Whitbread (LON: WTB) has swung into a £660.5 loss for the six months to 27 August.

The loss for the Premier Inn owner is compared to the £172.2m profit in the previous year.

As hotels were closed during the lockdown, revenue plunged £76.9m to £250.8m in the UK and Germany.

Over the UK lockdown, revenue plunged by 99% as almost all hotels were closed.

Since reopening hotels, Whitbread has said that performance has remained ahead of the market.

“Whitbread’s long-term strategy remains as relevant and compelling as ever,” said Chief executive Alison Brittain.

“The impact of the Covid pandemic on the hotel sector will undoubtedly be significant and we are already seeing signs of distress and constraint in the competitive landscape.

“This is likely to accelerate the structural changes in the market with supply contraction and constrained investment amongst independent and budget branded operators in both the UK and Germany.

“We hold a uniquely advantaged position in the UK market as the largest player with the strongest brand.

“Our financial flexibility and resilience, combined with a strong balance sheet, give us the ability and the confidence to invest with discipline and focus on strong long-term returns.

“We will be well placed to enhance our market leadership position even further in the UK, and accelerate our growth in Germany, supporting our guests and teams and driving long-term value for all our stakeholders,” Brittain added.

Whitbread shares (LON: WTB) are trading 3.16% higher at 2.315,00 (0828GMT).

An obligatory Parental Guidance sticker has been stuck on Monday’s global equities movements. Because, between election, company data, and COVID jitters, it was an unadulterated horror show.

Global equities hardly elated over the election

Quaking in their boots just over a week out from the US election, global equities watch in horror as the Biden lead that was priced in, is slowly but surely being gnawed away at by a resilient Trump campaign.

Having performed terribly early on – and bagged the Biden campaign a 12% poll lead – team Trump has now narrowed the consensus poll margin to 9%, with some outlandish pollsters now forecasting a Trump lead in voter sentiment – let alone electoral college votes.

Now, sure, Rasmussen are Trump’s favoured pollsters, and they may well be trying to manifest a Trump lead into existence, but data such as these may still be enough to shake the confidence of some investors who’d previously banked on a Biden victory. Speaking on the markets’ preferences for election outcomes, Kingswood CIO, Rupert Thompson, said:

“The market’s preferred outcome seems to be for a clean sweep by the Democrats which will allow the implementation of a sizeable fiscal stimulus. If by contrast, there were split control of the Presidency and Congress, this would effectively lead to a continuation of the status quo with divided government a major constraint on new policies. Worst of all, however, would be a close and contested result with possibly weeks of rancour and confusion in prospect.”

Company data expected to be positive, but preparing for disappointment might add to Monday’s downside

Another factor weighing on global equities is the anticipation of blue chip company data being published during the week. And, while much of this earnings data is expected to have a positive tone, pricing in positive results creates the possibility of disappointment, and there’s every chance those kind of jitters have been amplified by Monday’s other worries.

Some of the companies set to publish their performance data this week include the American big tech cabal, including Microsoft, Amazon, Apple, Alphabet and Facebook. Further, there will be a Q3 GDP reading on Thursday, on which, Spreadex Financial Analyst, Connor Campbell, comments:

“That should, at least, be a positive, with analysts forecasting growth of 32% at the annualised rate, compared to Q2’s 31.4% contraction.”

Nothing short of COVID carnage

The third and final factor weighing on Monday’s global equities performance, are ongoing COVID updates. With case numbers expanding rapidly across Europe, equities losses were led by Germany, with SAP shares down some 22%, and seeing the DAX shed 3.43% on Monday. IG Analyst, Joshua Mahony, adds:

“The German focus has also been highlighted by the latest Ifo business climate figure, with the survey reversing lower for the first time since the height of the crisis in April.”

