“In the years ahead, we will create together an even more diverse organisation, supporting the recovery with a special focus on vulnerable consumers, embracing new technology, playing our part in tackling climate change, enforcing high standards and ensuring the UK is a thought leader in international regulatory discussions.”

Rishi Sunak announces Nikhil Rathi as new FCA Chief Executive

Chancellor of the Exchequer Rishi Sunak announced on Monday that Nikhil Rathi will take over as Chief Executive of the FCA.

Prior to today’s announcement, Mr Rathi served as the Chief Executive of the London Stock Exchange from 2015, and is well-acquainted with Treasury officials, having served as Director of Financial Services for five years from 2009.

In his new role at the Financial Conduct Authority, Rathi will succeed Christopher Woolward, who acted as the interim Chief Executive following Andrew Bailey‘s departure to head up the Bank of England in March. Rathi is being appointed on a five-year term, with Woolard continuing to act as interim Chief Executive until the appointment begins.

Speaking on the announcement, Chancellor Rishi Sunak, said:

“Nikhil is the outstanding candidate for the position of Chief Executive of the Financial Conduct Authority, and I am delighted that he has agreed to take up the role.”

“We have conducted a thorough, worldwide search for this crucial appointment and, through his wide-ranging experiences across financial services, I am confident that Nikhil will bring the ambitious vision and leadership this organisation demands.”

Once Rathi assumes his new role, he will be paid an annual salary of £455,000 and be required to give up any of his existing interests in the London Stock Exchange.

As reported by The Guardian, he will be the first BAME chief of the FCA, and during his tenure, Rathi aims to make the FCA a ‘more diverse organisation’, as well as focusing policy on tech innovation, climate change and continuing Woolward’s legacy of focusing on vulnerable consumers.

Speaking on his new role, incoming FCA Chief Executive Nikhil Rathi commented:

“I look forward to building on the strong legacy of Andrew Bailey and the exceptional leadership of Christopher Woolard and the FCA Executive team during the crisis. FCA colleagues can be very proud of their achievements in supporting consumers and the economy in all parts of the UK in recent months.”

BoE Governor says UK was on brink of insolvency

Bank of England governor Andrew Bailey candidly revealed the true extent of the impact of the coronavirus pandemic on the UK economy, admitting that Britain reached the brink of insolvency in the early stages of the outbreak. If the Bank had not intervened, the government would have faced a “market meltdown” and struggled to fund itself for the first time in its 325-year long history.

Unprecedented times, unprecedented measures

Speaking to Sky News podcast ‘The World Tomorrow’ on Monday morning, Bailey reflected on the extreme measures that the Bank of England was forced to take in order to keep the UK economy afloat earlier this year. After a record 20.4% contraction in April and warnings that the economy could shrink by 14% over the course of 2020, the Bank has already injected a total of £300 billion in efforts to maintain market liquidity, but the forecast for the rest of the year remains decidedly grim. Bailey warned that many viable British companies will fail to make it to the other side of the crisis – with widespread predictions of a recession – and added that the Bank’s unprecedented quantitative easing programme should not be taken for granted. Last week, the finance institution raised its bond purchase target to £745 billion, following on from a record drop in interest rates to 0.1% back in March. He commented on the economy’s 2020 performance: “We basically had a pretty near meltdown of some of the core financial markets”.Getting back on track

After starting as Governor of the Bank of England in the week before UK lockdown measures came into force, Bailey has faced a challenging first few months on the job. He has since suggested that the Bank should start to cut back on its asset purchases before it begins to raise interest rates again, in direct opposition to his predecessor’s strategy. “When the time comes to withdraw monetary stimulus, in my opinion it may be better to consider adjusting the level of reserves first without waiting to raise interest rates on a sustained basis”. Previous Governor Mark Carney said that the Bank would increase interest rates before selling purchases back to the market in its post-pandemic plans. On the contrary, Bailey stated that he wants to avoid high central bank holdings of government debt in the future, adding: “Elevated balance sheets could limit the room for manoeuvre in future emergencies”.Uncertainty grips markets

After a tumultuous Monday morning for global equities amid fears of a second wave of coronavirus, the FTSE 100 (INDEXFTSE: UKX) is down by 18.42 points or 0.29% BST 14:25 22/06/20. The DAX (INDEXDB: DAX) continues its downward trajectory at -0.49% CEST 15:07 22/06/20 and the CAC 40 (INDEXEURO: PX1) struggles to recover from a pessimistic performance earlier on at -0.47% CEST 15:09 22/06/20.Centrica shares dip despite announcing digital and renewable British Gas X

British energy company Centrica (LON:CNA) announced on Monday that it had launched British Gas X, a modern-day challenger to its British Gas flagship brand.

