s announcement will see 80 hotels sign new leases with the Goodnight brand, with one deal insider saying on the news:

“This has the potential to completely decimate their [Travelodge’s] business,”

The row began with the hotel chain owners withholding a quarterly rent bill that was due in March, and landlords have since responded, saying they feel as if the fund owners used the pandemic to secure more favourable terms.

Less sleep tight and more sleepless nights

Landlords have until mid-November to reject the rent proposals termed in the CVA.

For now, it looks as if the Travelodge V-shaped recovery may be somewhat modest in its trajectory. With its inner city offerings yet to pick up to pre-pandemic pace, and another rival – using a similar business model – entering the picture early next year, any long-term outlook should contain at-best tentative positivity.

Dyson is the latest company to announce a series of job losses amid the Coronavirus pandemic.

During a video conference on Thursday, the staff was told that 600 UK jobs and a further 300 worldwide roles would be cut.

“The Covid-19 crisis has accelerated changes in consumer behaviour and therefore requires changes in how we engage with our customers and how we sell our products,” said a spokesperson for the group.

“We are evolving our organisation and reflecting these changes to make us faster, more agile, and better able to grow sustainably.”

“These proposals would regrettably result in around 600 redundancies in the UK and 300 in the rest of the world. We are fully supporting those who are impacted, finding alternative roles where possible,” the spokesperson added.

Most of those affected by the job cuts will be staff in retail and customer service roles.

Whilst Dyson has not used the furlough scheme or relied on any public money during the pandemic, the group is owned by James Dyson’s, Britain’s wealthiest person. Dyson is worth over £16.2bn.

“There’s a lot of resentment that we are owned by the richest man in the UK but a temporary blip in sales has resulted in 900 job losses worldwide,” a source told the Guardian.

“His increase in wealth last year alone would be enough to make everyone [of the staff] in the UK affected a millionaire and he’d still have £3bn of it left over,” the source added.

Earlier this year during the pandemic, Dyson created the “ventilator challenge”, where it helped build medical ventilators in the aid to treat patients of the Coronavirus.

Shares at Anglo-Dutch conglomerate Unilever (LON:ULVR) have surged more than 8% on Thursday after the company reported better than expected figures as part of its H1 2020 results.

The consumer goods giant – which owns a number of household names, including Dove, Ben & Jerry’s and PG Tips – recorded a €25.7 billion turnover in the first half of 2020, falling just 1.6% year-on-year.

Underlying sales slipped just 0.3% in the three months leading up to 30 June, compared with market analysts’ predictions of 4.3% drop, while the company’s underlying operating margin rose to 19.8% from 19.3% in 2019.

Overcoming the cautious projections for H1 2020, Unilever pulled in a pre-tax profit of €4.5 billion – up from €4.3 billion in H1 2019.

A closer look

Analysts were expecting a much sharper drop in sales for the period between April to June, as worldwide lockdown measures stifled the retail sector and billions of people were confined to their homes in an effort to prevent the spread of coronavirus.

With the widespread closure of restaurants, cinemas and ‘non-essential’ stores, Unilever appears to have suffered from a drop in sales of hygiene products as millions were forced to work from home at the peak of the pandemic.

Beauty and personal care underlying sales fell by 0.3% as people abandoned offices for the comfort of their own homes. The company reported that global lockdowns led to a fall in demand for skin care, deodorants and hair care products.

Dove – Unilever’s largest beauty brand – nonetheless remained resilient with mid-single digit growth, as well as double-digit growth for Suave as the company increased its hand sanitiser production by more than 600% to keep up with greater demand for personal disinfectants.

Home cleaning products enjoyed a surge in sales during lockdown, with underlying sales up 3.2% as consumers flocked to purchase Cif and Domestos products to clean their homes and disinfect surfaces that may have been contaminated with coronavirus.

Teaming up with environmental health experts, Domestos helped to educate consumers on how to effectively cleanse surfaces to prevent the spread of infection, subsequently reporting ‘strong’ double-digit growth in H1.

Food and refreshment sales suffered the most, with underlying sales down 1.7%, with food service sales down 40% due to restaurant and eatery closures and out-of-home ice cream sales slipping 30% as the tourism industry ground to a halt.

However, household favourite brands Knorr and Hellman’s performed well with double-digit growth, while at-home ice cream consumption soared by 26% in Q2 – with Magnum and Ben & Jerry’s enjoying a surge in sales as both ‘continue to grow strongly’.

CEO statement

Unilever CEO Alan Jope released a statement alongside the company’s H1 results, saying:

“Performance during the first half has shown the true strength of Unilever. We have demonstrated the resilience of the business – in our portfolio, in a continued step-up in operational excellence, and in our financial position – and we have unlocked new levels of agility in responding to unprecedented fluctuations in demand.

“From the start of the Covid-19 crisis, we have been guided by clear priorities in line with our multi-stakeholder business model to protect our people, safeguard supply, respond to new patterns of consumer demand, preserve cash, and support our communities.

“Our focus for the rest of 2020 will continue to be volume led competitive growth, absolute profit and cash delivery as this is the best way to maximise shareholder value.

“I would like to thank every member of the Unilever team for the outstanding commitment they have shown in the most difficult of circumstances”.

Investor insight

The company’s optimistic results sent Unilever’s share price soaring by 8.55% or 370.00p to 4,700.00p at BST 13:38 23/07/20, finally gaining ground lost since shares first began to fall back in February.

