FTSE slips while US markets rally – a mixed bag for global equities

The FTSE 100 index (INDEXFTSE:UKX) has dipped this afternoon by 1.16%, despite being on course to record its best quarter since 2010, at the tail-end of the financial crisis.

Ongoing concerns surrounding coronavirus have weighed heavily on markets for the past few weeks, and PM Boris Johnson’s announcement of a New Deal-style spending spree has failed to stir up much of a response from the London Stock Exchange.

New figures from the Office for National Statistics (ONS) released on Tuesday revealed that the UK economy shrank even more than expected in the first quarter of 2020, contracting 2.2% between January and March, in what was the joint largest drop since 1979.

AstraZeneca shares slip despite new Japan orphan drug designation

British-Swedish pharamaceuticals company AstraZeneca (LON:AZN) saw its share price dip on Tuesday despite having announced that its selumetinib treatment had been granted orphan drug designation (ODD) in Japan, for the treatment of neurofibromatosis 1 (NF1).

The announcement comes as trials showed the treatment was effective in reducing tumour volume in paediatric patients with NF1, Today’s ODD follows approval in the US, with additional regulatory submissions underway.

AstraZeneca said that selumetinib is developed and commercialised in partnership with Merck and Co. (NYSE:MRK), and that the treatment would help those experiencing plexiform neurofibromas as a result of NF1.

Speaking on the condition, José Baselga, Executive Vice President, Oncology R&D, said:

“Neurofibromatosis type 1 can have a devastating impact on children and new medicines are urgently needed to help treat the resulting plexiform neurofibromas and associated clinical issues. Current options in most countries are limited and this designation is a significant step forward in bringing the first medicine for NF1 to paediatric patients in Japan.”

Roy Baynes, Senior Vice President and Head of Global Clinical Development, Chief Medical Officer, MSD (Merck) Research Laboratories, said on the new treatment:

“Plexiform neurofibromas are one of the key manifestations of NF1 and can lead to pain and disfigurement. In the SPRINT trial, selumetinib was shown to reduce the size of these tumours in children. We are hopeful that we will be able to bring this treatment to this underserved paediatric patient community in Japan.“

The plexiform neurofibromas tumour grows along a patient’s nerve sheaths, and can cause issues such as disfigurement, motor dysfunction, airway dysfunction, visual impairment and bowel and bladder dysfunction. The selumetinib treatment, when trialled, reduced tumour volumes by at least 20% in 66% of the NF1 patients it was tested on (33 out of 50). Today’s ODD by The Japanese Ministry of Health, Labour and Welfare means selumetinib will be added to the list of medicines used for the treatment of rare conditions. ODD is a classification designated for treatments for diseases that affect fewer than 50,000 patients in Japan, for which, AstraZeneca says, “there is a high unmet need”.Despite the seemingly positive update, AstraZeneca shares dipped by over 1.20%, before recovering slightly to a 0.99% dip, to 8,463.00p per share 30/06/20 12:34 BST. This is up frm the company’s year-long nadir of 6,221.00p in mid-March, but down from its 9,004.00p high in mid-May. The company’s p/e ratio is 102.15p, its dividend yield is modest but reliable at 2.58%.

Cineworld shares stable as reopening date postponed until July 31st

Cineworld Group plc (LON:CINE) has announced that it will postpone the reopening of its UK and US cinemas until 31st of July, citing a lack in new film releases. The company had previously stated that all of its transatlantic sites would be able to open from the 10th of July. In a company statement, Cineworld insisted that the move was “in line with recent adjustments to the schedule of upcoming movie releases”.

A number of big summer blockbusters – including Disney’s live-action remake of Mulan and upcoming Christopher Nolan flick Tenet – have been forced to push back their premiers until August in order to maximise profit. Cineworld is accordingly concerned that the delay in releases could lead to low engagement from the public, as the cinema sector prepares to relaunch with social distancing measures in place following the coronavirus pandemic.

In a previous announcement, Cineworld laid out its plans to reopen cinemas with the health and wellbeing of its customers and employees as its priority. The company emphasised its commitment to social distancing, with new film schedules to “manage queues and traffic in and around its premises” and “enhanced sanitation and cleanliness procedures” to ensure sites have minimal opportunity to spread the highly-infectious Covid-19 virus.

Earlier this year, the chain was forced to close 787 cinemas across 10 countries worldwide and company bosses relinquished salaries and bonuses to help cut costs as the business struggled through the pandemic. Cineworld had already suffered a fall in profits in 2019, leaving the company in a precarious position when lockdown measures came into force in the UK back in March. The company had been in the process of slowly chipping away at its $3.7 billion debt when it closed all of its sites in April.