Following behind the German fall was the French CAC, down 1.50% as cases hit ‘record highs’, while Spain enters a state of emergency, and TUI and Carnival shares falling sees the FTSE shed 0.97%. Mr Mahony adds:

“While we are seeing nations attempt to stifle the spread of the virus through more localised and tentative restrictions, it seems highly likely that we will eventually see a swathe of nationwide lockdowns if the trajectory cannot be reversed.”

While further restrictions appear likely, hope prevails for a COVID vaccine to be developed during the early stages of next year. These hopes, however, were not enough to see Eurozone equities regain their composure, with the Dow Jones delivering a late gut shot, by opening down over 2.50%.

It’s an age-old and at times over-simplistic adage: buy low, sell high. But it exists for a reason, and research conducted by behavioural finance experts, Oxford Risk, shows just how much we might lose by choosing not to invest during the pandemic.

The company states that many retail investors make decisions on the basis of ’emotional comfort’, which they estimate costs your typical investor around 3% per year in returns – during an average year. Given the increased level of market volatility during the pandemic, however, they believe the level of emotional decision-making has increased ‘dramatically’, and so too has the potential cost of emotional investment.

In fact, Oxford Risk predicts that with many choosing to increase their cash allocation due to pandemic uncertainty, ‘reluctance’ to invest might cost retail investors between 4% and 5% per year in long-term returns.

The company adds that what it calls the ‘Behaviour Gap’ – losses due to timing decisions caused by investing more money when times are good for stock markets and less when they are not – costs investors an average of 1.5% to 2% a year over time.

Having built up an expertise in developing financial decision-making software, Oxford Risk states that wealth managers and financial advisors remain ‘ poorly equipped’ to deal with complexity, uncertainty, behavioural biases and the ’emotional and psychological roller-coaster ride’ their clients have faced during the COVID pandemic.

Speaking on emotional decision-making, Oxford Risk’s Head of Behavioural Finance, Greg B Davies, PhD, said that human conversations are vital during times of crisis, but added that better diagnostic tools are needed to assess clients’ personalities and ‘likely behavioural traits’. He says:

“The suitability processes of many wealth management businesses are typically too human heavy, inefficient, and front loaded to the beginning of the client relationship to keep up with rapidly changing client circumstances at scale during a crisis. Understanding of client financial personality is typically limited to risk profiling – often badly – and subjective human assessment.”

“Very few wealth management propositions are using the sort of objective, science-based measures that are needed to provide a comprehensive picture of their clients. There is too much guesswork and not enough technology.”

The company adds that there are common behaviours that investors adopt during volatile periods, which include focusing too heavily on the present and on small details, and feeling compelled to take action when the best solution might be a mroe hands-off, patient approach. These behaviours can lead to underinvestment, selling low, and decreased diversification, as clients choose to invest in the familiar.

Oxford Risk has launched a free Market Emergency Survival Kit which allows retail investors to measure six key dimensions of financial personality, which the company has identified through extensive research into investor psychology and financial wellbeing. The service also provides personalised recommendations on how best to invest, which are based on the findings.

Speaking on the measures investors can take, Oxford Risk’s CEO< Marcus Quierin, PhD, comments:

“Many of these actions will mean that investors turn paper losses into real ones. If they don’t need to withdraw money for immediate expenses, then the losses are only virtual… until they panic and make them real.”

“The investments in the news are not your investments. Retail investors should avoid watching the markets day-to-day as this will only increase anxiety to no useful end, and make you feel like you should be doing something, without any useful guidance to what that should be. Long-term plans should be looked at through long-term lenses.”

Mr Quierin adds that investors should focus only on factors that they can control, and in turn might postpone discretionary spending, and use volatile periods as an opportunity to take stock of long-term financial plans. He finishes by saying that consumers would benefit from choosing to invest in the ‘risk premium’. Put simply: the long-term reward for owning shares that eventually weather every short-term risk that can be thrown at them.

According to data compiled by ComprarAcciones, M&A deal activity in the pharma sector rose by 17% during the first half of 2020.