Unilever’s dividend yield stands at 0.031%, with its P/E ratio at 24.16.

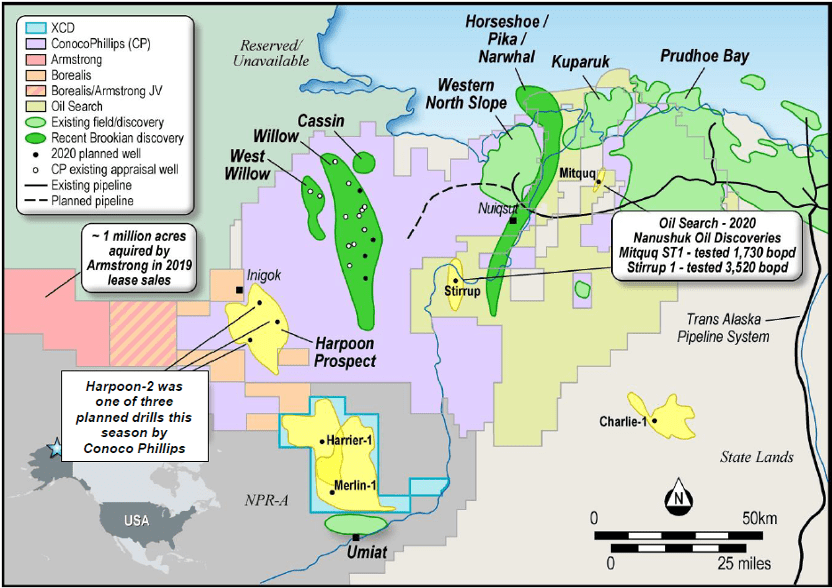

Alaska’s North Slope basin has a long history of successful oil discoveries — recent discoveries have included the two largest conventional oil discoveries onshore North America in over 40 years.

It is the location of North America’s largest current oil field, Prudhoe Bay, which originally contained over 25 billion barrels of oil. Furthermore, the basin is surrounded by several other large oilfields, having together produced over 17 billion barrels of oil since 1977 through the Trans Alaska Pipeline System.

Oil exploration junior, 88 Energy Ltd (AIM:88E | ASX:88E) has recently expanded its position on the North Slope, acquiring XCD Energy and its 135,000 acre Project Peregrine.

88 Energy now has net half a billion acres of exploration ground across multiple world class assets with multi-billion barrel discovery potential on the North Slope, with Peregrine joining Project Icewine and the Yukon Leases in 88 energy’s portfolio.

Project Peregrine

Project Peregrine comes with three onshore prospects already identified at the project — Merlin (Nanushuk), Harrier (Nanushuk), Harrier Deep (Torok).

Combined, these prospects have a mean unrisked recoverable prospective resource of 1.6 billion barrels of oil, as per an independent report generated by ERC Equipoise.

To the north and south of Project Peregrine sit major oil discoveries.

Willow, located to the north of Peregrine, is a 0.75 billion barrel discovery made by oil major ConocoPhillips (NYSE: COP).

A recent well drilled by ConocoPhillips, just 15 kilometres from Project Peregrine, encountered hydrocarbons at its Harpoon prospect which is interpreted to be directly on trend and analogous to the Harrier prospect at Peregrine.

The Peregrine Project also lies directly to the north of the Umiat oil accumulation that’s estimated to have greater than 1.0 billion barrels of oil in place.

Project Peregrine (blue) lease position relative to ConocoPhillips Harpoon Prospect and Willow Oil Field

2021 Drilling Planned

88 Energy intends to drill two, low cost wells to explore Project Peregrine in early 2021.

These wells will be testing the resource potential of Peregrine, with the aim of unlocking the next major oil discovery on the North Slope.

As 88 Energy currently holds 100% of the project, it intends to do a farm out deal with other partners that want exposure to near term upside.

The company will be undertaking low cost options for well drilling, estimating that the two wells will to cost ~US$15 million.

88 Energy has identified two primary prospects — Merlin and Harrier that total over 1 billion barrels, that it is intent on drilling in early 2021. Both prospects are located on trend to existing recent discoveries, with Harrier recently being de-risked by evidence of hydrocarbons at Conoco’s Harpoon-2 well.

Project Icewine

In addition to the newly acquired Project Peregrine, there remains significant opportunity and value at the company’s Project Icewine.

Despite a negative market overreaction to early results from the Charlie-1 well at Project Icewine earlier this year further investigations have been promising. These results were released amid ‘peak fear’ from the COVID-19 pandemic and faced a record low oil price environment.

However, 88 Energy views that sell off as an overreaction.

The company has just released sidewall core analysis using two different techniques. Both demonstrate that the primary targets — the Seabee and Torok Formations — are in fact, full of oil.

Reservoir modelling of stimulation of the formations is now underway to understand flow potential.

More lab data and news is to come from Charlie-1 and 88 Energy has identified a new preferred well location to test the conventional targets at Project Icewine — a location with better reservoir quality.

A farm-in partner is also being sought to further investigate Project Icewine in the search for flowing hydrocarbons.

All up, major upcoming activity includes the farm-out of Project Peregrine in the lead up to the drilling of two wells in early 2021, plus the integration of new results from the Charlie-1 well, and reinvigoration of the farm out process for Project Icewine.