A number of movies have been lined up for release later this summer when Cineworld does eventually open its doors, with titles such as A Quiet Place Part II and Antebellum. Nolan’s fan-favourite Inception is also scheduled to be re-released on IMAX.

Investor insight

Despite today’s disappointing update, Cineworld’s share price has continued its recent upward trajectory with a 4.46% or 2.56p increase to 59.88p at 12:10 BST. The chain’s dividend yield sits at 0.21% and its P/E ratio at 5.62.Smiths Group shares rally on ‘resilient’ COVID trading

FTSE-listed engineering firm Smiths Group (LON:SMIN) saw its share price bounce on Tuesday, as the company booked robust trading during the COVID pandemic.

For its continuing operations, Smiths Group said that underlying revenue for the ten months to 31 May 2020 was up 2% year-on-year. Meanwhile, reported year-to-date revenue jumped 6%, which included a 3% rise provided by the acquisition of United Flexible.

The company said that its performance over the last four months was driven by its strong order books at the start of the pandemic, and the overall momentum of first half trading. It did note, however, that there had been some slowing down, with its customers and operations impacted by COVID. It said that it was currently operating at all 75 of its plants but was not immune to higher consequential costs.

Throughout its divisions, Smiths Group stated that; John Crane still booked year-to-date revenue growth, Smiths Detection performed strongly due to delivery of original equipment programmes, Flex-Tek performs well though its aerospace and Smiths Interconnect has had its revenues impacted, though orders and revenues have both recently improved.

In addition, the company noted that Smiths Medical saw underlying revenue growth of 2% in the second half, alongside year-to-date revenue growth of 1%. While the division’s non-COVID procedures suffered, demand for critical care restocking was strong.

Further to its trading update, the company also announced that it would be undertaking a restructuring plan to maintain its strong performance after the virus, and help it to deliver its operating margin goal of 18-20%. The programme will be group-wide, with a £65 million operating cost split between FY2020 and FY2021. Smiths Group said the restructuring would substantially offset costs in FY2021 and deliver the full annualised benefit of £70 million in FY2022.

Smiths Group response

Company Chief Executive Andy Reynolds Smith commented on the results:“ Market-leading positions and a flexible business model have enabled the Group to continue to perform through crisis disruption.”

“Our immediate focus is the safety of our people and business continuity for our customers. We will continue to take the actions necessary to safeguard our long-term competitiveness. I very much regret that this will result in some job losses. My sincere personal thanks go to the amazing Smiths employees around the world for their dedication and commitment.”

“The Group has a resilient business model; market-leading positions, a culture of innovation at its heart, combined with relentless execution. We are confident that we will meet the challenges of the current crisis – and emerge stronger, better able to outperform long-term.”

Investor insights

Following the update, Smiths Group shares rallied significantly by 7.74% or 100.50p to 1,398.50p per share 30/06/20 11:59 BST. The company is still rated as a ‘Strong Buy’ or ‘Buy’ in most analysts’ eyes. The median price target is 1,450.00p a share, while its share price at the start of trading on Tuesday, was down 11.09% year-on-year. Th company has a p/e ratio of 18.98 and a dividend yield of 3.30%.Shell share price slips amid warnings of $22 billion slash to assets value

The Royal Dutch Shell PLC (LON:RDSA) share price has slipped by 2.34% just before lunchtime on Tuesday as the company warns that the historic slump in oil prices could reduce the value of its assets by as much as $22 billion.

A tumultuous few months for the oil industry look set to have a lasting long-term impact on prices, with Shell predicting the average cost per barrel to stand at just $35 over the course of 2020. The company is said to be expecting a 40% drop in sales over the second quarter – a loss of equivalent to 4 million barrels per day (bpd) – significantly more than previous estimates of 3.5 million.

Shell’s second quarter results are due to be released on the 30th of July. Oil and gas production is expected to average at 2.35 million bpd between April and June, down from 2.71 million bpd in the first quarter.

Global travel restrictions and a free-fall in consumer demand drove oil prices down to their lowest levels since 1982 in April, with the average price per barrel tumbling to just $20 at the peak of the coronavirus pandemic. Shell’s announcement sees the world’s largest fuel retailer follow in the footsteps of rival oil giant BP’s plans to slash $17.5 billion off the value of its own oil and gas assets.

Brent crude oil is currently trading at around $41 per barrel, but a full recovery is still far out of reach: the average price per barrel stood at $66 at the start of the year. It appears it will take some time before prices return to pre-crisis levels, as Shell has released its forecasted benchmark average for Brent crude to $40 and $50 for 2021 and 2022 respectively. BP (LON:BP), on the other hand, expects prices to reach a high of just $55 – and not until 2050.