The company said a test website for British Gas X was already up and running, and that the new service would be entirely online and designed for ‘digitally savvy’ consumers.

It added that existing British Gas customers can switch to the new service ‘at any time with no exit fees’, and that they will offset the energy customers use from ‘100% renewable’ sources. The new company has been launched in an effort to stay with the times, in the highly competitive British energy market.

This follows the continued trend towards decarbonising British energy, which is having something of a renaissance under the ‘build back better’ initiative, which aims to see Britain rebuild from the Coronavirus pandemic by relying on greener energy solutions. The likes of BP with its drive towards renewables, Drax Energy extending its ESG facility and Abuandance launching its renewables-based fixed-rate debentures, are all testament to recent efforts to modernise British energy generation.

Today’s news also comes after the announcement that Centrica would axe up to 5,000 jobs, while rival Ovo planned to close offices and lay off 2,600 staff.

Following the update, Centrica shares dipped by 3.51% or 1.51p to 41.51p per share 14:05 BST 22/06/20. The company’s p/e ratio stands at 5.89, its dividend yield is generous at 12.09%.

FTSE 100 wavers amid fears of coronavirus second wave

The FTSE 100 (INDEXFTSE: UKX), DAX (INDEXDB: DAX) and CAC 40 (INDEXEURO: PX1) all opened with an underwhelming performance on Monday morning, dropping over 1% as markets responded to mounting fears of a second wave of coronavirus.

By mid-morning, both the DAX and the CAC 40 had recovered, up 0.4% – however the momentum trailed off not long after, with all 3 markets slipping back into the negative by noon.

Reports of an outbreak at a German meat processing factory and a spike in cases in Beijing have concerned investors, throwing cold water over the progress made at the start of the month when the FTSE 100 traded at its highest level since the start of the pandemic.

Markets can’t make up their minds

The markets’ tumultuous behaviour is a reflection of the conflicting news to hit the headlines in the past week. Russ Mould, investment director at stockbroker AJ Bell, commented on Monday morning’s performances:“Investors continue to be pulled from different directions by various headwinds and tailwinds. On one hand there is positive news such as Spain accepting UK tourists without the need for quarantine, adding to the list of restrictions being lifted across Europe. On the other hand, the US still seems to be struggling to contain the coronavirus and the risk of a second wave is still front of mind for many people”.

Jim Reid, strategist at Deutsche Bank, weighed in: “The virus spread continues to create a lot of uncertainty in markets. For example, does it matter that the troublesome US states are continuing to see case numbers increase or does it provide some good news that economies can stay open as cases rumble on?”. UK investors may find solace in Prime Minister Boris Johnson’s announcement scheduled for tomorrow, in which he is expected to lay out the government’s plan to reopen the hospitality sector by the 4th of July – amid a revision of the official 2m social distancing guidelines, deemed by industry leaders as too restrictive. Non-essential retailers opened last Monday to queues and crowds in England, indicating that the relaxation of lockdown measures could bring a much-needed boost to the economy after months of suffering and a record 20.4% contraction at the peak of the pandemic. However, the travel industry in particular continues to struggle as countries refuse to reopen borders and summer holiday plans are scuffled. British Airways-owner IAG (LON: IAG) share price slipped almost 5% at noon, with cruise operators Carnival plc (LON: CCL) down 5.26% and easyJet (LON: EZJ) weathering a 0.80% drop.The road ahead

So, mixed signals overall as share prices almost universally slide and global news bulletins continue to focus on coronavirus-induced anxiety. At midday there was a snippet of market confidence as the seasonally adjusted IHS Markit UK Household Finance Index (HFI) reported a rise to 40.7 in June from 37.8 in May. Joe Hayes, an economist at IHS Markit, was quick to dampen any over-excitement on the good news: “It is reassuring to see the UK Household Finance Index rebounding in June, as it suggests that the financial hardship endured during the height of the lockdown is easing. Job security perceptions are still at extreme levels of pessimism, and the data here suggest there has been little pickup. This isn’t surprising given that large parts of the UK economy remain shuttered, but such negativity towards employment status is likely to generate risk aversion in consumption habits, which will undermine the recovery. Incomes from employment were also in deep contraction territory during June. Key to the economy returning to pre-COVID-19 levels of economic output as quick as possible will be strong demand, which will encourage robust business activity and employment growth. If households are fearful for their job security and their incomes are falling, the UK’s path of recovery could be a slow one”.Go Outdoors on brink of administration

The JD Sports brand, Go Outdoors, is expected to fall into administration.