Sponsored by 88 Energy

Vietnam is a high growth market situated in the heart of Asia. Its cohesive population of 100m people is young, hard-working and increasingly digitally connected. Over the last 30 years, Vietnam has experienced high levels of GDP growth, averaging about 6 to 7% and attracting record levels of Foreign Direct Investment (FDI) with almost USD 20 bn in 2019. It also is an increasingly open economy, with trade equivalent to 200% of GDP, and the government has negotiated a number of free trade agreements.

Vietnam is one of the original countries in what was formerly known as the Trans-Pacific Partnership TPP and is now the somewhat unpronounceable alphabet soup of the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CTCPP). In addition, Vietnam recently approved a bilateral EU free trade agreement, which could serve as a model for a new free trade agreement with the UK.

Perhaps more important than a static GDP number is the per capita GDP which has just recently passed USD 3,000, which is considered an inflection point in an emerging consumer society. For example, Thailand doubled its GDP from this point in seven years and China doubled its within five years.

V for Victory – against the coronavirus

Vietnam declared war on the coronavirus in late January and emerged victorious in containing it within about 90 days by the end of April. The government was very quick to react when the first cases were confirmed during the Lunar New Year (‘Tet’) holiday in January by imposing a large-scale quarantine, stopping flights to China, and implementing control and trace to identify outbreaks. It also employed all the tools in the ‘media’ armory to keep its citizens informed via social media, traditional media, as well as propaganda art.

Vietnam is in many ways a Confucian ‘East-Asian’ society, with strong community values, and an adherence to authority. Its social cohesion and the government’s effective response meant that Vietnam was one of the first countries to come out of lockdown at the end of April after a relatively short three-week lockdown. Since mid-April there have been no community spread cases, and remarkably, in a population of close to 100m people, there have been less than 400 infected cases in total and zero deaths. The closest someone came to death was a British pilot with Vietnam Airlines, the National Carrier, an unfortunate super-spreader which created a cluster of infections around a popular expat-bar in Ho Chi Minh City’s District Two.

He was in a coma and at death’s door for almost 100 days in an Intensive Care Unit in Vietnam. The Vietnamese people rallied around him, even offering him their own lungs, and he went on to make a complete and full recovery. He has now returned to his home city of Motherwell in the UK, saying that ‘I would have died’ if it were not for Vietnam.

V – Shaped recovery

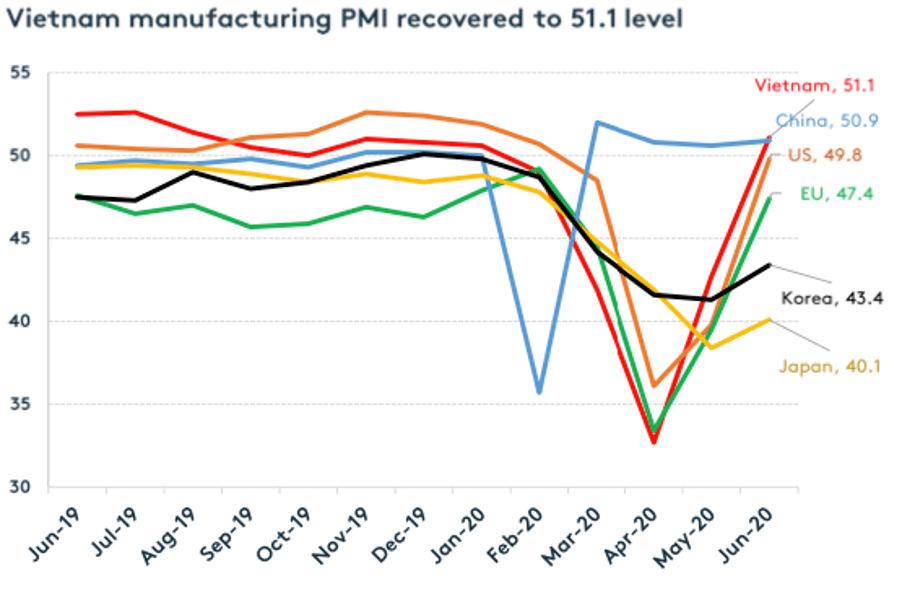

Vietnam has the potential to make a V-shape road to recovery post-pandemic. The Purchasing Managers Index (PMI) rose sharply from the depths of the pandemic, as the country gradually went back to work. Retail sales have also been rising, though some discretionary spending has been unsurprisingly delayed.

The GDP growth for the first six months of 2020 was 1.8%, and the full year is expected to be somewhere between 3% and 4%. This is lower than the 6-7% trend but is a rare positive number in a world of fearful negative growth forecasts.

Prospects for Vietnam will be strengthened as more manufacturers look to its proximity to key markets and abundant, well-educated and young workforce as a powerful source of production. Last year’s trade spat between the US and China accelerated a ‘China-plus-one’ strategy as supply chains are increasingly being broadened in an attempt to diversify risk and bend costs down. Vietnam has seen decades of strong FDI into the manufacturing sector and has enhanced its logistics and business-to-business (B2B) services to facilitate this growth.