On the bright side, the disruption caused by the pandemic has afforded oil companies an opportunity to restructure their business plans. BP has already announced its intentions to refocus its strategy and shift to low-carbon energy, and pressure is mounting for industry-leading Shell to implement a similar scheme. The company has made some major changes already, cutting its dividend for the first time since World War II and slashing spending by $5 billion to $20 billion for 2020.

The next quarter is still expected to be especially tough for the oil industry, with Credit Suisse (SIX:CSGN) analyst Thomas Adolff warning that Shell’s announcement should be a “wake-up call” for other oil giants.

Shell’s second quarter 2020 update note came with an upbeat comment from the company, however, which stated that “given the impact of COVID-19 and the ongoing challenging commodity price environment, Shell continues to adapt to ensure the business remains resilient”.

Investor insight

Shell’s share price has slipped by 2.34% or 31.40p to 1,308.40p at BST 11:30. The company’s dividend yield stands at 0.10% and its P/E ratio at 6.54.On the Beach reports 66pc fall in revenues

On the Beach has reported a 66% fall in revenues for the first half of the year, as demand falls amid the Coronavirus pandemic.

Due to falling demand and a surge in cancellations, pre-tax profit fell from £13.4m to £2.3m and revenues fell two thirds to £21.4m.

“On the Beach continues to successfully build a leading position as more consumers discover the ease of use and wide choice of beach holidays across our platforms,” said Simon Cooper, the group’s chief executive.

“The flexibility and asset light nature of our business model together with our recently strengthened balance sheet and the actions we have taken since the middle of March means we are well placed to capitalise on the inevitable structural changes in the market post Covid-19. As a result, the board continues to look to the future with confidence,” he added.

Bookings remain low for 2021, however remain stronger than this year so far thanks to the early release of flights next year by most airlines.

The group’s chief financial officer has resigned. Paul Meehan will step down 17 July to “pursue other business interests”.

“I have very much enjoyed my time with On the Beach and feel that now is the right time to concentrate on and pursue other business interests,” said Meehan.

“I have worked closely with Shaun since he joined the group and I believe he is well-placed to take over the CFO role and deliver on the next phase of OTB’s growth,” he added.

Shares in On the Beach (LON: OTB) are trading -2.15% (0923GMT).

Wirecard UK ban lifted, allowing customers to access cash

The Financial Conduct Authority has lifted the restrictions on Germany’s Wirecard, allowing payments to continue.

After the company collapsed last week, the FCA banned Wirecard Card Services leaving thousands of people across the UK locked out of their accounts on Friday.

The FCA said in a statement: “We have been working closely with Wirecard UK and other authorities over the last few days to ensure that the firm was able to meet certain conditions required to lift the restrictions we imposed on it.”

“We are now in a position to allow Wirecard to resume operational activity. This means customers will now, or very shortly, be able to use their cards as usual,” the FCA added.

Wirecard’s German parent company filed for insolvency amid a £1.7bn alleged accounting fraud. Markus Braun, the former boss, has been arrested after he was accused of inflating Wirecard’s finances to make them appear more attractive to investors. Braun has been bailed from police custody after posting a deposit of €5m on Tuesday.

The UK watchdog said it chose to freeze accounts in order to protect customers’ cash.

The UK operations of the company has said itis working closely with the FCA. The company said:

“There may be a delay before all card programmes are fully operational, so some customers could find themselves unable to transact immediately but we anticipate this lasting no longer than 24 hours. We apologise for the inconvenience to our valued customers that the temporary suspension caused.”

Byron Burger seeks buyer as it teeters on the brink of administration

British burger chain Byron Hamburgers Limited – also known as Byron Burger – is currently embroiled in last-ditch negotiations with buyers after its private equity owners filed a notice for bankruptcy this afternoon. The hope is that a “pre-packed” administration deal will attract bidders to buy up either the brand name or a number of the chain’s 51 restaurants nationwide.

The business is owned by private equity fund Three Hills Capital Partners, who purchased the chain back in 2017. Just three months ago, the company hired KPMG advisors to guide Byron Burger through the unprecedented pressure from the coronavirus pandemic. The chain was one of hundreds of restaurants forced to close their doors due to the government’s lockdown measures brought in at the end of March.

It appears that Byron Burger has been preparing for this news for some time now. KPMG has been trying to sell the chain since May, but so far no buyers have come forward to snap up the premium burger brand. A source close to the company stated that three potential buyers have expressed interest in buying some parts of the business, but neither Byron Burger, Three Hills Capital or KPMG have commented on the claims.