As the Coronavirus pandemic is putting pressure on the UK high street, the brand has suffered from closed stores and a lack of online demand.

JD Sports bought Go Outdoors in a £112m deal in 2016. The brand has 67 stores and has over 2,000 employees.

The Manchester-based retail group specialises in fishing, cycling and camping gear and has not yet commented on the news, reported first today by Sky News.

JD Sports is expected to publish full-year results in July. It’s Go Outdoor brand was struggling before the pandemic. In August 2019, it posted a loss of around £40m.

Go Outdoors will be the most recent of a string of companies that have been hit by the Coronavirus pandemic. Since the crisis hit the UK, retailers including Laura Ashley, Debenhams, Oasis and Warehouse have called in administrators and thousands of high street jobs have been axed.

Whilst the high street reopened earlier this month, compared to the same period in 2019 footfall was down 45.3% according to retail analyst firm Springboard.

Although shops are reopening, our changed shopping habits will affect the high street for months to come.

“Consumers have changed their spending habits, and will be increasingly used to going without much of their discretionary shopping,” said Duncan Brewer, head of the UK retail and consumer team at consultants Oliver Wyman.

“With the inevitable recession coming, it’s likely that many will continue to be careful with spending, even if they are comfortable shopping in the first place,” he added.

The JD Sports (LON: JD) share price is trading -1.89% at 634.80 (0941GMT).

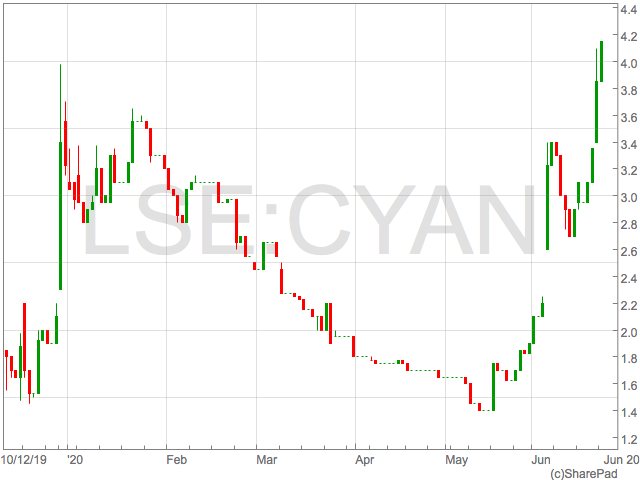

CyanConnode shares jump on the roll out of Indian contract

CyanConnde (LON:CYAN) has announced the commencement of an India contract relating to CyanConnode’s Narrowband Radio Frequency Smart Mesh Networks.

CyanConnde’s Smart Mesh Networks enable the Internet of Things (IoF) in end applications such as smart metering in power distribution.

Today’s announcement signals the eventual commencement of a Indian contract that had suffered delays, causing revenue to be recognised in a different accounting periods than previously expected.

Despite the delays, the first shipment of 10,000 CyanConnode OmniMesh Modules has been made to the project in India and the production of Smart Meters its set to begin shortly.

CyanConnode shares rallied over 11% in early trade on Monday following the news.

“The shipment is part of a contract to supply up to 200,000 Omnimeshenabled smart meters, worth £3.3m, as per the group’s press release issued in January 2020,” analysts at Arden Partners said in a research note.

“CyanConnode’s original expectation was that the installation of the project would be completed within fifteen months of kick-off, and that c.80% of revenue would have been recognised during the first two years with the remainder received over the 7-year support and maintenance contract commencing from the point of the project ‘going live’.”

CyanConnode pointed to COVID-19 slowing progress but were confident on ongoing demand and the growth of their Omnimesh Network Canopy.

“There has been a good start towards providing the Omnimesh Network Canopy, which will provide a hybrid RF Smart Mesh and Cellular communication network, that is licensed for up to 200,000 Omnimesh enabled smart meters,” said Anil Daulani, CyanConnode India CEO and MD.