Source: IHS Markit

A number of international companies started to relocate to Vietnam, and we see strong evidence of that trend continuing as Apple and other global brands look to increase what they make in Vietnam. That will also have a positive knock-on effect in the private sector. Other parts of ASEAN, Singapore and Thailand, adopted a Michael-Porter inspired ‘cluster’ approach to creating centres of specialized large-scale manufacturing in the 1980s and 1990s (e.g. hard disk drives in Singapore and Thailand, semiconductors in Singapore, and automotive component and finished vehicles in Thailand’s coastal Rayon region). This approach can lead to a localized supply chain of the master-supplier, an Apple or Samsung, for example, and then its myriad of sub-contractors. This notion has already attracted Samsung, which makes nearly every tablet and phone in Vietnam with close to 100,000 employees across the country and has accelerated the expansion of its industrial park.

In addition to the planned investment by the government into infrastructure (a total amount of USD 30 bn over the next few years), Vietnam’s private sector will also see increasing opportunities. The government recently passed a Private-Public-Partnership (PPP) to encourage private investment as a means to finance infrastructure. Unlike the UK where the government plans ‘brown-field’ rejuvenation of existing commercial and retail centres in an attempt to breathe life into hollowed-out sectors, much of the infrastructure development in Vietnam is in ‘green-field’ projects that are known to have a multiplier effect on economic growth.

After a few years of hibernation, the privatization of state-owned assets and enterprises will resume this year. The government is committed to selling off equity stakes in companies that become listed, or indeed privatizing businesses for the first time. One of the companies set for sale is the country’s largest brewer (and the world’s 20th largest brewer by volume) Sabeco (HOSE: SAB), which produces the popular Saigon and ‘333’ rice-brewed beers. Vietnam’s beer, and when served cold makes a great accompaniment to the fragrant flavours of Vietnam’s delicious noodles and spring rolls, as visiting celebrities like Obama and Bourdain have attested to.

Private capital in the form of private equity has also been growing rapidly over the past 15 years since the first major amendments of securities and enterprise laws were passed. In 2005, the new laws enabled different share classes, including preference shares, to be used in structuring private equity investments.

These structures can help bridge the gap of valuation expectations where capital is sought by selling a minority stake to an investor who can help grow the company. One such investment was in a private property company 15 years ago. This company went on to list on the stock exchange, the investor made a very handsome return on their investment, and the company went on to work with many other institutional investors, attracting hundreds of millions of foreign capital. The company, including its subsidiaries, is now worth about USD 30bn and accounts for around 20% of the local stock market.

Most importantly perhaps for UK investors, is the way in which the capital markets have grown and deepened. Daily liquidity across Vietnam’s stock markets is currently around USD 350m. This is more than the entire size of the market back when the UK’s Prudential (now Eastspring) was an early successful investor on behalf of its Vietnamese life insurance customers in the capital markets.

Vietnam Holding (LON: VNH) was established in 2006 and since 2009 has been an adopter of the UN’s Principles on Responsible Investing (UNPRI). Originally listed on the AIM market in 2019, the Investment Trust moved to the premium segment of the wider market. It now manages a concentrated portfolio of around 25 Vietnamese companies across three main themes: Industrialisation, Urbanisation and the Domestic Consumer. Over the last decade, VNH has backed many companies that have gone on to become significant well-known brands. Identifying good mid-cap companies takes patience and requires a local-on-the-ground presence.

VNH also thoroughly screens and engages with companies from an environmental, social and governance (ESG) perspective. Buying an index, or ETF, is another way to access the Vietnamese market, but gets you the good, the bad and the ugly.

VNH is able to invest across a spectrum of opportunities, from smaller private companies looking to list in a couple of years, through mid-cap companies growing at more than 20% per annum to the larger business opportunities with over USD 1 bn in market value (‘large cap’ stocks). Over the years, a number of small-to-mid cap stocks have enjoyed such impressive growth compounding that they are now in the ranks of the large-caps. VNH is approximately 65% invested in large caps and 35% in mid-caps, with an average company size of USD 500m. VNH typically holds up to 5% percent in a company and routinely engages with its management and boards on good governance, transparency, environmental impact and corporate social responsibility.

The CIO of Dynam Capital, Vu Quang Thing, co-founded the Vietnam Institute of Directors, and is an acknowledged authentic voice on board best practices and investor reporting and relations.

Although Vietnam has many of the characteristics of a more recognized ‘emerging market’ in part due to the size of the equity market already being above USD 160 bn, and with more than 1,500 companies to invest in, it is still classified by MSCI as a frontier market. In fact, this year Vietnam is likely to be the largest component of the Frontier Market Index. As a frontier market, it is estimated that only one in five emerging market investors are present: it will be a game changer in a few years if and when Vietnam is classified as an MSCI Emerging Market.

Vietnam has emerged from the covid-19 crisis as a winner. Its capital markets are set for expansion, the infrastructure is improving, and it will continue to attract interest from manufacturers and other types of companies looking to diversify away from China. Its macro-economic position is the envy of much of the world, and this could improve in a scenario where the US dollar weakens. Clearly the world as a whole is facing uncertainties, and there will be winners and losers ahead. Vietnam has signaled the ‘V’ for Victory sign against the devastating coronavirus, and this fast-growing country of 100m people is one to keep an eye out for in the months and years ahead.

Vietnam Holding Limited (LSE: VNH) can be purchased through your stockbroker, or wealth manager, and should be considered as a part of a diversified portolio for investors with a mid-to long-term investment horizon.

