FTSE rallies 1.3% as banking stocks surge

“A negative start in the US failed to dent Europe’s gains this Friday, while the Dow Jones [struggled] following the latest stimulus update.”

“Despite Nancy Pelosi stating that she and Treasury Secretary Steven Mnuchin are ‘just about there’ regarding a covid-19 relief plan, Trump’s economic advisor Larry Kudlow has claimed ‘the ball’s not moving much right now’, once again casting doubt on the chance of a pre-election package.”

“The concern is that, though a Joe Biden victory would potentially lead to a larger stimulus bill, it would also leave tight-fisted Republicans with little impetus to do anything that might help the incoming President during the ‘lame-duck’ period between November and January. And that could mean no economic relief until the New Year.”

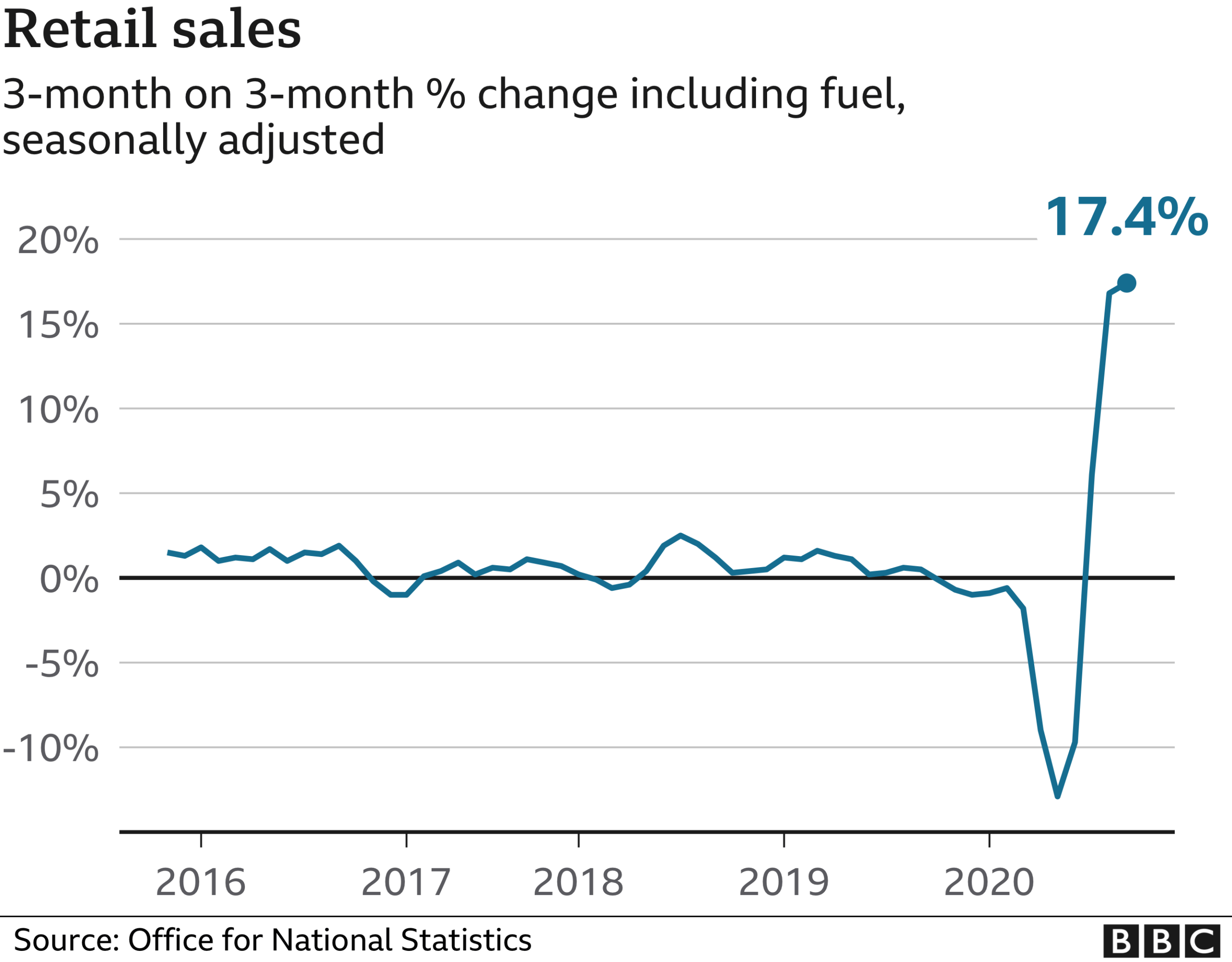

Did retail sales really bounce back in September?