“India is still seeing an increase of Covid-19 cases, and I wish to express my sympathies to families who have been affected. I remain optimistic and look forward to giving further updates relating to new orders in due course.”

CyanConnode shares were 11.68% stronger at 4.30p in early Monday morning trading in London.

CyanConnode shares were 11.68% stronger at 4.30p in early Monday morning trading in London.

CyanConnode shares were 11.68% stronger at 4.30p in early Monday morning trading in London.

CyanConnode shares were 11.68% stronger at 4.30p in early Monday morning trading in London.

UK debt exceeds GDP for first time since 1963

The UK government’s debt has exceeded the size of the economy for the first time since 1963, following a record £55.2 billion of government borrowing during May. In the last year, UK debt has risen to a total of £1.95 trillion – 100.09% of GDP – joining the likes of the USA and Japan in the list of countries with more national debt than income. Public borrowing is set to reach £300 billion by the end of the financial year; a figure twice as large as at the height of the 2008/09 global financial crisis. Forecasts for UK GDP over the course of 2020 include a projected 8.3% dive.

It’s not all doom and gloom – or is it?

On Friday, the Office for National Statistics (ONS) released its first estimate of retail sales for the month of May, indicating that the UK economy may be starting to bounce back after months of coronavirus-induced toil with a 12% increase in sales on the previous month. The long-awaited reopening of hardware and gardening stores stirred an encouraging 42% increase in sales during May, and online companies enjoyed a record 33.4% of total spending – a modest jump up from 30.8% recorded in April. Fuel sales witnessed a significant increase on the last couple of months, but still stand at an eye-watering 42.5% lower than they did in February, before travel restrictions were put in place. Clothing stores have suffered the worst out of all retailers, with sales down more than a bruising 60% in May. Non-essential stores were only permitted to open from 15th June onwards, meaning the June figures will also likely be significantly less than this time last year – even as high street stores bask in the boost from returning customers. The knock-on effect of panic-buying in March and April continue to keep food and household essentials sales high, although they are beginning to slip back towards the expected levels for this time of year, down on the previous month by 0.3% in May. The optimistic stats come with a hefty dose of caution however, as the ONS warns that overall sales are still down 13.1% from February, before the pandemic’s chokehold managed to get a firm grasp of the UK economy. In the three months leading up to May, the total volume of retail sales plummeted by a record 12.8%, with declines across all UK stores except food and online retailing.Britain’s public finance problem

Although the retail sector is enjoying a return to relative normality in June, the ONS figures continue to cast a long shadow over the good news. Public borrowing of £55.2 billion during May represents a nine-fold increase on this time last year, and the government is still expected to borrow a total of £350 billion over the course of 2020 – significantly overshooting the UK Treasury Office for Budget Responsibility’s forecast of £300 billion. Capital Economics’ chief economist, Paul Dales, was keen to emphasise the upwards trajectory expected from the economy over the rest of 2020: “Both net borrowing and the net cash requirement should trend down from here as the economy reopens”. Not all are in agreement that a quick and clean economic recovery is on the horizon though. Samuel Tombs, the chief UK economist at the consultancy firm Pantheon Macroeconomics, weighed in: “Unofficial indicators of households’ overall spending remain very weak; Barclaycard, for instance, reported that spending fell 26.7% year over year in May, not vastly better than April’s 36.5% decline”.The road to recovery

The UK government’s borrowing will likely be offset by the Bank of England’s £100 billion stimulus package, announced this Thursday, but the looming threat of a second wave of coronavirus infections continues to cast a dark cloud over market confidence. In spite of all this, bouncing off of rising oil prices and a slip in the sterling exchange rate, the FTSE 100 climbed up 82.13 points (1.32%) to 6,306.32 at BST 14:19 19/06/20. The US indices are expected to emerge on a stronger performance than yesterday, with the Dow Jones average predicted to increase by 295 points to 26,375, ending on a positive note before the weekend.Bank of England £100bn stimulus – what are the pros and cons of QE?

On Thursday the Bank of England announced it would extend its bond-buying programme by £100 billion, in a bid to support the UK economy through the Coronavirus pandemic. The move sees a continuation of the bank’s quantitative easing, which began at £200 billion in 2009, and after today’s announcement stands at £745 billion.

It follows £200 billion-worth of bond purchases back in March, the (in this context) encouraging news that UK inflation was at a four-year low, and the ONS report which stated that the UK economy had contracted by 20.4% in April.