If an investor does buy part of the brand, the likelihood is that there would be significant restaurant closures and job losses. Byron Burger has not changed its decision to reopen some of its locations from mid-July onwards, but the firm is expected to be smaller. This is not the first time Byron Burger has faced financial difficulties, however, as the company brought in KPMG back in 2018 to rescue and restructure the business as it struggled against a crowded market.

With over 2,100 employees across all 51 of its sites, Byron Burger makes up part of the tsunami of private equity purchases in the restaurant sector in the early 2010s. The company has been in deep water since 2018, according to recent accounts revealing a pre-tax loss of £47.2 million across the year.

A combination of sky-rocketing rent rates and a bustling high street restaurant market left Byron Burger in a weak position even before the pandemic made its mark. Now, with the majority of its employees on furlough and not expected to be reinstated once the company’s doors open to customers again next month, Byron Burger is nestled in an especially precarious spot.

Nevertheless, the chain and its owners are said to be optimistic that a “pre-packed administration deal” can be reached with a buyer before its July opening date. Oliver Kolodseike, associate research director at property consultants Colliers International, argued on the contrary that the outlook for the restaurant sector as a whole remains decidedly grim:

“With restrictions on table covers and customers opting for takeaways over sit-down meals surrounded by Plexiglas screens, it remains to be seen as to whether restaurants in the UK will even be profitable under social distancing regulations once their doors are allowed to reopen”.

Chesapeake Energy share price plummets as company files for administration

Shale gas drilling powerhouse Chesapeake Energy Corporation (NYSE:CHK) has filed for bankruptcy, sending its share price down 7%. The Oklahoma-based fracking pioneer has racked up debts of $9 billion as well as a notorious reputation for its negative environmental impact – the company is ranked the 90th most polluting business in the world.

Chesapeake has no doubt fallen victim to the record plunge in oil prices, following the paralysing impact of the coronavirus pandemic on the energy industry. The company was first reported by Reuters to have sought out debt advisors in March, but months of negotiations with creditors were unable to offset Chesapeake’s hefty dues.

Current CEO Doug Lawlor inherited a notably worse $13 billion debt when he came to the helm back in 2013, using widespread spending cuts and asset sales to help reduce the company’s debt as far as possible. However, this year’s historic free-fall in oil prices was the nail in the coffin for the struggling business.

Chesapeake was co-founded by Aubrey McClendon, an outspoken and prominent advocate for shale drilling, who curiously died in 2016 in a violent car crash in Oklahoma while facing a federal probe into bid-rigging. McClendon had overseen Chesapeake grow from a outlying wildcatter to a top US producer of natural gas. It is still the sixth-largest producer by volume in the country.

Remarking on Chesapeake’s announcement, Lawlor stated: “Despite having removed over $20bn of leverage and financial commitments, we believe this restructuring is necessary for the long-term success and value creation of the business”.

Just last year, Lawlor made a $4 billion concerted effort to cut back on Chesapeake’s reliance on natural gas reserves. Its shares suffered heavily for the decision, and the value of the company’s oil and gas holdings have already sank by $700 million this quarter.

Chesapeake shares have dropped more than 90% this year making them one of the biggest causalities of the demand destruction caused by coronavirus.

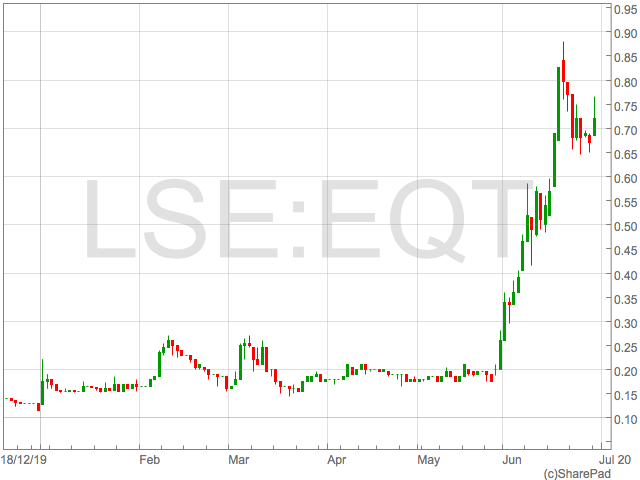

EQTEC shares surge on JV announcement, up over 500% in 2020

EQTEC shares (LON:EQT) surged on Monday as the waste technology and gasification company announced an agreement to distribute green energy solutions in Ireland.