The problem with this positive way of thinking is that retail sales aren’t actually experiencing exponential growth, Instead, September’s growth was lower than the previous month, there appear to be challenges ahead, and the growth is not being experienced by retailers across the board.

Indeed, new lockdown restrictions will have the double-edged-sword effect. The first half of this will be a reduction in customers and potential closure of some shops. As stated by Kingswood CIO, Rupert Thompson:

“Retail sales posted an unexpectedly strong gain in September, rising 1.5% m/m to be up 4.7% from a year earlier. However, this is only encouraging up to a point as this strength was prior to the introduction of the new lockdown/social distancing measures. Business confidence fell back in October with the decline led by the services sector, the area the most vulnerable to the latest restrictions. This fall highlights the need for the new package of support measures announced by the Chancellor yesterday.”

The second consideration will be a change in consumer behaviour, with customers focusing on outlets perceived to be selling essential and cut-price goods, as will as outlets offering online retail opportunities. As said by Mark Lynch, Partner at Oghma Partners:

“While these figures highlight British stoicism in supporting a fragile economy, it is important to note that these retail sales figures might be slightly misleading in terms of giving an impression of the strength of the consumer economy as a whole. UK shoppers have been buying more food and drink at supermarkets because they have been spending less on eating out. The Government’s lockdown restrictions have re-emphasised earlier trends that we saw around Spring which showed positive sales growth for direct to consumer and supermarket companies. We have already seen a significant shift in consumer behaviour which has boosted growth for those companies in Q2 and to a lesser extent in Q3 but which now look to boost growth again in Q4.”

The problem with this positive way of thinking is that retail sales aren’t actually experiencing exponential growth, Instead, September’s growth was lower than the previous month, there appear to be challenges ahead, and the growth is not being experienced by retailers across the board.

Indeed, new lockdown restrictions will have the double-edged-sword effect. The first half of this will be a reduction in customers and potential closure of some shops. As stated by Kingswood CIO, Rupert Thompson:

“Retail sales posted an unexpectedly strong gain in September, rising 1.5% m/m to be up 4.7% from a year earlier. However, this is only encouraging up to a point as this strength was prior to the introduction of the new lockdown/social distancing measures. Business confidence fell back in October with the decline led by the services sector, the area the most vulnerable to the latest restrictions. This fall highlights the need for the new package of support measures announced by the Chancellor yesterday.”

The second consideration will be a change in consumer behaviour, with customers focusing on outlets perceived to be selling essential and cut-price goods, as will as outlets offering online retail opportunities. As said by Mark Lynch, Partner at Oghma Partners:

“While these figures highlight British stoicism in supporting a fragile economy, it is important to note that these retail sales figures might be slightly misleading in terms of giving an impression of the strength of the consumer economy as a whole. UK shoppers have been buying more food and drink at supermarkets because they have been spending less on eating out. The Government’s lockdown restrictions have re-emphasised earlier trends that we saw around Spring which showed positive sales growth for direct to consumer and supermarket companies. We have already seen a significant shift in consumer behaviour which has boosted growth for those companies in Q2 and to a lesser extent in Q3 but which now look to boost growth again in Q4.”

“We are sadly seeing more and more long term problems for Food to Go and food service providers that are unable to service clients as per normal. The fact is that more end user businesses will go bust, including pubs, restaurants and the more food service manufacturing capacity and, to a lesser extent, Food to Go capacity we will see taken out of the market.”