Author’s Note: the title ‘Viva Vietnam’ was first used by Standard Chartered Bank in 2003, when they correctly called the first growth cycle in Vietnam’s capital markets. I was working at Standard Chartered at the time and had successfully co-led an investment in a company that manufactured branded toiletries for the emerging consumer classes in south-east-Asia. They had a dominant position in the Malaysian market, a population of about 30m people, and a small but fast-growing business in Vietnam. During the due-diligence on the investment (which was a ‘home-run’ generating substantial gains), I was so taken by the incredible prospects that I moved my family to Vietnam for five years and helped Prudential invest across a wide-range of asset classes on behalf of its domestic customers.

The author of this article is Craig Martin, Chairman of Dynam capital (www.dynamcapital.com), a Guernsey regulated fund manager focused exclusively on the exciting opportunities in Vietnam. Dynam has a team of 12 Vietnamese professionals on the ground in Ho Chi Minh City.

Dynam is the Investment Manager for Vietnam Holding Limited (LON:VNH) an Investment Trust listed on the premium segment of the Main market of the London Stock Exchange.

See www.vietnamholding.com for more information.

Tesla (NASDAQ: TSLA) reported a $110m profit on Wednesday – the fourth consecutive income and a milestone for the carmaker.

Compared to the $408m last year, the net profit means there is the possibility of Tesla being considered for inclusion in the S&P 500.

In a statement, the group said: “Our business has shown strong resilience during these unprecedented times. Despite the closure of our main factory in Fremont for nearly half the quarter, we posted our fourth sequential GAAP profit in Q2 2020, while generating positive free cash flow of $418m.”

“We believe the progress we made in the first half of this year has positioned us for a successful second half of 2020. Production output of our existing facilities continues to improve to meet demand, and we are adding more capacity. Later this year, we will be building three factories on three continents simultaneously,” the group added.

The growth in profits is largely down to the opening of a new factory in China, where costs are heavily lower. The company is focused on growing and also announced new factories in Germany and Texas.

“I’ve never been more excited and optimistic about the future of Tesla in the history of the company,” said Elon Musk, the group’s controversial chief executive.

The group has seen a strong year, where this month it reported production of 90,650 vehicles in the second quarter – ahead of forecasts.

Shares in Tesla (NASDAQ: TSLA) jumped 5% following the news and have more than tripled over the course of the year, growing $430 to over $1,550.

One of the first things you’re taught in international relations class is the school of neorealism, which posits that the international system exists in a state of anarchy, with all states vying for the greatest share of power. Each state’s share of power is relative and determined by their distribution of capabilities – military, economic, natural resource, technological, demographic etc – and for our discussion of Trump, Brexit and trade deals, we’re most interested in the economic capabilities of each actor.

You see, apart from giving us uncomfortable reality checks, realism is also useful as a parsimonious explanation of complex dynamics. Whereas many would, perhaps rightly, complain that international relations involves complex and myriad considerations and analyses, realism plays a simpler game. It says, regardless of whether our nation’s proclivity is more towards being offensive or defensive, we all want security and prosperity, and each agent (nation-state) attempts to improve its capabilities relative to others – by increasing its economic growth, military strength, stake in resource extraction, technological and scientific innovation, and so on.

Why is this relevant for a Trump presidency?

Now it is worth noting that this zero-sum trend does not always play out. Indeed, over the last four decades, the West has typically favoured globalisation and complex supply chains. While these mechanisms have helped our more economically capable states (traditionally Western countries) to become more capable, as their citizens specialised more intensively in high-income sectors such as legal, financial and generally white-collar services, these changes have not negatively impacted the previously less capable states. In fact, relative changes in power dynamics have been in favour of many newly industrialising nations, with the economic and military development of countries such as China, India and Brazil among others far surpassing the relative development of Western nations during the same period.

This trend, it seemed, would occur perpetually, with China rising at such a rate that people began questioning the longevity of the US’s hegemony. This was, perhaps, revised over the last four years, with Donald Trump as president. Certainly, any fair analysis of Trump would not credit him with any revolutionary expansions in America’s capabilities. What he has done, however, is wobble the tracks of the Chinese boom train, with a combination of tariffs and rhetoric which have made it harder for the Chinese to supply the US – and its allies – with Chinese goods and services with the ease it became accustomed to.

This anti-Sino approach is just a small part of Trump’s pro-American protectionism, which, in fact, isn’t just disruptive for China, but anyone that’s not the US.

In this sense, Trump America is the twenty-first century vindication of realism. Realising that power is a matter not just of how much of each capability you have, but how much you have relative to everyone else, we can imagine the Trump approach to be one of maximising domestic benefits while minimising the benefits incurred by others.

And, putting yourself in the shoes of a US citizen who enjoys seeing their country as the biggest and baddest player in the game, you can see why the Trump approach might be appealing. Regarding economic capabilities, (for the sake of being simple, we’ll use GDP) US GDP has risen from $10.25 trillion in 2000, to 20.54 trillion in 2018. During the same period, Chinese GDP skyrocketed from $1.21 trillion, to $13.61 trillion. These trajectories, save for US efforts to slam the brakes on everybody’s perpetual growth, would have seen it unseated as the unitary global hegemon. However, we now know that the US is willing to not play nice in order to keep its throne, and this should be concerning for relatively small fry who rely on its mercy, such as the UK.