To many, this would appear to be a positive shift, given the economic impacts of the pandemic. However, the rise in pharma industry deals might not come as a surprise to some, and it is worth noting that the deals being done, were less audacious than those completed during previous years.

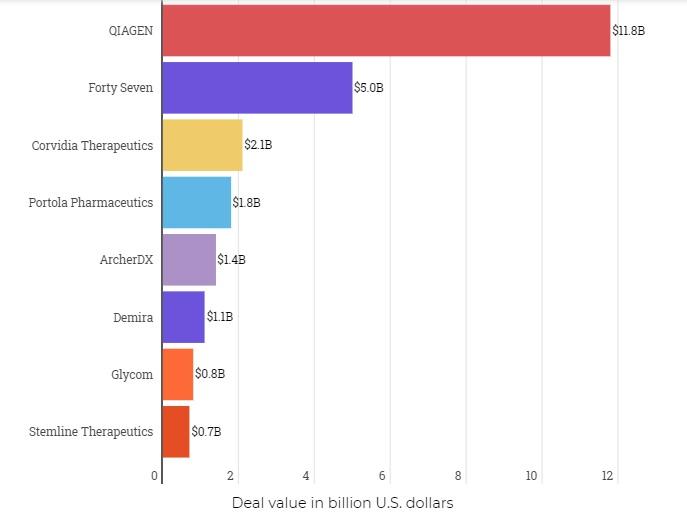

Though a total of 41 deals were done during H1 2020, the total deal value during the second quarter – $3.3 billion – was the lowest quarterly sum since the first quarter of 2018.

Similarly, PwC reported that the pharma subsector saw a 56% drop in deal value between the second half of 2019 and H1 2020. For pharma, biotech and medical devices sectors as a whole (PLS), deal value fell by 87.2% during the same period comparison.

Top pharma deal H1 2020, PwC data, compraracciones graphic

While those numbers might appear drastic, the comparison is only amplified when we look at year-on-year trends. During the first half of 2019, the total deal value for the pharma subsector was $100.1 billion. In contrast, ComprarAcciones reported that the total value of pharma sector deals was $7.7 billion, down by over 92% year-on-year.Similarly, combined pharma and life sciences M&A deal value fell from $272.9 billion, to $35 billion. During the same periods, the number of deals fell from 119, to 99, while deals in H2 2019 stood at 129.

According to S&P Global, the healthcare industry as a whole started off the second half of 2020 with 13 deals, valued at more than $1 billion.

Speaking on declining deal volumes and value in the pharma sector, the ComprarAcciones report added:

“On the other hand, based on a report from Global Data, the global M&A deal value started on a downtrend in Q1 2020. It went from $151.2 billion to $129.9 billion from February to March. Another study from S&P Global shows that the decline carried into Q2 2020, with a 35% drop in deal volume. Similarly, total transaction value dropped by 40%, the highest drop since 2015.”“Comparing H1 2020 to H2 2019, the total deal volume sank by 32% year-over-year (YoY) from 10,155 deals to 6,938 according to Merger Market. Deal values sank by 53%, from $1.9 trillion to $901.6 billion during the same period.”

Driver Group shares (LON: DRV) surged over 11% on Monday as the group said it expects pre-tax profit to be £2.5m for the year to September 30.

Due to challenges around the pandemic, profit will be a 16% decrease from last year’s £3m total.

“Since January 2020 Driver Group has been managing the impact of Covid-19 on the business and by adopting a flexible home working model has continued to service its clients effectively and sustainably with the minimum of business interruption. Activity levels overall have been broadly consistent with those achieved in the first half, with a strong performance in the UK and Europe offset by a weaker result in the Middle East and Asia Pacific regions,” said the group in a statement.

Driver Group has opened a new office in New York which will enhance the group’s ability to service its clients in North America and provides improved access to the important South American markets.

The firm has also restructured the Middle East and the Asia Pacific operations so it can meet the changing business demands in those regions.