Plant-based meat and dairy alternatives market to hit €7.5bn in Europe by 2025

“Shifting consumer preferences combined with the increasing awareness of the role of a more plant-rich diet in tackling some of the key ecological and health consequences of our current global food system has led to the rise of plant-based alternatives, both as stand-alone businesses as well as existing businesses pivoting into this space. At Tribe, we have found a clear expansion in the number of opportunities to support this transition as an investor over the last couple of years.”

“Plant-based meat and dairy is now disrupting the food production industry in many of the same ways that renewables disrupted the energy market over the last 30 years. The annual growth rate European retail sales of meat and dairy alternatives of 10% between 2010 and 2020 though does compare favourably to the 3.3% growth in renewables in a similar period1, showing the size of the potential opportunity for investors in new food developments.”

“As this shift continues, we also have to commit to managing and reducing the impacts that such a wholesale change in agriculture can create – for example, the issues with soy production leading to deforestation is documented. Investors must be aware of the impact and sustainability issues associated with plant-based food too, if they are to identify those companies who are managing themselves for this transition sustainably. Those companies who have adopted frameworks that help them navigate the complex issues embedded in agriculture, for example the Natural Capital Protocol or the Regenerative Organic certification scheme, are better placed to manage the sustainability issues associated with this transition.”

Griffin Mining shares surge 9% on positive Q3 performance

Stock selections for 2020 year end from Zak Mir & Alan Green

US Presidential Election – where do polls stand after the final debate?

Being honest: having watched the previous exchanges, I could only bring myself to watch the second half of last night’s debate, and even then I was tempted to flick back onto a re-run of ‘Merlin’. From what we saw, Trump was as bombastic as ever, though a lot more managed in terms of delivery. Unfortunately for Biden, this meant that the incumbent POTUS looked in charge when he was speaking, and more respectful when he wasn’t. The same could not be said for Biden. with the exception of a strong closing statement, Biden seemed to have all the opportunities and facts to land decisive blows on Trump, but lacked the conviction – or the calm – to do so. Coming unstuck at some points due to Trump’s repetitive and combative style, the only thing keeping the Democrat candidate afloat last night was simply the fact that he was arguing for generically agreeable policies, and making statements that were patently true (the president, of course, never burdens himself with these kinds of constraints). Overall, it was another cringeworthy watch, with the difference from earlier bouts being that Trump looked slightly more level-headed, and at points, Biden looked lost for words. With a considerable rift opening up in polling between candidates after the first debate, the incumbent president just had to appear semi-palatable for voter sentiment to swing even slightly in his favour. And indeed, it appears to have done just that.Who won tonight’s debate?@YouGovAmerica: Biden 54% (+19) Trump 35% .@CNN: Biden 53% (+14) Trump 39%@DataProgress: Biden 52% (+11) Trump 41%

— Political Polls (@Politics_Polls) October 23, 2020

National GE: Biden 53% (+10) Trump 43% . Generic Congressional Ballot: Democrats 51% (+8) Republicans 43%@GSG/@GBAOStrategies, RV, 10/15-19https://t.co/i9Zu5wO4Jz

— Political Polls (@Politics_Polls) October 23, 2020

Now, while Biden appears to still have a considerable lead – around 9-10% in most polls – this has narrowed from polling the previous week, with most giving him a 10-12% advantage. The latter poll, giving him just a 6% lead, might be a tad drastic (and from a Trump-leaning pollster), but it does also signify the smallest advantage awarded to Biden since the 30-day election countdown began. Significantly, the 6% figure covers voter intentions, rather than electoral college votes. This matters because in terms of ECs, Trump’s voter spread gives him an advantage. Indeed, Clinton had a 5% poll lead going into the 2016 election, and 3 million (4-5%) more votes than her rival, but ended up losing by 77 college votes. With this in mind, Biden supporters mustn’t fall at the final hurdle, as any vote lead below 10% will likely be too close for comfort. As we approach election day, the narrowing margins are also reflected in swing states, even though Biden still retains a lead in most:National GE: Biden 52% (+6) Trump 46%@SurveyMonkey/@tableau/@axios, LV, 10/19-21https://t.co/XyP5kztmIf