Brexit Britain: small fish in a pond with big fish

Likely not much surprise to anyone, but when compared to the US, the UK is a bit of a tiddler. Militarily, we are comparatively miniscule; technologically, we produce a fraction of the patents and are home to far fewer tech giants; we rely on US strength for our resource security; and economically, we are little over a tenth of the size of the US, with a 2018 GDP of $2.8 trillion.

Now, in a situation where the US has a relatively benign leader, keen on preserving the ‘special relationship’, a lonely Britain knocking on the door and asking for fair treatment would be less of a problem. Sadly, that is not the case.

Trump, as we have discussed, is unreserved in putting US interests first, and he makes no exception when dealing with the UK. He knows that we need a trade deal with the US more than they need one with us, and he knows this makes the UK extremely susceptible to the US’s will. Firstly, because, under an ideal free trade agreement, a greater proportion of our exports will be US-bound than theirs would be UK-bound. Secondly, they have the clout and resources to start a tariff war with the UK, knowing that it’ll hurt them less than it’ll hurt us. Third, knowing we’re unlikely to negotiate particularly favourable terms with the EU, they’ll know the UK are desperate, and will therefore be more likely to agree to unfair terms with the US.

And these dynamics are now our reality. With the US demanding parity of market access, the erosion of UK food standards and removal of protections on NHS services and drug prices, Trump has sent a clear message to the UK. We will give you what you want if you offer us everything you hold dear.

Playing the neorealist game of counting capabilities for a moment, if we look at the UK versus the US in terms of economic scale; the global GDP in 2018 was around $142 trillion, with the US and UK representing roughly $20.5 trillion and $2.8 trillion respectively. Alternatively, we might turn the global GDP into a ratio out of 100, with the UK having a rough stake of 2/100, and the US holding a stake of 14.5/100. Now, this comparison may not be all-inclusive, but it indicates the UK’s vulnerability. We are a small fish, pleading for the benevolence of a big fish that has decided that its friendship are secondary to its appetite – but things have not always been so hopeless.

Indeed, while the infamous Suez crisis tells us that the US has always been quite particular about when it chooses to be the UK’s friend, the UK has not always been quite so helpless when playing the international field. Pre-empting the expected response, I am not referring to the British Empire – that period of British dominance has well passed, and short of some miracle, (thankfully) shows little sign of occurring in the near future. Instead, what I am referring to is the UK’s time as an EU member.

While at best third in command of the EU agenda – behind the Franco-German double entente – the UK was part of a body of unilateral rights and standards that were hard to erode, even by the largest of big powers. Rather than going, hands extended with a $2.85 trillion GDP, to an audacious US president for a trade deal, the UK could have been part of the EU bloc, with a nominal GDP of $18.3 billion in 2019. These numbers might seem over-simplistic or even meaningless to some, but when we have a president who makes neorealist IR theory more accurate than ever, these numbers have more significance than many would care to realise.

The simple fact is that it is far easier to dictate terms with Trump as part of the EU than it is outside of it. Once the EU bloc has agreed upon a policy direction, it can defend these decisions with the voices – and power – of over 25 nations against external antagonists. This is not denying, of course, the EU’s current internal turmoil – as evidenced in the recent debate over pandemic recovery spending. However, as a group of small and medium-sized countries acting together, the EU has successfully protected itself against attempts to erode its citizens rights and standards, with all external actors having to adhere if they want to trade goods with the vast single market.

This luxury of dictating terms to outsiders is only afforded to these little fish because of their decision to band together, and acting to prevent each individual agent being bullied by bigger fish. Of course, it would be right to argue that EU’s decision to give membership to nations which are economically troubled (take your pick) and ethically questionable (potentially Turkey) might have put an expiry date on the organisation in its current form. With that being said, Britain’s choice to exit the bloc when it did puts us at the mercy of an unmerciful president, and we should pray that he doesn’t secure another term in November. If he does, we may find that the standards and services which preserve our way of life, will be at an acute risk.

Further, and I fear, concurrently, our opportunities to trade with the EU – now from outside of it – will be limited if we align ourselves with the US script. The narrative of pro-US trade deal Conservatives has so far been one of welcoming cheaper, lower-quality goods, as this will improve the range of goods available to UK consumers. In fact, it is unlikely that any move towards lower standards will be in any way partial. Trump will likely demand that UK supermarkets accept US goods on their shelves, and once this starts, I fear it will mark the decline of existing UK standards. Under the pretence of ‘choice’, cheaper goods will likely gain market share as initial consumer resistance to the new products gradually dissipates. Over time, UK farmers will have a very real dilemma on their hands: supply the lower quality goods that UK consumers are buying, or maintain standards to trade with the EU.

Ultimately, all we need to know is that Trump getting another four years in office will be an entirely bleak deal for the UK. Floating the idea of a triumphant US-UK trade deal may give Britain some leverage in its negotiations with the EU (plainly because we’ll appear less desperate), but doing so while at Trump’s behest, may mean we have to make some very real concessions. We’ll likely be reminded, once again, that Brexit in the time of Trump can only bring us more pain than gain.

According to a new report by Email security company Tessian, some 43% of employees made mistakes which had resulted in cybersecurity repercussions for themselves or their company. The report, titled ‘The Psychology of Human Error’, was carried out in April on a total of 2,000 participants from the UK and US, to reveal the effects of stress, distraction and workplace disruption on people’s tendency to make errors at work.