Mark Wheeler, chief executive of Driver Group, said: “I am pleased to be able to report that Driver Group has performed well during the year and has managed the uncertainty caused by the Covid-19 pandemic to ensure the business remained profitable and cash generative throughout the year in spite of a reduced level of activity.

“I am confident that the reduced cost base and renewed focus on our core business of higher margin expert witness and dispute resolution in both APAC and the Middle East will deliver improved operating performance. Alasdair and Stefan have proven track records in our business and I look forward to working with them and with our new colleagues in our operations in America and South Africa over the next few years to deliver significant progress,” he added.

Driver Group shares (LON: DRV) are 8.09% higher at 48,10 (1054GMT).

New aircraft orders have hit a record low over September.

No new orders were placed during the month of September and just 13 orders were made over the whole quarter – a 91.4% fall compared to the same period last year.

July saw four orders, whilst in August there were nine. It is the worst three-month since records began.

ADS chief executive Paul Everitt said: “The aerospace and aviation industries have invested in robust health and safety measures as part of aircraft design which makes the risk of transmission when travelling aboard an aircraft extremely low.

“We need to continue to work together internationally to improve consumer confidence and encourage a return to the skies.

“The quarantine period that passengers face when they return home is one of the main barriers to UK aviation’s recovery and testing can play a major role in reducing this.

“The government should rapidly implement a testing regime so that the 14-day quarantine period can be shortened. This will help improve confidence amongst travellers and in turn put the aviation and aerospace sectors on a path towards recovery.”

Ministers have said that are looking at reducing the UK quarantine period from 14 days to between 10 days and a week.

Shares in airline groups have plummeted over 2020 as the sector has been hit by travel restrictions and a fall in journeys amid the Coronavirus pandemic.

The union, Unite, estimated that in June 12,000 jobs had been lost in the sector, which supports around 110,000.

United Carpets shares (LON: UCG) surged +15% on Monday’s opening after posting a 24% increase in sales for the 19 weeks to 1 October 2020.

The specialist retail carpet and floor covering retailer said that despite no revenue generated during the eight weeks over lockdown, strong sales since have kept the group in a strong financial position.

United Carpets expects further challenges to arise from the pandemic and Brexit, which may deter demand.

The group warned that a “no-deal” Brexit may result in additional import tariffs on flooring products, and the longer-term impact from Covid-19 on unemployment and economic recovery may lead to a challenging retail environment in the next year.

Paul Eyre, the chief executive of United Carpets, said, “Since our stores were allowed to re-open, we have been encouraged by a strong period of trading. Customers appear to have been making up for the purchases they would have made during lockdown, with an increased focus on home improvements.

“Looking ahead, however, there are a number of significant, potential headwinds facing our sector and the UK economy in general strong demand for home improvement products combined with disrupted production due to Covid-19, have led to raw material shortages and, consequently, increased input prices across our sector.”

United Carpets had cash and cash equivalents of £5m from the end of September. Of this, £2m was received under the Coronavirus Business Interruption Loan, and the group also gained from the deferral of £1m of tax payments.

“Accordingly, the Board believes that the Group has sufficient capital to support the business through the current challenges, and is well placed in the event of any further restrictions due to the ongoing Covid-19 crisis,” said the group in its trading update.

United Carpet shares (LON: UCG) are currently trading +19.69% at 3,89 (1017GMT).

Tighter restrictions across Europe led to stock markets opening significantly lower on Monday morning.

UK’s FTSE 100 index down 0.8% at 5,812, Germany’s Dax fell 2.7%, France’s CAC was down 1.3%, and Spain’s Ibex fell by 1.3%.

“Restrictions are continuing to tighten around the world, especially in Europe, where Spain just entered a state of emergency, and Italy has introduced its most severe measures since the end of its national lockdown in May,” said Connor Campbell from Spreadex, commenting on stock markets across Europe.

“And the pace of the virus is showing no signs of slowing down, with a new record number of daily cases in the US, and confirmation of 137 local cases in China,” he added.