The deal involves a partnership with the Carbon Sole Group for a number of projects including biogas, waste-to-energy and district heating.

The projects will utilise EQTEC’s Gasifier Technology whilst Carbon Sole will lead the development of the business.

EQTEC shares rose as much as 12% on the news meaning shares in the green technology company are now up over 520% in 2020.

The rise has been driven by a series of similar announcements demonstrating EQTEC’s expansion of it’s joint venture model in a wide range of clean energy projects.

“Developing partnerships with high quality and established stakeholders in our target markets has been a key focus of EQTEC since I joined the company,” said David Palumbo, CEO of EQTEC.

“We are particularly excited about this collaboration agreement with Carbon Sole as we rarely find a developer with such a great understanding of the sector matched with a thorough understanding of the energy needs of the towns and available resources in which the projects are to be vested.”

“Carbon Sole have made numerous public sector presentations and submissions towards the decarbonisation of gateway towns and regions, including actively participating in public sector stakeholder steering groups and workshops in respect of Renewable Supports and Climate Action Funding.”

“Carbon Sole have been advising both public and industrial sectors in Ireland on the decarbonisation of industrial processes and energy transition for a number of years. We enter this partnership very confident that it will evolve beyond the current three projects under development.”

“Ireland is a very interesting market for us, offering numerous opportunities, particularly given its unique characteristic of being now the only EU state in the islands of the North Atlantic. It is also the location of our corporate headquarters and we intend to be a significant player in the decarbonisation process of its industries.”

“Developing partnerships with high quality and established stakeholders in our target markets has been a key focus of EQTEC since I joined the company,” said David Palumbo, CEO of EQTEC.

“We are particularly excited about this collaboration agreement with Carbon Sole as we rarely find a developer with such a great understanding of the sector matched with a thorough understanding of the energy needs of the towns and available resources in which the projects are to be vested.”

“Carbon Sole have made numerous public sector presentations and submissions towards the decarbonisation of gateway towns and regions, including actively participating in public sector stakeholder steering groups and workshops in respect of Renewable Supports and Climate Action Funding.”

“Carbon Sole have been advising both public and industrial sectors in Ireland on the decarbonisation of industrial processes and energy transition for a number of years. We enter this partnership very confident that it will evolve beyond the current three projects under development.”

“Ireland is a very interesting market for us, offering numerous opportunities, particularly given its unique characteristic of being now the only EU state in the islands of the North Atlantic. It is also the location of our corporate headquarters and we intend to be a significant player in the decarbonisation process of its industries.”

“Developing partnerships with high quality and established stakeholders in our target markets has been a key focus of EQTEC since I joined the company,” said David Palumbo, CEO of EQTEC.

“We are particularly excited about this collaboration agreement with Carbon Sole as we rarely find a developer with such a great understanding of the sector matched with a thorough understanding of the energy needs of the towns and available resources in which the projects are to be vested.”

“Carbon Sole have made numerous public sector presentations and submissions towards the decarbonisation of gateway towns and regions, including actively participating in public sector stakeholder steering groups and workshops in respect of Renewable Supports and Climate Action Funding.”

“Carbon Sole have been advising both public and industrial sectors in Ireland on the decarbonisation of industrial processes and energy transition for a number of years. We enter this partnership very confident that it will evolve beyond the current three projects under development.”

“Ireland is a very interesting market for us, offering numerous opportunities, particularly given its unique characteristic of being now the only EU state in the islands of the North Atlantic. It is also the location of our corporate headquarters and we intend to be a significant player in the decarbonisation process of its industries.”

“Developing partnerships with high quality and established stakeholders in our target markets has been a key focus of EQTEC since I joined the company,” said David Palumbo, CEO of EQTEC.

“We are particularly excited about this collaboration agreement with Carbon Sole as we rarely find a developer with such a great understanding of the sector matched with a thorough understanding of the energy needs of the towns and available resources in which the projects are to be vested.”

“Carbon Sole have made numerous public sector presentations and submissions towards the decarbonisation of gateway towns and regions, including actively participating in public sector stakeholder steering groups and workshops in respect of Renewable Supports and Climate Action Funding.”

“Carbon Sole have been advising both public and industrial sectors in Ireland on the decarbonisation of industrial processes and energy transition for a number of years. We enter this partnership very confident that it will evolve beyond the current three projects under development.”

“Ireland is a very interesting market for us, offering numerous opportunities, particularly given its unique characteristic of being now the only EU state in the islands of the North Atlantic. It is also the location of our corporate headquarters and we intend to be a significant player in the decarbonisation process of its industries.”