The report also found that 20% of companies had lost customers following an instance of emails mistakenly being sent to the wrong recipient, with these details containing either irrelevant information or at worst, potentially sensitive information. Tessian said that as much as 58% of employees surveyed admitted to making this mistake at some point, with 10% saying they had lost their job as a result of making such an error.

Additionally, a quarter of respondents admitted to having clicked on a phishing email at work. These type of mechanisms are commonly used by scammers, seeking to ‘phish’ or steal data from the email recipient, often including financial and personal details. Interestingly, instances of mistakenly opening phishing emails were most common in the tech sector, with 47% of employees in the field admitting to having clicked on a phishing email.

Why are these mistakes so common?

Though the reasons these mistakes happen are likely numerous, Tessian’s report focused on psychological factors which may have contributed to lapses in staff focus.

The number one reason cited for potentially cybersecurity jeopardising mistakes was employees being distracted, with 47% of employees stating that distraction was the main reason they’d fallen for a phishing scam, while 41% cited distraction as the reason for emails sent to the wrong recipient.

Contrary to many of the more positive cases in favour of flexible work arrangements, some 57% of respondents said they were more distracted when working from home, which would lead us to wonder whether the impact of employee mistakes have been even more acute during lockdown.

Other factors which caused staff to click on scam emails include 43% of respondents initially perceiving phishing emails to be legitimate, with 41% saying that scam emails appeared to be sent from senior executives or well-known brands.

The final issue discussed in the report was fatigue. With the stress and hassle of reconfiguring work arrangements and lifestyles to lockdown life, some 44% of respondents stated that fatigue contributed to them sending emails to the wrong person.

Speaking on the findings, Standford University Professor and expert in social dynamics, Jeff Hancock, commented:

“Understanding how stress impacts behaviour is critical to improving cybersecurity. This year, people have had to deal with incredibly stressful situations and a lot of change. And when people are stressed, they tend to make mistakes or decisions they later regret. Sadly, hackers prey on this vulnerability. Businesses, therefore, need to educate employees on the ways a hacker might take advantage of their stress during these times, as well as the security incidents that can be caused by human error.”

Other factors outside of psychological strains included biological characteristics. The report found that staff aged 18-30 were five times more likely to have made mistakes which may have compromised tehir company’s cybersecurity, than employees over the age of 51.

Further, Tessian also found that male employees were twice as likely to fall for a phishing scam than their female counterparts, with 34% of male employees clicking on a data-stealing email versus 17% of female staff.

The alarming regularity of poor cybersecurity

Instances of high profile cybersecurity breaches seem to make their way into the news cycle on an uncomfortably regular basis for many consumers. Should the move to a more tech-integrated society continue at its current high pace, companies will need to convince their users that online solutions don’t come with inherent risk attached to them.

Speaking on how online security can be improved on an institutional level, Tessian CEO, Tim Sadler, commented:

“Cybersecurity training needs to reflect the fact that different demographics use technology and respond to threats in different ways and that a one-size-fits-all approach to training won’t work. It is also unrealistic to expect every employee to spot a scam or make the right cybersecurity decision 100 per cent of the time, especially during these uncertain times.”

“To prevent simple mistakes from turning into serious security incidents, businesses must prioritise cybersecurity at the human layer. This requires understanding individual employees’ behaviours and using that insight to tailor training and policies to make safe cybersecurity practices truly resonate for each person.”

Kingfisher (LON: KGF) reported strong sales on Wednesday, leading to the B&Q owner to forecast a rise in half-year profits.

For the quarter to 18 July, the group reported a 21.6% rise in like-for-like sales compared to the same period a year previously.

Kingfisher started reopening stores across the UK and France from mid-April, whilst its click-and-collect and home delivery meant that online sales were consistently 200% higher in May and June.

The company said in a statement: “Our top priority remains ensuring the health and safety of our colleagues and customers, serving our markets as a retailer of essential goods, and protecting our business for the long term.”

“The operational and financial actions we have taken, together with the strong demand for home improvement we are currently seeing, give us a sound footing in the current crisis and beyond,” it added.

“While we are entering the second half with a favourable trading backdrop, second half visibility remains low given uncertainty around COVID-19 and the wider economic outlook.”

Whilst many businesses are announcing wide-scale redundancy plans and axing jobs, Kingfisher said last month that they plan to hire 3,000 to 4,000 employees to cope with the surge in online demand.

Half-year results for the group will be shared in September. The Kingfisher share price (LON: KGF) is trading +10% at 247.70 (0855GMT).

London-based fintech company Yobota commissioned an independent body from the Market Research Society to survey 2,000 UK consumers on their usage of financial technology services during the lockdown period.

The research illustrated, first and foremost, that 64% of those surveyed had relied upon fintech to manage their finances between March and June, which was up from 42% pre-lockdown – representing an increase of over 50%.

One in three consumers also said that the lockdown had exposed them to the range of technological solutions on offer for financial management tasks, with 42% planning to use fintech products ‘much more’ than they previously had, even as bank branches reopen.

How are we using fintech?

Despite the increasing range and sophistication of online financial tools, most UK adults still prefer to use fintech for menial online banking tasks, with 88% using their apps to check their accounts and 80% transferring money.

This compared to 35% who had used virtual offerings to withdraw funds out of an investment and 27% who had used online tools to shop around for new financial products. Also worth noting, is the 21% who secured new financial products – such as credit and debit cards – without ever speaking to a human.

A fintech-enabled future?