Markets also fell in response to US stimulus talks – where an agreement has still not been reached.

“Time is fast running out, if it hasn’t already – why would either side want to get a deal done, especially blue wave-praying Democrats, when the country’s political landscape could’ve completely shifted in a week and a half’s time?” said Campbell.

In Asia, China’s SSE composite index fell 0.8% while Japan’s Nikkei was down by 0.1%.

The price of oil has also fallen. Brent crude 2.27%, to $40.82 a barrel whilst the price of US light crude fell 2.43% at $38.88 a barrel.

“Oil is under pressure on the back of concerns that supply from Libya will rise as rival factions have called a ceasefire and that should pave the way for an increase in output. The worries about rising coronavirus cases in Europe and the US has sparked demand concerns,” said David Madden, market analyst at CMC Markets UK.

Yourgene Health Plc shares (LON: YGEN) plunged 11.54% on Monday’s opening bell after the group shared results for the half-year ended 30 September 2020.

Revenues for the half-year were up 5% to £8.2m with “strong European revenues offsetting the headwinds from COVID-19 on international sales.”

Impacts from the pandemic were offset by the strong UK and European growth. UK growth was primarily driven by Corona related products and services.

Revenue across Europe surged by 80% to £2.9m from the £1.6m in the same period a year previously.

International markets were affected by the enforced lockdowns, which inhibited cross-border shipments and in-country non-COVID-19 testing, especially in Japan and India.

Lyn Rees, Chief Executive Officer of Yourgene, commented: “I am pleased to report continued year-on-year growth in the first half in the most challenging of circumstances, and it goes to show the core resilience that Yourgene has developed through its greater geographic and business diversity.

“With the US and Japan now reopening for business, I expect to see International revenues growing rapidly around our core products and we are busy recruiting commercial resource to support the growth in activity from existing customers and to drive the on-boarding of new ones. In our UK service laboratory we have successfully achieved our initial capacity objective of 10,000 COVID-19 tests per month and are now focussed on delivering 20,000 tests per month, which we hope to have in place by January 2021.

“Furthermore, our acquisition of Coastal Genomics in this period demonstrates our continued ability to execute on select, highly attractive inorganic growth opportunities. Our full year outlook remains in line with management expectations and we look forward to updating investors again when we publish our half-year results in December,” added Rees.

Yourgene Health Plc shares (LON: YGEN) are currently 7.54% down at 18,03 (0836GMT).

The Hut Group shares (LON: THG) opened higher on Monday morning after the group’s trading statement for the three months ending 30 September 2020.

The online retailer listed on the stock exchange last month +38.6% year-on-year revenue growth for Q3 with a +51.3%, year-on-year growth in online revenues to £320.2m.

The Hut Group has raised full-year 2020 revenue guidance to between £1.48bn and £1.52bn.

Matthew Moulding, the group’s chief executive and executive chairman commented:

“I am pleased to report a strong period of trading in our first quarterly update as a public company, including an upgrade to revenue growth guidance for 2020. I would like to thank all our colleagues for their huge contribution to date. Our strong organic revenue growth across all divisions, numerous THG Ingenuity partnership deals, and the recent acquisition of luxury skincare brand Perricone MD, demonstrates our strategic direction and progress in the period.

“Our decision to list on the London Stock Exchange provides us with a strong platform to raise the profile of both Ingenuity and our Brands, and further supports their strong organic growth. Our acquisition strategy remains unchanged, with a focus to complement organic growth with brand IP and Ingenuity infrastructure additions.

“THG has a very strong balance sheet, enabling us to further invest across each of our growth pillars. THG’s core competencies leave it exceptionally well placed and we are witnessing increased opportunities, in scale and volume, for selective acquisitions across all our divisions and geographies.

“I am delighted to announce the establishment of our Advisory panel with the first three appointments made to provide additional counsel and support to THG’s Board sub-committees. This is a transformational step for THG and we look forward to making additional appointments over the medium term,” he added.