— Political Polls (@Politics_Polls) October 23, 2020

PENNSYLVANIA Biden 51% (+7) Trump 44%@Muhlenberg/@mcall, LV, 10/13-20https://t.co/IPQTBKbwHR

— Political Polls (@Politics_Polls) October 23, 2020

MICHIGAN Biden 48% (+9) Trump 39% .#MIsen: Peters (D-inc) 45% (+6) James (R) 39%

EPIC-MRA, LV, 10/15-19https://t.co/9ujjpFrWRL — Political Polls (@Politics_Polls) October 23, 2020

Though winning in most swing states, sentiment projections in Florida seem to change depending on which poll you’re looking at. Florida and Pennsylvania are especially significant, though, with 49 ECs between them being more than enough to decide the outcome of the 2020 election. Worth noting, also, that Biden is far and away viewed as the more ‘decent’ candidate – 64% saying yes to Biden, versus 37% agreeing that Trump has decency. Also, following last night’s debate, Biden’s approval rating rose from 55% to 56%, while Trump’s fell from 42% to 41%. If none of these factors offer Biden supporters consolation about the narrowing margins, then hopefully they take some heart from The Economist’s bold predictions:FLORIDA Trump 50% (+2) Biden 48%@SurveyMonkey/@tableau/@axios, LV, 9/24-10/21https://t.co/XyP5kztmIf

— Political Polls (@Politics_Polls) October 23, 2020

Overall, though, an election is not won by polls, and as we saw in 2016, the polls can get it badly, badly wrong. The only way to see your candidate in the White House, is to go out and vote for them. An improvement on last time’s 55% voter turnout, would be a victory for US politics as a whole.#Latest @TheEconomist Forecast:

Chance of winning the electoral college: Biden 92% Trump 7% Chance of winning the most votes: Biden 99% Trump 1% Estimated electoral college votes: Biden 345 Trump 193https://t.co/6Ei5T5ogc2 — Political Polls (@Politics_Polls) October 23, 2020

InterContinental Hotels shares restless as revenues slide 53%

However, there was some room for optimism. During Q3, the company opened 82 new hotels and signed a further 14,000 rooms. This brings its total rooms opened in 2020 up to 23,000, and its total estate up to 890,000 rooms across 5,977 hotels, up 2.9% year-on-year.

Further, the company booked positive cash flow in Q3, with total liquidity at the end of September rising to £2.1 billion. It also added that it was on track to reduce its business costs by £150 million, targeting at least half of that number ‘to be sustainable into 2021’.

InterContinental Hotels dust themselves off

Coming through a tough year, company CEO, Keith Barr, discusses both the challenges and opportunities that lie ahead:Despite the challenges we’ve faced, we have continued to open new hotels and sign more into our pipeline. This is recognition of consumer preference for our brands and strong owner relationships, and also the long-term attractiveness of the markets we operate in and the relative resilience of our business model. We signed 82 hotels in the quarter, taking us to 263 year-to-date, more than a quarter of which are conversions. As we continue to invest in growth initiatives, we do so with a strict focus on cost reduction and an unwavering commitment to act responsibly for our people, guests, owners and local communities.”

“A full industry recovery will take time and uncertainty remains regarding the potential for further improvement in the short term, but we take confidence from the steps taken to protect and support our owners and drive demand back to our hotels as guests feel safe to travel. Our actions have resulted in ongoing industry outperformance in our key markets, and we remain focused on leveraging the strength of our brands, scale and market positioning to recover strongly and drive future growth.”

Investor notes

Following the news, InterContinental Hotels Group shares dipped by 2.39% or 102.00p, down to 4,161.00p a share 23/10/20 12:38 BST. This level is around 5% above analysts’ target price of 3,951.54p a share, but beneath its six-month high of 4,484.00p seen in September. Analysts currently have a ‘Hold’ stance on the company’s stock, it has a p/e ratio of 18.38, and it currently has a 66.92% ‘Underperform’ rating from the MarketBeat communityInfrastructure India shares rise on full-year results

Barclays shares surge 7% on £1.1bn profit