With the UK, and specifically London, being home to many of the world’s new fintech entrants, the rising use of these products by British consumers seems like a natural occurrence.

Some 15% of people said they had been frustrated by their bank’s poor technology offerings, while this figure rises to 28% between the 18-34 age bracket. Underlining the importance of these tools going forwards, 47% of respondents said that tech offerings were now a ‘key consideration’ when choosing a financial service provider.

Not only will fintech become more prevalent as the quality and scale of services improves, but also as trust increases. Many consumers are still sceptical about carrying out sensitive transactions online, so the fast rise of fintech – still in its relative infancy – should tell us all we need to know about its potential to become the predominant form of banking in the future.

Aside from benefiting over time from a younger generation that are comfortable living more tech-integrated lives, companies know that tightening up security while increasing convenience, will be the key to making fintech a more integral part of modern life.

Although Vietnam has many of the characteristics of a more recognized ‘emerging market’ in part due to the size of the equity market already being above USD 160 bn, and with more than 1,500 companies to invest in, it is still classified by MSCI as a frontier market. In fact, this year Vietnam is likely to be the largest component of the Frontier Market Index. As a frontier market, it is estimated that only one in five emerging market investors are present: it will be a game changer in a few years if and when Vietnam is classified as an MSCI Emerging Market.

Vietnam has emerged from the covid-19 crisis as a winner. Its capital markets are set for expansion, the infrastructure is improving, and it will continue to attract interest from manufacturers and other types of companies looking to diversify away from China. Its macro-economic position is the envy of much of the world, and this could improve in a scenario where the US dollar weakens. Clearly the world as a whole is facing uncertainties, and there will be winners and losers ahead. Vietnam has signaled the ‘V’ for Victory sign against the devastating coronavirus, and this fast-growing country of 100m people is one to keep an eye out for in the months and years ahead.

Vietnam Holding Limited (LSE: VNH) can be purchased through your stockbroker, or wealth manager, and should be considered as a part of a diversified portolio for investors with a mid-to long-term investment horizon.

Author’s Note: the title ‘Viva Vietnam’ was first used by Standard Chartered Bank in 2003, when they correctly called the first growth cycle in Vietnam’s capital markets. I was working at Standard Chartered at the time and had successfully co-led an investment in a company that manufactured branded toiletries for the emerging consumer classes in south-east-Asia. They had a dominant position in the Malaysian market, a population of about 30m people, and a small but fast-growing business in Vietnam. During the due-diligence on the investment (which was a ‘home-run’ generating substantial gains), I was so taken by the incredible prospects that I moved my family to Vietnam for five years and helped Prudential invest across a wide-range of asset classes on behalf of its domestic customers.

The author of this article is Craig Martin, Chairman of Dynam capital (www.dynamcapital.com), a Guernsey regulated fund manager focused exclusively on the exciting opportunities in Vietnam. Dynam has a team of 12 Vietnamese professionals on the ground in Ho Chi Minh City.

Dynam is the Investment Manager for Vietnam Holding Limited (LON:VNH) an Investment Trust listed on the premium segment of the Main market of the London Stock Exchange.

See www.vietnamholding.com for more information.

Although Vietnam has many of the characteristics of a more recognized ‘emerging market’ in part due to the size of the equity market already being above USD 160 bn, and with more than 1,500 companies to invest in, it is still classified by MSCI as a frontier market. In fact, this year Vietnam is likely to be the largest component of the Frontier Market Index. As a frontier market, it is estimated that only one in five emerging market investors are present: it will be a game changer in a few years if and when Vietnam is classified as an MSCI Emerging Market.

Vietnam has emerged from the covid-19 crisis as a winner. Its capital markets are set for expansion, the infrastructure is improving, and it will continue to attract interest from manufacturers and other types of companies looking to diversify away from China. Its macro-economic position is the envy of much of the world, and this could improve in a scenario where the US dollar weakens. Clearly the world as a whole is facing uncertainties, and there will be winners and losers ahead. Vietnam has signaled the ‘V’ for Victory sign against the devastating coronavirus, and this fast-growing country of 100m people is one to keep an eye out for in the months and years ahead.

Vietnam Holding Limited (LSE: VNH) can be purchased through your stockbroker, or wealth manager, and should be considered as a part of a diversified portolio for investors with a mid-to long-term investment horizon.

Author’s Note: the title ‘Viva Vietnam’ was first used by Standard Chartered Bank in 2003, when they correctly called the first growth cycle in Vietnam’s capital markets. I was working at Standard Chartered at the time and had successfully co-led an investment in a company that manufactured branded toiletries for the emerging consumer classes in south-east-Asia. They had a dominant position in the Malaysian market, a population of about 30m people, and a small but fast-growing business in Vietnam. During the due-diligence on the investment (which was a ‘home-run’ generating substantial gains), I was so taken by the incredible prospects that I moved my family to Vietnam for five years and helped Prudential invest across a wide-range of asset classes on behalf of its domestic customers.

The author of this article is Craig Martin, Chairman of Dynam capital (www.dynamcapital.com), a Guernsey regulated fund manager focused exclusively on the exciting opportunities in Vietnam. Dynam has a team of 12 Vietnamese professionals on the ground in Ho Chi Minh City.

Dynam is the Investment Manager for Vietnam Holding Limited (LON:VNH) an Investment Trust listed on the premium segment of the Main market of the London Stock Exchange.

See www.vietnamholding.com for more information.